-

Rising demand for natural, zero-calorie sweeteners is driving steviol glycoside adoption, with the global stevia market growing at a CAGR of over 8–10%.

-

Increasing health concerns such as obesity and diabetes are boosting usage, as over 60% of consumers prefer sugar alternatives with low glycemic impact.

-

Expansion in food & beverage applications (soft drinks, dairy, bakery) is accelerating demand, accounting for over 70% of total steviol glycoside consumption.

-

Technological advancements in purification and Reb M/Reb D production are improving taste profiles, reducing bitterness by 30–40%.

-

Growing adoption in emerging markets across Asia-Pacific and Latin America is driving growth, with these regions contributing over 45% of global demand.

Steviol Glycoside Market Report Scope & Overview:

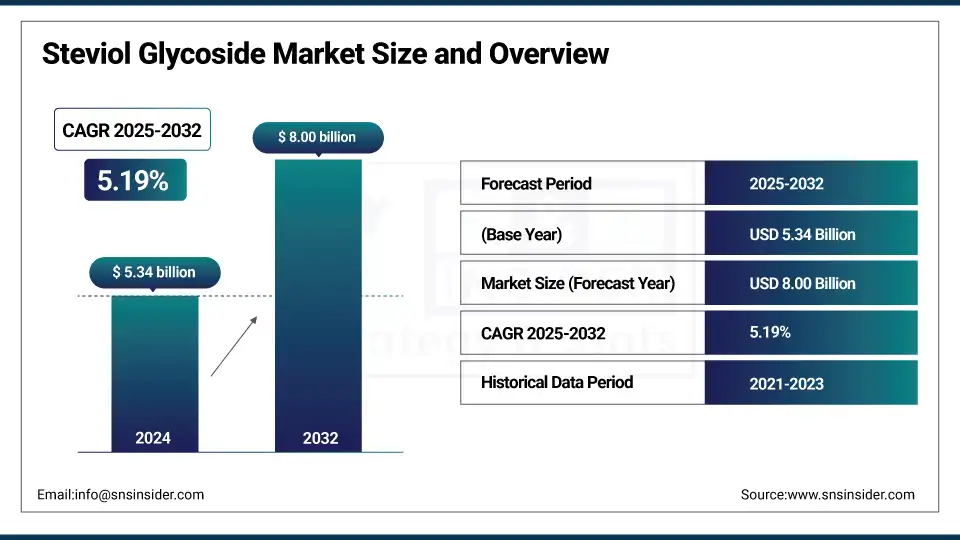

The Steviol Glycoside market size was valued at USD 5.34 billion in 2024 and is expected to reach USD 8.00 billion by 2032, growing at a CAGR of 5.19% over the forecast period of 2025-2032.

Growing interest in clean-label, plant-based sweeteners in line with worldwide sugar-reduction continues to drive the steviol glycoside market. Reformulation in the food and beverage space to meet consumer health preferences and regulatory mandates, such as sugar taxes, with high-purity glycosides. Fermentation-derived production is among the key steviol glycoside market trends that are improving taste and purity. PureCircle has received FDA GRAS for enzyme-modified Rebaudioside M, helping to grow the steviol glycoside market.

Steviol Glycoside Market Size and Forecast

-

Market Size in 2024: USD 5.34 Billion

-

Market Size by 2032: USD 8.00 Billion

-

CAGR: 5.19% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Steviol Glycoside Market - Request Free Sample Report

Steviol Glycoside Market Trends

The FDA has received and reviewed more than 50 GRAS notices for high-purity steviol glycosides, confirming product safety. The market share for steviol glycoside is supported by bio-conversion developments and the trend towards sustainability. Steviol glycoside companies such as Ingredion have ramped up production after taking over PureCircle to meet the increasing market share of steviol glycosides. The market in North America and Asia Pacific for stevia extracts is closely followed by the steviol glycoside merchant market. An innovation case is presented in addition to the safety and scalability drivers in the steviol glycoside market analysis.

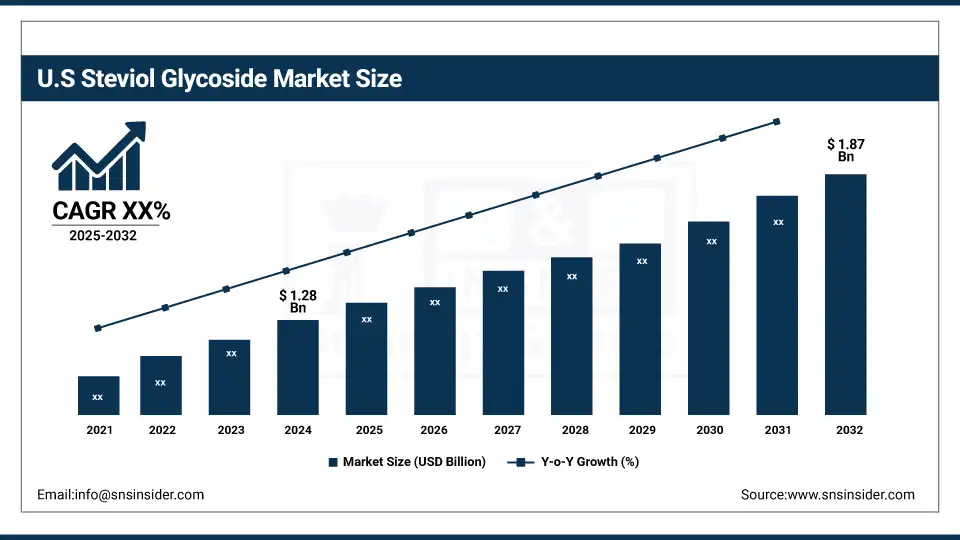

The U.S. dominates the North American steviol glycoside market with a market size of USD 1.28 billion in 2024 and is projected to reach a value of USD 1.87 billion by 2032 with a market share of around 71%. The growth is due to advanced processing infrastructure and regulatory leadership. The FDA’s GRAS Inventory features over 50 listings for steviol glycosides, demonstrating federal confidence in their food use. USDA ERS data indicates an 18% increase in low-calorie sweetener use in packaged goods from 2022 to 2023, driven by consumer health trends. PureCircle’s expansion in Illinois doubled production capacity for enzyme-modified glycosides. These developments contribute to the country’s significant steviol glycoside market share and accelerate clean-label innovation in the broader stevia market.

Market Dynamics:

Drivers:

-

Government sugar-tax policies accelerate steviol glycoside adoption in food and beverage reformulations

Sugar-reduction regulation in more than 30 countries is driving brands to reformulate products with natural alternatives. U.S. low-calorie sweetener use increased by 18 percent in 2023, according to the USDA Economic Research Service. This change is powering this sector, and that is the growth of the steviol glycoside market, mainly in beverages, where brands are looking to keep the taste and reduce the sugar content. Regulatory measures such as the UK soft drinks industry leading levy have also boosted the adoption of stevia in typical products, boosting steviol glycoside market statistics, and extending the world stevia extract industry.

-

Sustainability commitments by steviol glycoside companies drive circular-economy practices across supply chains

Steviol glycoside suppliers are also promoting sustainable farming methods, with Ingredion's partnership with PureCircle in Paraguay aiming to reduce water consumption by 25% and increase the yield of stevia leaf. These initiatives encompass regenerative farming, precision irrigation, and biomass recycling and are in keeping with wider circular economy commitments. This type of measure makes an important contribution to securing raw material supply and to environmental protection. Such advancements play a vital role in the steviol glycoside market growth, supporting brand confidence in natural, responsibly-sourced products and steviol glycoside market trends as businesses aim to gain eco-aware options.

Restraints:

-

Consumer taste perception and lingering bitterness limit mass adoption in certain applications

Despite the better taste of newer glycosides such as Rebaudioside M, a significant number of consumers are still sensitive to aftertaste in products containing stevia. Sensory studies conducted for EFSA suggested that up to 20% of panelists detected bitterness in even the highest purity preparations. This sensory handicap has compromised product acceptability in the dairy, confectionery, and fine beverage industries. Because of this, most steviol glycoside suppliers depend on combining stevia with other sweetening agents. This limits the market trends of steviol glycoside and its potential total substitution of conventional sugar in a wide range of food applications.

Segmentation Analysis:

By Product

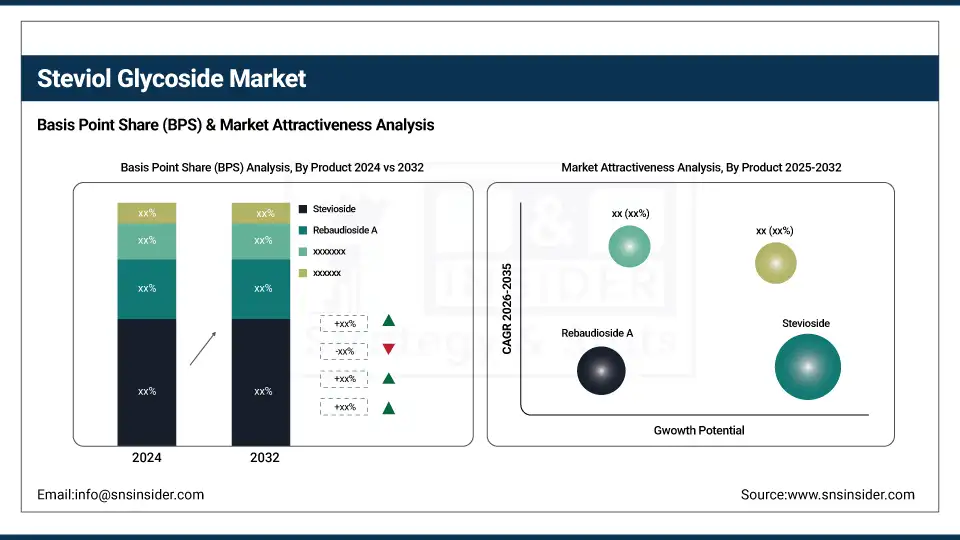

Stevioside dominated the steviol glycoside market in 2024 with a 35.2% share as it is proven to be safe, easily available, and cost-effective. More than 50 GRAS notices on high-purity Stevioside for the U.S. FDA approval have proved its extensive acceptance from a regulatory aspect. Its intensive, bitter-sweet taste is particularly attractive for baked products and other processed products, ensuring broad market acceptance. The long tradition in food and cola soft drink applications enables its domination in the stevia extract market in various regions.

Rebaudioside A is the fastest-growing segment in the steviol glycoside market, expected to grow at a CAGR of 5.68% during 2025–2032. Its clean flavor profile and high perceived sweetness have resulted in it being used in greater volumes in low- and no-calorie beverages. The use of enzyme-converted Rebaudioside A has been internationally accepted with the recent authorisation of the European Food Safety Authority. Advancements in fermentation-based extraction also demonstrate scale, enabling companies to dial down bitterness in their formulas. This is part of a broader development of the increasing trend in market growth of steviol glycosides, using cleaner and better-tasting options.

By Processing Method

Farming-based production led the steviol glycoside market in 2024 with a 60.5% share, owing to its long-established supply chain and raw material availability. Market leaders, including China and Paraguay, have established a strong stevia farming base for global food-grade material. PureCircle and other major steviol glycoside companies are still investing in contract farming models to ensure a consistent supply. The conventional farming methodology still prevails over new technologies employed to produce rebaudioside A and steviol glycosides fields on a broader basis due to the cost efficiency and the available regional farming expertise, and will favor the stevia extract market through 2024.

Fermentation-based production is the fastest-growing processing method in the steviol glycoside market with a CAGR of 5.42% from 2025 to 2032. This allows for the creation of less common glycosides such as Rebaudioside M and D with a good taste profile and lower bitterness. Firms like Evolva and Cargill have also turned to microbial fermentation to help ensure purity, consistency, and sustainability. Moreover, enzyme-converted glycosides have been approved as a safe natural sweetener source by EFSA and FDA, as well, inspiring confidence in industry. These benefits place fermentation as a contemporary alternative supporting market requests for innovation and clean labels.

By End-use

Food applications dominated the steviol glycoside market in 2024 with a 38.3% share on account of the increasing sugar-reduction campaign and processed food reformulation. Steviol glycosides are used in the bakery, confectionery, and ready-to-eat category in the food industry as they are heat-stable and sweet. There was an 18% increase in non-nutritive sweetener use in packaged food that complied with global health guidelines in 2023, according to the USDA. Robust low-sugar foods consumer demand and regulatory backing set food as the leading application segment in continuing steviol glycoside market trends and demand scope.

Beverages are the fastest-growing end-use segment in the steviol glycoside market, projected to expand at a CAGR of 5.57% from 2025 to 2032. International sugar-tax regulations and health trends have led major beverage brands to reformulate with high-purity steviol glycosides. The EFSA and WHO both back the use of stevia in drinks to help cut calories. Coca-Cola, PepsiCo, and Nestlé have extended their product ranges with stevia, consolidating a market trend as a result. Rising consumption of flavored waters, energy drinks, and functional drinks also contributes to the growth in the stevia extract market.

Regional Analysis:

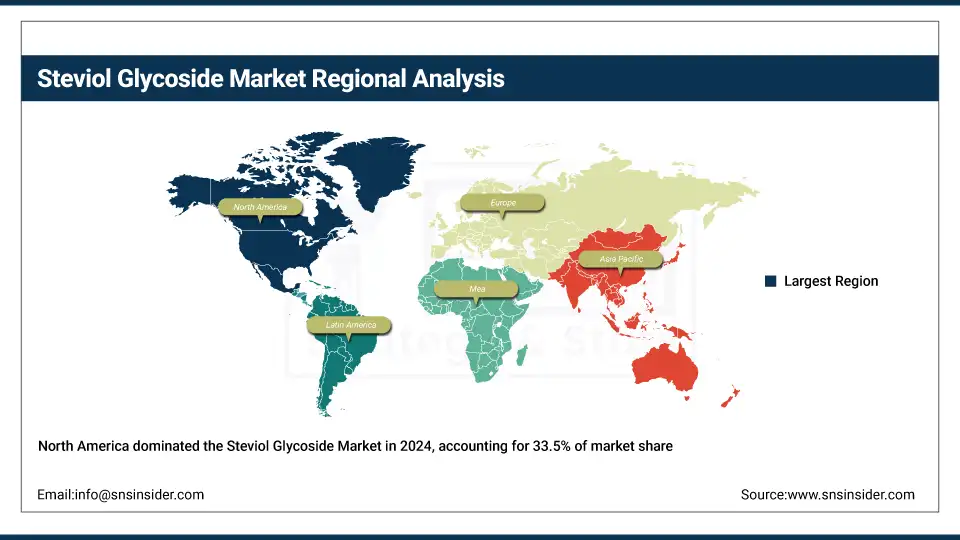

North America held the leading 33.5% steviol glycoside market share in 2024, driven by rising demand for natural sugar alternatives and government-backed health initiatives. The FDA’s GRAS status for over 50 high-purity steviol glycosides facilitated accelerated product approvals, contributing to rapid steviol glycoside market growth. Consumer shift toward clean-label food and beverage products in the U.S. and Canada further supports regional expansion. Major steviol glycoside companies such as PureCircle (Ingredion) expanded their U.S. operations to meet increasing demand, reinforcing North America’s influence in the global stevia extract market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific accounts for 30.1% of the steviol glycoside market and is the fastest-growing region with a CAGR of 5.58%. Its rapid growth is fueled by large-scale stevia cultivation, supportive government farming policies, and surging consumer demand for low-sugar foods. Steviol glycoside companies like Zhucheng Haotian Pharm and GLG Life Tech have scaled production across China and Southeast Asia. The Asia Pacific region benefits from local ingredient sourcing, cost efficiency, and evolving food regulations that favor natural sweeteners, driving strong steviol glycoside market growth and competitive production scale.

China dominates the Asia Pacific steviol glycoside market as the world’s largest stevia leaf cultivator and processor. The Ministry of Agriculture has launched programs supporting high-yield stevia farming, boosting raw material availability. Zhucheng Haotian Pharm’s collaboration with Coca-Cola and PepsiCo to supply high-purity Rebaudioside A showcases China's global role. China exported over 85% of the global stevia raw material in 2023, according to UN Comtrade data. These strategic advancements reinforce China’s leadership in the steviol glycoside industry and enhance the region’s overall stevia extract market strength.

Key Players:

The major steviol glycoside market competitors include Cargill Incorporated, Tate & Lyle PLC, PureCircle (a part of Ingredion), ADM (Archer Daniels Midland Company), Ingredion Incorporated, GLG Life Tech Corporation, HOWTIAN (Zhucheng HaoTian Pharm Co., Ltd.), Evolva Holding SA, Kerry Inc., and Layn Corporation.

Recent Developments:

-

In May 2024, Ingredion launches PureCircle™ Clean Taste Solubility Solution, a “first-of-its-kind” drop-in stevia sweetener that mimics sugar without additives, following global sensory validation

-

In January 2024, Avansya (Cargill-DSM joint venture) secures positive safety opinions from EFSA and the UK FSA for its EverSweet fermentation-derived Reb M/D sweetener, paving the way for EU commercial launches

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.34 billion |

| Market Size by 2032 | USD 8.00 billion |

| CAGR | CAGR of 5.19% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Stevioside, Rebaudioside A, Rebaudioside C, Dulcoside A, Others) •By Processing Method (Fermentation-based Production, Farming-based Production) •By End-use (Food, Beverage, Medicine, Chemicals, Paints & Coatings, Personal Care, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Cargill, Incorporated, Tate & Lyle PLC, PureCircle (a part of Ingredion), ADM (Archer Daniels Midland Company), Ingredion Incorporated, GLG Life Tech Corporation, HOWTIAN (Zhucheng HaoTian Pharm Co., Ltd.), Evolva Holding SA, Kerry Inc., and Layn Corporation |

Frequently Asked Questions

Bitterness perception and aftertaste in stevia-based products limit mass adoption across various premium food categories.

Key manufacturers include Cargill, Tate & Lyle, PureCircle, ADM, Ingredion, GLG Life Tech, and HOWTIAN.

North America and Asia Pacific dominate the steviol glycoside market, supported by regulatory approvals and large-scale production.

The steviol glycoside market is projected to grow at a CAGR of 5.19% from 2025 to 2032.

The global steviol glycoside market was valued at USD 5.34 billion in 2024, reflecting rising clean-label demand.

Get in Touch