Superdisintegrants Market Report Scope & Overview:

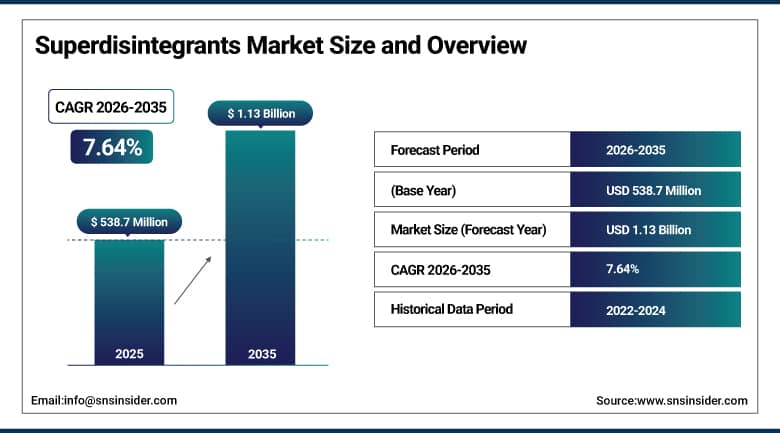

The Superdisintegrants Market was valued at USD 538.7 Million in 2025 and is expected to reach USD 1.13 Billion by 2035, growing at a CAGR of 7.64% from 2026–2035.

The global superdisintegrants market is advancing as the pharmaceutical industry’s solid dosage form development pipeline increasingly specifies highly efficient disintegration agents whose swelling, wicking, and deformation mechanisms provide rapid tablet and capsule disintegration that conventional disintegrant materials including corn starch and microcrystalline cellulose cannot achieve at equivalent concentrations. Superdisintegrants including croscarmellose sodium, crospovidone, and sodium starch glycolate deliver disintegration times measured in seconds to minutes at concentrations of 2 to 6% by weight, enabling orodispersible tablet and immediate-release capsule formulations whose rapid drug release improves bioavailability in absorption-limited API formulations.

In 2024, IFF (International Flavors & Fragrances) launched enhanced grades of its Ac-Di-Sol croscarmellose sodium superdisintegrant with optimised particle size distribution and improved compressibility profiles for high-speed tablet compression applications, enabling pharmaceutical manufacturers to achieve faster disintegration at lower superdisintegrant concentrations without compromising tablet mechanical strength or friability performance. The improved grades addressed the pharmaceutical formulation challenge of balancing rapid disintegration performance with adequate tablet hardness in high-dose API formulations whose compressibility requirements conflict with the porous tablet structure needed for rapid water penetration and disintegration agent activation.

Market Size and Forecast:

-

Market Size in 2026E: USD 580.0 Million

-

Market Size by 2035: USD 1.13 Billion

-

CAGR: 7.64% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Superdisintegrants Market - Request Free Sample Report

Superdisintegrants Market Trends:

-

Orally disintegrating tablet formulation growth is driving above-average superdisintegrant demand for mouth-dissolving paediatric and geriatric dosage forms.

-

Natural superdisintegrant development using modified plant polysaccharides is progressing as pharmaceutical excipient sustainability requirements tighten.

-

High-speed tablet compression requirements are driving particle-engineered superdisintegrant grades offering improved flow properties at commercial press speeds.

-

Biosimilar tablet formulation activity is creating growing superdisintegrant procurement from emerging pharmaceutical manufacturers entering complex generic markets.

-

Co-processed excipient development combining superdisintegrants with fillers and binders is improving orally disintegrating tablet manufacturability and mechanical properties.

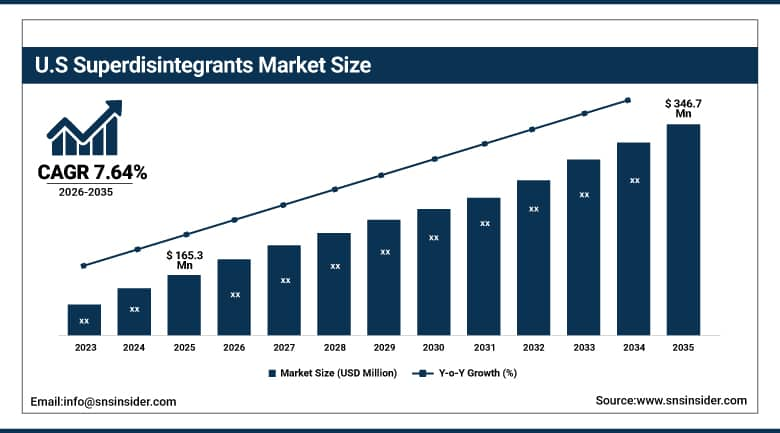

U.S. Superdisintegrants Market Outlook:

The U.S. Superdisintegrants Market was valued at approximately USD 165.3 Million in 2025 and is expected to reach approximately USD 346.7 Million by 2035, growing at a CAGR of approximately 7.64%.

The United States leads North American revenues through the world’s largest pharmaceutical manufacturing base, the highest number of FDA-approved solid dosage form drug products creating consistent superdisintegrant procurement, and the advanced formulation R&D investment in orodispersible tablet platform development. IFF, Ashland, and Roquette sustain U.S. superdisintegrant market leadership through their comprehensive pharmaceutical excipient portfolios, technical regulatory support capabilities, and validated supply chain infrastructure supporting pharmaceutical manufacturer quality requirements.

In 2023, Roquette Frères launched LYCATAB PGS croscarmellose sodium with enhanced functionality for direct compression tablet manufacturing, providing improved compactibility and reduced tablet capping risk at high compression forces. The product addressed the direct compression formulation challenge where superdisintegrant concentration optimisation for rapid disintegration conflicts with maintaining adequate tablet tensile strength under high-speed rotary press operation, creating a formulation window limitation that the enhanced grade’s improved compressibility profile expands for a broader range of API concentrations and tablet press configurations.

Superdisintegrants Market Segment Analysis:

-

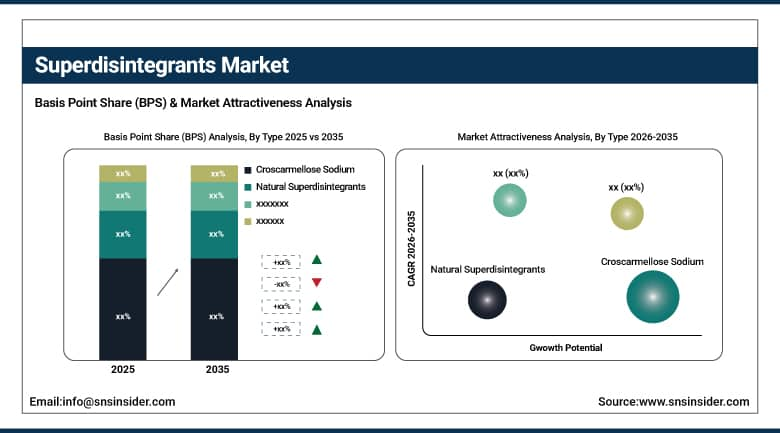

By Type, croscarmellose sodium segment dominated the superdisintegrants market with approximately 36% market share in 2025 through its balance of rapid disintegration and tablet compatibility, the natural superdisintegrants segment is projected to register the fastest CAGR of around 8.9% during 2026–2035.

-

By Formulation, tablets segment dominated the superdisintegrants market with the largest share in 2025, while orally disintegrating tablets are the fastest growing formulation driven by paediatric, geriatric, and dysphagia patient population demand.

-

By Therapeutic Area, neurological diseases segment dominated the superdisintegrants market with the largest share in 2025 through antiepileptic and CNS drug tablet formulation demand, while Oncology is the fastest growing through targeted oral solid dosage form development.

-

By End User, pharmaceutical companies segment dominated the superdisintegrants market with the largest share in 2025, while contract manufacturing organizations are the fastest growing end user through outsourcing of solid dosage form manufacturing.

By Type, croscarmellose sodium dominates, natural superdisintegrants grow fastest

Croscarmellose sodium retained the dominant type position with the largest share of the superdisintegrants market in 2025. Its commercial primacy reflects the technically superior balance of rapid water absorption-driven swelling, effective capillary action-mediated tablet wetting, and excellent tablet mechanical compatibility that croscarmellose sodium delivers at standard incorporation concentrations of 2 to 4%, creating the preferred disintegrant for the broadest range of direct compression and wet granulation tablet formulations across diverse API types. Croscarmellose sodium’s comprehensive global regulatory acceptance documented in the FDA’s Inactive Ingredient Database, the European Medicines Agency’s excipient guideline, and the ICH Q8 pharmaceutical development regulatory framework across all major pharmaceutical markets creates specification confidence that sustains its formulation development selection as the default superdisintegrant option for new oral solid dosage form programmes.

Natural superdisintegrants are growing fastest because the pharmaceutical industry’s increasing emphasis on excipient sustainability, green chemistry principles, and bio-based raw material sourcing is creating research and commercial investment in plant-derived polysaccharide disintegrants whose renewable agricultural origin, biodegradable end-of-life profile, and non-synthetic production create environmental advantages over petroleum-derived synthetic excipient alternatives. Modified plantago ovata seed husk, agar, guar gum, and cassava starch derivatives are emerging as natural superdisintegrant candidates whose performance is progressively being optimised through chemical modification and particle engineering to approach croscarmellose sodium’s disintegration efficacy at commercially relevant tablet compression settings.

By Formulation, tablets dominate, ODTs grow fastest

Tablets retained the dominant formulation position with the largest share of the superdisintegrants market in 2025. The tablet dosage form’s extraordinary commercial scale, encompassing the majority of the world’s approximately 7,000 approved oral drug products, creates a superdisintegrant procurement base whose aggregate volume substantially exceeds all other solid dosage form types combined. Immediate-release tablet formulations specifying croscarmellose sodium or crospovidone at 2 to 6% concentrations for rapid in vivo disintegration and API dissolution, extended-release tablets whose enteric and sustained-release coating systems sit on superdisintegrant-containing tablet cores, and chewable tablet formulations each represent distinct tablet types creating ongoing superdisintegrant procurement.

Orally disintegrating tablets are growing fastest because the growing clinical recognition of dysphagia’s prevalence across 15% of the general population and its substantially higher incidence among neurological, geriatric, and oncology patient populations creates formulary motivation for ODT alternatives to conventional tablets whose swallowing requirement creates compliance barriers in affected patient groups. Each pharmaceutical company that develops an ODT version of an established tablet product targeting dysphagia patients or paediatric populations creates superdisintegrant procurement at the typically higher concentrations of 5 to 10% required for the one-minute or faster mouth dissolution specification that ODT regulatory guidelines require.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

India |

44.8% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Superdisintegrants Market Insights

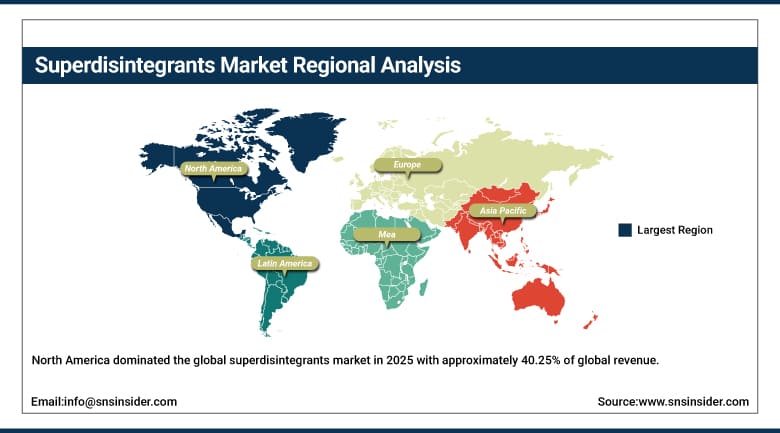

North America dominated the global superdisintegrants market in 2025 with approximately 40.25% of global revenue, driven by the world’s largest pharmaceutical manufacturing base, the highest FDA new drug approval rate creating consistent new formulation development procurement, and the concentration of IFF, Ashland, and Roquette’s superdisintegrant commercial operations. The United States accounts for approximately 82.5% of North American revenues through its pharmaceutical manufacturing concentration.

Canada contributes supplementary North American revenues through its growing pharmaceutical generic manufacturing sector’s superdisintegrant procurement, the growing ODT formulation activity in paediatric and geriatric drug product development, and the food-grade natural superdisintegrant research activity at Canadian university pharmaceutical sciences programmes creating academic procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Superdisintegrants Market Insights

Europe is a significant superdisintegrants market where the EU’s stringent pharmaceutical excipient quality requirements, the European Directorate for the Quality of Medicines’ excipient monograph standards, and the large innovative and generic pharmaceutical manufacturing sectors create consistent high-quality superdisintegrant demand. Germany accounts for approximately 22.4% of European revenues through its large pharmaceutical manufacturing sector, Bayer’s and Boehringer Ingelheim’s tablet formulation procurement, and JRS Pharma’s German manufacturing of pharmaceutical excipients including superdisintegrant grades.

Switzerland’s multinational pharmaceutical headquarters’ formulation development procurement, Ireland’s large contract pharmaceutical manufacturing sector’s superdisintegrant consumption, and the UK’s generic pharmaceutical manufacturers’ solid dosage form production collectively sustain European superdisintegrant market development. European pharmaceutical sustainability initiatives are accelerating natural and bio-based superdisintegrant development investment.

Asia Pacific Superdisintegrants Market Insights

Asia Pacific is the fastest-growing regional superdisintegrants market, driven by India’s world-leading generic pharmaceutical manufacturing capacity creating the largest individual superdisintegrant consumption volume outside North America, China’s expanding pharmaceutical solid dosage form manufacturing, and the growing South Korean and Japanese ODT pharmaceutical pipeline. India accounts for approximately 44.8% of Asia Pacific revenues through its world-leading generic tablet manufacturing whose annual production volume of billions of tablets creates proportional superdisintegrant procurement.

China’s pharmaceutical manufacturing modernization under GMP upgrade programmes, South Korea’s sophisticated pharmaceutical excipient quality requirements, and Japan’s advanced ODT pharmaceutical market whose innovative oral dosage form development creates premium superdisintegrant procurement collectively sustain Asia Pacific’s fastest-growing regional trajectory. The progressive tightening of pharmaceutical excipient quality standards across Asian regulatory frameworks is creating preference for quality-certified superdisintegrant grades.

MEA & Latin America Superdisintegrants Market Insights

Israel leads MEA revenues through its pharmaceutical manufacturing sector’s advanced solid dosage form expertise, Teva Pharmaceutical’s generic tablet formulation procurement, and the growing regional pharmaceutical manufacturing investment in Gulf Cooperation Council countries creating new superdisintegrant demand. Saudi Arabia’s growing pharmaceutical manufacturing sector creates expanding regional excipient procurement.

Brazil leads Latin American revenues through its large domestic pharmaceutical manufacturing sector’s tablet production, the growing generic pharmaceutical market’s solid dosage form development, and ANVISA’s pharmaceutical quality requirements creating certified excipient specification preference. Mexico and Argentina contribute growing secondary demand through their pharmaceutical manufacturing investment.

Market Dynamics:

Growth Drivers: Pharmaceutical pipeline growth in solid dosage forms and ODT adoption in paediatric and geriatric patient populations driving superdisintegrant demand

The superdisintegrants market’s growth is driven by the pharmaceutical industry’s expanding solid dosage form pipeline whose global annual NDA and ANDA approval volume creates proportional new formulation superdisintegrant procurement. Each new immediate-release tablet, orodispersible tablet, and fast-dissolving capsule product development programme creates superdisintegrant technical evaluation, formulation development lot procurement, and subsequent commercial-scale supply qualification. The growing pharmaceutical pipeline activity in neurological disorders, cardiovascular diseases, and oncology, whose tablet-based drug delivery preference creates consistent solid dosage form development investment, sustains superdisintegrant demand across the highest-value therapeutic categories whose per-unit API cost creates formulation investment motivation.

The ODT dosage form’s growing market adoption driven by patient adherence advantages in neurological, psychiatric, and paediatric patient populations whose swallowing difficulty, compliance challenges, or caregiver administration requirements create clinical preference for mouth-dissolving formulations is creating the superdisintegrant market’s fastest-growing application category. Each new neurological or psychiatric drug product that converts from a conventional tablet to an ODT formulation to improve patient compliance creates a superdisintegrant concentration and grade change that typically increases per-tablet superdisintegrant content, amplifying the commercial impact of ODT conversion on superdisintegrant procurement volume.

Restraints: Limited superdisintegrant compatibility with hygroscopic APIs and stringent quality requirements increasing excipient certification burden

Superdisintegrants’ ionic character and moisture-absorbing swelling mechanism create formulation compatibility challenges with hygroscopic APIs whose moisture sensitivity causes degradation or polymorphic transformation upon contact with water-absorbing excipients during tablet manufacturing and storage. Each water-sensitive API whose stability requires minimizing tablet moisture exposure creates a superdisintegrant selection constraint that may limit acceptable options to crospovidone’s non-ionic, non-aqueous swelling mechanism over the ionic croscarmellose sodium and sodium starch glycolate alternatives.

Pharmaceutical excipient regulatory compliance requirements including IPEC-PQG Good Manufacturing Practice guideline conformity, compendial monograph testing, and certificate of analysis documentation for each excipient lot create quality assurance investment that smaller superdisintegrant manufacturers serving emerging pharmaceutical markets may find commercially burdensome. Each new ICH Q11 or Q7 excipient compliance requirement creates supplier qualification documentation whose preparation cost and regulatory affairs expertise requirement constrains the number of compliant superdisintegrant suppliers in less-developed pharmaceutical supply chain markets.

Opportunities: Natural superdisintegrant development aligned with pharmaceutical sustainability goals and co-processed excipient innovation creating premium grades

Natural superdisintegrant development from plant polysaccharide sources representing the pharmaceutical excipient equivalent of green chemistry innovation creates a commercially significant near-term market opportunity whose realization depends on achieving disintegration performance equivalent to synthetic alternatives at competitive cost economics. Each natural superdisintegrant candidate whose regulatory submission establishes a pharmacopoeial monograph creates a compendially-accepted excipient option that pharmaceutical formulators can specify without additional regulatory justification, removing the primary adoption barrier for natural alternatives whose novel excipient regulatory pathway is currently more complex than established synthetic superdisintegrant alternatives.

Co-processed excipient development combining superdisintegrants with diluents, glidants, or lubricants in a single particle structure creates pharmaceutical manufacturing efficiency improvements that simplify formulation composition and reduce blending process steps in direct compression tablet manufacturing. Each new co-processed excipient incorporating a superdisintegrant function within a multi-functional excipient particle creates a commercial grade commanding premium pricing above pure superdisintegrant commodity markets, sustaining manufacturer innovation investment in new co-processed product development.

Recent Developments:

-

2024: IFF launched enhanced Ac-Di-Sol croscarmellose sodium grades with optimized particle size distribution and improved compressibility for high-speed tablet compression applications, enabling faster disintegration at lower concentrations without compromising tablet mechanical strength.

-

2023: Roquette Frères launched LYCATAB PGS croscarmellose sodium with enhanced compactibility and reduced tablet capping risk for direct compression manufacturing, expanding the formulation window for rapid disintegration at high compression forces.

-

2023: Ashland Global Holdings introduced Plasdone XL-10 crospovidone with improved flowability and reduced dust characteristics for pharmaceutical tablet manufacturing environments, addressing operator safety and process efficiency requirements at high-throughput commercial tablet press operations.

Superdisintegrants Market Key Players are:

-

IFF (International Flavors & Fragrances) Inc.

-

JRS Pharma GmbH & Co. KG

-

Roquette Frères SA

-

BASF SE (Pharma Solutions)

-

Ashland Global Holdings Inc.

-

DFE Pharma GmbH

-

Colorcon Inc.

-

SPI Pharma Inc.

-

Ideal Cures Pvt. Ltd.

-

Blanver Farmoquimica Ltda.

-

Sigachi Industries Ltd.

-

Kerry Group PLC

-

Shin-Etsu Chemical Co. Ltd.

-

Croda International PLC

-

IMCD N.V.

-

Merck KGaA (Supelco)

-

Asahi Kasei Corporation

-

Peter Greven GmbH & Co. KG

-

Aqualon (Ashland)

-

Qualichem Inc.

Superdisintegrants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 538.7 Million |

| Market Size by 2035 | USD 1.13 Billion |

| CAGR | CAGR of 7.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Croscarmellose Sodium, Crospovidone, Sodium Starch Glycolate, Natural Superdisintegrants, Others) • By Formulation (Tablets, Capsules, Orally Disintegrating Tablets, Others) • By Therapeutic Area (Neurological Diseases, Gastrointestinal Diseases, Cardiovascular Diseases, Oncology, Others) • By End User (Pharmaceutical Companies, Contract Manufacturing Organizations, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IFF (International Flavors & Fragrances) Inc., JRS Pharma GmbH & Co. KG, Roquette Frères SA, BASF SE (Pharma Solutions), Ashland Global Holdings Inc., DFE Pharma GmbH, Colorcon Inc., SPI Pharma Inc., Ideal Cures Pvt. Ltd., Blanver Farmoquimica Ltda., Sigachi Industries Ltd., Kerry Group PLC, Shin-Etsu Chemical Co. Ltd., Croda International PLC, IMCD N.V., Merck KGaA (Supelco), Asahi Kasei Corporation, Peter Greven GmbH & Co. KG, Aqualon (Ashland), and Qualichem Inc. |

Frequently Asked Questions

The Superdisintegrants Market is expected to grow at a CAGR of 7.64% from 2026 to 2035.

The Superdisintegrants Market was valued at USD 538.7 Million in 2025.

Expanding pharmaceutical solid dosage form pipeline creating formulation procurement, ODT adoption in paediatric and geriatric populations requiring faster mouth dissolution, growing biosimilar and generic tablet manufacturing, and natural superdisintegrant development aligned with pharmaceutical sustainability initiatives are the primary growth factors.

Croscarmellose Sodium dominated with the largest share in 2025.

North America dominated the Superdisintegrants Market in 2025 with approximately 40.25% of global revenues.

Get in Touch