Solar Backsheet Market Report Scope & Overview:

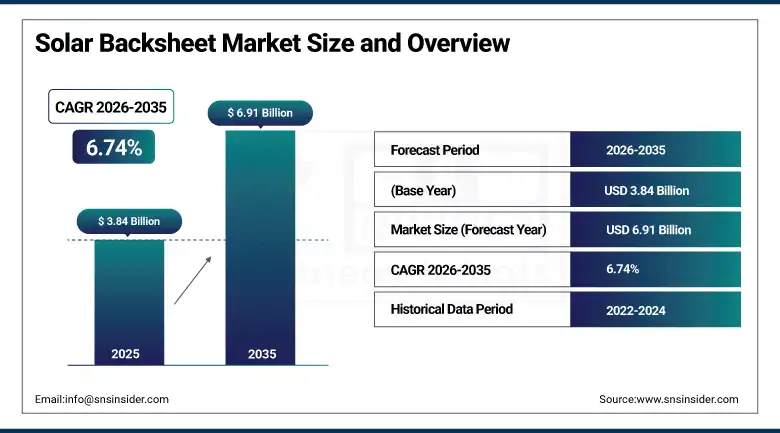

The Solar Backsheet Market was valued at USD 3.84 Billion in 2025 and is expected to reach USD 6.91 Billion by 2035, growing at a CAGR of 6.74% from 2026 to 2035.

The solar backsheet market is experiencing stable growth across the globe owing to the growing solar PV installations, increasing investments in renewable energy infrastructure, and the rising demand for robust photovoltaic module protection materials used in the utility-scale and distributed solar ecosystems across the globe. Solar manufacturers are increasingly adopting fluoropolymer and advanced multilayer backsheet technologies to improve electrical insulation, UV resistance, moisture protection and long-term durability of modules in harsh environmental conditions around the globe. Increasing adoption of bifacial solar modules and high-efficiency PV systems are further accelerating commercialisation opportunities across advanced solar material ecosystems worldwide. In 2025, the world produced more than 780 GW of solar PV modules, and the Asia Pacific, Europe and North America continued to see growth in investment in renewable energy manufacturing.

In 2025, DuPont continued to scale advanced manufacturing of Tedlar-based solar backsheets and high-durability photovoltaic protection technologies to support the growing deployment of utility-scale and high-efficiency solar modules globally. The increasing adoption of weather-resistant multilayer polymer structures and recyclable photovoltaic protection materials also drives the long-term growth of the market globally. Global investments in solar manufacturing infrastructure surpassed USD 510 Billion during 2025. Governments and solar developers have increasingly adopted advanced photovoltaic protection materials that support long-term renewable energy commercialisation ecosystems across the globe.

Market Size and Forecast

-

Market Size in 2026E: USD 4.10 Billion

-

Market Size by 2035: USD 6.91 Billion

-

CAGR: 6.74% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Solar Backsheet Market - Request Free Sample Report

Solar Backsheet Market Trends

-

Rising deployment of high-efficiency solar PV modules is increasing demand for advanced weather-resistant and UV-stable solar backsheet materials globally.

-

Solar manufacturers are increasingly adopting fluoropolymer-based backsheets to improve module durability, electrical insulation, and long-term operational performance across utility-scale solar projects.

-

Growing investments in bifacial solar modules are accelerating adoption of transparent and high-reflectivity backsheet technologies supporting improved photovoltaic efficiency worldwide.

-

Increasing focus on recyclable and environmentally sustainable photovoltaic materials is driving innovation in non-fluoropolymer and eco-friendly solar backsheet manufacturing ecosystems globally.

-

Solar module manufacturers are increasingly investing in multilayer polymer technologies and advanced coating systems supporting improved moisture resistance and long-term solar module reliability worldwide.

The U.S. Solar Backsheet Market Outlook

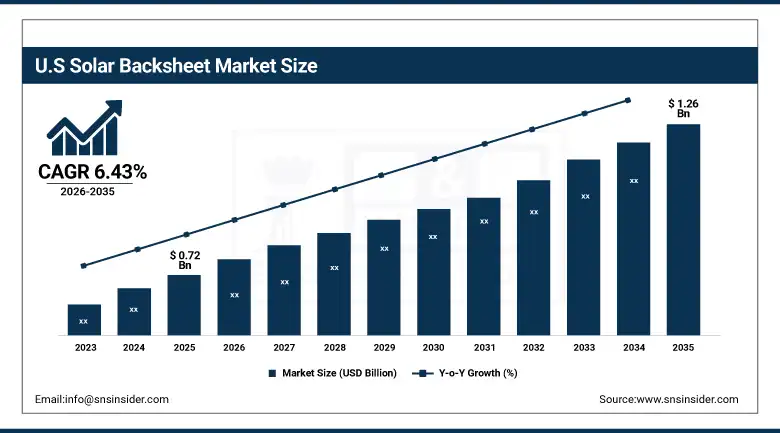

The U.S. Solar Backsheet Market was valued at approximately USD 0.72 Billion in 2025 and is expected to reach approximately USD 1.26 Billion by 2035, growing at a CAGR of approximately 6.43% from 2026 to 2035.

The US solar backsheet market continues to grow due to the rise of utility-scale solar installation projects, rising investment in US-based solar panel manufacturing activities, and high demand for highly protective photovoltaic modules. Solar module manufacturers and renewable energy companies have been observed to use fluoropolymer and multilayer polymer backsheet technology on photovoltaic panels which provide better UV resistance and electrical insulation. In 2025, the US installed more than 58 GW of solar power with faster investments in local photovoltaic panel manufacturing and growth of the renewable energy sector.

In March 2025, Cybrid Technologies expanded advanced fluoropolymer-free photovoltaic backsheet manufacturing and high-weather-resistance solar protection materials supporting utility-scale renewable energy deployments across the United States. In addition, First Solar enhanced integrated solar manufacturing and deployment of high-performance photovoltaic material to support next-generation solar module efficiency across the country. During 2025, the United States accounted for over USD 74 Billion investments into solar manufacturing and renewable energy infrastructure. Deployment of high-efficiency solar modules and advanced photovoltaic protection materials further continued to support long-term commercialisation opportunities within the national solar backsheet market.

Solar Backsheet Market Segment Analysis

-

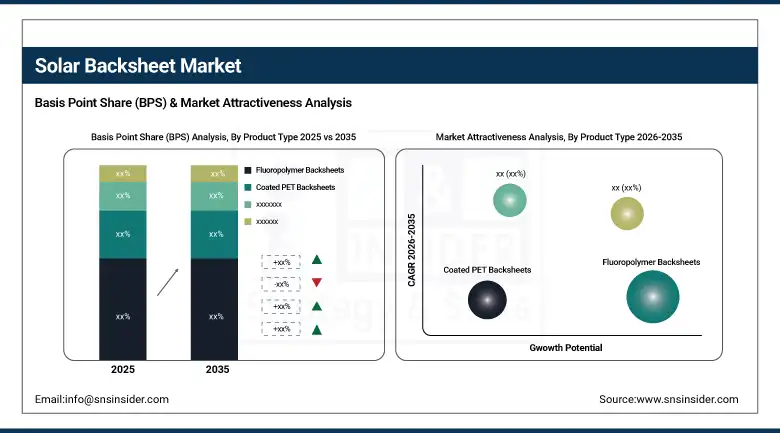

By Product Type, fluoropolymer backsheets dominated the solar backsheet market with 51.00% share in 2025, while non-fluoropolymer backsheets are the fastest growing product type with the highest CAGR from 2026 to 2035.

-

By Installation Type, ground-mounted solar systems dominated the solar backsheet market with 56.00% share in 2025, while floating solar systems are the fastest growing installation type with the highest CAGR from 2026 to 2035.

-

By Thickness Type, 100–500micron backsheets dominated the solar backsheet market with 47.00% share in 2025, while above 500micron backsheets are the fastest growing thickness type with the highest CAGR from 2026 to 2035.

-

By Application, utility-scale solar projects dominated the solar backsheet market with 58.00% share in 2025, while residential solar installations are the fastest growing application with the highest CAGR from 2026 to 2035.

-

By End User, utility providers dominated the solar backsheet market with 55.00% share in 2025, while the residential sector is the fastest growing end-user segment with the highest CAGR from 2026 to 2035.

By Product Type, fluoropolymer backsheets dominate, non-fluoropolymer backsheets grow fastest

Fluoropolymer backsheets dominated the market and gained a share of approximately 51% in the total revenue share due to excellent weather durability, UV resistance, and long-term electrical insulation properties for utility-scale and rooftop solar projects across the globe in 2025.Globally, the solar module manufacturers were increasingly using photovoltaic protection materials based on fluoropolymer that support better operational stability and longer module life under harsh environmental conditions. The commercialisation opportunities across advanced fluoropolymer photovoltaic ecosystems globally accelerated further with increasing deployment of high-efficiency solar PV systems and utility-scale renewable energy infrastructure.

Non-fluoropolymer backsheet is expected to witness the fastest CAGR during the forecast period. The growth is attributed to the increasing demand for environmentally sustainable and recyclable photovoltaic protection materials across the globe. The solar manufacturers are transitioning to fluorine-free multilayer structures to enable lower production costs, sustainability targets and increased manufacturing flexibility in next-generation solar module ecosystems around the world.

By Installation Type, ground-mounted solar systems dominate, floating solar systems grow fastest

Ground-mounted solar systems dominated the solar backsheet market, accounting for roughly 56% of the revenue share. This was due to the growing number of utility-scale renewable energy projects and the increasing installation of large solar farms globally. Advanced weather-resistant photovoltaic protection materials were increasingly adopted by renewable energy developers, allowing high efficiency energy generation and stable long term operation across utility scale installations across the globe. Rising investments in grid-scale solar infrastructure further strengthened the commercialisation opportunities across advanced photovoltaic material ecosystems worldwide.

Floating solar systems are expected to register the fastest CAGR due to increasing deployment of water-based renewable energy projects and growing focus on land-efficient solar power generation across the globe. Further increased investments in reservoir-based solar projects and advanced moisture-resistant photovoltaic technologies accelerated the commercialisation opportunities for floating solar ecosystems globally.

By Thickness Type, 100–500 microns dominate, above 500 microns grow fastest

100-500 micron backsheets dominated the solar backsheet market in 2025 and accounted for around 47% of total revenue share on account of strong balance between durability, flexibility and cost-efficiency across utility-scale and rooftop solar installations globally. Solar module manufacturers have increasingly used medium thickness multilayer backsheet structures to improve electrical insulation, UV stability and long-term photovoltaic reliability under different climatic conditions worldwide. The increasing installation of utility-scale solar projects and bifacial photovoltaic modules also drove the commercialisation opportunities for advanced medium-thickness photovoltaic protection materials worldwide.

Backsheets above 500 micron are projected to register the fastest CAGR over the forecast period owing to increasing demand for high-durability photovoltaic protection materials for harsh environmental and utility-scale solar applications worldwide. The increasing adoption of large-scale renewable energy projects in desert, coastal and high-temperature environments continued to accelerate commercialisation opportunities for thick multilayer photovoltaic backsheet ecosystems worldwide.

By Application, utility-scale solar projects dominate, residential solar installations grow fastest

Utility-scale solar projects dominated the solar backsheet market in 2025 and held a revenue share of around 58% of the overall market on account of rising investments in renewable energy infrastructure and increasing deployment of large-scale photovoltaic installations across the globe. Globally, governments and energy developers continued to expand solar parks and grid-scale renewable energy ecosystems to support long-term commercialisation of clean energy. The demand for long-lasting photovoltaic protective materials and high-performance solar module technologies is growing, which further boosted the market expansion across the world. Global utility-scale renewable energy investments in 2025 exceeded USD 310 Billion, driving long-term commercialisation opportunities across the photovoltaic material ecosystems globally.

The residential solar segment is projected to register the fastest CAGR over the forecast period owing to the increasing adoption of rooftop solar, rising electricity prices, and growing consumer focus on distributed renewable energy generation across the globe. Long-term photovoltaic commercialisation opportunities continued to be supported worldwide by expanding rooftop solar financing programmes and residential clean energy incentives.

By End User, utility providers dominate, residential sector grows fastest

Utility providers dominated the solar backsheet market in 2025 and accounted for approximately 55% revenue share due to increasing deployment of utility-scale solar projects and rising renewable energy capacity expansion across the globe. The worldwide adoption of advanced photovoltaic protection materials and weather-resistant solar module technologies supporting high-efficiency power generation and long-term operational reliability by energy providers increasingly occurred. Rising government decarbonisation targets and clean energy transition initiatives further reinforced the commercialisation opportunities across utility-scale photovoltaic ecosystems globally.

The residential sector is projected to witness the fastest CAGR due to rising deployment of rooftop solar and increasing adoption of distributed renewable energy systems globally. Growing consumer awareness of clean energy generation and expanding residential solar financing ecosystems continued to accelerate long-term market expansion globally.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

57.34% |

|

North America |

United States |

82.16% |

|

Europe |

Germany |

31.42% |

|

Middle East & Africa |

Saudi Arabia |

24.87% |

|

Latin America |

Brazil |

46.18% |

North America Solar Backsheet Market Insights

North America solar backsheet market held nearly 27.6% of the global revenue share, spurred by increasing installation trends in utility-scale projects, substantial investments in solar manufacturing facilities across the region, and deployment of advanced photovoltaic backsheet protective material in the US and Canada. North America solar power infrastructure investments in 2025 were estimated to cross USD 118 Billion with First Solar ramping up its integrated photovoltaic manufacturing capacity for commercialisation of efficient solar modules at the global level.

Europe Solar Backsheet Market Insights

Europe held around 22.9% share of the global solar backsheet market revenues in 2025 on account of aggressive decarbonisation targets, surging rooftop solar installations, and growing demand for recyclable photovoltaic protection materials in countries such as Germany, France, Italy, Spain, and the United Kingdom. Solar manufacturers enhanced regional adoption of environmentally sustainable multilayer backsheet structures and high-durability photovoltaic protection technologies supporting distributed renewable energy ecosystems. In 2025, Europe’s investments in renewable energy infrastructure exceeded USD 92 billion. Coveme has supported the commercialisation ecosystems for advanced photovoltaic backsheets and solar materials that underpin next-generation renewable energy infrastructure worldwide.

Growing acceptance of distributed solar power and smart renewable energy infrastructure is contributing to the growth of markets in Europe in the long run. Germany continued its dominance in rooftop solar and photovoltaics innovations, while Spain rapidly increased its capacity to build renewable energy infrastructure.

Asia Pacific Solar Backsheet Market Insights

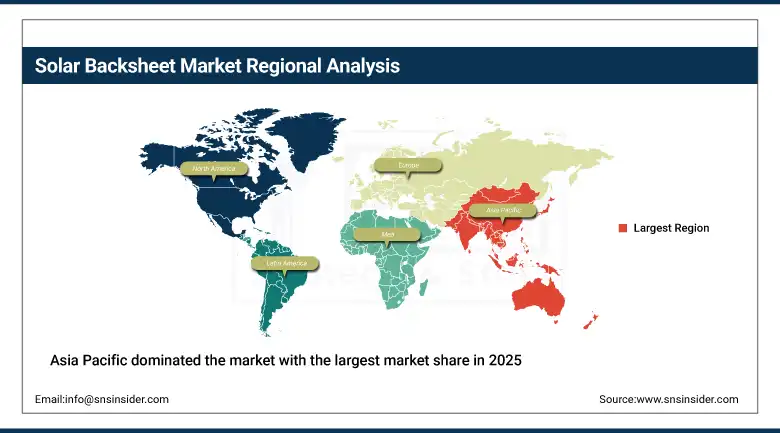

Asia Pacific dominated the market with the largest market share in 2025 and is expected to continue its dominance in the global solar backsheet market during the forecast period owing to presence of large-scale solar module manufacturing capacity, surging photovoltaic installations, and increasing renewable energy infrastructure in China, India, Japan, and South Korea. Solar manufacturers increasingly adopted advanced fluoropolymer and multilayer photovoltaic protection materials enabling long-term module durability and high-efficiency energy generation within utility-scale and distributed solar ecosystems regionally. In 2025, the Asia Pacific region invested over USD 260 Billion in solar manufacturing, while Cybrid Technologies reinforced advanced photovoltaic backsheet production ecosystems to support the commercialisation of next-generation solar modules worldwide.

Long-term market growth in Asia Pacific is being bolstered by increasing adoption of bifacial solar modules and higher government renewable energy targets. China was the leader in photovoltaic manufacturing and the deployment of utility-scale solar infrastructure, while India increased investments in rooftop solar and domestic solar manufacturing in 2025.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Solar Backsheet Market Insights

Middle East & Africa and Latin America collectively added up to an approximate 8.3% share in the revenue of the global photovoltaic solar backsheet market by 2025, driven by the increased renewable energy investments, utility-scale solar infrastructure, and expansion of the photovoltaic manufacturing infrastructure in countries like Brazil, Saudi Arabia, UAE, South Africa, and Argentina. Renewable energy companies started using weather-resistant and moisture-proof photovoltaic backsheet material for large scale solar energy farm installations. In 2025, the region invested more than USD 54 Billion in solar energy infrastructure, while Jolywood focused on the commercialisation of photovoltaic high-performance materials to support utility-scale renewable energy projects.

Brazil’s solar infrastructure development continued to be robust in Latin America in 2025, with Saudi Arabia ramping up investments in renewable energy projects. Solar farm installations and widespread use of renewable energy sources helped further develop the photovoltaic backsheet material market in emerging regions across the globe.

Market Dynamics

Growth Drivers: Rising global solar installations and high-efficiency PV module adoption

The surge in the deployment of utility-scale solar projects coupled with the rise in the investments in renewable energy infrastructure is propelling the growth of the global solar backsheet market. Solar module manufacturers are increasingly adopting advanced fluoropolymer and multilayer photovoltaic protection materials that facilitate enhanced UV resistance, electrical insulation and long-term module durability across harsh operating environments globally. The increasing penetration of bifacial solar modules and high-efficiency photovoltaic systems is also further driving commercialisation opportunities across advanced solar protection material ecosystems worldwide. Global solar PV installations surpassed 620 GW in 2025, while renewable energy infrastructure investments continued to grow rapidly across Asia Pacific, Europe and North America worldwide.

Restraints: Raw material price volatility and photovoltaic recycling challenges

The global solar backsheet market is facing operational headwinds from volatile polymer and fluorochemical raw material prices as well as rising photovoltaic recycling challenges. Worldwide, solar material producers are facing increasing costs in the production of advanced fluoropolymers, multilayer coating technologies and high performance photovoltaic protection systems. In addition, growing environmental concerns related to the disposal and recycling of fluorinated photovoltaic materials are leading to regulatory and operational complexities for renewable energy ecosystems worldwide. Global photovoltaic material costs grew more than 9% in 2025, with sustainability compliance requirements continuing to impact solar manufacturing operations worldwide.

Opportunities: Expansion of recyclable photovoltaic materials and bifacial solar ecosystems

The global solar backsheet market is witnessing a rise in the use of recyclable photovoltaic materials and the implementation of bifacial solar technologies, which are opening up lucrative commercialisation opportunities. Around the world, solar manufacturers are investing more in fluorine-free multilayer structures, transparent photovoltaic protection materials and advanced weather-resistant coating technologies to support next-generation solar module efficiency. Further strengthening long-term market expansion opportunities globally are greater investments in sustainable solar manufacturing ecosystems and smart renewable energy infrastructure. The global bifacial solar modules deployment crossed 180 GW in 2025 and the increasing demand for sustainable photovoltaic protection technologies has driven the commercialisation of advanced solar material ecosystems across the globe.

Recent Developments:

-

2026: Cybrid Technologies introduced advanced fluoropolymer-free photovoltaic backsheet solutions with enhanced UV resistance and recyclable multilayer structures supporting next-generation sustainable solar module manufacturing globally.

-

2026: Coveme expanded high-performance photovoltaic backsheet manufacturing capacity across Europe and Asia Pacific supporting rising demand for bifacial solar modules and utility-scale renewable energy projects.

-

2025: Jolywood launched upgraded transparent backsheet technologies optimized for bifacial photovoltaic systems and high-efficiency utility-scale solar infrastructure deployments globally.

-

2025: DuPont expanded advanced Tedlar photovoltaic protection materials with enhanced moisture resistance and long-term durability targeting large-scale solar power projects across North America and the Middle East.

Solar Backsheet Market Key Players are:

-

DuPont de Nemours Inc

-

Coveme S.p.A

-

Cybrid Technologies Inc.

-

Jolywood (Suzhou) Sunwatt Co. Ltd

-

Hangzhou First Applied Material Co. Ltd.

-

Krempel GmbH

-

Vishakha Renewables Pvt. Ltd.

-

Arkema S.A

-

3M Company

-

Toray Industries Inc.

-

Toyo Aluminium K.K.

-

Endurans Solar

-

Isovolta AG

-

Dunmore Corporation

-

Taiflex Scientific Co. Ltd

-

Madico Inc

-

Mitsubishi Chemical Corporation

-

Saint-Gobain S.A

-

Polyplex Corporation Ltd

-

Jiangsu Zhonglai Photovoltaic New Material Co. Ltd

Solar Backsheet Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.84 Billion |

| Market Size by 2035 | USD 6.91 Billion |

| CAGR | CAGR of 6.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Fluoropolymer Backsheets, Non-Fluoropolymer Backsheets, Coated PET Backsheets) • By Installation Type (Roof-Mounted Solar Systems, Ground-Mounted Solar Systems, Floating Solar Systems) • By Thickness Type (Below 100 Microns, 100–500 Microns, Above 500 Microns) • By Application (Utility-Scale Solar Projects, Commercial Solar Installations, Residential Solar Installations) • By End User (Utility Providers, Commercial & Industrial Sector, Residential Sector) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DuPont de Nemours Inc., Coveme S.p.A., Cybrid Technologies Inc., Jolywood (Suzhou) Sunwatt Co. Ltd., Hangzhou First Applied Material Co. Ltd., Krempel GmbH, Vishakha Renewables Pvt. Ltd., Arkema S.A., 3M Company, Toray Industries Inc., Toyo Aluminium K.K., Endurans Solar, Isovolta AG, Dunmore Corporation, Taiflex Scientific Co. Ltd., Madico Inc., Mitsubishi Chemical Corporation, Saint-Gobain S.A., Polyplex Corporation Ltd., Jiangsu Zhonglai Photovoltaic New Material Co. Ltd. |

Frequently Asked Questions

The Solar Backsheet Market is expected to grow at a CAGR of 6.74% during the forecast period.

The Solar Backsheet Market was valued at approximately USD 3.84 Billion in 2025.

Increasing solar PV installations, rising deployment of bifacial solar modules, and growing demand for durable photovoltaic protection materials are major factors driving market growth globally.

Fluoropolymer backsheets dominated the market in 2025 due to superior UV resistance, moisture protection, and long-term photovoltaic durability across utility-scale solar projects globally.

Asia Pacific dominated the Solar Backsheet Market in 2025 due to extensive solar module manufacturing capacity, rising renewable energy investments, and expanding photovoltaic infrastructure across China and India.

Get in Touch