Hyperscale Computing Market Report Scope & Overview:

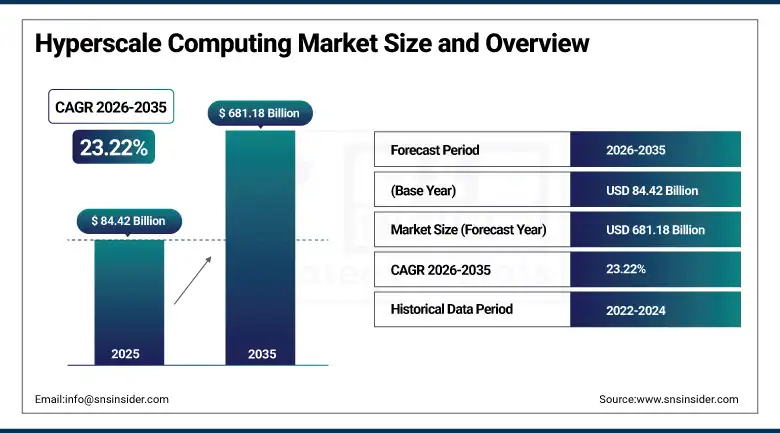

The Hyperscale Computing Market was valued at USD 84.42 Billion in 2025 and is expected to reach USD 681.18 Billion by 2035, growing at a CAGR of 23.22% from 2026–2035.

Hyperscale computing refers to large-scale distributed computing infrastructure operated by cloud providers, internet platforms, and major enterprises to deliver computing, storage, and networking resources on demand. These environments consist of thousands of interconnected servers across multiple data centers, enabling highly efficient and scalable digital services. The key advantage of hyperscale architecture is its ability to provide significantly lower infrastructure costs compared to traditional enterprise data centers while maintaining high performance and reliability. Growth in artificial intelligence applications, including large language models and generative AI systems, is driving unprecedented demand for hyperscale infrastructure. As a result, organizations are investing heavily in advanced data centers, GPUs, and high-speed networking technologies.

In 2024, Microsoft announced plans to invest USD 80 billion in AI data centre infrastructure globally, with more than half allocated to U.S. facilities, representing the largest single-year infrastructure capital commitment in the company's history. This extraordinary investment reflected

Market Size and Forecast

-

Market Size in 2026E: USD 104.01 Billion

-

Market Size by 2035: USD 681.18 Billion

-

CAGR: 23.22% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Hyperscale Computing Market - Request Free Sample Report

Hyperscale Computing Market Trends

-

Generative AI and large language model adoption are driving unprecedented investment in hyperscale infrastructure, increasing demand for advanced GPUs, high-bandwidth memory, and high-speed networking systems

-

Liquid cooling technologies are gaining traction in hyperscale data centers as high-performance AI servers generate heat levels that traditional air-cooling systems cannot efficiently manage

-

Sovereign cloud requirements and data residency regulations are encouraging hyperscale providers to establish localized cloud regions to support compliance and expand adoption among regulated industries

-

Integration of edge computing with hyperscale cloud platforms is enabling faster processing of latency-sensitive workloads while maintaining centralized storage and large-scale computing resources

-

Growing power consumption from AI infrastructure is accelerating interest in nuclear and other next-generation energy sources to ensure reliable, continuous operation of hyperscale data centers

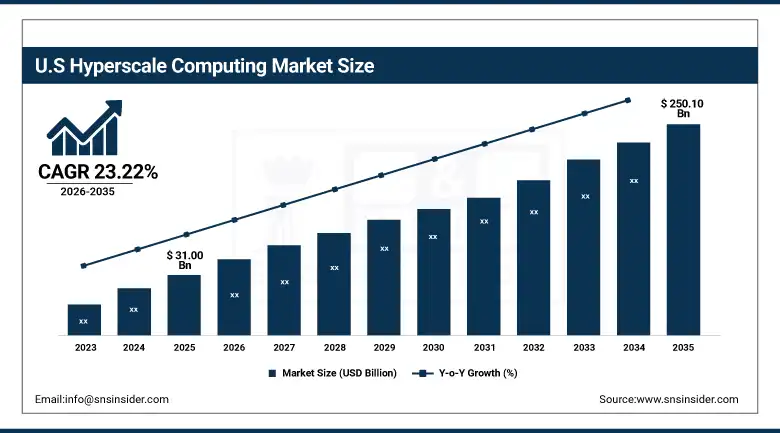

U.S. Hyperscale Computing Market Outlook

The U.S. Hyperscale Computing Market was valued at approximately USD 31.00 Billion in 2025 and is expected to reach approximately USD 250.10 Billion by 2035, growing at a CAGR of approximately 23.22%.

The United States is the largest and most influential hyperscale computing market, driven by the presence of major cloud service providers and extensive investments in large-scale data center infrastructure. Strong demand from artificial intelligence developers, cloud platforms, and enterprise customers continues to fuel expansion of computing capacity and advanced networking systems. The country also benefits from significant government cloud adoption initiatives, which generate substantial demand for hyperscale services across federal agencies and public-sector organizations. Continuous investments in AI infrastructure, high-performance computing, and cloud innovation reinforce the United States' leadership position and make it a key driver of global hyperscale computing market growth.

In 2025, Google Cloud announced the Ironwood TPU, its seventh-generation tensor processing unit purpose-built for AI inference workloads, offering 10 times the performance of its predecessor TPU and making Google's proprietary AI chip infrastructure the most commercially significant alternative to NVIDIA GPU-based hyperscale AI computing.

Hyperscale Computing Market Segment Analysis

-

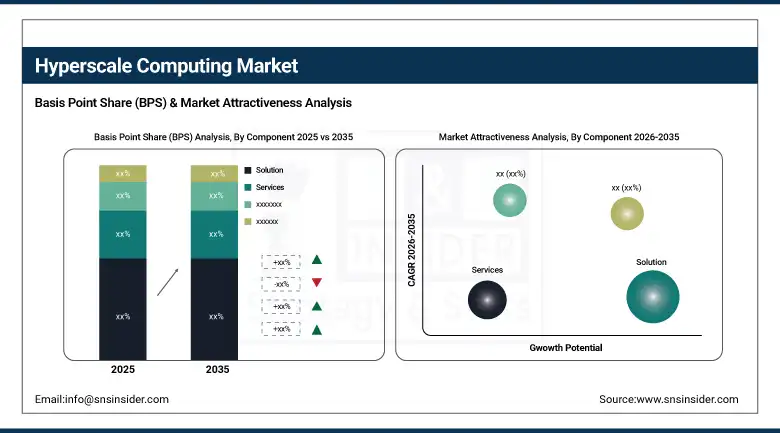

By Component, the Solution segment dominated the Hyperscale Computing Market with approximately 76% share in 2025, while the Services segment is the fastest growing component with a CAGR of 24.98%, driven by growing demand for maintenance, advisory, and support services as hyperscale operations expand.

-

By Deployment Mode, the Public Cloud segment dominated the Hyperscale Computing Market with the largest share in 2025, while Hybrid Cloud is the fastest growing deployment mode as enterprises balance cloud economics with data control requirements.

-

By Organization Size, the Large Enterprises segment dominated the Hyperscale Computing Market with approximately 71% share in 2025, while the Small & Medium-Sized Enterprises segment is the fastest growing organisation size as cloud-native architecture democratises hyperscale resource access.

-

By End User, the Cloud Service Providers segment dominated the Hyperscale Computing Market with the largest share in 2025, while the Healthcare segment is among the fastest growing end users driven by AI diagnostic, genomics, and medical imaging workload growth.

By Component, solutions dominate, services grow fastest

Solutions retained the dominant component position with approximately 76% of the hyperscale computing market in 2025. The solution segment's commercial primacy reflects the capital intensity of hyperscale hardware infrastructure whose server, storage, and networking procurement represents the overwhelming majority of hyperscale computing investment. Each hyperscale data centre campus represents billions of dollars of server rack, GPU accelerator, high-bandwidth networking switch, and storage array investment whose procurement concentration among the major cloud providers creates an enormous solution revenue pool that services revenue cannot approach in magnitude despite its faster growth rate.

Services are growing fastest at 24.98% CAGR, driven by the expanding complexity of hyperscale operations whose scale requires professional services for architecture design, security assessment, performance optimisation, migration management, and managed services delivery that organisations cannot efficiently staff internally. As cloud adoption matures and AI workload complexity increases, the requirement for specialised advisory, implementation, and ongoing managed services to optimise hyperscale infrastructure utilisation and cost creates above-market services revenue growth at the major cloud providers and their system integrator partners.

By Organization Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organisation size position with approximately 71% of the hyperscale computing market in 2025. Their commercial dominance reflects both the scale of their hyperscale infrastructure investment and the commercial concentration of the most demanding AI workloads in large technology companies, financial institutions, and healthcare organisations whose data volumes, AI model complexity, and performance requirements necessitate hyperscale computing access at the largest scale. Large technology companies whose own products are delivered through hyperscale cloud infrastructure represent the highest-value individual hyperscale customers whose GPU cluster reservations, committed use discounts, and custom infrastructure requirements create multi-year, multi-billion-dollar commercial relationships with hyperscale providers.

SMEs are the fastest-growing organisation size segment because hyperscale cloud platforms' consumption-based pricing model enables small and medium businesses to access computing resources that would require prohibitive capital investment if deployed on-premises. Each SME that adopts cloud-native architecture becomes a hyperscale computing customer whose per-organisation revenue is lower than large enterprise equivalents but whose aggregate across millions of SME customers creates substantial market revenue growth as digital business adoption progresses across the global commercial ecosystem.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.4% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

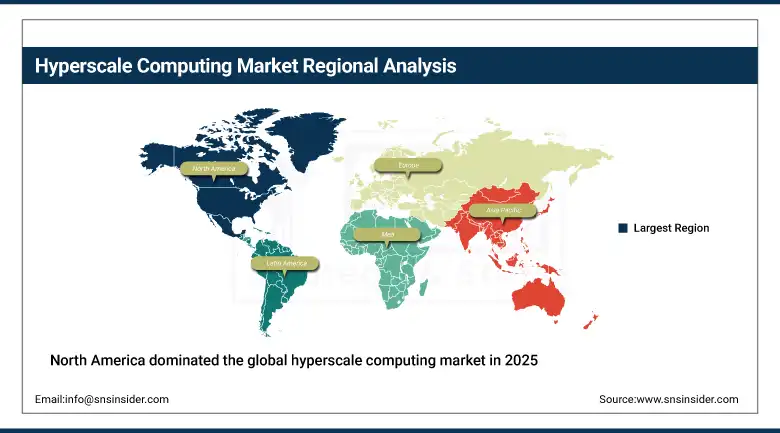

North America Hyperscale Computing Market Insights

North America dominated the global hyperscale computing market in 2023, accounting for the largest regional revenue share. The United States accounts for approximately 82.4% of North American revenues through its extraordinary concentration of cloud service provider headquarters, AI research organisations, and hyperscale infrastructure investors whose combined annual capital deployment defines the global hyperscale computing market's commercial trajectory. Amazon Web Services, Microsoft Azure, and Google Cloud's combined annual infrastructure investment represents the world's largest private sector capital programme in any technology category, creating the commercial foundation that sustains North American hyperscale market dominance independent of growth rate comparisons with emerging regional markets.

Canada contributes supplementary demand through its growing cloud adoption, the commercial presence of Shopify and other cloud-native technology companies, and its strategic importance as a data sovereignty-compliant alternative to U.S. data centre locations for Canadian government and regulated industry cloud workloads. Canada's growing AI research ecosystem at institutions including the Vector Institute and Mila creates academic hyperscale demand that complements the commercial cloud adoption driving national market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hyperscale Computing Market Insights

Europe held a significant share of the global Hyperscale Computing Market in 2025. Germany, the United Kingdom, Ireland, Sweden, and the Netherlands are the leading national hyperscale markets whose combination of major cloud provider regional infrastructure, enterprise cloud adoption, and regulatory compliance requirements create consistent and growing demand. Ireland has emerged as the European hyperscale infrastructure hub for U.S. cloud providers seeking European market proximity, regulatory alignment, and renewable energy availability whose combined characteristics make it the EU's leading hyperscale data centre construction market by annual investment.

Europe's GDPR data sovereignty requirements, the EU Data Act's cloud switching and interoperability provisions, and the AI Act's compute governance implications collectively create a regulatory framework whose compliance requirements sustain European hyperscale infrastructure investment independent of demand-side growth drivers. Germany accounts for approximately 28.5% of European revenues through its large enterprise cloud adoption, the concentration of European industrial AI workloads in its manufacturing sector, and the sovereignty requirements of its highly regulated financial services industry.

Asia Pacific Hyperscale Computing Market Insights

Asia Pacific is the fastest-growing regional hyperscale computing market, driven by the extraordinary digital economy scale of China, the rapid cloud adoption in India and Southeast Asia, and the government AI investment programmes of Japan and South Korea. China accounts for approximately 38.5% of Asia Pacific revenues through its domestic hyperscale ecosystem of Alibaba Cloud, Tencent Cloud, and Huawei Cloud whose combined infrastructure scale rivals Western hyperscale providers and whose domestic AI development programmes create sustained hyperscale GPU cluster demand within China's information technology sovereignty framework.

India's digital economy growth, government cloud procurement under the National Cloud Programme, and the rapidly expanding startup ecosystem's cloud-native architecture adoption are creating above-regional-average national market growth that positions India as the most commercially dynamic emerging hyperscale market within Asia Pacific. Southeast Asian markets including Singapore, Malaysia, and Indonesia are attracting hyperscale data centre investment as regional digital economy growth creates cloud demand that international providers are addressing through regional infrastructure establishment.

MEA & Latin America Hyperscale Computing Market Insights

The UAE leads MEA revenues at approximately 38.4% through its strategic ambition to become the Middle East's AI and cloud hub, with substantial government AI investment under the UAE AI Strategy 2031 and the commercial presence of all major hyperscale cloud providers whose UAE regions serve the broader GCC and North Africa market. Saudi Arabia's Vision 2030 digital transformation programme and its NEOM smart city project create substantial government hyperscale procurement that makes the Kingdom the region's second-largest national market.

Brazil leads Latin American revenues at approximately 44.2% through its large digital economy, the concentration of cloud provider Latin American regional infrastructure in São Paulo, and the growing enterprise cloud adoption driven by digital transformation investment across banking, retail, and industrial sectors. Mexico, Colombia, and Chile contribute growing secondary market demand as their digital economies mature and cloud adoption penetration increases beyond early adopter technology company segments into broader enterprise deployment.

Market Dynamics

Growth Drivers: Generative AI workload explosion driving unprecedented GPU cluster investment and cloud adoption maturation across enterprise segments globally

The hyperscale computing market's extraordinary growth rate is driven by the AI revolution's transformation of computing infrastructure requirements at a pace and scale that the industry had not previously experienced in any technology transition. Generative AI's training infrastructure requirements, where a single frontier model training run consuming tens of millions of GPU hours creates procurement demand for thousands of NVIDIA H100 and H200 GPUs per cluster at USD 30,000 to USD 40,000 per unit, represent a demand category whose commercial scale has propelled hyperscale capital expenditure from approximately USD 150 billion in 2022 to over USD 350 billion in 2024 across the major providers. Each new foundation model generation whose capability improvements create new commercial applications expands the inference infrastructure required to serve those applications at scale, creating a perpetual demand growth cycle whose commercial momentum sustains the hyperscale computing market's exceptional growth trajectory.

Enterprise cloud adoption maturation is simultaneously creating above-trend hyperscale demand as the migration of core enterprise workloads from on-premises infrastructure to cloud platforms progresses from early adopter technology companies toward mainstream financial services, healthcare, manufacturing, and government sectors whose cloud adoption journey creates sustained multi-year hyperscale demand that diversifies market growth beyond AI-specific workload categories.

Restraints: Power supply constraints and AI chip supply concentration creating infrastructure deployment bottlenecks that limit hyperscale expansion velocity

Hyperscale data centre construction is increasingly constrained by power supply availability whose grid connection timelines of three to seven years at many locations substantially exceed the construction timelines of the data centre facility, creating power-limited deployment queues at established hyperscale locations including Northern Virginia, the Netherlands, and Dublin. AI GPU server clusters operating at 50 to 100 kilowatts per rack create power density requirements that exceed the infrastructure design parameters of existing data centre facilities, requiring new construction or significant power upgrades that extend deployment timelines. NVIDIA's effective monopoly on high-performance AI training GPUs creates supply concentration risk where procurement constraints at a single semiconductor company can delay hyperscale AI infrastructure deployment programmes across the entire industry simultaneously.

Opportunities: Sovereign AI infrastructure programmes and edge AI inference deployment represent transformative commercial frontiers for hyperscale market expansion

Government sovereign AI infrastructure programmes, where national governments invest in domestic hyperscale computing infrastructure to develop and deploy AI applications without dependence on foreign cloud providers, represent a new and rapidly growing hyperscale demand category whose commercial scale reflects geopolitical imperatives rather than purely commercial return-on-investment calculations. The UAE, Saudi Arabia, Singapore, France, and India each have sovereign AI programmes with multi-billion-dollar hyperscale infrastructure components whose procurement creates substantial market demand at government-directed economics. Edge AI inference deployment creates the next frontier of hyperscale market expansion as the most latency-sensitive AI applications including autonomous vehicles, industrial quality control, and real-time language translation require inference computing infrastructure distributed across thousands of edge locations whose collective compute capacity and management complexity create a new distributed hyperscale architecture demand category.

Recent Developments:

-

2025: Google Cloud announced the Ironwood TPU, its seventh-generation tensor processing unit for AI inference workloads, delivering 10 times the performance of its predecessor and establishing Google's proprietary AI chip infrastructure as the most commercially significant alternative to NVIDIA GPU-based hyperscale AI computing.

-

2024: Microsoft announced USD 80 billion in global AI data centre infrastructure investment, the largest single-year infrastructure capital commitment in the company's history, reflecting the scale of GPU cluster infrastructure required to serve Azure's growing AI workloads and OpenAI partnership requirements.

-

2024: Amazon Web Services launched its second-generation Trainium2 AI training chip, offering up to 4 times better performance and energy efficiency versus Trainium1, advancing AWS's proprietary AI silicon strategy of reducing dependency on NVIDIA GPU supply while creating cost-performance advantages for AWS cloud AI training customers.

Hyperscale Computing Market Key Players

-

Amazon Web Services Inc. (AWS)

-

Microsoft Corporation (Azure)

-

Google LLC (Google Cloud)

-

Meta Platforms Inc.

-

Alibaba Cloud (Alibaba Group)

-

Tencent Cloud (Tencent Holdings)

-

Huawei Technologies Co. Ltd.

-

Oracle Corporation

-

International Business Machines Corp. (IBM)

-

Hewlett Packard Enterprise Co.

-

Dell Technologies Inc.

-

Cisco Systems Inc.

-

NVIDIA Corporation

-

Intel Corporation

-

Advanced Micro Devices Inc. (AMD)

-

Equinix Inc.

-

Digital Realty Trust Inc.

-

NTT Ltd.

-

Rackspace Technology Inc.

-

Server Technology Inc.

Hyperscale Computing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 84.42 Billion |

| Market Size by 2035 | USD 681.18 Billion |

| CAGR | CAGR of 23.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud) • by Organization Size (Large Enterprises, Small & Medium-Sized Enterprises) • by End User (Cloud Service Providers, Internet & Social Media Platforms, Financial Services, Healthcare, Retail & E-Commerce, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amazon Web Services Inc. (AWS), Microsoft Corporation (Azure), Google LLC (Google Cloud), Meta Platforms Inc., Alibaba Cloud (Alibaba Group), Tencent Cloud (Tencent Holdings), Huawei Technologies Co. Ltd., Oracle Corporation, International Business Machines Corp. (IBM), Hewlett Packard Enterprise Co., Dell Technologies Inc., Cisco Systems Inc., NVIDIA Corporation, Intel Corporation, Advanced Micro Devices Inc. (AMD), Equinix Inc., Digital Realty Trust Inc., NTT Ltd., Rackspace Technology Inc., Server Technology Inc. |

Frequently Asked Questions

The Hyperscale Computing Market is expected to grow at a CAGR of 23.22% from 2026 to 2035.

The Hyperscale Computing Market was valued at USD 84.42 Billion in 2025.

Generative AI and foundation model training and inference creating unprecedented GPU cluster procurement demand, enterprise cloud adoption maturation across mainstream industry sectors, sovereign AI infrastructure investment by national governments, and the expansion of cloud-native architecture into SME segments are the primary growth factors.

The Solution segment dominated the Hyperscale Computing Market with approximately 76% share in 2025, while the Services segment is the fastest growing at a CAGR of 24.98%.

North America dominated the Hyperscale Computing Market in 2023, with the United States accounting for approximately 82.4% of North American revenues through the concentration of AWS, Microsoft Azure, and Google Cloud's primary infrastructure.

Get in Touch