US Stormwater Management Market Report Scope & Overview:

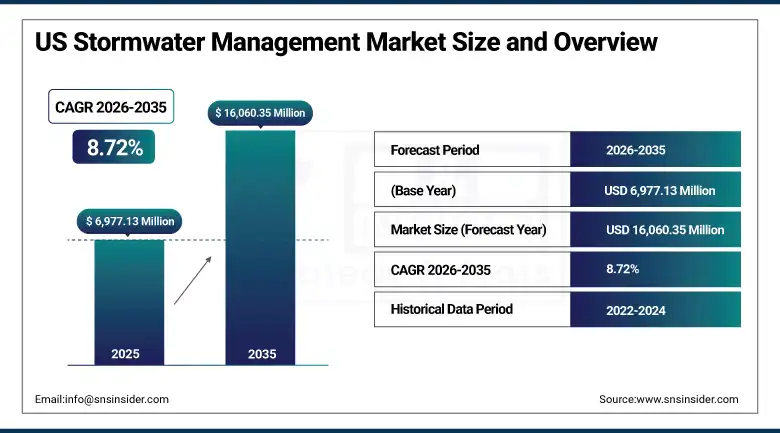

The US Stormwater Management Market was valued at USD 6,977.13 Million in 2025 and is expected to reach USD 16,060.35 Million by 2035, growing at a CAGR of 8.72% from 2026–2035.

The U.S. stormwater management market is a rapidly growing sector focused on the effective control and treatment of stormwater runoff across urban, suburban, and rural landscapes. The market is driven by increasing urbanization, EPA’s National Pollutant Discharge Elimination System Municipal Separate Storm Sewer System permit programme creating regulatory compliance investment motivation, and the extraordinary climate change-driven intensification of precipitation events whose increased runoff volume and pollutant loading exceed legacy stormwater infrastructure design capacity. The Bipartisan Infrastructure Law’s dedicated stormwater infrastructure investment and growing municipal adoption of green infrastructure are collectively transforming the market toward nature-based solutions that create ecological co-benefits beyond hydraulic performance.

In 2024, the EPA finalized its updated NPDES Multi-Sector General Permit for Stormwater Discharges Associated with Industrial Activity (MSGP), strengthening pollutant discharge benchmarks, expanding electronic reporting requirements, and enhancing effluent limitation guidelines for industrial stormwater discharges across 29 industrial sectors. The permit update creates above-average compliance investment from industrial facilities that must implement Best Management Practices documentation, sampling, and corrective action programmes meeting the strengthened discharge quality standards before permit coverage is granted.

Market Size and Forecast

-

Market Size 2026E: USD 7,585.90 Million

-

Market Size 2035: USD 16,060.35 Million

-

CAGR (2026-2035): 8.72% from 2026 to 2035

-

Fastest Growing U.S. Region: West

-

Largest U.S. Region: South

To Get more information On US Stormwater Management Market - Request Free Sample Report

US Stormwater Management Market Trends

-

Rising federal and state investments in resilient stormwater infrastructure driving adoption of advanced stormwater management systems across urban and suburban areas

-

Growing implementation of green infrastructure solutions, including bioswales, permeable pavements, and rain gardens, to improve runoff management and water quality

-

Increasing deployment of smart stormwater monitoring technologies using IoT sensors, real-time analytics, and remote monitoring for efficient drainage system management

-

Expanding focus on flood mitigation, urban resilience, and climate adaptation strategies boosting demand for sustainable stormwater management solutions

-

Strengthening environmental regulations and water quality compliance requirements encouraging municipalities and developers to invest in modern stormwater treatment and retention systems

US Stormwater Management Market Segment Analysis

-

By Service Type, Installation Services segment dominated the US Stormwater Management Market in 2025 with 49% share; Annual Maintenance Services segment is the fastest growing segment.

-

By Solution Type, Detention & Infiltration segment dominated the market in 2025 with 31% share; Biofiltration segment is the fastest growing segment.

-

By Infrastructure Type, Gray Infrastructure segment dominated the market in 2025 with 58% share; Green Infrastructure segment is the fastest growing segment.

-

By End User, Municipal Infrastructure segment dominated the market in 2025 with 42% share; Communities segment is the fastest growing segment.

By Service Type, Installation Services segment dominates the US Stormwater Management Market, Annual Maintenance Services segment expected to grow fastest

The Installation Services segment dominated the US Stormwater Management Market owing to increased investments in the development of stormwater management infrastructure, urban drainage, and flood prevention systems. The increase in construction of residential, commercial and industrial infrastructure has resulted in the demand for professional installation of the systems including detention, drainage, and water management. Environmental laws, aging infrastructure and efficient stormwater management systems are some other factors that have contributed towards the dominance of this segment.

The Annual Maintenance Services segment is the fastest growing in the US Stormwater Management Market owing to the requirement for inspection, cleaning, repair, and performance monitoring of aged stormwater management systems. The increase in regulatory requirements for maintenance along with an increase in severe weather conditions is leading to increased adoption of preventive service agreements. The rising awareness about the longevity and efficiency of operations is further fuelling demand for annual maintenance services.

By Solution Type, Detention & Infiltration segment dominates the US Stormwater Management Market, Biofiltration segment expected to grow fastest

The Detention & Infiltration segment dominated the US Stormwater Management Market as these solutions help minimize stormwater runoff, manage peak discharge, and facilitate groundwater recharge. They find extensive applications in residential, commercial, industrial, and municipal projects in order to comply with stormwater management regulations and mitigate flooding risks. Their reliability, durability, cost-effectiveness, and applicability in both new projects and redevelopment have helped in solidifying their market dominance.

The Biofiltration segment is the fastest growing in the US Stormwater Management Market owing need for sustainable and environmentally friendly stormwater management technologies that filter out pollution and purify water is expected to increase the demand for these solutions. Rising use of green infrastructure, stringent environmental norms, and climate resilience measures will be encouraging their implementation in urban projects. Ongoing efforts towards eco-friendly drainage and LID solutions will fuel the demand even further.

By Infrastructure Type, Gray Infrastructure segment dominates the US Stormwater Management Market, Green Infrastructure segment expected to grow fastest

The Gray Infrastructure segment dominated the US Stormwater Management Market because traditional drainage system, pipes, culverts, retention basins, and underground systems are important in managing stormwater on a wider scale in urban areas. Flood prevention and effective management of stormwater are facilitated through such systems. With continued efforts in improving transport infrastructure, drainage systems, and replacement of aged public systems, gray infrastructure has been dominating the market in recent times.

The Green Infrastructure segment is the fastest growing in the US Stormwater Management Market due to the need for more sustainable urban planning and natural water management solutions. Green gardens, bioswales, pervious pavements, and green roofs manage the amount of runoff, improve water quality, and increase groundwater recharge. The increasing governmental backing and environmental sustainability, as well as increasing low-impact development, have helped achieve this.

By End User, Municipal Infrastructure segment dominates the US Stormwater Management Market, Communities segment expected to grow fastest

The Municipal Infrastructure segment dominated the US Stormwater Management Market owing to the significant amount of investments being made by local governments for developing measures to prevent floods, upgrade drainage, and improve stormwater quality. Local municipal authorities are making efforts to update their infrastructure in view of urbanization trends, changes in rain patterns, and increased environmental compliance standards. Installation of stormwater collection, detention, and treatment systems across cities has helped this market segment retain its dominance.

The Communities segment is the fastest growing in the US Stormwater Management Market owing to increased residential developments and implementation of sustainable stormwater management methods for neighborhoods. Homeowners associations, mixed-use development and residential communities have been installing stormwater management systems that help minimize flooding and conserve water in addition to adhering to environmental regulations. The growing awareness about green infrastructure benefits has been driving demand in this growing end user segment.

Regional Analysis

|

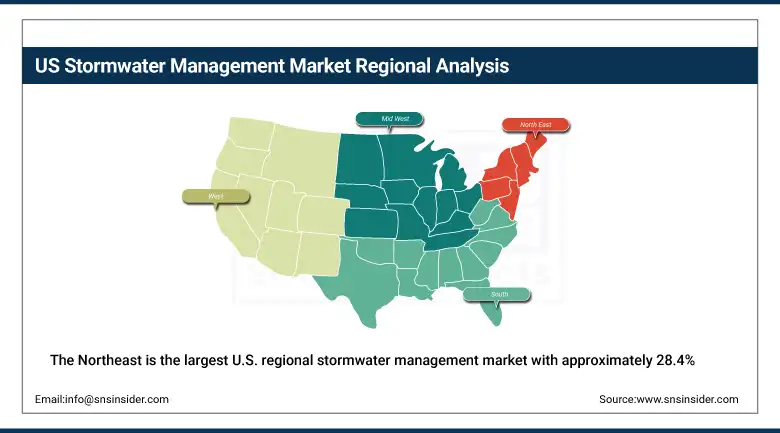

U.S. Region |

Market Share, 2025 (%) |

|---|---|

|

Northeast |

28.4% |

|

Midwest |

21.8% |

|

South |

38.8% |

|

West |

11.0% |

Northeast US Stormwater Management Market Insights

The Northeast accounted for 28.4% of the US Stormwater Management Market in 2025, owing to factors like old urban stormwater drainage systems, population density, and strict environmental policies. States such as New York, Pennsylvania, Massachusetts, and New Jersey have been continually spending on projects for the prevention of combined sewer overflow, green infrastructure, and flood resilience. Urban redevelopment along with the need for meeting federal standards of stormwater quality are expected to increase demand for detention systems and filtration systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Midwest US Stormwater Management Market Insights

The Midwest held 21.8% of the US Stormwater Management Market in 2025, driven by increasing construction and installation of infrastructure and stormwater management in the industrial and residential sectors of development is leading to the growth in this segment. Heavy rainfall, old drainage facilities, and investment in water management solutions are fueling the need for detention basins, infiltration facilities, and filtration technology in the region. Some of the states, such as Illinois, Ohio, Michigan, and Wisconsin, are focusing on protecting their watersheds and flood prevention.

South US Stormwater Management Market Insights

The South dominated a significant 38.8% share of the US Stormwater Management Market in 2025, on account of urbanization, construction, and occurrence of frequent hurricane activity and extreme precipitation. Investments in municipal infrastructure development, flood control, and drainage systems have increased the adoption of techniques such as detention, bio-filtration, and green infrastructure. The states have continuously focused on stormwater management in order to mitigate flood threats.

North Carolina’s post-Hurricane Florence stormwater infrastructure resilience investment, Georgia’s Atlanta metro area’s impervious surface runoff management, and Virginia’s Chesapeake Bay TMDL compliance stormwater investment collectively sustain the Southeast’s fastest-growing regional status.

West US Stormwater Management Market Insights

The West represented 11.0% of the US Stormwater Management Market in 2025, due to greater investments made in water conservation, sustainable city planning, and development of green infrastructure. The implementation of strict environmental policies coupled with the rising fears of droughts, wildfires, and flash floods is driving municipalities towards the use of innovative technologies in stormwater capture, infiltration, and treatment systems. The state of California, Washington, and Oregon are the significant contributors in this region.

Market Dynamics

Growth Drivers: EPA NPDES regulatory compliance and climate resilience infrastructure investment creating structured procurement

EPA’s NPDES MS4 permit programme’s non-discretionary compliance requirement is the U.S. stormwater management market’s most commercially certain structural growth driver. Each MS4 permit renewal cycle that increases Minimum Control Measure specificity, adds enhanced water quality standards, or extends permit coverage to newly regulated municipalities create structured compliance investment whose regulatory non-compliance risk creates procurement motivation independent of budget constraint. EPA’s 2025 MS4 permit rule revision expanding coverage to smaller Phase II communities creates new market entrants whose first-time stormwater programme compliance creates above-average installation service procurement.

Climate change-driven precipitation intensification is creating above-standard stormwater infrastructure investment from the documented increase in 100-year storm event frequency, sea level rise-influenced tidal flooding intersection with stormwater outfall hydraulics, and atmospheric river event runoff volumes exceeding legacy infrastructure design capacity. Each climate event that creates flood damage exceeding design capacity sustains political motivation for above-standard stormwater infrastructure investment whose funding comes from FEMA BRIC, Bipartisan Infrastructure Law, and state resilience programme allocations.

Restraints: High deployment cost and complex maintenance requirement for green infrastructure

The relatively high capital cost of bioretention cell construction, green roof installation, and permeable pavement deployment creates adoption barriers for cost-constrained municipal procurement whose capital budget competition moderates green infrastructure specification pace. Each lifecycle cost analysis that demonstrates green infrastructure’s lower long-term cost than conventional detention basin alternatives require multi-decade planning horizon justification that municipal budget cycles whose annual appropriation focus creates structural difficulty in demonstrating.

Green infrastructure maintenance complexity whose bioretention cell vegetation management, soil media replacement, and inlet debris removal requires specialized ecological expertise and consistent seasonal attention creates operational procurement barriers for municipalities without internal green infrastructure maintenance capability. Each system failure from deferred maintenance that reduces pollutant removal performance creates regulatory compliance vulnerability that sustains pressure for above-standard maintenance investment.

Opportunities: Smart stormwater and PFAS treatment system development

Smart stormwater management system deployment represents the most commercially premium near-term market development whose real-time sensor network, predictive control algorithm, and cloud-based performance monitoring create stormwater asset optimization value substantially exceeding passive infrastructure alternatives. Each smart gate installation that pre-empties detention basins before forecast storm events create quantifiable flood risk reduction whose performance data justifies above-passive-infrastructure capital investment. Opti’s Real-Time Control system, Xylem’s smart water platform, and FlowWorks’ flow monitoring analytics collectively demonstrate the commercial viability of intelligent stormwater infrastructure.

PFAS stormwater treatment system development represents the most commercially significant emerging compliance-driven market opportunity whose EPA’s PFAS maximum contaminant level setting creates treatment requirement for stormwater infiltration adjacent to drinking water sources. Each fire training area, airport runway, and industrial site whose PFAS-laden stormwater requires treatment before discharge or infiltration creates structured specialty treatment system procurement whose per-site cost creates above-average commercial relationship value.

Recent Developments:

-

2026: Stantec Inc. expanded its stormwater engineering and green infrastructure design services in 2026, focusing on MS4 compliance-driven projects and climate adaptation frameworks integrating permeable pavements, bioretention systems, and watershed-scale planning solutions for U.S. municipalities.

-

2025: Advanced Drainage Systems (ADS) expanded its smart stormwater monitoring and detention solutions portfolio in 2025 through enhanced IoT-enabled water level tracking systems and digital drainage analytics platforms for municipal flood risk management applications.

-

2025: Xylem Inc. strengthened its stormwater intelligence capabilities by integrating AI-based real-time flow monitoring and predictive flood modeling solutions into urban water infrastructure networks to support climate-resilient stormwater planning and emergency response systems.

US Stormwater Management Market Key Players are:

-

Advanced Drainage Systems, Inc.

-

Oldcastle Infrastructure

-

Contech Engineered Solutions LLC

-

StormTrap LLC

-

HSI Services, Inc.

-

Jensen Precast

-

Lane Enterprises, Inc.

-

Terre Hill Concrete Products

-

ParkUSA

-

Bio Clean Environmental Services, Inc.

-

AquaShield, Inc.

-

Fabco Industries, Inc.

-

StormwateRx LLC

-

Forterra, Inc.

-

CULTEC, Inc.

-

Prinsco, Inc.

-

The HDPE Company LLC

-

Brentwood Industries, Inc.

-

Modular Wetlands Systems, Inc.

-

CrystalStream Technologies, Inc.

US Stormwater Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6,977.13 Million |

| Market Size by 2035 | USD 16,060.35 Million |

| CAGR | CAGR of 8.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Installation Services, Repair Services, Annual Maintenance Services, Others) • By Solution Type (Detention & Infiltration, Biofiltration, Separation, Filtration, Specialty Filters, Others) • By Infrastructure Type (Green Infrastructure, Gray Infrastructure, Hybrid Infrastructure) • By End User (Individual Homes, Communities, Municipal Infrastructure, Military Bases, Retail and Office Spaces, Hospitality, Others) |

| Regional Analysis/Coverage | Northeast, Midwest, South, West |

| Company Profiles | Advanced Drainage Systems, Inc., Oldcastle Infrastructure, Contech Engineered Solutions LLC, StormTrap LLC, HSI Services, Inc., Jensen Precast, Lane Enterprises, Inc., Terre Hill Concrete Products, ParkUSA, Bio Clean Environmental Services, Inc., AquaShield, Inc., Fabco Industries, Inc., StormwateRx LLC, Forterra, Inc., CULTEC, Inc., Prinsco, Inc., The HDPE Company LLC, Brentwood Industries, Inc., Modular Wetlands Systems, Inc., CrystalStream Technologies, Inc. |

Frequently Asked Questions

Installation Services dominated the US Stormwater Management Market.

The US Stormwater Management Market is expected to grow at a CAGR of 8.72% from 2026 to 2035.

The US Stormwater Management Market was valued at 6,977.13 million in 2025.

South dominated the US Stormwater Management Market in 2025.

EPA’s NPDES MS4 permit programme creating non-discretionary compliance investment across 7,500+ regulated municipalities.

Get in Touch