Standalone 5G Network Market Report Scope & Overview:

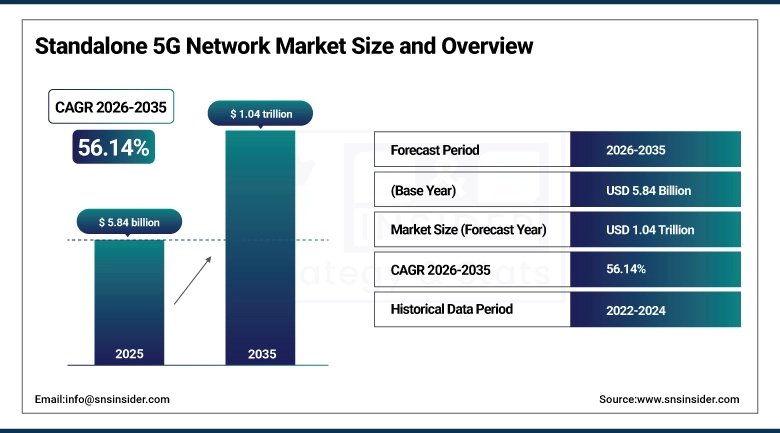

The Standalone 5G Network Market was valued at USD 5.84 billion in 2025 and is expected to reach USD 1.04 trillion by 2035, growing at a CAGR of 56.14% from 2026-2035.

The Standalone 5G Network Market is expanding owing to the growing need for ultra-low latency connections, massive Internet of Things (IoT) implementations, and sophisticated enterprise solutions. Investment growth in private 5G networks, intelligent manufacturing, autonomous technologies, and edge computing is fueling the adoption rate. The telecommunication industry is upgrading its infrastructure to facilitate faster, more dependable, and entirely cloud-native 5G network services worldwide.

The GSMA's 5G Standalone Report 2024 documents that 36 operators across 25 countries had commercially launched SA 5G networks as of July 2023, with an additional 72 operators in active SA 5G deployment or testing demonstrating accelerating adoption that is moving SA 5G from a pioneering technology to mainstream network evolution.

Standalone 5G Network Market Size and Forecast

-

Market Size in 2025: USD 5.84 Billion

-

Market Size by 2035: USD 1.04 Trillion

-

CAGR: 56.14% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Standalone 5G Network Market - Request Free Sample Report

Standalone 5G Network Market Trends

-

Cloud-native 5G core development where SA 5G core network functions are deployed as containerized microservices on cloud infrastructure rather than proprietary hardware is enabling the dynamic scaling, continuous software update, and multi-vendor interoperability that traditional hardware-based network architectures cannot achieve.

-

Network slicing commercialization is advancing beyond technical feasibility trials to commercial B2B product offerings where enterprise customers purchase dedicated slice capacity with guaranteed bandwidth, latency, and security isolation parameters creating the enterprise connectivity service revenue that justifies SA 5G investment economics above NSA alternatives.

-

Private SA 5G network adoption is accelerating in manufacturing, mining, and logistics environments where the latency, security, and reliability guarantee of private dedicated network infrastructure outperform shared public network performance for mission-critical industrial applications.

-

Open RAN integration with SA 5G core is creating vendor-diverse SA 5G deployment architectures where radio access hardware and software are sourced from different vendors through standardized O-RAN interfaces reducing equipment cost and vendor dependency while enabling innovation at each architectural layer independently.

-

SA 5G integration with edge computing platforms where MEC (Multi-access Edge Computing) infrastructure is co-located with SA 5G radio sites — is enabling the ultra-low-latency edge application delivery that SA 5G's URLLC capability makes technically feasible for the first time.

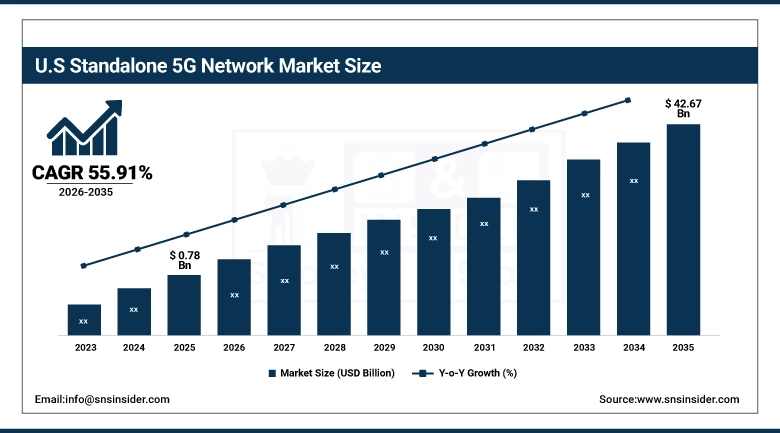

U.S. Standalone 5G Network Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 42.67 billion by 2035, growing at a CAGR of 55.91% from 2026-2035.

The U.S. Standalone 5G Network Market is expanding owing to growing private 5G network deployments, surging low-latency enterprise connectivity needs, and fast-growing IoT implementations. Growing telecom investments, edge computing implementation, and smart manufacturing initiatives are driving standalone 5G infrastructure growth across industries in the country.

T-Mobile's 2024 annual report documents that its SA 5G network covered 210 million people in the United States the world's most extensive commercial SA 5G coverage deployment by population reach with network slicing services commercially available to enterprise customers across 34 metropolitan areas.

Standalone 5G Network Market Segment Analysis

-

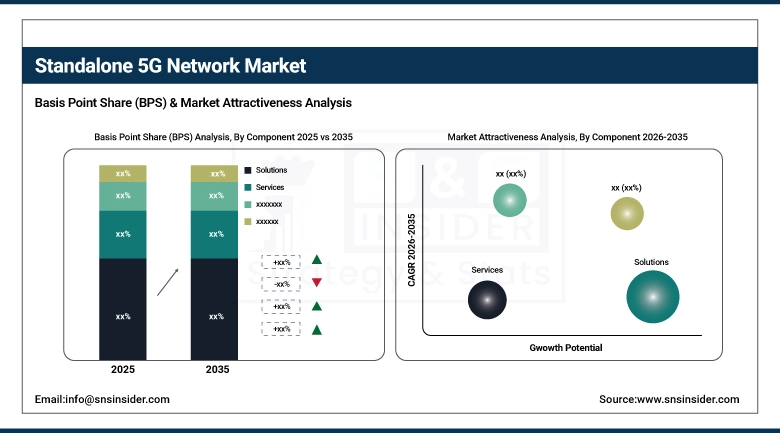

By Component, Solutions dominated with ~83% share in 2025; Services growing at fastest CAGR.

-

By Spectrum, Sub-6 GHz dominated the market in 2025; mmWave growing fastest CAGR.

-

By Network, Public dominated with ~68% share in 2025 and also growing at fastest CAGR.

-

By End Use, Manufacturing dominant; Automotive & Transportation growing at fastest CAGR.

By Component: Solutions dominate at 83%, Services growing fastest

Solutions held approximately 83% of the Standalone 5G Network Market in 2025, encompassing the hardware, software, and integrated technology stack that constitutes SA 5G network infrastructure: 5G core network software (AMF, SMF, UPF, and other core network functions), radio access network equipment, edge computing infrastructure, and network management platforms. The solutions segment's dominance reflects the capital-intensive nature of SA 5G deployment where telecom operators and enterprise private network customers invest billions in core network software licenses, radio equipment procurement, and site construction that constitute the infrastructure investment component of SA 5G deployment. Cloud-native 5G core software from vendors including Ericsson (Cloud Packet Core), Nokia (AirGile Cloud Native Core), and Mavenir (cloud-native open 5G core) — represents the highest-value software component of SA 5G solutions whose annual subscription or perpetual license pricing sustains solutions segment revenue dominance.

Services are growing at the fastest CAGR, driven by the implementation, integration, and managed service complexity that SA 5G deployment creates complexity that is substantially greater than NSA 5G deployment's simpler overlay on existing 4G infrastructure. SA 5G deployment requires cloud-native core network orchestration expertise, Open RAN component integration, network slicing architecture design, and enterprise customer onboarding for slice services each requiring specialized professional services that operator network engineering teams and enterprise IT organizations typically source externally. Consulting, implementation, integration, support, and training services collectively create a growing services revenue stream that scales with SA 5G deployment acceleration.

By Spectrum: Sub-6 GHz dominates, mmWave fastest CAGR

Sub-6 GHz spectrum held the dominant SA 5G market position in 2025, reflecting its favorable coverage-capacity balance that makes it the primary spectrum for wide-area SA 5G deployment. Low-band sub-6 GHz (600-900 MHz) provides nationwide coverage through deep indoor penetration and extended range that mmWave's centimeter waves cannot achieve. Mid-band sub-6 GHz (2.5-4.2 GHz) provides the capacity-coverage balance that operators use for urban and suburban SA 5G deployment delivering substantially higher throughput than low-band while maintaining the coverage that population-dense areas require from a limited number of base station sites. The majority of commercial SA 5G deployments globally use sub-6 GHz spectrum as the primary coverage layer, sustaining this spectrum band's market dominance.

mmWave spectrum (24-100 GHz) is growing at the fastest SA 5G CAGR, driven by the ultra-high-bandwidth applications augmented and virtual reality, fixed wireless access in dense buildings, industrial automation with high-bandwidth sensor data that require the multi-Gbps throughput that mmWave delivers. mmWave's limitations shorter range, reduced building penetration, and sensitivity to rain and humidity restrict its deployment to dense urban outdoor hotspots, indoor enterprise environments, and fixed wireless access scenarios. As SA 5G deployment matures and operators complement wide-area sub-6 GHz coverage with mmWave capacity layers in the highest-traffic locations, mmWave adoption is growing at accelerating rates.

By End Use: Manufacturing dominant, Automotive fastest

Manufacturing held the dominant SA 5G end-use position, reflecting the industrial IoT applications machine-to-machine communication, automated quality control, robotic coordination, and real-time equipment monitoring whose requirements SA 5G's URLLC and network slicing capabilities serve uniquely. Smart factory deployments using private SA 5G networks where 5G connectivity replaces the mix of Wi-Fi, wired Ethernet, and legacy wireless systems that complicate industrial IoT deployments are being demonstrated at manufacturing facilities including BMW's Leipzig plant, Bosch's manufacturing facilities, and numerous semiconductor fabs where SA 5G provides the deterministic communication that precision manufacturing control requires. Automotive and Transportation is expected to register the fastest end-use CAGR, driven by C-V2X (Cellular Vehicle-to-Everything) communication where SA 5G's URLLC enables the sub-10ms vehicle communication latency that collision avoidance, traffic signal integration, and eventually autonomous driving applications require.

Standalone 5G Network Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

45% |

|

North America |

United States |

88% |

|

Europe |

Germany |

26% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

48% |

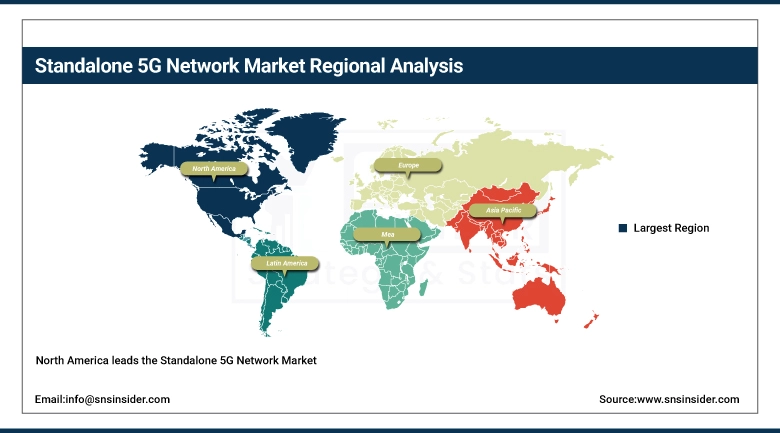

North America SA 5G Market Insights

North America leads the Standalone 5G Network Market, anchored by the United States' competitive carrier SA 5G deployment race and the world's most advanced enterprise private SA 5G program. T-Mobile's nationwide SA coverage, Verizon's C-band SA deployment, and AT&T's SA 5G evolution program collectively represent the world's largest single-country SA 5G infrastructure investment. The U.S. market's enterprise SA 5G adoption where manufacturing companies, healthcare systems, and logistics operators are deploying private SA 5G networks for dedicated enterprise connectivity is more commercially advanced than equivalent enterprise SA 5G adoption in any other national market, creating the commercial validation ecosystem that sustains U.S. market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific SA 5G Market Insights

Asia Pacific represents both the SA 5G Market's leading region by deployment scale with China, South Korea, Japan, and Australia each maintaining active commercial SA 5G programs and its fastest-growing region by investment trajectory. China Mobile, China Unicom, and China Telecom have collectively deployed SA 5G infrastructure covering over 1 billion people, making China the world's most extensively SA 5G-covered country by population reach. South Korea's three major carriers SK Telecom, KT, and LG Uplus were among the world's first commercial SA 5G launchers and maintain the world's highest per-capita SA 5G subscription penetration rates. Japan's SA 5G development led by NTT Docomo, KDDI, and SoftBank is particularly active in private 5G enterprise applications where Japanese manufacturers' Industry 4.0 investment creates demand for SA 5G capabilities.

Europe SA 5G Market Insights

Europe's SA 5G Market is growing with Germany's private 5G enterprise programs Deutsche Telekom, Vodafone Germany, and O2 Telefónica Germany all offering private SA 5G network services for manufacturing enterprise customers the UK's national SA 5G coverage program, and the EU's Connected and Automated Mobility initiative whose C-V2X SA 5G component creates government investment in automotive SA 5G infrastructure. The EU's 5G Action Plan's requirement for all major transport corridors to be covered by uninterrupted 5G connectivity by 2025 sustains SA 5G deployment investment beyond purely commercial carrier economics in member states whose transport corridor coverage obligations require infrastructure investment ahead of commercial revenue development.

MEA and Latin America SA 5G Market Insights

The Middle East's SA 5G Market is growing rapidly with Saudi Arabia's STC, UAE's Etisalat (e&), and Qatar's Ooredoo among the world's early commercial SA 5G launchers reflecting the Gulf states' determination to build world-class telecommunications infrastructure as a component of their economic diversification strategies. Saudi Arabia's VISION 2030 national digitization agenda has made SA 5G network development a priority infrastructure investment, with STC's SA 5G network covering major Saudi cities. Latin America's SA 5G market is in earlier development stages, with Brazil's Claro and TIM and Mexico's AT&T and Telcel beginning SA 5G commercial deployments as spectrum auctions and regulatory frameworks mature to support SA architecture investment.

Standalone 5G Network Market Growth Drivers:

-

Enterprise digital transformation and network slicing commercialization driving extraordinary standalone 5G network market growth globally

The SA 5G Market's extraordinary 56.14% CAGR reflects the rapid commercialization of a technology platform whose capabilities are qualitatively superior to predecessor wireless generations in ways that create entirely new business model possibilities. Network slicing commercially available only on SA 5G architectures enables operators to offer enterprise connectivity as a programmable infrastructure service whose guaranteed performance parameters (bandwidth, latency, reliability) are contractually enforceable in ways that best-effort public network connectivity cannot match. The industrial IoT applications smart factory machine control, automated quality inspection, robotic coordination that constitute Industry 4.0's automation ambition require the deterministic connectivity that SA 5G provides, creating industrial enterprise demand that sustains SA 5G deployment investment beyond the consumer connectivity upgrade that NSA 5G primarily serves.

Standalone 5G Network Market Restraints:

-

High deployment costs and core network transformation complexity creating standalone 5G network market challenges globally

SA 5G deployment requires telecom operators to replace their existing 4G core network with a new cloud-native 5G core a transformation whose cost and operational disruption is substantially greater than NSA 5G's simpler radio overlay on existing core infrastructure. Core network replacement requires new hardware infrastructure, cloud orchestration platform deployment, network function migration, and the operational expertise in cloud-native networking that traditional telecom network operations teams have not required for legacy packet core management. The capital cost of complete core network replacement estimated at USD 500 million to USD 2 billion for a major national carrier depending on network size creates a financial commitment that requires clear revenue case justification for enterprise network slicing services whose commercial development is still in its early phases.

Standalone 5G Network Market Opportunities:

-

Private enterprise 5G networks and edge computing integration creating transformative standalone 5G network market growth globally

Private enterprise SA 5G where manufacturing facilities, ports, airports, and campuses deploy dedicated SA 5G networks on licensed or shared spectrum exclusively for their own operational use represents the market's most commercially compelling near-term opportunity because enterprise ROI cases are more immediately calculable than public carrier service revenue growth projections. A BMW factory that deploys a private SA 5G network for real-time CNC machine communication, automated guided vehicle coordination, and AR-assisted assembly guidance can calculate the productivity improvement, quality improvement, and labor cost reduction that network-dependent automation enables creating a business case that justifies private SA 5G investment independent of public network economics. Edge computing integration where SA 5G network infrastructure and edge compute resources co-evolve at network edges creates the platform for latency-sensitive enterprise applications whose development sustains SA 5G network investment above the connectivity-only case.

Recent Developments:

-

2026: T-Mobile launched its SA 5G Network Slicing commercial service enabling enterprise customers to procure guaranteed 5G bandwidth, latency, and geographic coverage parameters through a software-defined API achieving 85 enterprise customers including three Fortune 500 manufacturers, two major U.S. health systems, and a national logistics company within six months of commercial launch, representing the first large-scale commercial SA 5G network slicing deployment in North America.

-

2025: Ericsson and BMW completed deployment of the world's largest private SA 5G manufacturing network spanning BMW's Dingolfing production facility in Bavaria with 5,000+ connected devices including assembly robots, AGVs, and quality control cameras reporting 22% improvement in production line flexibility through 5G-enabled reconfigurable assembly cell connectivity and 34% reduction in wired network maintenance cost through wireless replacement of legacy industrial Ethernet in dynamic production zones.

Standalone 5G Network Market Key Players

Some of the Standalone 5G Network Market Companies

-

Ericsson AB

-

Nokia Corporation

-

Huawei Technologies Co. Ltd.

-

Samsung Electronics Co. Ltd.

-

ZTE Corporation

-

Qualcomm Technologies Inc.

-

Intel Corporation

-

Mavenir Systems Inc.

-

Cisco Systems Inc.

-

IBM Corporation

-

Amazon Web Services Inc.

-

Microsoft Corporation (Azure for Operators)

-

Google LLC (Google Cloud Telecom)

-

NEC Corporation

-

Fujitsu Limited

-

Verizon Communications Inc.

-

AT&T Inc.

-

T-Mobile US Inc.

-

China Mobile Ltd.

-

SK Telecom Co. Ltd.

Standalone 5G Network Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.84 Billion |

| Market Size by 2035 | USD 1.04 Trillion |

| CAGR | CAGR of 56.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Spectrum (Sub-6 GHz, mmWave) • By Network (Public, Private) • By End Use (Manufacturing, Healthcare, Automotive & Transportation, Retail, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ericsson AB, Nokia Corporation, Huawei Technologies Co. Ltd., Samsung Electronics Co. Ltd., ZTE Corporation, Qualcomm Technologies Inc., Intel Corporation, Mavenir Systems Inc., Cisco Systems Inc., IBM Corporation, Amazon Web Services Inc., Microsoft Corporation, Google LLC, NEC Corporation, Fujitsu Limited, Verizon Communications Inc., AT&T Inc., T-Mobile US Inc., China Mobile Ltd., SK Telecom Co. Ltd. |

Frequently Asked Questions

Ans: The Standalone 5G Network Market was valued at USD 5.84 billion in 2025.

Ans: Automotive & Transportation is growing at the fastest CAGR; Manufacturing is the dominant end use.

Ans: Public segment dominated with approximately 68% share and is also growing at the fastest CAGR.

Ans: Solutions dominated with approximately 83% share; Services are growing at the fastest CAGR.

Ans: The Standalone 5G Network Market is expected to grow at a CAGR of 56.14% from 2026 to 2035.

Get in Touch