Sulfur-Based Micronutrients Market Report Scope & Overview:

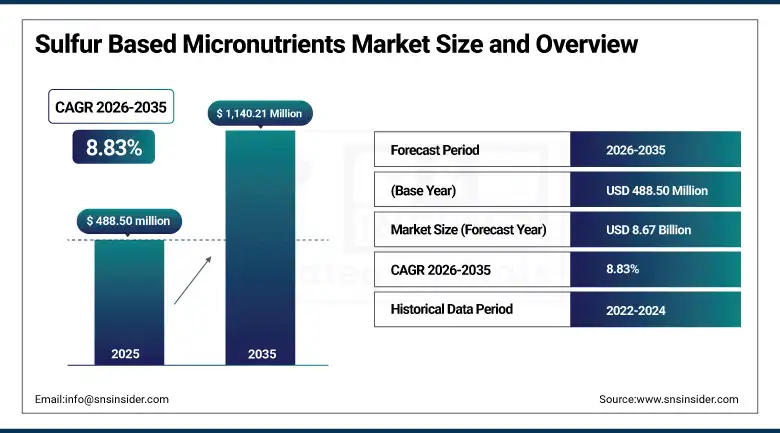

The Sulfur-Based Micronutrients Market was valued at USD 488.50 Million in 2025 and is expected to reach USD 1,140.21 Million by 2035, growing at a CAGR of 8.83% from 2026–2035.

The global sulfur-based micronutrients market is experiencing sustained commercial growth as the agricultural sector confronts a systemic and widening sulfur deficiency crisis whose consequences for crop yield and quality are compelling farmers, agronomists, and government agencies to systematically integrate sulfur into balanced fertilizer programmes. Sulfur is an essential macronutrient for plant protein synthesis, chlorophyll formation, enzyme activity, and oil quality in oilseed crops, but its progressive depletion from agricultural soils due to reduced atmospheric sulfur deposition, intensive cropping without supplementation, and the near-universal transition to high-analysis sulfur-free fertilizers has created a widespread deficiency that now affects hundreds of millions of hectares of cropland across Asia Pacific, Europe, and North America. Sulfur-bentonite-zinc formulations have emerged as the commercially dominant product category because they simultaneously address sulfur and zinc deficiencies that co-occur across the same soil types, delivering dual-nutrient correction in a single cost-efficient granular application that is compatible with existing bulk blending and broadcasting equipment.

Yara International launched its Sulfan sulfur-bentonite product range expansion into South Asian markets in 2024, specifically targeting wheat and canola growing regions across India and Bangladesh where soil sulfur deficiency is confirmed across more than 60% of tested agricultural land. The expansion reflects the commercial recognition that South Asia represents the most commercially significant underserved market for sulfur-based micronutrient products whose adoption is constrained by awareness and distribution infrastructure rather than agronomic need.

Market Size and Forecast

-

Market Size in 2026E: USD 531.60 Million

-

Market Size by 2035: USD 1,140 Million

-

CAGR: 8.83% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Sulfur Based Micronutrients Market - Request Free Sample Report

Sulfur-Based Micronutrients Market Trends

-

Rising global soil sulfur deficiency is increasing demand for sulfur-based micronutrient fertilizers.

-

Growing adoption of controlled-release sulfur formulations is improving nutrient efficiency and reducing losses.

-

Increasing integration with precision agriculture is enhancing sulfur application accuracy and productivity.

-

Expanding government subsidy programs are supporting sulfur micronutrient adoption in major agricultural markets.

-

Rising oilseed crop cultivation is driving higher demand for sulfur-based nutrient solutions globally.

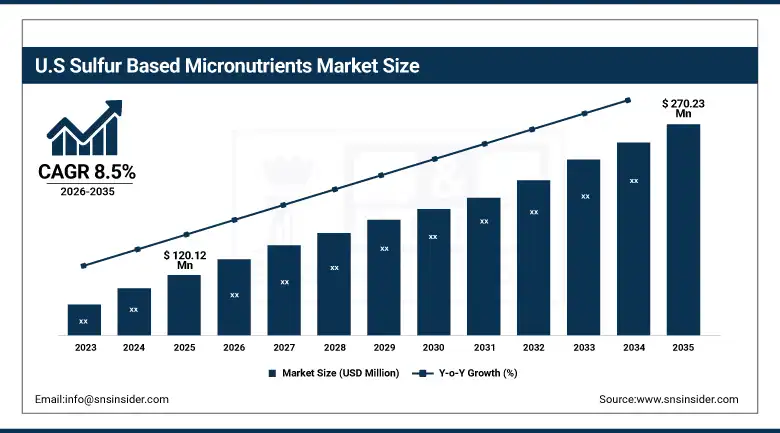

The U.S. Sulfur-Based Micronutrients Market Outlook

The U.S. Sulfur-Based Micronutrients Market was valued at approximately USD 120.12 Million in 2025 and is expected to reach approximately USD 270.23 Million by 2035, growing at a CAGR of approximately 8.5%.

Demand in the U.S. market is driven by the progressive recognition among American agronomists and crop advisors that sulfur deficiency is now a commercially significant yield-limiting factor across the corn belt, wheat belt, and oilseed growing regions whose soils have been progressively depleted of sulfur as atmospheric deposition has declined by over 60% since the Clean Air Act’s SO2 emission controls took effect. North American soil test data consistently shows that sulfur deficiency is now as commercially important as traditional macronutrient deficiencies in limiting maximum economic yield across canola, corn, alfalfa, and wheat production systems. Tiger-Sul Products’ sulfur-bentonite product range and Nutrien’s specialty nutrition products collectively serve the majority of U.S. commercial farmer demand for sulfur-based micronutrient correction, distributed through the cooperative and retailer agronomy network that defines the American fertilizer market’s commercial infrastructure.

Tiger-Sul Products expanded its sulfur-bentonite product range in 2024 with new combination micronutrient grades including sulfur-bentonite-zinc and sulfur-bentonite-boron formulations targeting the corn and canola growing regions where co-occurring micronutrient deficiencies are progressively identified in commercial soil testing programmes as limiting crop response to primary macronutrient applications that fail to reach maximum yield potential without adequate micronutrient correction.

Sulfur-Based Micronutrients Market Segment Analysis

-

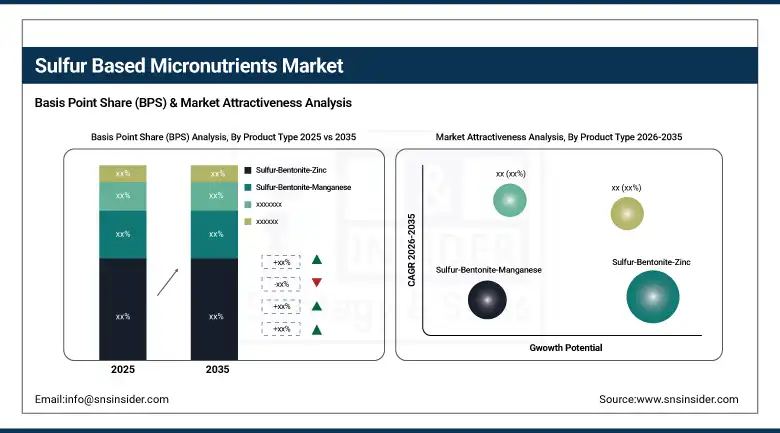

By Type, sulfur-bentonite-zinc segment dominated the sulfur-based micronutrients market with 38.5% share in 2025. While the sulfur-bentonite-manganese segment is the fastest growing during 2026–2035.

-

By Form, solid segment dominated the sulfur-based micronutrients market with over 55% share in 2025. While the liquid segment is the fastest growing during 2026–2035.

-

By Application, cereals & grains segment dominated the sulfur-based micronutrients market with 37.9% share in 2025. While the oilseeds & pulses segment is the fastest growing at a CAGR of 9.67% during 2026–2035.

-

By Mode of Application, the soil application segment dominated the sulfur-based micronutrients market in 2025. While the fertigation segment is the fastest growing.

By Type, sulfur-bentonite-zinc dominates, sulfur-bentonite-manganese grows fastest

Sulfur-bentonite-zinc retained the dominant type position with 38.5% of the sulfur-based micronutrients market in 2025. Its commercial primacy reflects the extraordinary geographic prevalence of the sulfur-zinc co-deficiency that this formulation addresses simultaneously. Global soil surveys consistently identify sulfur and zinc as the two most commercially significant micronutrient deficiencies affecting crop yield across the calcareous soils of South Asia, the intensively cropped soils of China and Southeast Asia, and the sandy or low organic matter soils of North America and South America where both nutrients are subject to leaching and crop removal without replenishment. The dual-deficiency correction logic of sulfur-bentonite-zinc is compelling from a farm economics perspective: one product application corrects two yield-limiting deficiencies at a combined cost substantially lower than two separate micronutrient applications, creating a clear financial justification that facilitates agronomist recommendation and farmer adoption without requiring extensive economic analysis.

Sulfur-bentonite-manganese is the fastest-growing type as expanding soil testing programmes and agronomist awareness are identifying manganese deficiency as a more widespread yield-limiting factor than previously recognized, particularly in high-pH soils resulting from heavy liming practices whose elevated pH reduces manganese plant availability below the threshold for adequate enzyme function and photosynthetic activity. The combined sulfur-manganese formulation is commercially attractive because the sulfur bentonite carrier’s acidifying effect in the soil zone immediately surrounding each granule temporarily improves manganese solubility and plant availability as the product disperses, creating a synergistic delivery mechanism that makes the combined product agronomically superior to separate sulfur and manganese applications in high-pH soil environments.

By Application, cereals & grains dominate, oilseeds & pulses grow fastest

Cereals and grains retained the dominant application position with 37.9% of the sulfur-based micronutrients market in 2025, a commercial dominance that reflects the foundational position of wheat, rice, maize, barley, and millet as the world’s highest-acreage crop categories whose aggregate sulfur requirement represents the single largest demand pool for sulfur-based micronutrient products globally. Sulfur’s role in cereal crop nutrition extends beyond simple yield improvement into grain quality determination: wheat protein content and baking quality, malt barley protein specification compliance, and rice milling quality are each directly influenced by sulfur availability during grain fill, creating agronomic and commercial quality incentives for sulfur application that reinforce the yield maximization motivation. In major wheat-producing regions including India, Pakistan, Bangladesh, China, and Eastern Europe, sulfur deficiency is now identified as one of the primary constraints on closing the gap between actual and potential wheat yield, creating sustained institutional and farmer motivation for sulfur-based micronutrient programme development.

Oilseeds and pulses are the fastest-growing application at a CAGR of 9.67% through 2035, driven by the extraordinary global expansion of oilseed crop acreage whose biofuel mandate, food oil demand, and protein meal supply requirements collectively create consistently growing canola, soybean, sunflower, and mustard acreage that generates proportional sulfur demand. Oilseed crops have the highest sulfur requirement per hectare of any major crop category because sulfur is a direct component of the glucosinolate and protein molecules that define oilseed quality, making sulfur availability during pod fill and seed development a primary determinant of oil content, protein quality, and crop marketability. The global expansion of rapeseed and canola cultivation into new growing regions in Eastern Europe, Russia, Kazakhstan, and Australia is simultaneously creating new geographic demand pools for sulfur-based micronutrient products whose agronomic necessity in high-yielding oilseed production is well-established.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

India |

32.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Sulfur-Based Micronutrients Market Insights

North America is a significant and commercially sophisticated sulfur-based micronutrients market where the established precision agriculture infrastructure, commercial agronomy advisory services, and large-scale commodity crop farming operations create both the technical capability and commercial motivation for systematic sulfur programme development. The United States accounts for approximately 82.5% of North American revenues through its combination of large-scale canola, corn, wheat, and alfalfa production regions where sulfur deficiency is increasingly confirmed in commercial soil testing and where yield response data from university extension programmes and private agronomists is progressively compelling large-scale operator adoption of sulfur supplementation programmes.

Canada is a particularly commercially significant market for sulfur-based micronutrients as the country’s vast canola production, whose Prairie Province acreage represents the world’s largest single national canola crop, generates the highest aggregate oilseed sulfur demand of any national market outside South Asia. Tiger-Sul Products’ Canadian headquarters and Tiger-Sul’s established distribution network across Prairie Province agri-retail serve this demand with a product range specifically developed for the agronomic and soil conditions of Canadian canola and wheat production.

Europe Sulfur-Based Micronutrients Market Insights

Europe is a mature and commercially active sulfur-based micronutrients market where the dramatic reduction in atmospheric sulfur deposition from coal-burning power stations since the 1990s has created a progressive cropland sulfur deficiency that is well-documented in national soil surveys and whose correction is increasingly incorporated into standard agronomic recommendations for oilseed rape, wheat, barley, and grassland production across the United Kingdom, Germany, France, and Scandinavia. Germany accounts for approximately 22.3% of European revenues through its large oilseed rape and cereal production base whose high-yield farming systems’ sulfur demand is served by an established agri-retail distribution network distributing sulfur-bentonite and ammonium sulphate products to commercial farm operators.

The United Kingdom is Europe’s most commercially advanced market for sulfur-based micronutrient adoption, where AHDB Arable’s sulfur advisory framework and the Fertilizer Industry Association’s systematic sulfur education programme have successfully established sulfur application as a standard agronomic practice in oilseed rape and spring cereal production. UK oilseed rape’s elevated sulfur requirement combined with the country’s historically well-documented sulfur deficiency following the removal of SO2 atmospheric deposition created the clearest agricultural economic case for sulfur investment that has driven adoption rates materially above the European average.

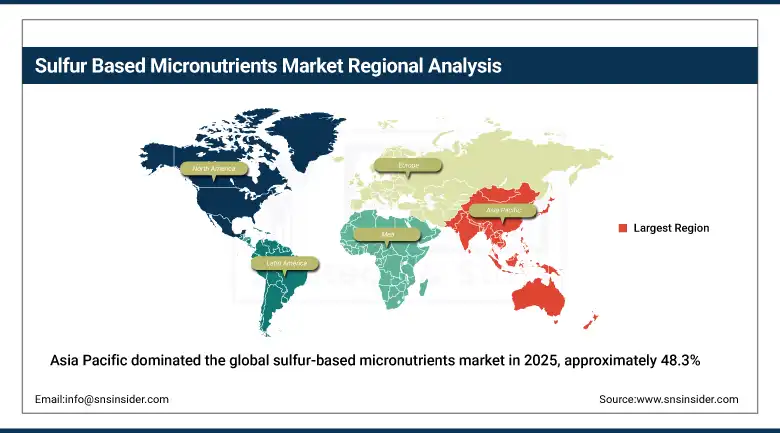

Asia Pacific Sulfur-Based Micronutrients Market Insights

Asia Pacific dominated the global sulfur-based micronutrients market in 2025, accounting for approximately 48.3% of global revenues, driven by the region’s combination of the world’s largest agricultural land area, the highest documented prevalence of sulfur-deficient soils, and rapidly growing government and institutional support for micronutrient fertilizer adoption. India accounts for approximately 32.6% of Asia Pacific revenues as the most commercially significant growth market, where soil sulfur deficiency affects over 60% of agricultural land tested and where the Indian Council of Agricultural Research’s systematic promotion of sulfur application in wheat, mustard, and rice production is progressively translating agronomic awareness into commercial fertilizer market demand.

China, Bangladesh, and Southeast Asian nations represent significant secondary markets within Asia Pacific where intensive rice and vegetable production on heavily depleted soils creates structural sulfur deficiency that commercial fertilizer programmes are progressively addressing through sulfur-enriched NPK blends and standalone sulfur-based micronutrient products. IFFCO and Coromandel’s domestic manufacturing capabilities in India and growing distribution infrastructure in Bangladesh and Southeast Asia are progressively making affordable sulfur-based micronutrient products accessible to smallholder farmers whose adoption is the most commercially significant near-term growth driver in the regional market.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Sulfur-Based Micronutrients Market Insights

The Middle East and Africa and Latin America are growing sulfur-based micronutrients markets where expanding agricultural intensification, increasing government support for micronutrient fertilization, and the progressive adoption of precision agriculture soil testing are creating structured demand for sulfur-based products. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its protected and greenhouse horticulture sector’s intensive production whose soil sulfur depletion rates create consistent micronutrient supplementation requirements, and the country’s grain and vegetable production programmes under Vision 2030’s agricultural self-sufficiency agenda.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its extraordinary agricultural productivity, whose soybean, sugarcane, maize, and coffee production systems generate sulfur demand at the scale of the world’s largest tropical agricultural system. Brazilian soil science research on the interaction between sulfur availability and soybean yield in the Cerrado production system has established a compelling agronomic evidence base that is progressively driving sulfur-based micronutrient adoption among large-scale commercial producers whose average farm size makes micronutrient investment economically justifiable relative to yield improvement benefits.

Market Dynamics

Growth Drivers: Rising soil sulfur deficiency, expanding oilseed crop cultivation, and growing adoption of precision agriculture are driving demand for sulfur-based micronutrients globally.

The progressive depletion of sulfur reserves in agricultural soils is the market’s most structurally certain long-term commercial growth driver. Atmospheric sulfur deposition has declined by 60 to 80% across North America and Europe since industrial emission controls took effect, removing a previously reliable background sulfur input that masked deficiency in many farming systems. Simultaneously, the intensification of crop production and the universal adoption of high-analysis sulfur-free fertilizers have accelerated soil sulfur removal without replacement, creating a widening deficiency whose severity is confirmed in progressively more soil testing programmes. This structural depletion dynamic creates a growing need for active sulfur supplementation that is independent of commodity price cycles and farming economic conditions, sustaining consistent market demand growth.

Oilseed crop expansion is simultaneously creating the market’s fastest-growing demand segment because oilseed crops’ sulfur requirement per hectare substantially exceeds that of cereal crops, and because the global expansion of canola, soybean, sunflower, and mustard acreage driven by biofuel mandates and food oil demand is creating proportional growth in the aggregate sulfur demand that fertilizer programmes must satisfy to achieve maximum yield potential. Each percentage point increase in global oilseed acreage creates above-proportional sulfur-based micronutrient demand growth whose compounding with expanding precision agriculture soil test coverage progressively converts latent agronomic need into commercial purchase decisions.

Restraints: Limited farmer awareness, competition from low-cost elemental sulfur alternatives, and inconsistent government subsidy programs are restraining sulfur-based micronutrients market growth.

Low farmer awareness of sulfur deficiency’s visual symptoms and its distinction from other nutrient disorders or crop stress factors represents the most commercially significant adoption barrier in developing market smallholder farming communities where agronomic extension service coverage is limited. Unlike nitrogen deficiency, whose yellowing leaf symptoms are familiar to most farmers, sulfur deficiency’s similar but more leaf base-concentrated chlorosis is frequently misdiagnosed or attributed to other causes, delaying the adoption of sulfur correction programmes that soil testing would quickly identify as commercially justified.

Competition from elemental sulfur as a lower-cost alternative to sulfur-bentonite and speciality sulfur micronutrient formulations creates margin pressure for value-added product manufacturers. Elemental sulfur’s much lower cost per kilogram of sulfur delivered makes it commercially attractive for large-scale applications where agronomic precision and multi-nutrient combination value are less important than absolute cost per hectare correction. The slower oxidation rate of fine elemental sulfur particles relative to sulfur-bentonite formulations whose bentonite dispersant improves contact with soil microorganisms reduces elemental sulfur’s agronomic equivalence in some soil types, creating a performance-based commercial case for premium formulations that must be communicated clearly to overcome the price differential barrier.

Opportunities: Expanding micronutrient subsidy programs, controlled-release fertilizer innovation, and precision soil testing integration are creating growth opportunities in the sulfur-based micronutrients market.

India’s National Mission for Sustainable Agriculture’s micronutrient component and the government’s Soil Health Card scheme create institutional channels through which sulfur deficiency identification is translating into government-backed recommendation and subsidy support for sulfur-based micronutrient application across the country’s vast smallholder farming population. Each Soil Health Card distributed in a sulfur-deficient district creates a government-endorsed recommendation that commercial fertilizer distributors can leverage to develop retail sales, connecting the institutional agronomic awareness that government programmes create with the commercial distribution infrastructure that serves the Indian agricultural market.

Controlled-release sulfur fertilizer innovation represents a high-value commercial development opportunity whose polymer-coated and chemically stabilized formulations improve sulfur use efficiency by releasing plant-available sulfate progressively over the crop growing season rather than in a single flush following application. The premium pricing that proven controlled-release formulations command relative to standard sulfur-bentonite products creates a commercially attractive high-margin product development pathway for sulfur-based micronutrient manufacturers whose investment in controlled-release technology provides competitive differentiation and improved farmer ROI outcomes that sustain premium brand loyalty.

Recent Developments:

-

2024: Yara International expanded its Sulfan sulfur-bentonite product range into South Asian markets in 2024, specifically targeting wheat and canola growing regions across India and Bangladesh where soil sulfur deficiency affects over 60% of tested agricultural land, addressing the region’s most commercially significant underserved market for sulfur-based micronutrient products with a distribution expansion supported by local agronomic advisory infrastructure investment.

-

2024: Tiger-Sul Products expanded its sulfur-bentonite product range with new combination micronutrient grades including sulfur-bentonite-zinc and sulfur-bentonite-boron formulations in 2024, targeting the corn and canola growing regions of North America where co-occurring micronutrient deficiencies are progressively identified in commercial soil testing as limiting crop yield response to primary macronutrient application programmes.

-

2024: ICL Group launched its Nova-K Sulfur specialty nutrition product line in 2024, incorporating controlled-release sulfur with potassium for simultaneous macronutrient and sulfur delivery in high-value horticultural and specialty crop markets, demonstrating the commercial trend toward multi-nutrient precision delivery products whose combined value proposition commands premium pricing above single-nutrient sulfur-bentonite alternatives.

Sulfur-Based Micronutrients Market Key Players are:

-

Nutrien Ltd.

-

Yara International ASA

-

The Mosaic Company

-

ICL Group Ltd.

-

K+S Aktiengesellschaft

-

Coromandel International Limited

-

Deepak Fertilisers and Petrochemicals Corporation Ltd.

-

Kugler Company

-

Tiger-Sul Products LLC

-

Haifa Group

-

Koch Fertilizer LLC

-

EuroChem Group AG

-

CF Industries Holdings Inc.

-

Bunge Limited

-

Indian Farmers Fertiliser Cooperative Limited (IFFCO)

-

National Fertilizers Limited (NFL)

-

Zuari Agro Chemicals Ltd.

-

Rashtriya Chemicals and Fertilizers Limited (RCF)

-

OCP Group

-

SQM S.A.

Sulfur-Based Micronutrients Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 488.50 Million |

| Market Size by 2035 | USD 1,140.21 Million |

| CAGR | CAGR of 6.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Sulfur-Bentonite-Zinc, Sulfur-Bentonite-Manganese, Sulfur-Bentonite-Iron, Sulfur-Bentonite-Molybdenum, Others) • By Form (Solid, Liquid, Granular) • By Application (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others) • By Mode of Application (Soil Application, Foliar Application, Fertigation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nutrien Ltd., Yara International ASA, The Mosaic Company, ICL Group Ltd., K+S Aktiengesellschaft, Coromandel International Limited, Deepak Fertilisers and Petrochemicals Corporation Ltd., Kugler Company, Tiger-Sul Products LLC, Haifa Group, Koch Fertilizer LLC, EuroChem Group AG, CF Industries Holdings Inc., Bunge Limited, Indian Farmers Fertiliser Cooperative Limited (IFFCO), National Fertilizers Limited (NFL), Zuari Agro Chemicals Ltd., Rashtriya Chemicals and Fertilizers Limited (RCF), OCP Group, SQM S.A. |

Frequently Asked Questions

Asia Pacific dominated the Sulfur-Based Micronutrients Market in 2025, accounting for approximately 48.3% of global revenues.

Sulfur-Bentonite-Zinc dominated the Sulfur-Based Micronutrients Market with 38.5% share in 2025.

Progressive soil sulfur depletion, expanding oilseed crop cultivation, and increasing precision agriculture soil testing adoption are driving demand for sulfur-based micronutrients globally.

The Sulfur-Based Micronutrients Market was valued at USD 488.50 Million in 2025.

The Sulfur-Based Micronutrients Market is expected to grow at a CAGR of 8.83% from 2026 to 2035.

Get in Touch