Sulfur Fertilizer Market Report Scope & Overview:

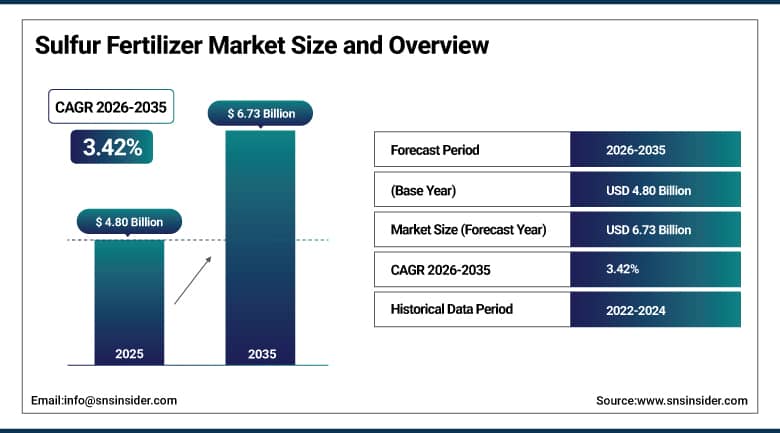

The Sulfur Fertilizer Market was valued at USD 4.80 Billion in 2025 and is expected to reach USD 6.73 Billion by 2035, growing at a CAGR of 3.42% from 2026–2035.

The global sulfur fertilizer market is growing at a steady pace. Sulfur is the important macronutrient for plant growth, essential for amino acid synthesis, protein formation, chlorophyll development, and enzyme activation. The market is primarily driven by increasing sulfur deficiency in soil. The progressive reduction of sulfur dioxide atmospheric deposition through industrial emission control programmes, which previously supplied agriculturally significant atmospheric sulfur to soils, has created a structural soil sulfur deficit that requires fertilizer supplementation to maintain crop productivity. Rising food demand from a growing global population, increasing farmer awareness of balanced fertilization, and government-backed soil health programmes collectively sustain consistent market growth.

In 2025, the International Fertilizer Association reported that approximately 73% of soils in Europe and North America are now sulfur-deficient due to reduced atmospheric deposition from industrial SO₂ emission controls. The structural nature of this deficiency, whose atmospheric source elimination creates permanent fertilizer dependency, sustains long-term sulfur fertilizer demand and creates above-average market growth motivation for sulfur fertilizer producers whose supply addresses an agronomic need that cannot be met through alternative nutrient sources.

Market Size and Forecast:

-

Market Size in 2026E: USD 4.96 Billion

-

Market Size by 2035: USD 6.73 Billion

-

CAGR: 3.42% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Sulfur Fertilizer Market - Request Free Sample Report

Sulfur Fertilizer Market Trends:

-

Ammonium sulfate demand is rising due to combined nitrogen and sulfur supply, improving fertilizer application efficiency for farmers.

-

Controlled-release elemental sulfur fertilizers are gaining adoption for long-term nutrient availability in high-duration crop cycles.

-

Sulfur-enriched NPK fertilizers are expanding as blended formulations improve nutrient completeness and reduce multiple application needs.

-

Precision sulfur application using soil testing and GPS-based variable rate technology is improving nutrient use efficiency in fields.

-

Bio-based sulfur fertilizers from industrial by-products are growing due to low cost, sustainability benefits, and circular economy adoption.

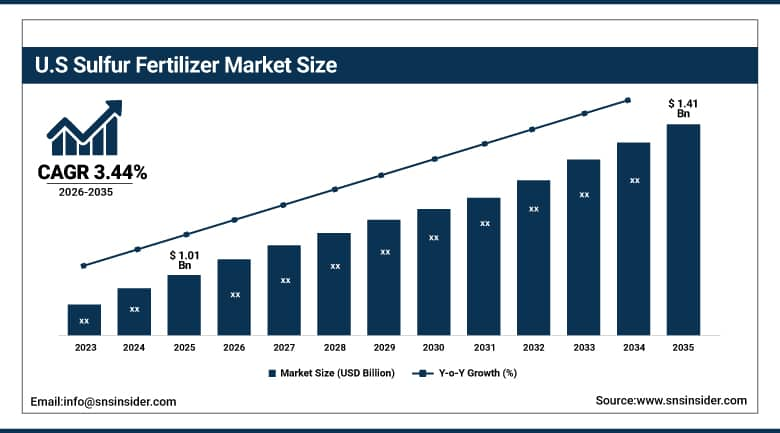

U.S. Sulfur Fertilizer Market Outlook:

The U.S. Sulfur Fertilizer Market was valued at approximately USD 1.01 Billion in 2025 and is expected to reach approximately USD 1.41 Billion by 2035, growing at a CAGR of approximately 3.44%.

The U.S. is the most commercially significant sulfur fertilizer market within the fastest-growing North American region. The Mosaic Company, Nutrien, Yara International’s U.S. operations, and Koch Agronomic Services collectively serve the domestic market. The U.S. Corn Belt’s progressive soil sulfur depletion from decades of high-yield corn production without adequate sulfur replacement creates structured agronomic motivation for corn and soybean sulfur fertilization. USDA’s 4R Nutrient Stewardship programme’s emphasis on sulfur as an essential secondary nutrient creates institutional awareness that sustains U.S. farmer procurement. Atmospheric sulfur deposition’s documented decline from Clean Air Act SO₂ emission controls creates the structural demand driver that sustains above-average U.S. market growth.

Mosaic Company expanded its MicroEssentials SZ premium sulfur-enhanced granular fertilizer production capacity in 2024, responding to growing farmer demand for sulfur-containing granular blends whose single-product application of nitrogen, phosphorus, potassium, and sulfur creates operational efficiency and improves sulfur distribution. The capacity expansion reflects commercial recognition that U.S. corn and soybean farmer willingness to pay for convenience and uniformity.

Sulfur Fertilizer Market Segment Analysis:

-

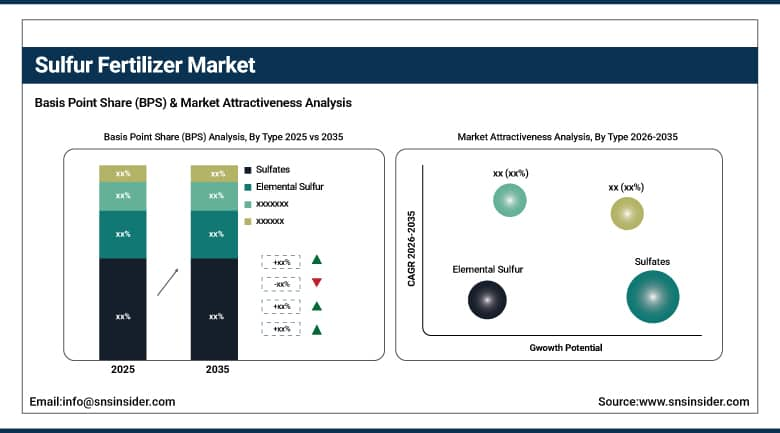

By Type, the sulfates segment dominated the sulfur fertilizer market with approximately 44% share in 2025, while the elemental sulfur segment is the fastest growing.

-

By Form, the solid segment dominated the sulfur fertilizer market with approximately 68% share in 2025, while the liquid segment is the fastest growing.

-

By application method, the soil application segment dominated the sulfur fertilizer market with approximately 55% share in 2025, while the fertigation segment is the fastest growing.

-

By Crop Type, the cereals & grains segment dominated the sulfur fertilizer market with approximately 36% share in 2025, while the oilseeds & pulses segment is the fastest growing.

By Type, sulfates dominate, elemental sulfur grows fastest

Sulfates retained the dominant type position with approximately 44% of the sulfur fertilizer market in 2025. Ammonium sulfate’s dual nitrogen and sulfur nutrition, whose combined macronutrient and secondary nutrient delivery in a single application creates agronomic and operational efficiency, makes it the most widely specified sulfate fertilizer in annual field crop programmes. Potassium sulfate’s chloride-free potassium and sulfur combination creates specification preference in chloride-sensitive crops whose SOP economics justify the premium over MOP alternatives. The fertilizer sector’s industrial co-product sulfate supply from caprolactam, acrylonitrile, and ammonium bisulfite manufacturing creates consistent low-cost sulfate availability that sustains competitive pricing.

Elemental sulfur is the fastest-growing type because its lower cost per unit of sulfur nutrient relative to sulfate alternatives creates economic motivation for adoption in broad-acre field crop production whose scale makes per-unit input cost differentials commercially significant. Sulphur-enhanced nitrogen fertilizer’s incorporation of elemental sulfur into urea and ammonium nitrate granules creates distribution efficiency that sustains above-average elemental sulfur commercial growth in markets where nitrogen-sulfur blended products are gaining farmer adoption.

By Application Method, soil application dominates, fertigation grows fastest

Soil application retained the dominant application method position with approximately 55% of the sulfur fertilizer market in 2025. Broadcast pre-plant and side-dress soil incorporation’s compatibility with standard farm machinery, its applicability to all field crop production systems including rainfed dryland agriculture, and its established agronomic recommendation infrastructure create the most commercially accessible sulfur delivery approach across diverse agricultural systems globally. Granular ammonium sulfate’s broad-acre broadcast application in combination with primary NPK fertilizers creates the single most commercially significant sulfur fertilizer application context whose aggregate procurement scales with global field crop production acreage.

Fertigation is the fastest-growing application method because drip-irrigated and center-pivot-irrigated high-value crop production’s precision liquid sulfur delivery enables root-zone placement efficiency that broadcast application cannot achieve. Ammonium thiosulfate and potassium thiosulfate’s compatibility with liquid fertilizer injection systems creates fertigated sulfur nutrition that maximizes plant uptake efficiency and minimizes surface volatilization losses. The global expansion of drip irrigation in water-scarce agricultural regions creates proportional new fertigation sulfur application channel procurement that compounds with each new irrigated hectare established.

By Form, solid dominates, liquid grows fastest

Solid sulfur fertilizers retained the dominant form position with approximately 68% of the sulfur fertilizer market in 2025. Granular form’s compatibility with standard broadcasting, side-dressing, and deep placement equipment creates the most commercially versatile sulfur delivery form for the field crop production systems that constitute the majority of global sulfur fertilizer consumption. Granular ammonium sulfate, elemental sulfur prills, and calcium sulfate granules each represent commercially established products whose distribution infrastructure, storage stability, and mechanical application compatibility create specification simplicity that liquid alternatives cannot match in dryland and rainfed agricultural systems.

Liquid sulfur fertilizers are the fastest-growing form because ammonium thiosulfate’s compatibility with liquid fertilizer prescription programmes, fertigation system injection, and foliar application creates growing commercial adoption in precision agriculture and irrigated crop production whose value-per-hectare justifies liquid system investment. Each liquid fertilizer dealer that adds ammonium thiosulfate to its fluid fertilizer blend programme creates retail procurement that sustains above-average liquid segment commercial growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

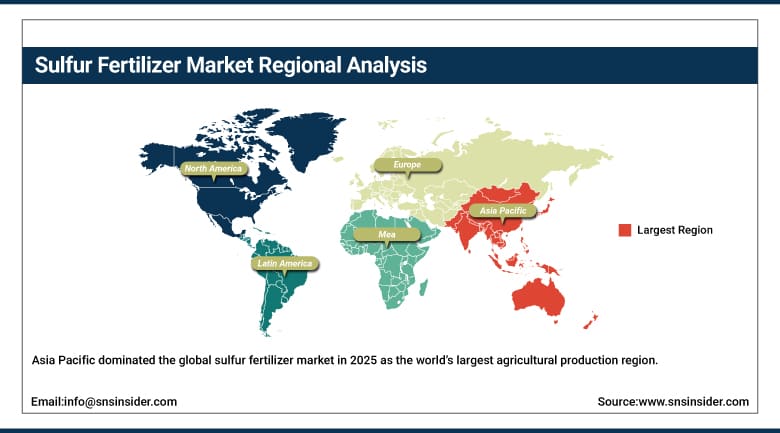

Asia Pacific Sulfur Fertilizer Market Insights:

Asia Pacific dominated the global sulfur fertilizer market in 2025 as the world’s largest agricultural production region. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary rice, wheat, and oilseed production whose combined cultivation area creates the largest national sulfur fertilizer procurement volume globally. India’s rapidly expanding oilseed and cereal production, supported by government fertilizer subsidy programmes that increasingly include sulfur-containing products, creates above-average regional market growth.

Southeast Asia’s palm oil and rubber plantation expansion, Japan’s intensive vegetable production, and South Korea’s precision agriculture adoption create significant secondary markets whose aggregate procurement reinforces Asia Pacific’s commercial dominance. The region’s severe soil sulfur deficiency in tropical and sub-tropical soils that receive high rainfall leaching creates structural agronomic demand that sustains above-average per-hectare sulfur fertilizer application motivation.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Sulfur Fertilizer Market Insights

North America is the fastest-growing regional sulfur fertilizer market, driven by documented soil sulfur depletion from Clean Air Act SO₂ emission controls, progressive farmer awareness of sulfur deficiency’s yield impact, and the growing adoption of sulfur-enhanced nitrogen fertilizers in the Corn Belt. The United States accounts for approximately 87.4% of North American revenues through Mosaic’s MicroEssentials premium sulfur products, Nutrien’s sulfur fertilizer distribution, and Koch Agronomic Services’ liquid thiosulfate portfolio.

Canada contributes approximately 12.6% of North American revenues through its canola production’s above-average sulfur requirement creating structured procurement, the prairie grain sector’s growing sulfur deficiency awareness, and Agrium-Nutrien’s distribution infrastructure serving Western Canadian agricultural markets.

Europe Sulfur Fertilizer Market Insights

Europe is a technically sophisticated sulfur fertilizer market where EU emission control’s dramatic reduction of atmospheric sulfur deposition has created widespread soil sulfur deficiency that fundamentally transformed the market from a minor specialty to an agronomically essential nutrient. Germany accounts for approximately 22.3% of European revenues through its intensive cereal, oilseed, and vegetable production, BASF’s and K+S’s domestic fertilizer market presence, and the farming community’s above-average agronomic knowledge sustaining premium sulfur product adoption.

France, United Kingdom, and Poland are significant secondary markets where rapeseed’s above-average sulfur requirement, wheat’s protein quality response, and vegetable production’s sulfur nutrition create consistent institutional procurement from technically engaged farming operations.

MEA & Latin America Sulfur Fertilizer Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its commercial date palm, vegetable, and cereal production whose sulfur fertilization requirement in the arid calcareous soil environment creates structured procurement. Brazil leads Latin American revenues at approximately 44.2% through its extraordinary soybean, corn, and sugarcane production whose combined cultivation area and above-average sulfur removal through grain and stalk export creates structural soil sulfur depletion that sustains growing fertilizer procurement.

Argentina’s soybean and sunflower production create significant secondary Latin American sulfur fertilizer demand, while South Africa’s maize and sugarcane production creates consistent MEA secondary market procurement.

Market Dynamics:

Growth Drivers: Structural soil sulfur depletion from emission controls and growing oilseed production creating above-average per-hectare demand

The structural elimination of atmospheric sulfur deposition through SO₂ emission controls under the Clean Air Act, EU Large Combustion Plant Directive, and equivalent international frameworks is the sulfur fertilizer market’s most commercially certain long-term growth driver. Each year of continued SO₂ emission reduction progressively deepens soil sulfur deficits in previously sulfur-adequate agricultural soils, creating growing agronomic motivation for fertilizer supplementation. International Fertilizer Association data documenting 73% of European and North American soils now sulfur-deficient demonstrates the structural scale of this demand driver whose commercial consequence compounds with each successive decade of emission-controlled deposition decline.

Global oilseed production’s extraordinary expansion, driven by vegetable oil demand for food and biofuel, creates above-average per-hectare sulfur requirement that sustains above-market sulfur fertilizer procurement growth relative to cereal crop alternatives. Canola and rapeseed’s 25-40 kg S/ha requirement, combined with the extraordinary pace of global oilseed acreage expansion, creates a demand growth mechanism that compounds both per-hectare rate and cultivation area simultaneously.

Restraints: Commodity price volatility reducing farmer fertilizer investment and environmental concern about sulfate leaching

Commodity crop price cycles create fertilizer application rate volatility as farmer input cost management during low-price periods prioritizes primary macronutrient NPK investment over secondary nutrient sulfur supplementation. Each commodity price downturn that reduces farmer gross margin creates sulfur fertilizer application rate reduction whose commercial impact on market volume creates procurement volatility that moderates the market’s underlying structural demand growth trajectory.

Sulfate leaching in high-rainfall and sandy soil agricultural environments creates agronomic and environmental concern about sulfate fertilizer efficiency in systems where leaching losses reduce plant uptake efficiency. Each region where sulfate leaching creates both agronomic waste and potential water quality impact creates specification pressure toward controlled-release elemental sulfur alternatives whose slower oxidation to sulfate reduces leaching vulnerability, moderating high-solubility sulfate fertilizer adoption in sensitive soil environments.

Opportunities: Sulfur-enhanced NPK blends and precision variable-rate sulfur application

Sulfur-enhanced NPK compound fertilizer represents the most commercially expansive near-term product development opportunity whose integration of sulfur into standard balanced fertilizer blends creates market access through the existing NPK procurement infrastructure without requiring separate sulfur purchasing decisions. Each NPK fertilizer formulation that incorporates sulfate or elemental sulfur creates incremental sulfur fertilizer market volume that compounds with the NPK market’s production scale. Mosaic’s MicroEssentials SZ demonstrates the commercial success of this approach whose premium pricing over commodity NPK sustains investment in sulfur-enhanced product development.

Precision variable-rate sulfur application represents the most commercially value-accretive technology adoption direction for premium sulfur fertilizer products whose site-specific prescription application creates maximum agronomic benefit from minimum input investment. Each farm that adopts variable-rate sulfur application creates above-average precision product specification procurement whose combined agronomic and economic efficiency creates adoption motivation that sustains premium product development investment.

Recent Developments:

-

2026: ICL Group launched enhanced elemental sulfur-based fertilizers targeting controlled-release nutrient availability for high-value crop production systems.

-

2026: Haifa Chemicals expanded water-soluble sulfur fertilizer solutions for fertigation systems supporting horticulture and greenhouse crop optimization.

-

2025: Nutrien expanded sulfur-enhanced fertilizer portfolio in North America, improving crop yield efficiency through integrated nutrient management solutions.

Sulfur Fertilizer Market Key Players are:

-

Nutrien Ltd.

-

The Mosaic Company

-

Yara International ASA

-

ICL Group Ltd.

-

Koch Agronomic Services LLC

-

BASF SE

-

Sociedad Química y Minera de Chile (SQM)

-

K+S AG

-

Haifa Chemicals Ltd.

-

Tiger-Sul Products LLC

-

Sulphur Mills Limited

-

Coromandel International Ltd.

-

Zuari Agro Chemicals

-

Deepak Fertilisers and Petrochemicals

-

Arabian Sulphur Company

-

Nufarm Limited

-

Helena Agri-Enterprises

-

Tessenderlo Group

-

OCI Nitrogen

-

Compass Minerals International

Sulfur Fertilizer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.80 Billion |

| Market Size by 2035 | USD 6.73 Billion |

| CAGR | CAGR of 3.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Sulfates, Elemental Sulfur, Others) • By Form (Solid, Liquid, Powder) • By Application Method (Soil Application, Fertigation, Foliar Spray) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Plantation Crops, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nutrien Ltd., The Mosaic Company, Yara International ASA, ICL Group Ltd., Koch Agronomic Services LLC, BASF SE, Sociedad Química y Minera de Chile (SQM), K+S AG, Haifa Chemicals Ltd., Tiger-Sul Products LLC, Sulphur Mills Limited, Coromandel International Ltd., Zuari Agro Chemicals, Deepak Fertilisers and Petrochemicals, Arabian Sulphur Company, Nufarm Limited, Helena Agri-Enterprises, Tessenderlo Group, OCI Nitrogen, Compass Minerals International |

Frequently Asked Questions

The market is expected to grow at a CAGR of 3.42% from 2026 to 2035.

The market was valued at USD 4.80 Billion in 2025.

Increasing sulfur deficiency in soil driven by the structural elimination of atmospheric SO₂ deposition through industrial emission controls, creating permanent fertilizer dependency.

Sulfates dominated the market with approximately 44% share in 2025.

Asia Pacific dominated the Sulfur Fertilizer Market in 2025.

Get in Touch