Strategic Consulting Services Market Report Scope & Overview:

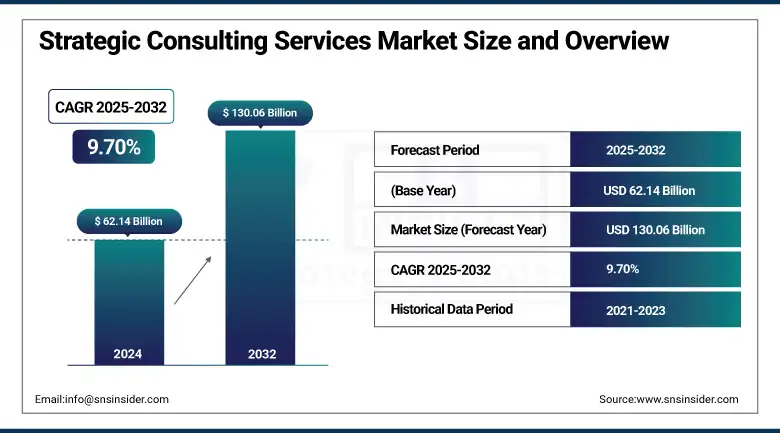

The Strategic Consulting Services Market Size was valued at USD 62.14 billion in 2024 and is expected to reach USD 130.06 billion by 2032 and grow at a CAGR of 9.70% over the forecast period 2025-2032.

The Strategic Consulting Services Market is continuously evolving as organizations face unprecedented pressure to adapt to changing global conditions, technological disruption competitive strategies. They aid businesses to explore avenues to grow, restructure the business, handle mergers and acquisitions, and drive digital transformation. These are key in keeping your business goals in line with the reality of the marketplace and adding value for the long term. The increase in complexity of the decision-making process in BFSI, healthcare, IT & telecom, and manufacturing industries, and the demand for expert-oriented solutions in complex process management, drive the market growth. Innovation in AI, data analytics, and sustainability makes high-value consulting in even greater demand.

To Get more information On Strategic Consulting Services Market - Request Free Sample Report

In the market, AI is significantly improving productivity and reshaping operations. A 2023 study by Harvard Business School and BCG involving 758 consultants showed that those using GPT-4 completed 12.2% more tasks, were 25.1% faster, and achieved over a 40% improvement in output quality. Reports also state that over 160,000 consultants are actively automating repetitive tasks. Additionally, firms like KPMG and PwC are investing $2 billion and $1 billion, respectively, in AI integration initiatives.

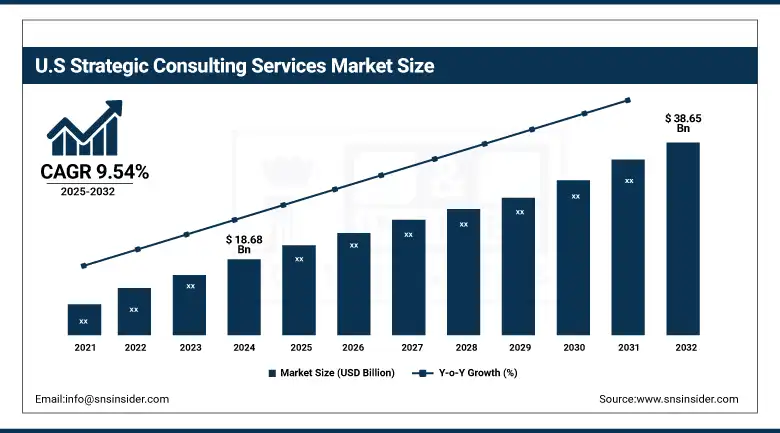

The U.S. Strategic Consulting Services Market size was USD 18.68 billion in 2024 and is expected to reach USD 38.65 billion by 2032, growing at a CAGR of 9.54% over the forecast period of 2025–2032.

Digitalization is being adopted by a variety of industries, which has created a strong demand in the U.S. market for innovation. In North America, the nation ranks first thanks to its sophisticated technology infrastructure, availability of global consulting firms, and adoption of artificial intelligence (AI) and analytics. Sturdy corporate spending in strategy consulting, market complexities, and regulatory environments to sail through further elevates the regional strength of the U.S. as the strategic consulting kingpin.

Strategic Consulting Services Market Dynamics

Key Drivers:

-

Rising Need for Digital Transformation Across Enterprises Drives Strategic Consulting Services Market Expansion Globally

The increasing demand for digital transformation across various industries is a key driver fueling the growth of the strategic consulting services market. Organizations are investing heavily in integrating advanced technologies such as artificial intelligence, cloud computing, and big data analytics to improve operational efficiency, customer experience, and innovation capacity. Strategic consulting firms play a crucial role in helping companies design and implement these digital initiatives by providing expert guidance and tailored strategies. As businesses face rapidly evolving competitive landscapes, consultants assist in navigating technological disruptions and aligning IT capabilities with overall business goals. In March 2023, several top consulting firms expanded their digital advisory portfolios to meet this surging client demand, reflecting the sustained momentum of this growth driver.

Challenges:

-

Complex Regulatory Environments and Compliance Requirements Pose Significant Challenges for Strategic Consulting Services Market Growth

A major restraint in the strategic consulting services market is the complex and ever-changing regulatory landscape that varies widely across industries and regions. Consulting firms must continuously adapt to diverse compliance standards related to data privacy, cybersecurity, environmental laws, and financial reporting. This complexity adds layers of difficulty when designing and executing strategic plans, requiring deep sector-specific knowledge and constant monitoring of legal changes. Additionally, increased regulatory scrutiny raises operational costs and extends project timelines, impacting the overall efficiency of consulting engagements. These regulatory hurdles limit the agility of consulting firms and pose barriers to rapid market expansion, especially in highly regulated sectors such as finance, healthcare, and energy.

Opportunities:

-

Expanding Adoption of AI-Driven Analytics Enhances Strategic Consulting Services Market with Innovative Data-Backed Decision-Making Capabilities

The growing adoption of AI-driven analytics is creating a significant opportunity for the strategic consulting services market by enabling consultants to offer highly precise, data-backed insights. Artificial intelligence tools help analyze large volumes of data quickly, identify emerging trends, and predict market behaviors, which allows consultants to deliver more actionable and tailored recommendations to clients. This technological integration is shifting the consulting industry towards a more analytical, results-oriented model. In January 2024, several leading consulting firms introduced AI-powered decision support platforms, underscoring how AI adoption is transforming service delivery and expanding the scope of strategic consulting. This innovation enhances the value proposition of consulting services, attracting organizations seeking competitive advantages through advanced analytics.

Challenges:

-

Intense Competition Among Consulting Firms Challenges Market Players in Differentiating and Maintaining Profitability

The strategic consulting services market is the intense competition among numerous global and boutique consulting firms striving to differentiate their offerings. With a crowded marketplace, firms find it difficult to stand out based on traditional consulting expertise alone and must constantly innovate to stay relevant. This competitive environment pressures firms to invest heavily in technology, diversify service portfolios, and enhance client relationship management to retain and attract clients. Additionally, increased client expectations for faster, measurable business outcomes have intensified pricing pressures, resulting in narrower profit margins. As a result, maintaining differentiation while ensuring sustainable growth and profitability remains a significant hurdle for market players.

Strategic Consulting Services Market Segmentation Analysis:

By Service Type

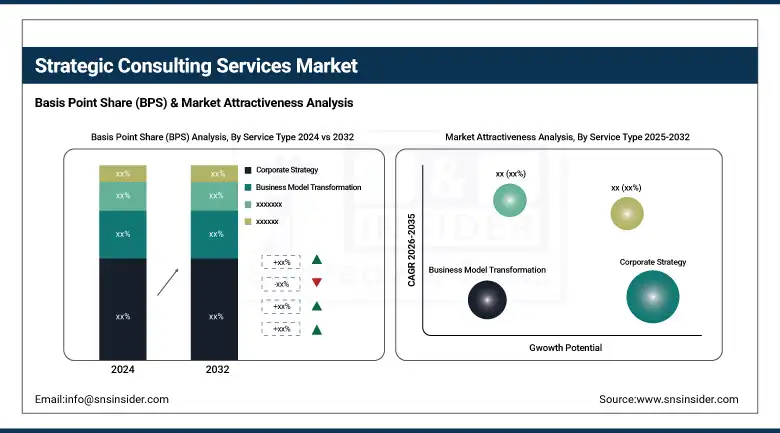

The Corporate Strategy segment leads the market with 28% revenue share due to businesses seeking long-term growth roadmaps amid market uncertainties. Firms like McKinsey and BCG have recently launched specialized corporate strategy frameworks and scenario planning tools to enhance decision-making. This segment’s dominance is tied to growing demand for expert guidance in mergers, acquisitions, and business model innovations, reinforcing its crucial role within the strategic consulting services market in 2024.

The Digital & Operational Strategy segment is expanding rapidly, driven by the need to optimize processes and implement digital technologies. Companies like Accenture and Deloitte launched advanced digital transformation platforms and operational analytics tools in 2023, boosting adoption. This segment’s growth aligns with enterprises prioritizing agility and cost-efficiency, making it a pivotal component of the strategic consulting services market’s future expansion.

By Organization Size

Large enterprises dominate with 72% revenue share due to their extensive consulting needs across global operations. Firms such as PwC and EY have introduced tailored consulting packages targeting complex organizational structures and digital transformation initiatives. This segment’s dominance reflects its strategic importance in driving market growth, as large corporations continue investing heavily in consulting services to maintain competitive advantage and innovate business processes.

The SMEs segment is experiencing rapid growth, fueled by increased awareness of strategic consulting benefits among smaller firms. Startups and mid-sized companies are adopting consulting solutions to scale operations efficiently. Consulting providers like KPMG and Bain launched SME-focused advisory tools in 2023, addressing budget constraints and agility needs. This rising demand makes SMEs a critical growth driver in the strategic consulting services market’s forecast period.

By Industry Vertical

The BFSI sector holds the largest share is 24%, due to ongoing regulatory changes, digital banking adoption, and risk management demands. Leading consulting firms, including Deloitte and Capgemini, launched fintech advisory and compliance services in 2023, enhancing sector-specific expertise. The BFSI segment’s dominance underscores the importance of strategic consulting in navigating market volatility and technology disruption within this highly regulated and dynamic industry.

The Transportation & Logistics sector is rapidly growing, driven by supply chain digitization and efficiency optimization needs. Firms like Kearney and IBM launched blockchain-based logistics solutions and predictive analytics platforms in late 2023. This growth reflects the sector’s increasing reliance on strategic consulting to improve operational visibility, reduce costs, and manage complex global supply chains, positioning it as a key emerging market within strategic consulting services.

By Engagement Model

Project-Based Consulting holds the largest share is 48%, due to its flexibility and clear deliverables suited for specific business challenges. Leading firms such as BCG and Accenture have introduced modular consulting packages and agile project management tools in 2023. This segment’s dominance reflects client preference for defined scope engagements that deliver targeted outcomes, reinforcing its pivotal role within the strategic consulting services market.

Retainer and long-term advisory services are growing rapidly as clients seek continuous strategic support and proactive risk management. Firms like McKinsey and EY launched subscription-based advisory models and digital monitoring platforms in 2023. This trend highlights increasing client preference for sustained partnerships, boosting the segment’s growth potential within the strategic consulting services market.

By Technology Focus

The Data Analytics & BI segment leads with 32% share as businesses prioritize data-driven decision-making. Providers such as IBM and SAS launched enhanced analytics platforms and self-service BI tools in 2023. The segment’s dominance is supported by growing demand for actionable insights, predictive analytics, and visualization capabilities, making it a cornerstone of the strategic consulting services market’s value proposition.

AI/ML Strategy services are the fastest-growing, driven by the need to embed intelligent automation and predictive modeling. Consulting firms like Deloitte and PwC launched AI strategy accelerators and machine learning advisory services in early 2024. This rapid growth reflects organizations’ increasing focus on leveraging AI to enhance innovation, operational efficiency, and competitive advantage, positioning the segment as a future market leader.

Strategic Consulting Services Market Regional Outlook:

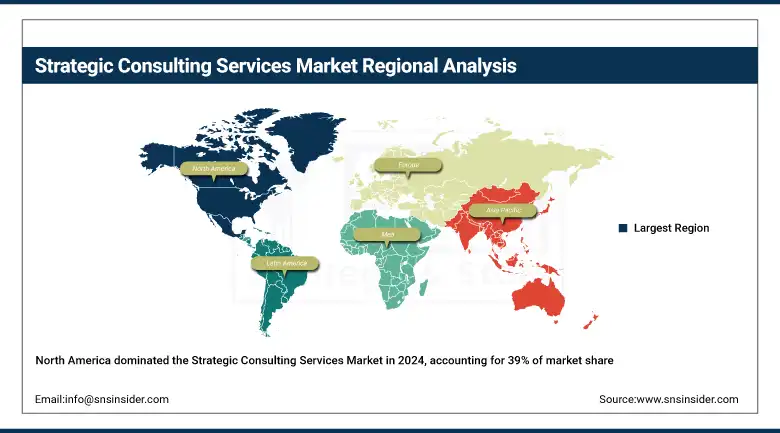

North America Dominates Strategic Consulting Services Market with an Estimated 39% Market Share in 2024. High concentration of multinational corporations and advanced digital infrastructure drives North America’s dominance in the strategic consulting services market growth. The United States is the dominant country in North America’s strategic consulting services market. It leads due to its robust economy, large base of Fortune 500 companies, and early adoption of emerging technologies such as AI, cloud computing, and big data analytics. The U.S. also has a mature consulting ecosystem with numerous global and boutique firms offering specialized services. Strong demand from sectors like finance, technology, and healthcare further solidifies its market leadership in 2024.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing strategic Consulting Services Market with an estimated CAGR of 10.9% in 2024. Rapid industrialization, digital adoption, and expanding SMEs fuel the fast growth of strategic consulting services in Asia Pacific. China dominates the Asia Pacific strategic consulting market, driven by its massive manufacturing base, government support for digital initiatives, and growing corporate investments in strategic planning. The country’s focus on innovation and increasing demand for transformation in sectors like technology, retail, and infrastructure boosts consulting needs. China’s expanding middle class and startup ecosystem also contribute to the surge in demand for expert strategic guidance in 2024.

Europe’s market benefits from a strong emphasis on sustainability, regulatory compliance, and digital innovation, driving demand for strategic consulting across multiple industries. Strict regulatory standards and a focus on sustainability encourage companies to seek strategic consulting for compliance and digital transformation in Europe. Germany leads the region due to its advanced industrial base, technological expertise, and proactive adoption of Industry 4.0. The country’s manufacturing and automotive sectors, coupled with significant investments in green technologies, generate consistent demand for strategic consulting services. Furthermore, evolving EU regulations encourage firms to seek expert guidance for compliance and transformation, reinforcing Germany’s dominance in 2024.

The Middle East & Africa region is witnessing growth due to major infrastructure projects, diversification away from oil dependency, and increasing government investments in technology. Similarly, Latin America’s market expands as countries focus on improving public services, digital adoption, and foreign investments. Both regions see a growing demand for consulting firms to guide large-scale projects and economic reforms. Despite some economic volatility, strategic consulting services are critical in helping businesses and governments navigate complex environments and optimize growth strategies in 2024.

Key Players:

The strategic consulting services market companies are McKinsey & Company, Boston Consulting Group (BCG), Bain & Company, Accenture, Deloitte Consulting, PwC (Strategy&), EY (EY-Parthenon), KPMG, Kearney (formerly A.T. Kearney), Oliver Wyman, and Others.

Recent Developments:

-

In January 2025, McKinsey entered into a strategic alliance with C3 AI, a Silicon Valley-based enterprise artificial intelligence software company. This partnership aims to enhance McKinsey's capabilities in delivering AI-driven solutions to clients, reflecting the firm's commitment to integrating advanced technologies into its consulting services.

-

In April 2025, BCG reported a 10% global revenue growth in 2024, reaching a record $13.5 billion. This growth was driven by increased demand for AI-related advisory services, which accounted for around 20% of total revenue. BCG's investment in AI has been a key driver of the firm's recent growth, collaborating with global technology leaders to integrate AI into business solutions.

-

In February 2025, Bain & Company released its Global M&A Report 2025, indicating that the M&A market is poised for a comeback as headwinds ease. The report highlights that technology disruption, post-globalization, and shifting profit pools will drive dealmaking in the year ahead, with generative AI expected to enable every step of the M&A process in the next five years.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 62.14 Billion |

| Market Size by 2032 | USD 130.06 Billion |

| CAGR | CAGR of 9.70% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Corporate Strategy, Business Model Transformation, Mergers & Acquisitions (M&A), Digital & Operational Strategy, Market Entry & Performance Improvement, and Risk Management, Compliance & Change Management) • By Organization Size (Large Enterprise, Small & Medium Enterprises (SMEs)) • By Industry Vertical (BFSI, IT & Telecom, Healthcare & Life Sciences, Manufacturing, Energy & Utilities, Retail & Consumer Goods, Government & Public Sector, and Transportation & Logistics) • By Engagement Model (Project-Based Consulting, Retainer/Long-Term Advisory, Interim Management, and Training & Workshops) • By Technology Focus (Data Analytics & BI, AI/ML Strategy, Cloud & ERP Consulting, and Cybersecurity Advisory) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | McKinsey & Company, Boston Consulting Group (BCG), Bain & Company, Accenture, Deloitte Consulting, PwC (Strategy&), EY (EY-Parthenon), KPMG, Kearney (formerly A.T. Kearney), Oliver Wyman, and Others. |

Get in Touch