Security And Vulnerability Management Market Report Scope & Overview:

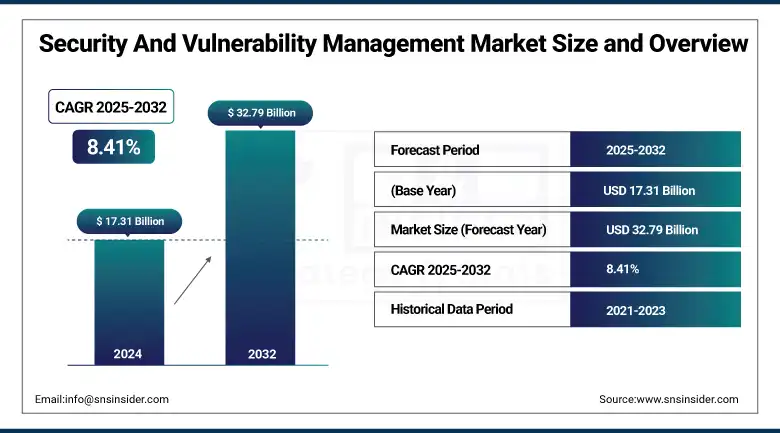

Security And Vulnerability Management Market was valued at USD 17.31 billion in 2024 and is expected to reach USD 32.79 billion by 2032, growing at a CAGR of 8.41% from 2025-2032.

The growth of Security and Vulnerability Management Market is attributed to increasing cyber threats, high adoption of advanced security solutions to identify vulnerabilities, growing digital transformation, high need of regulatory compliance, and the need for preventive measures needed to recognize, detect, and mitigate vulnerabilities across the industries to safeguard sensitive data and maintain continuity of business.

To Get more information On Security And Vulnerability Management Market - Request Free Sample Report

In the U.S., data breaches surged by 78% in 2023 compared to the previous year, despite increased cybersecurity investments highlighting the urgency for robust vulnerability management.

Cloud misconfigurations were responsible for 82% of data breaches in the same year, underlining the importance of secure cloud configurations.

Additionally, legislative efforts such as the UK’s Cyber Security and Resilience Bill (2024) are intensifying compliance requirements and driving organizations to adopt comprehensive security frameworks to meet these standards.

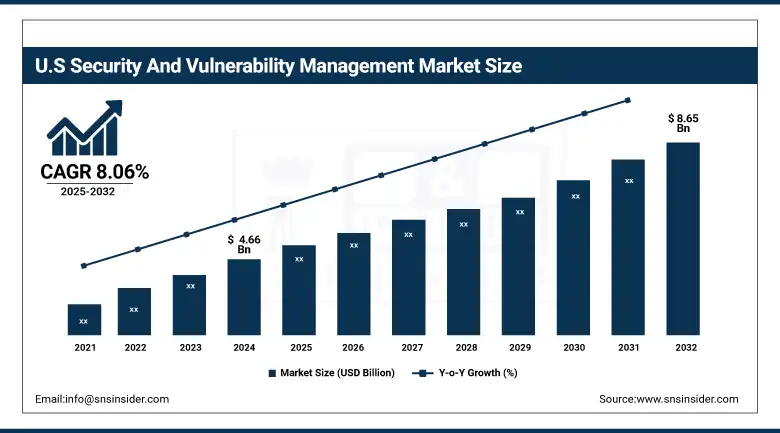

U.S. Security And Vulnerability Management Market was valued at USD 4.66 billion in 2024 and is expected to reach USD 8.65 billion by 2032, growing at a CAGR of 8.06% from 2025-2032.

Rising cyberattacks, need for advanced tools to identify and remediate vulnerabilities in critical infrastructure and enterprises along with increasing adoption of advanced security technologies to comply with government regulations are driving the growth of U.S. Security and Vulnerability Management Market.

To enhance national cybersecurity, the U.S. Department of Homeland Security initiated a $1 billion cyber grant program in September 2022 to support state, local, and territorial governments in addressing cyber risks and strengthening critical infrastructure resilience.

Additionally, the U.S. Department of Commerce has stepped up enforcement under its Information and Communications Technology and Services (ICTS) supply chain rules, focusing on protecting U.S. systems, software, and technology infrastructure from foreign cyber threats.

Security And Vulnerability Management Market Dynamics

Drivers

-

Increasing frequency and sophistication of cyberattacks is accelerating demand for real-time security and vulnerability management solutions globally.

Organizations are dealing with a sudden spike in sophisticated cyber threats including ransomware, zero-days, and targeted attacks, which have led to enterprises transitioning to more proactive and automated security and vulnerability management frameworks. As digital transformation continues to widen attack surfaces across cloud, IoT, and remote infrastructure, organizations have begun to emphasize integrated security more in terms of risk mitigation and compliance obligations. They allow for early detection, coordinated response, and patching of vulnerabilities, reducing the impact on potential disruptions. As a result, cybersecurity has become mission-critical element for operational continuity and brand reputation which is catalyzing huge market growth.

In 2023, ransomware attacks surged by 73% globally, with 6,670 incidents reportedhighlighting the growing scale of such threats. The U.S. healthcare sector was especially targeted, with over 2,800 ransomware complaints and nearly $60 million in adjusted losses.

Zero-day vulnerabilities also intensified, with Google’s Threat Analysis Group and Mandiant documenting 97 such exploits in 2023—a 50% rise from the previous year—further emphasizing the critical need for advanced vulnerability detection and mitigation solutions.

Restraints

-

Shortage of skilled cybersecurity professionals is restricting the effective deployment and optimization of vulnerability management solutions.

Although enterprise needs for sophisticated security technology are increasing, organizations need to find and retain skilled professionals who can deploy, configure, and maintain those systems. Talent at converting risk intelligence into actionable insights, adjusting automated responses, and patching vulnerabilities in a timely manner will remain in demand. These ants are not women: the global cybersecurity workforce gap makes the situation worse for those who do not have access to managed security services. This causes businesses to postpone implementation or utilize the tools as an afterthought, breaking the promise which vulnerability management solutions have to offer proactively as well as limiting the market growth.

Opportunities

-

Increasing focus on AI and machine learning integration is creating innovation opportunities in proactive threat detection and vulnerability prioritization.

An increasingly complex threat environment requires the need for agility and automation of security responses. However, with AI and ML technologies integrated into vulnerability management tools, threat prediction and anomaly detection can be done in real-time as well as the prioritization of vulnerabilities based on exploitability and business impact. These technologies help lessen the manual burdens placed on staff and increase accuracy in the large scale IT environments. With the enterprise trend to automate security operations and achieve predictive insights, solution providers can now Ikigai their efforts – creating differentiation through analytics, adaptive learning, and intelligent automation while transforming traditional vulnerability management into a major strategic cybersecurity enabler.

In March 2023, Microsoft introduced Security Copilot, an AI-powered cybersecurity assistant that integrates GPT-4 with Microsoft’s security tools to enhance real-time threat detection and vulnerability management.

Similarly, IBM incorporates AI in its QRadar Suite, where Watson AI enables faster incident investigation by automatically gathering threat intelligence and prioritizing critical vulnerabilities demonstrating how AI-driven tools are redefining the future of cybersecurity operations.

Challenges

-

Rapidly evolving threat landscape and zero-day vulnerabilities challenge the timeliness and responsiveness of existing security measures.

Cyber adversaries constantly improve strategies, while organisations struggle to catch up with new-found vulnerabilities and unknown attack methods. Zero-days are missed or insights come late when the exploit window for an attack has already compromised the security posture – this is the shortfall of traditional vulnerability scans. The evolution of these threats requires a faster cycle of detection and remediation, much faster than most legacy tools and processes can handle. The new era of adaptive strategies and real-time threat intelligence is at hand, and without it, most organizations are likely to lag behind, creating the so-called agility and proactive defense challenge for IT security in the future.

Security And Vulnerability Management Market Segmentation Analysis

By Component

Software segment held the largest revenue share of nearly 66% in 2024 for the Security and Vulnerability Management Market because of its key function to allow automation, real-time threat detection, and vulnerability assessment in various enterprise environments. Its simplicity of deployment, ongoing updates, and interfacing with security stacks already installed ensure software solutions remain a must-have for compliance and risk management. Businesses give priority to software platforms to support active cybersecurity stances and counter mounting cyber threats effectively.

Services segment is expected to grow at the fastest CAGR of about 9.66% from 2025–2032 due to rising demand for expert-managed security services, consulting, and threat remediation. As organizations face a shortage of skilled professionals, they increasingly outsource vulnerability management tasks to specialized service providers. The growing complexity of IT ecosystems and the need for 24/7 monitoring and response further drive the demand for flexible, cost-efficient security services across various industry verticals.

By Enterprise Size

Large Enterprises segment led Security and Vulnerability Management Market with the largest revenue share of nearly 69% in 2024 because they have large and sophisticated IT infrastructures to monitor vulnerabilities on an ongoing basis. They spend significantly in integrated security solutions to maintain compliance, safeguard information, and minimize operational threats. With large budgets and specialized cybersecurity teams, large enterprises are well-equipped to deploy and expand advanced vulnerability management systems to global operations.

SMEs segment will grow at the fastest CAGR of nearly 9.67% from 2025–2032 due to rising occurrences of planned cyberattacks on small businesses. As knowledge about cybersecurity increases and cost-effective, cloud-based software becomes increasingly available, SMEs are increasing spending on vulnerability management. Regulatory compliance forces and dependence on digital operations also fuel growth, encouraging smaller enterprises to implement proactive security software to protect confidential customer and business information.

By Deployment

Cloud segment led the Security and Vulnerability Management Market with the largest revenue share of nearly 58% in 2024 owing to the extensive use of cloud infrastructure across sectors. Cloud-based solutions are preferred by organizations for their scalability, flexibility, and capacity to provide real-time updates and centralized visibility of threats. As more workloads migrate to public and hybrid clouds, securing virtual environments has emerged as a strategic imperative, driving robust demand for cloud-native vulnerability management software.

On-premises segment will register the fastest growth CAGR of approximately 9.34% during 2025–2032 as a result of increased demand from regulated sectors that value control, data sovereignty, and tailored security policies. Healthcare, defense, and financial industries remain dependent on on-premises systems to maintain adherence to stringent data protection regulations. With the cloud breach concerns still lingering, most organizations are rediscovering strong on-premises vulnerability management infrastructure.

By Vertical

Defense/Government sector led the Security and Vulnerability Management Market with the largest revenue share of nearly 24% in 2024 because of their mission-critical, high-value information and continuous exposure to nation-state attacks. These industries are under strict security requirements, necessitating sophisticated vulnerability assessment technologies and ongoing vigilance. National cybersecurity programs also impose security and systems expenditure to safeguard infrastructure, networks, and sensitive information, ensuring government and defense sectors are major drivers of market leadership.

BFSI segment will increase at the fastest CAGR of approximately 9.74% from 2025–2032 as a result of growing digitization, online payments, and regulatory oversight. Banks encounter growing volumes of cyber attacks against customer information and payment infrastructures. To manage risks and uphold trust, the industry is spending money on next-generation vulnerability management solutions that have automated threat intelligence and compliance features. The demand for business continuity also speeds up the adoption of security within this sector.

By Type

Infrastructure Protection segment led the Security and Vulnerability Management Market with the largest revenue share of approximately 25% in 2024 owing to increased investment in the protection of strategic assets like energy grids, transportation networks, and industrial control systems. As these systems get increasingly digitized and integrated, they are increasingly vulnerable to cyber threats. Businesses and governments put infrastructure protection high on their agenda to avoid widespread disruptions and meet aggressive sector-specific security requirements.

Cloud Security segment shall grow at the fastest CAGR of around 9.45% from 2025–2032 due to increasing dependence on cloud computing and rising complexity in securing multi-cloud environments. Organizations are moving sensitive workloads to the cloud, and cloud-specific vulnerability management becomes crucial. Real-time monitoring, policy compliance, and threat response for dynamic virtual infrastructures are creating strong demand for sophisticated cloud security solutions specifically designed for distributed architectures.

By Target

Content Management Vulnerabilities segment led the Security and Vulnerability Management Market with the maximum revenue share of approximately 36% in 2024 owing to extensive deployment of CMS platforms such as WordPress, Drupal, and Joomla that are common targets for attacks. These platforms typically store sensitive information and are susceptible to unpatched plugins and misconfigurations. Businesses from all industries make it a top priority to lock down CMS environments since attacks can result in data leaks, defacement, and reputational loss.

API Vulnerabilities segment shall grow at the highest CAGR of around 10.14% from 2025–2032 owing to the proliferation of API adoption in cloud-native and mobile-first applications. As APIs grow more indispensable for data exchange and service integration, they also introduce new surfaces of attack. Organizations are making larger investments in solutions to discover, track, and counter API-level vulnerabilities. The adoption of microservices and third-party integrations only fuel this growth pattern.

Security And Vulnerability Management Market Regional Outlook

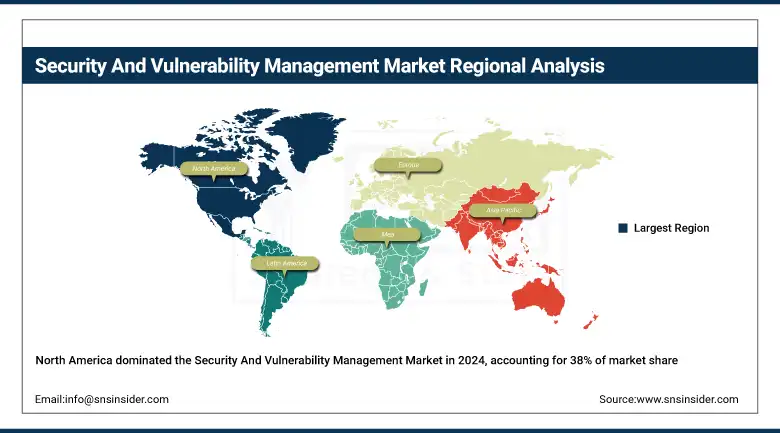

North America dominated the Security and Vulnerability Management Market in 2024 with the highest revenue share of about 38% due to developed cybersecurity infrastructure in the region, strict regulatory frameworks and enterprises adopting complex security solutions. Moreover, the rise in cyber threats coupled with the rising awareness of data protection among the government and private sectors have led to large investments, further consolidating North America in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The US dominated the Security and Vulnerability Management Market due to advanced cybersecurity infrastructure, high cyberattack incidents, strict regulations, and significant investments in security solutions.

Asia Pacific is expected to grow at the fastest CAGR of about 10.51% from 2025 to 2032 owing to rapid digital transformation, growth in IT and telecommunications sectors, and rising awareness of cybersecurity among emerging economies. Several factors, such as increased cloud adoption along with the growing number of cyberattacks along with government initiatives to enhance cybersecurity frameworks in China, India, and Japan, are expected to assist in domineering the pace of the growth of the market in the region

China is dominating the Asia Pacific Security and Vulnerability Management Market due to rapid digitalization, large IT infrastructure investments, growing cyber threats, and strong government cybersecurity initiatives.

Europe holds a significant share in the Security and Vulnerability Management Market due to stringent data protection regulations, increasing cyber threats, and growing adoption of advanced security technologies by enterprises and government organizations to safeguard sensitive information.

The UK is dominating the European Security and Vulnerability Management Market due to its strong cybersecurity regulations, advanced technology adoption, and significant investments in digital security.

Middle East & Africa and Latin America are witnessing steady growth in the Security and Vulnerability Management Market driven by increasing digitalization, rising cyber threats, growing government initiatives to improve cybersecurity infrastructure, and expanding awareness among businesses about data protection.

Key Players

AT&T Intellectual Property, CrowdStrike, Cisco Systems, Inc., Fortra, LLC, IBM Corporation, Microsoft, Qualys, Inc., Rapid7, RSI Security, Tenable, Inc and others.

Recent Developments:

-

In March 2025, CrowdStrike introduced an AI-powered Network Vulnerability Assessment within its Falcon Exposure Management platform, enabling real-time risk prioritization for network assets without additional hardware.

-

In April 2025, Rapid7 enhanced its Managed Detection and Response (MDR) service with a new Detection & Response Dashboard and AI Alert Triage Transparency, offering improved visibility into threats and AI-driven decisions.

-

In December 2024, Tenable launched Tenable Patch Management, an autonomous solution designed to streamline vulnerability remediation by automating patch deployment and reducing exposure windows.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 17.31 Billion |

| Market Size by 2032 | USD 32.79 Billion |

| CAGR | CAGR of 8.41% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Type (Endpoint Security, Cloud Security, Network Security, Application Security, Infrastructure Protection, Data Security, Others) • By Target (Content Management Vulnerabilities, IoT Vulnerabilities, API Vulnerabilities, Others) • By Deployment (Cloud, On-premises) • By Enterprise Size (Large Enterprises, SMEs) • By Vertical (BFSI, Healthcare, Defense/Government, IT and Telecom, Energy, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | AT&T Intellectual Property, CrowdStrike, Cisco Systems, Inc., Fortra, LLC, IBM Corporation, Microsoft, Qualys, Inc., Rapid7, RSI Security, Tenable, Inc. |

Frequently Asked Questions

North America dominated with about 38% revenue share due to advanced cybersecurity infrastructure and stringent regulations.

Infrastructure Protection led with about 25% revenue share due to investments in securing critical assets like energy grids and transport networks.

Increasing cyber threats and rising adoption of advanced security solutions across industries are the key growth drivers.

The security and vulnerability management market was valued at USD 17.31 billion in 2024.

The security and vulnerability management market is expected to grow at a CAGR of 8.41% during 2025–2032.

Get in Touch