STATCOM Market Report Scope & Overview:

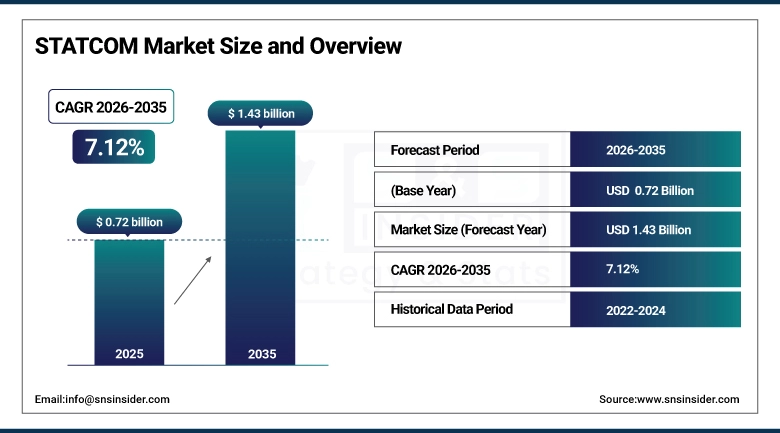

The STATCOM Market size was valued at USD 0.72 billion in 2025 and is expected to reach USD 1.43 billion by 2035, growing at a CAGR of 7.12% from 2026-2035.

The STATCOM market is expanding as utilities and grid operators prioritize advanced voltage regulation and reactive power compensation to support rising renewable energy integration. Increasing deployment of solar and wind assets is creating grid instability challenges that STATCOM systems effectively address. Modernization of aging transmission infrastructure, growth in industrial power demand, and the need for fast-response dynamic grid support are further accelerating adoption. Additionally, tighter grid-stability regulations and investments in smart grid technologies are boosting long-term market growth.

More than 1,200 STATCOM units operated globally, with MMC-based designs achieving over 98% efficiency, accelerating adoption across smart grids and utility renewable portfolios.

STATCOM Market Size and Forecast

-

Market Size in 2025: USD 0.72 Billion

-

Market Size by 2035: USD 1.43 Billion

-

CAGR: 7.12% from 2026 to 2035

-

Base Year: 2025E

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On STATCOM Market - Request Free Sample Report

STATCOM Market Trends Highlights:

-

Rising grid modernization initiatives drive adoption of advanced STATCOM solutions worldwide.

-

Increasing renewable energy integration boosts demand for voltage stabilization and power quality support.

-

Growing deployment in utilities and heavy industries to manage dynamic reactive power needs.

-

Expansion of high-voltage STATCOM installations supporting transmission network reliability and resilience.

-

Adoption of modular, compact STATCOM designs enabling easier grid integration and scalability.

-

Digital monitoring, analytics, and remote-control features enhance STATCOM performance and maintenance efficiency.

U.S. STATCOM Market Size Outlook:

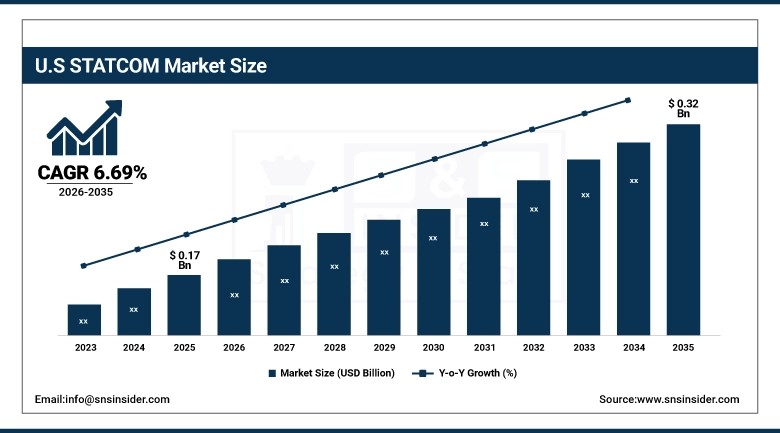

The U.S. STATCOM Market was valued at USD 0.17 billion in 2025 and is expected to reach USD 0.32 billion by 2035, growing at a CAGR of 6.69% from 2026-2035. Growth in the U.S. STATCOM market is driven by increasing grid modernization efforts, rising integration of renewable energy, and the need for fast, dynamic voltage stabilization. Utilities are upgrading infrastructure to manage fluctuating power flows, while stricter reliability standards and expanding industrial loads further support demand for advanced STATCOM systems.

The DOE is deploying over USD 20 billion to strengthen U.S. grid infrastructure, including 625 miles of new transmission lines adding 4,300 MW capacity, alongside major investments in HVDC, dynamic line ratings, and nationwide modernization to support rising renewable integration.

Market Growth Drivers: Increasing Integration of Renewable Energy Sources Driving STATCOM Market Growth

The rapid expansion of wind and solar installations is creating greater variability and instability in power grids, significantly increasing the need for advanced voltage regulation solutions. As renewable energy sources fluctuate due to changing weather conditions, utilities require fast-acting technologies like STATCOM systems to maintain voltage stability, provide dynamic reactive power support, and improve overall power quality. These systems help ensure seamless grid operation, reduce outages, and support higher renewable penetration. As global clean energy adoption accelerates, demand for STATCOM technology continues to rise across utility and industrial sectors.

Globally, rising renewable integration is boosting grid-resilience investments while revealing system vulnerabilities. India’s renewable capacity reached 220.10 GW in 2025, prompting major grid upgrades, while in the U.S., solar and storage made up 83% of 2025 capacity additions, intensifying grid-management challenges.

-

Growing Industrial Power Demand Boosting Adoption of STATCOM Systems

Rising power demand in energy-intensive industries such as steel manufacturing, mining, petrochemicals, and heavy electrical equipment is driving the need for reliable voltage stability and reactive power compensation. These industries operate large motors, furnaces, and heavy machinery that cause voltage fluctuations and power quality issues. STATCOM systems offer fast, precise, and dynamic support to stabilize voltage levels, minimize downtime, and improve operational efficiency. As industries expand production capacity and adopt more automated equipment, the demand for STATCOM solutions to ensure uninterrupted and high-quality power supply continues to grow.

Additional examples come from leading manufacturers like Merus Power, whose STATCOM technology in heavy industry (including electric arc furnaces in steel plants) leads to increased production by 7-10%, energy consumption reductions up to 7%, and CO2 reduction per ton produced

Market Restraints: High Initial Capital Investment Limiting Wider Adoption of STATCOM Systems

STATCOM systems involve substantial upfront investment due to the high cost of power electronics, transformers, advanced control systems, and specialized installation requirements. These expenses make STATCOMs considerably more expensive than traditional reactive power compensation solutions, creating challenges for small utilities, industrial facilities, and budget-constrained grid operators. Additionally, the need for skilled engineering expertise and site preparation further increases total project costs. As a result, many organizations opt for lower-cost alternatives like SVCs or capacitor banks, making high capital investment a major restraint on STATCOM market adoption.

STATCOM system installations typically require a high initial capital investment estimated between USD5 million to USD15 million for medium-capacity units, depending significantly on system specifications, capacity, and project complexity.

-

Availability of Lower-Cost Alternatives Restricting STATCOM Market Penetration

The presence of lower-cost reactive power compensation solutions—such as Static Var Compensators (SVCs), capacitor banks, and synchronous condensers—poses a significant restraint on STATCOM adoption, especially in cost-sensitive regions. These alternatives provide adequate voltage stability and reactive power support at a fraction of the cost of STATCOM systems. For many utilities and industrial users with limited budgets, the performance advantages of STATCOMs do not always justify the higher investment. As a result, decision-makers often choose these more economical technologies, slowing the overall market penetration of STATCOM solutions.

Cost comparisons show that SVCs generally cost about 70-90% of what STATCOM systems cost on a per MVAR basis. For example, one project showed SVC installation costs approximately USD0.644 million per 50 MVAR unit, while comparable STATCOM units ranged from USD0.2 to USD0.76 million per 50 MVAR depending on location and capacity.

Market Opportunities: Rising Integration of Renewable Energy Creating Strong Demand for STATCOM Solutions

The rapid growth of wind, solar, and hybrid renewable projects is increasing grid instability due to fluctuating power generation and variability in voltage levels. As utilities integrate more renewable capacity, the need for advanced reactive power compensation and dynamic voltage regulation becomes critical. STATCOMs provide fast, flexible, and highly efficient grid support, helping stabilize voltage, reduce flicker, and maintain power quality. With global renewable adoption accelerating, demand for STATCOM systems is rising sharply across transmission networks, renewable plants, and hybrid grid infrastructures.

Globally, grid instability and saturation are among the top challenges facing the renewables sector. In a 2025 industry survey, 60.1% of respondents identified grid saturation and instability as critical challenges, reflecting the impact of increased intermittent renewable generation.

-

Increasing Adoption of EVs and Charging Infrastructure Boosting Opportunities for STATCOM Deployment

The rapid expansion of electric vehicles (EVs) and the rollout of fast-charging infrastructure are creating strong opportunities for STATCOM integration. Fast chargers draw high power in short intervals, often causing voltage fluctuations, power-quality issues, and increased reactive power demand on local grids. STATCOMs provide rapid, dynamic voltage support and stabilize power supply for EV charging stations, especially in dense urban and commercial areas. As countries accelerate EV adoption and expand nationwide charging networks, the need for STATCOM solutions to maintain grid reliability and performance continues to grow significantly.

California Public Utilities Commission (CPUC): In 2025, policies and transmission project reviews emphasized grid modernization for managing growing EV charging demands and renewable energy expansion, including the potential incorporation of STATCOM and other grid support technologies.

STATCOM Market Segment Highlights

-

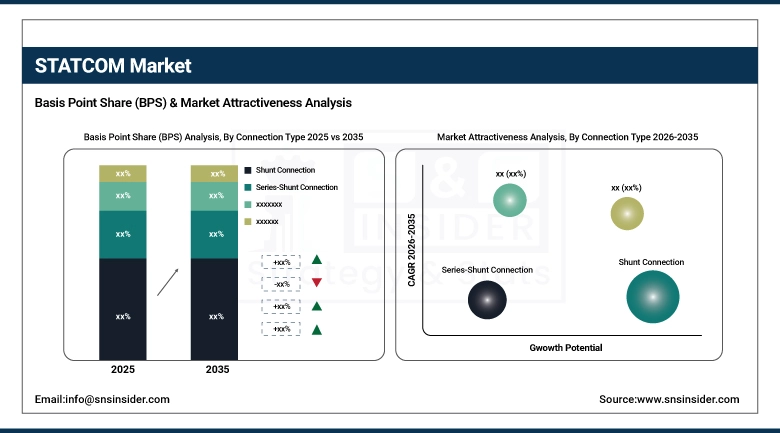

By Connection Type: In 2025, Shunt Connection led the market with 88% share, while Series-Shunt Connection is the fastest-growing segment with the highest CAGR (2026–2035).

-

By Technology: In 2025, Insulated Gate Bipolar Transistor (IGBT)-Based STATCOM led the market with 72% share, and is also the fastest-growing segment with the highest CAGR (2026–2035).

-

By Rated Power Outlook: In 2025, Medium Power STATCOM (20–100 MVAR) led the market with 41% share, while High Power STATCOM (>100 MVAR) is the fastest-growing segment with the highest CAGR (2026–2035).

-

By End Use Outlook: In 2025, Utility led the market with 38% share, while Renewable Energy is the fastest-growing segment with the highest CAGR (2026–2035).

By Connection Type, Shunt Connection segment led in 2025 and Series-Shunt Connection segment expected fastest growth 2026–2035

Shunt Connection dominated the STATCOM Market in 2025 because it is the most widely used configuration for voltage stabilization, reactive power compensation, and grid support. Its simple design, cost-effectiveness, and strong suitability for transmission and distribution networks ensure large-scale deployment across utilities and industrial grids.

Series-Shunt Connection is expected to grow fastest from 2026–2035 due to rising demand for advanced hybrid compensation systems capable of improving both voltage stability and power flow. Its ability to address complex grid challenges, especially in networks integrating renewable energy, supports its accelerating adoption.

By Technology, IGBT-Based STATCOM segment led in 2025 and IGBT-Based STATCOM segment expected fastest growth 2026–2035

Insulated Gate Bipolar Transistor (IGBT)-Based STATCOM dominated the market in 2025 and is expected to grow fastest from 2026–2035 because IGBT technology delivers superior switching efficiency, compact design, and enhanced dynamic response. These systems support advanced voltage control, enable higher reliability, and reduce operational losses. Growing renewable integration, stricter grid stability requirements, and the transition toward flexible, digitally controlled power electronics continue to push IGBT-based STATCOM solutions to the forefront of modern grid applications.

By Rated Power Outlook, Medium Power STATCOM (20–100 MVAR) segment led in 2025 and High Power STATCOM (>100 MVAR) segment expected fastest growth 2026–2035

Medium Power STATCOM (20–100 MVAR) dominated the market in 2025 due to strong deployment in transmission networks, industrial grids, and utility substations that require stable voltage regulation. Their balance of cost, performance, and adaptability across multiple grid environments ensures consistent adoption.

High Power STATCOM (greater than 100 MVAR) is expected to grow fastest from 2026–2035 because expanding renewable integration, larger transmission corridors, and modern high-capacity grids require robust reactive power support. Their capability to manage heavy load fluctuations and enhance long-distance power stability drives rapid market growth.

By End Use Outlook, Utility segment led in 2025 and Renewable Energy segment expected fastest growth 2026–2035

Utility end users dominated the STATCOM Market in 2025 because utilities face increasing pressure to maintain grid stability, support rising electricity demand, and integrate variable renewable power. Their large-scale infrastructure investments and need for reliable voltage management make them the primary adopters.

Renewable Energy is expected to grow fastest from 2026–2035 due to expanding solar and wind installations that require dynamic reactive power compensation. STATCOM systems help stabilize voltage fluctuations, enhance grid connectivity, and improve power quality, making them essential for modern renewable power integration.

STATCOM Market Regional Analysis

North America STATCOM Market Insights:

North America held a strong position in the STATCOM Market in 2025, driven by significant investments in grid modernization, rising integration of renewable energy sources, and increasing need for voltage regulation across aging transmission networks. The presence of major technology providers and supportive regulatory initiatives further strengthened the region’s adoption of advanced STATCOM systems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific STATCOM Market Insights:

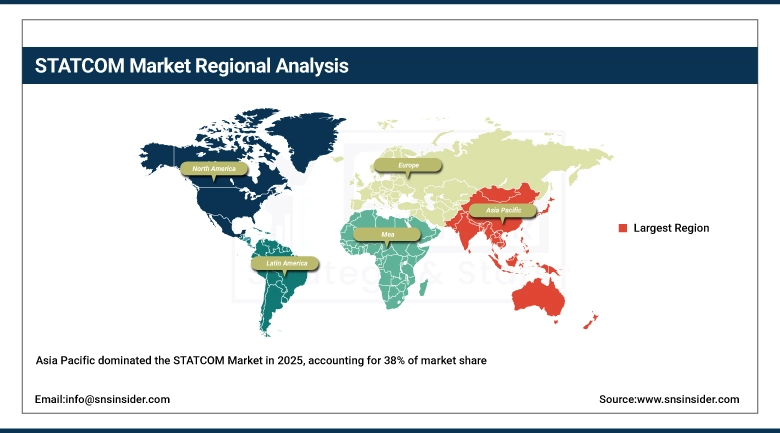

Asia Pacific dominated the STATCOM Market with a 38% share in 2025 due to rapid expansion of renewable energy installations, rising grid instability, and strong government initiatives to modernize transmission infrastructure. Increasing industrialization, higher power demand, and investments in smart grids further strengthened the region’s leadership in deploying advanced reactive power compensation technologies.

Asia Pacific is expected to grow at the fastest CAGR of about 8.24% from 2026–2035, driven by accelerated renewable energy integration, large-scale solar and wind capacity additions, and rising need for voltage stabilization across rapidly expanding power networks. Supportive regulatory policies, grid modernization projects, and increasing adoption of utility-scale STATCOM solutions fuel the region’s strong growth outlook.

Europe STATCOM Market Insights

Europe maintained a strong position in the STATCOM Market in 2025, supported by aggressive renewable energy targets, extensive wind power integration, and ongoing upgrades to transmission and distribution networks. The region’s strict grid stability requirements, emphasis on decarbonization, and adoption of flexible AC transmission technologies reinforced its significant market share and strategic importance.

Middle East & Africa and Latin America STATCOM Market Insights:

The Middle East & Africa and Latin America regions together showed steady growth in the STATCOM Market in 2025, supported by rising investments in power infrastructure, growing demand for grid stability, and increasing adoption of renewable energy projects. Expanding industrial activity, voltage fluctuation challenges, and gradual modernization of transmission networks further contributed to the regions’ improving market presence.

STATCOM Market Competitive Landscape:

ABB Ltd., established in 1988 through the merger of Sweden’s ASEA (founded in 1883) and Switzerland’s Brown, Boveri & Cie (founded in 1891), is a global leader in electrification and automation, delivering advanced power-grid technologies, including STATCOM systems, FACTS solutions, and digital substations. The company focuses on enhancing grid stability, improving voltage regulation, and supporting renewable-energy integration through its power-electronics portfolio. ABB’s STATCOM solutions are widely deployed in transmission networks, wind and solar farms, and industrial grids. With strong R&D capabilities, global manufacturing, and software-driven optimization platforms, ABB continues to expand its role in modernizing power infrastructure and enabling more resilient, flexible, and sustainable electricity systems.

-

April 2024: ABB published a new “Digital Substations in the News” item noting its digital-substation technologies being deployed, which tie into its grid-stability and power-electronics efforts.

Siemens Energy AG, established in 2020, provides a comprehensive range of power-grid solutions, including advanced STATCOM and FACTS technologies designed to improve voltage stability, reactive-power compensation, and grid reliability. The company supports large-scale renewable integration, HVDC systems, and smart-grid modernization projects worldwide. Siemens Energy leverages strong engineering expertise, digital monitoring platforms, and high-efficiency power-electronics to address rising energy-transition challenges. Its STATCOM systems are deployed across utilities, industrial networks, and renewable plants, helping enhance power-quality performance and system resilience in complex, high-demand grid environments.

-

In 2024: The story “Germany’s bold move to reinvent grid stability” covers the world’s first E-STATCOM using supercapacitors for voltage and frequency support.

Mitsubishi Electric Corporation, established in 1921, is a major supplier of power-electronics and grid-stability systems, offering STATCOM, HVDC, and dynamic-reactive compensation technologies. The company’s STATCOM solutions are engineered to deliver fast voltage control, improved power quality, and enhanced system stability across transmission and industrial grids. Mitsubishi Electric emphasizes reliability, modular engineering, and advanced semiconductor technologies in its grid-automation portfolio. With a global footprint and strong partnerships in utilities and renewable-energy sectors, the company plays a key role in strengthening power-system performance and supporting large-scale clean-energy integration.

-

May 26, 2023: The company’s Taipei affiliate won Taiwan’s first STATCOM order (±200 MVA) from Taiwan Power Company, aimed at stabilizing the Tainan Science Park grid with high renewable/industrial demand.

Hitachi Energy, established in 2020, is a world leader in grid-stabilization technologies, offering STATCOM, FACTS, HVDC, and digital-substation solutions. Its STATCOM systems deliver rapid reactive-power compensation, voltage support, and enhanced power-quality management for utilities, renewable-energy plants, and industrial customers. Hitachi Energy focuses on integrating power-electronics with digital monitoring, automation, and predictive-maintenance platforms to enable smarter, more flexible grid operations. With strong global project expertise and advanced engineering capabilities, the company supports grid modernization and the transition toward reliable, resilient, and sustainable energy systems.

-

May 20, 2025: Hitachi Energy wins contract with Transpower New Zealand to supply a ±150 MVAR STATCOM at Otāhuhu substation (Second stage) to support grid transformation and growing clean-energy demand.

STATCOM Companies are:

-

ABB Ltd.

-

Mitsubishi Electric Corporation

-

Hitachi Energy (Hitachi Ltd.)

-

GE Grid Solutions (General Electric)

-

Toshiba Energy Systems & Solutions Corporation

-

Rongxin Power Electronic Co., Ltd. (RXHK)

-

Ingeteam Power Technology, S.A.

-

Eaton Corporation plc

-

S&C Electric Company

-

NR Electric Co., Ltd.

-

Hyosung Heavy Industries

-

Siemens Gamesa / Siemens Transmission Solutions

-

Schneider Electric SE

-

Trinity Energy Systems Pvt. Ltd.

-

Adani Transmission / Adani Energy Solutions Ltd. (FACTS solutions)

-

KEPCO Engineering & Construction (KEPCO E&C)

-

Merus Power Oyj

-

Power Quality Systems / Power Electronics Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.72 Billion |

| Market Size by 2035 | USD 1.43 Billion |

| CAGR | CAGR of 7.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Connection Type (Shunt Connection, Series-Shunt Connection) • By Technology (GTO-Based STATCOM, IGBT-Based STATCOM, IGCT-Based STATCOM) • By Rated Power Outlook (Low Power STATCOM <20 MVAR, Medium Power STATCOM 20–100 MVAR, High Power STATCOM >100 MVAR) • By End Use Outlook (Utility, Steel Manufacturing, Mining, Renewable Energy, Hydrogen Power Plant, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd., Siemens Energy AG, Mitsubishi Electric Corporation, Hitachi Energy, GE Grid Solutions, Toshiba Energy Systems & Solutions Corporation, Rongxin Power Electronic Co., Ltd. (RXHK), Ingeteam Power Technology S.A., American Superconductor Corporation (AMSC), Eaton Corporation plc, S&C Electric Company, NR Electric Co., Ltd., Hyosung Heavy Industries, Siemens Gamesa / Siemens Transmission Solutions, Schneider Electric SE, Trinity Energy Systems Pvt. Ltd., Adani Energy Solutions Ltd. (Adani Transmission), KEPCO Engineering & Construction (KEPCO E&C), Merus Power Oyj, Power Electronics Group (Power Quality Systems). |

Frequently Asked Questions

Asia Pacific dominated in 2025, driven by rapid renewable expansion, grid instability challenges, and strong government initiatives supporting transmission modernization.

The Shunt Connection segment dominated due to its cost-effectiveness, simple configuration, and strong suitability for utility and industrial grid stabilization.

Growing renewable energy penetration and rising need for fast, dynamic voltage stabilization are the major factors driving widespread STATCOM deployment globally.

The STATCOM Market size in 2025 was USD 0.72 billion, supported by increasing demand for dynamic voltage regulation and advanced reactive power compensation.

The STATCOM Market is expected to grow at a CAGR of 7.12 from 2026 to 2035, driven by rising renewable integration and grid modernization.

Get in Touch