Syndromic Multiplex Diagnostics Market Report Scope & Overview:

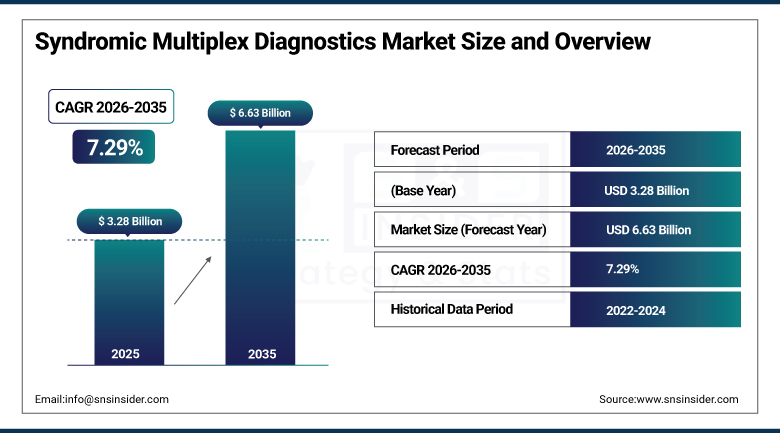

The Syndromic Multiplex Diagnostics Market was valued at USD 3.28 Billion in 2025 and is expected to reach USD 6.63 Billion by 2035, growing at a CAGR of 7.29% from 2026 to 2035.

The market for Syndromic Multiplex Diagnostics is experiencing growth due to the fact that conventional diagnostic methods which involve various stages and longer processing times have been replaced by more sophisticated solutions that enable the identification of multiple pathogens from one sample at once. It makes it possible to diagnose a disease much faster and is highly valued in healthcare facilities for rapid diagnosis especially respiratory, gastrointestinal and CNS infections. Global aging populations, technological advancements in diagnostics platforms, and rising prevalence of infectious diseases continue reinforcing structural demand, while precision testing that identifies multiple pathogens from a single specimen keeps shortening the path between specimen collection and targeted therapy.

bioMerieux received United States Food and Drug Administration clearance in February 2025 for its BIOFIRE FILMARRAY Gastrointestinal Panel Mid, a midplex molecular panel testing for eleven of the most common bacteria, viruses, and parasites associated with gastroenteritis from a single sample, with results available in approximately one hour.

Market Size and Forecast

-

Market Size in 2026E: USD 3.52 Billion

-

Market Size by 2035: USD 6.63 Billion

-

CAGR: 7.29% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Syndromic Multiplex Diagnostics Market- Request Free Sample Report

Syndromic Multiplex Diagnostics Market Trends

-

Next-generation sequencing-based assays are gaining traction for their value in detecting novel pathogens beyond conventional PCR panel capability.

-

Point-of-care clinics are emerging as the fastest-growing testing channel as diagnostics move closer to the patient.

-

Panels exceeding twenty pathogen targets are gaining adoption as laboratories seek more comprehensive single-sample diagnostic coverage.

-

Post-pandemic hospital investment continues reinforcing physician familiarity with multiplex respiratory testing workflows.

-

Infectious-disease surveillance programs are accelerating multiplex diagnostic demand for rapid outbreak detection and antimicrobial stewardship.

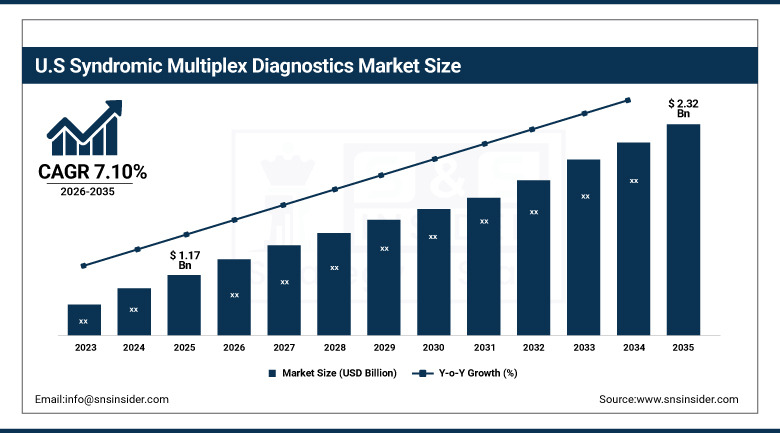

The United States Syndromic Multiplex Diagnostics Market Outlook

The United States Syndromic Multiplex Diagnostics Market was valued at USD 1.17 Billion in 2025 and is expected to reach USD 2.32 Billion by 2035, growing at a CAGR of 7.10% from 2026 to 2035.

United States had a lead in the demand for syndromic multiplex diagnostics in North America because the hospital laboratories and infectious disease surveillance initiatives witnessed a marked rise in the use of advanced molecular diagnostics. Nearly 53% of tertiary care hospitals used syndromic multiplex diagnostics that helped them identify pathogens faster in case of respiratory diseases or gastroenteritis.

Cepheid, headquartered in Sunnyvale, California, received United States Food and Drug Administration clearance for a gastrointestinal pathogen panel on its GeneXpert system, entering the rapid syndromic testing space with a platform offering ten-color optical module configurations that can be installed in both new and existing customer instruments without requiring a full system replacement.

Syndromic Multiplex Diagnostics Market Segmentation Analysis

-

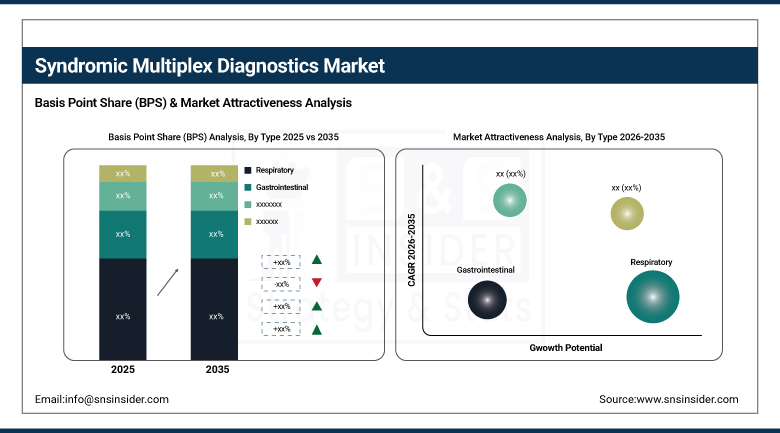

By Type, the respiratory segment held approximately 33.55% share in 2025, while the gastrointestinal segment is the fastest growing, with a CAGR of approximately 9.25%.

-

By Technology, the multiplex PCR segment held approximately 63.53% share in 2025, while the next-generation sequencing segment is the fastest growing, with a CAGR of approximately 10.75%.

-

By Panel Size, the 11-20 targets segment held approximately 45.15% share in 2025, while the above 20 targets segment is the fastest growing, with a CAGR of approximately 9.82%.

-

By End Use, the diagnostic laboratories segment held approximately 44.55% share in 2025, while the point-of-care clinics segment is the fastest growing, with a CAGR of approximately 8.32%.

By Type, respiratory led the market, gastrointestinal grew fastest

The respiratory segment dominated the type category in 2025, holding approximately 33.55% of total revenue, fueled by post-pandemic hospital investments and physician familiarity with multiplex respiratory workflows that remain the primary revenue generator across the broader diagnostics category. That established clinical adoption and testing infrastructure continues keeping respiratory panels firmly at the top of the broader type segmentation.

The gastrointestinal segment is projected to grow at the fastest CAGR of approximately 9.25% during the forecast period, driven by expanding panel offerings that address both severe and less severe gastroenteritis cases requiring rapid pathogen identification. Rising availability of midplex and full panel options letting laboratories choose coverage matched to patient acuity continues pushing this type category's growth rate ahead of the broader type segmentation.

By Technology, multiplex PCR led the market, next-generation sequencing grew fastest

The multiplex PCR segment held the largest technology share in 2025, at approximately 63.53%, anchored by its established clinical validation, rapid turnaround time, and broad physician familiarity across nearly every major hospital and laboratory setting. That combination of speed and clinical trust continues keeping multiplex PCR the dominant technology choice across the overwhelming majority of syndromic testing applications.

The next-generation sequencing segment is projected to grow at the fastest CAGR of approximately 10.75% during the forecast period, reflecting its value in detecting novel pathogens that conventional PCR panels are not designed to identify. Recent metagenomic sequencing confirmation of emerging pathogen spillover events considerably faster than traditional PCR methods continues pushing this technology category's growth rate ahead of the broader technology segmentation.

By Panel Size, 11-20 targets led the market, above 20 targets grew fastest

The 11-20 targets panel size segment held the largest share in 2025, at approximately 45.15%, representing the sweet spot where diagnostic comprehensiveness and cost efficiency intersect favorably for the majority of clinical testing scenarios. That balance of coverage and affordability continues keeping this panel size range the default choice across most hospital and laboratory syndromic testing programs.

The above 20 targets segment is projected to grow at the fastest CAGR of approximately 9.82% during the forecast period, as laboratories increasingly seek maximum single-sample diagnostic coverage for complex cases where broader pathogen detection meaningfully improves clinical decision-making. Rising demand for comprehensive coverage in complex or high-risk patient populations continues pushing this panel size category's growth rate ahead of the broader panel size segmentation.

By End Use, diagnostic laboratories led the market, point-of-care clinics grew fastest

The diagnostic laboratories segment held the largest end-use share in 2025, at approximately 44.55%, attributed to high patient footfall and better accessibility to patients compared with more specialized testing settings. That combination of volume and accessibility continues keeping diagnostic laboratories firmly at the top of the broader end-use segmentation across nearly every major healthcare system.

The point-of-care clinics segment is projected to grow at the fastest CAGR of approximately 8.32% during the forecast period, as diagnostics continue moving closer to the patient to enable faster treatment decisions without requiring samples to travel to centralized laboratory facilities. Rising demand for expedited, near-patient diagnostic results continue pushing this end-use category's growth rate ahead of the broader end-use segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.40% |

|

Europe |

Germany |

27.10% |

|

Asia Pacific |

China |

35.30% |

|

Middle East & Africa |

UAE |

26.60% |

|

Latin America |

Brazil |

38.00% |

North America Syndromic Multiplex Diagnostics Market Insights

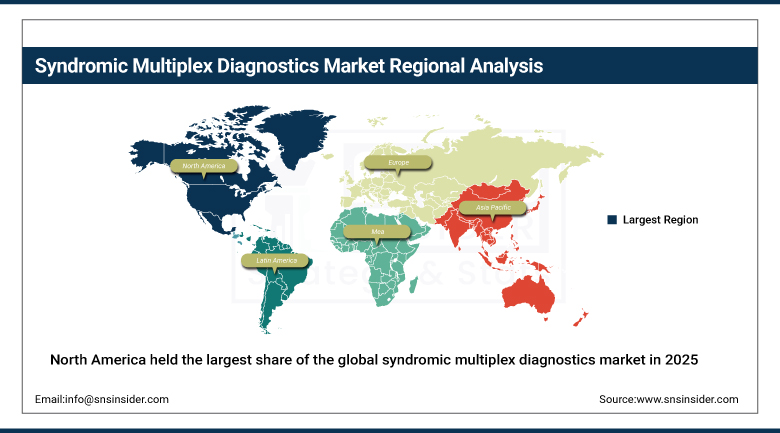

North America held the largest share of the global syndromic multiplex diagnostics market in 2025, at approximately 41.85%, driven by advanced healthcare infrastructure and hospital laboratories expanding advanced molecular diagnostic adoption substantially. Approximately forty-one percent of diagnostic laboratories upgraded automated PCR platforms as high-throughput infectious-disease testing demand increased across regional healthcare networks.

The United States accounted for roughly 84.40% of regional revenue, reflecting its concentration of tertiary-care hospitals and diagnostic laboratory networks integrating syndromic multiplex testing panels. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding molecular diagnostics adoption, keeping North America firmly ahead of every other region in this market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Syndromic Multiplex Diagnostics Market Insights

Europe captured a significant market share of the syndromic multiplex diagnostics market on a global scale during 2025, backed by well-established hospital laboratory systems and increased investments in infectious disease surveillance programs within the region. Germany made up around 27.10% of the regional market revenue owing to the presence of established hospital laboratories and advanced molecular diagnostic companies in the country.

France, the United Kingdom, and Italy followed a broadly similar trajectory, as continued infectious-disease surveillance and antimicrobial stewardship program investment extended syndromic multiplex diagnostics adoption across the continent's largest healthcare markets. Continued regulatory support for rapid diagnostic technology is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Syndromic Multiplex Diagnostics Market Insights

Asia Pacific was the fastest-growing region in the global syndromic multiplex diagnostics market, driven by expanding healthcare infrastructure investment, rising infectious disease burden, and growing government support for rapid diagnostic technology adoption across the region's largest economies. Continued expansion of diagnostic laboratory networks continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 35.30% of regional revenue, supported by aggressive healthcare infrastructure investment and expanding domestic diagnostics manufacturing capability. Japan and South Korea contributed significant additional regional demand through their own advanced healthcare systems and rising molecular diagnostics adoption, reinforcing Asia Pacific's position as the clear growth leader in this market.

MEA & Latin America Syndromic Multiplex Diagnostics Market Insights

The Middle East & Africa market experienced a significant increase in the adoption of syndromic multiplex diagnostics in 2025, owing to the increasing investment in healthcare infrastructure and the growing development of infectious disease surveillance programs in the Gulf countries in particular. The United Arab Emirates contributed about 26.60% to the regional revenue, aided by the digitalization policies of the country.

Latin America expanded at a comparable pace, led by Brazil at roughly 38.00% of regional revenue, where growing healthcare infrastructure investment continued to support category growth. Mexico and Argentina followed a similar trajectory as regional diagnostic laboratory capacity expanded further through the remainder of the forecast period.

Growth Drivers: Rapid diagnosis demand and infectious disease burden

Technological advancements in diagnostics technologies, combined with rising prevalence of various infectious diseases, continue to be the central force behind syndromic multiplex diagnostics market growth. Traditional diagnostic tests often require multiple steps and take longer to deliver results, while syndromic multiplex diagnostics offer a comprehensive solution by testing for multiple pathogens simultaneously in a single sample, significantly reducing diagnosis time.

The increasing need for diagnostic solutions that can provide prompt and accurate results, along with an aging global population vulnerable to infection complications, continues to contribute towards structural demand growth in nearly all key medical settings. The rising cases of respiratory, gastrointestinal, and sexually transmitted infections have continued to drive demand for panels for syndromic tests.

Restraints: High panel costs and reimbursement variability

The substantial cost of comprehensive multiplex panels, particularly those covering more than twenty pathogen targets, continues to restrict adoption among smaller diagnostic laboratories and healthcare facilities operating with constrained budgets. That cost barrier continues concentrating the most comprehensive panel adoption among well-resourced tertiary-care hospitals and large diagnostic laboratory networks.

Variability in reimbursement policy across different healthcare systems and payers continues complicating adoption decisions for laboratories evaluating whether to invest in expanded panel offerings. That reimbursement uncertainty continues requiring diagnostics companies to build strong clinical utility evidence to support payer coverage decisions across different regional markets.

Opportunities: Next-generation sequencing expansion and point-of-care migration

Growing adoption of next-generation sequencing-based assays presents substantial opportunity for diagnostics companies positioned to serve novel pathogen detection needs that conventional PCR panels cannot address. Companies capable of delivering genuinely rapid, clinically actionable sequencing-based diagnostics stand to capture a growing share of demand as infectious-disease surveillance programs continue expanding.

Continued migration of syndromic testing toward point-of-care clinic settings presents a further significant growth avenue, as diagnostics move closer to the patient to enable faster treatment decisions. Manufacturers capable of delivering compact, easy-to-operate multiplex testing platforms suited to point-of-care environments stand to capture meaningful new revenue streams through 2035.

Recent Developments:

-

2024: bioMerieux received United States FDA Special 510(k) clearance in December for its BIOFIRE FILMARRAY Tropical Fever Panel, a syndromic PCR test targeting chikungunya, dengue, Leptospira, and Plasmodium species, with commercial launch in the United States targeted for the first quarter of 2025.

-

2025: DiaSorin continued expanding its Plex system panel portfolio, submitting an expanded target gastrointestinal test designed to broaden pathogen coverage for laboratories seeking comprehensive single-sample diagnostic solutions.

-

2025: Becton, Dickinson and Company continued expanding its BD Cor lab-based system panel offerings, adding smaller, more targeted gastrointestinal panels to complement its broader automated molecular diagnostics portfolio.

Syndromic Multiplex Diagnostics Market key players are:

-

BioFire Diagnostics, LLC

-

Cepheid

-

F. Hoffmann-La Roche Ltd.

-

Luminex Corporation

-

QIAGEN N.V.

-

Bio-Rad Laboratories, Inc.

-

Abbott Laboratories

-

Seegene Inc.

-

Bruker Corporation

-

Becton, Dickinson and Company

-

Thermo Fisher Scientific Inc.

-

Hologic, Inc.

-

T2 Biosystems, Inc.

-

DiaSorin S.p.A.

-

Coris BioConcept

-

Randox Laboratories Ltd.

-

Genomadix Inc.

-

Talis Biomedical Corporation

-

bioMerieux SA

-

Meridian Bioscience, Inc.

Syndromic Multiplex Diagnostics Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.28 Billion |

| Market Size by 2035 | USD 6.63 Billion |

| CAGR | CAGR of 7.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Respiratory, Gastrointestinal, Central Nervous System, Bloodstream) • By Technology (Multiplex PCR, Next-Generation Sequencing) • By Panel Size (11-20 Targets, Above 20 Targets, Below 10 Targets) • By End Use (Diagnostic Laboratories, Hospitals, Point-of-Care Clinics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BioFire Diagnostics, LLC, Cepheid, F. Hoffmann-La Roche Ltd., Luminex Corporation, QIAGEN N.V., Bio-Rad Laboratories, Inc., Abbott Laboratories, Seegene Inc., Bruker Corporation, Becton, Dickinson and Company, Thermo Fisher Scientific Inc., Hologic, Inc., T2 Biosystems, Inc., DiaSorin S.p.A., Coris BioConcept, Randox Laboratories Ltd., Genomadix Inc., Talis Biomedical Corporation, bioMérieux SA, Meridian Bioscience, Inc. |

Frequently Asked Questions

The Multiplex PCR segment held approximately 63.53% share in 2025.

The Syndromic Multiplex Diagnostics Market was valued at USD 3.28 Billion in 2025.

The Syndromic Multiplex Diagnostics Market is expected to grow at a CAGR of 7.29% from 2026 to 2035.

Rising demand for rapid, comprehensive pathogen diagnostics combined with growing infectious disease prevalence is the major growth factor.

North America held the largest share of the Syndromic Multiplex Diagnostics Market in 2025, at approximately 41.85%.

Get in Touch