Tanker Shipping Market Report Scope & Overview:

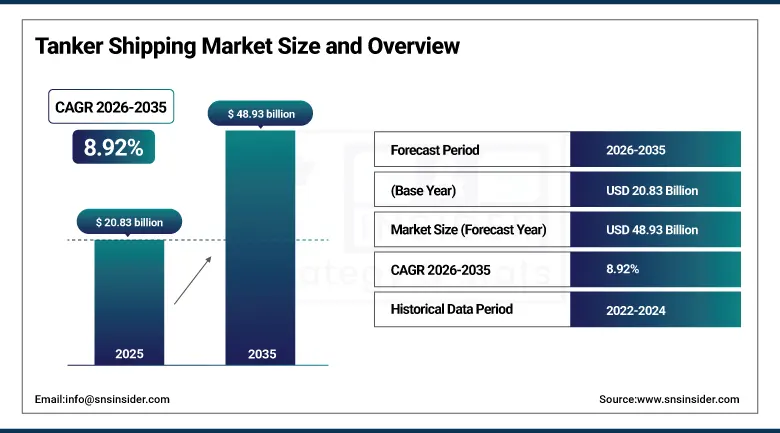

The Tanker Shipping Market valued at USD 20.83 Billion in 2025 and is projected to reach USD 48.93 Billion by 2035, expanding at a CAGR of 8.92% during the forecast period 2026–2035.

The tanker shipping industry is in the throes of a structural transformation, driven by shifts in crude trade flows, the build-out of LNG-linked marine logistics infrastructure and mounting long-haul transportation demand in the wake of geopolitical realignments in global energy markets. Ongoing refinery expansions throughout Asia and the Middle East drive continued volumes of seaborne crude and petroleum products transportation. However, in parallel, there is an increasing trend toward more investments in modernizing fleets where companies are investing in fuel-efficient ships, optimizing emissions, and ensuring compliance with IMO environmental regulations.

In 2025-2026, some of the major tanker companies worldwide made additional investments in their LNG-ready and dual-fuel fleets along with voyage management and emission monitoring systems using AI technologies.

Market Size and Forecast

-

Market Size 2026E: USD 22.68 Billion

-

Market Size 2035: USD 48.93 Billion

-

CAGR: 8.92% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Tanker Shipping Market - Request Free Sample Report

Tanker Shipping Market Trends

-

Rising deployment of AI-powered fleet optimization and predictive vessel maintenance systems.

-

Increasing investments in LNG-ready and low-emission tanker fleets.

-

Growing adoption of cloud-based cargo tracking and real-time voyage monitoring technologies.

-

Expansion of digital maritime logistics and smart shipping infrastructure.

-

Increasing utilization of fuel efficiency analytics and automated navigation technologies.

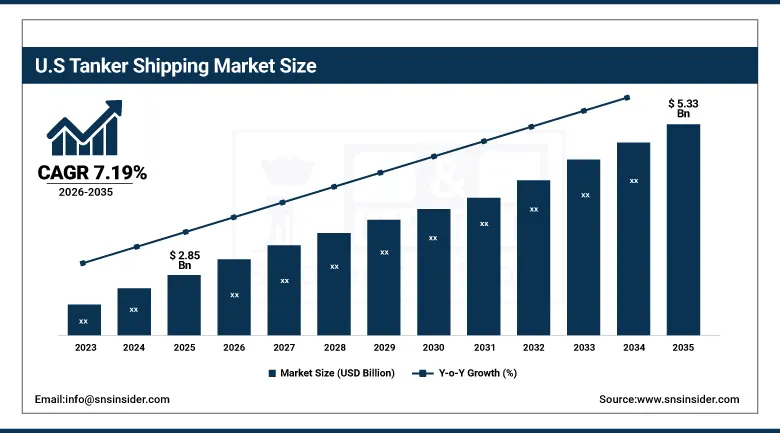

The U.S. Tanker Shipping Market Size Outlook

The U.S. Tanker Shipping Market was valued at USD 2.85 billion in 2025 and is expected to reach approximately USD 5.33 billion by 2035, expanding at a CAGR of 7.19% during 2026–2035.

The United States continues to be one of the principal countries supporting the activities of global tankers through increased exports of crude oil, establishment of facilities for transporting liquefied natural gas (LNG), and innovations in maritime technology. There has been an upsurge in the use of AI-based programs that offer efficient route navigation and fuel saving services. Expansion of business and upgrading of maritime infrastructures will contribute to future growth.

By 2026, some U.S.-based tanker fleet operators adopted AI-based voyage optimization systems in combination with real-time fuel monitoring and emissions compliance technologies.

Tanker Shipping Market Segment Analysis

-

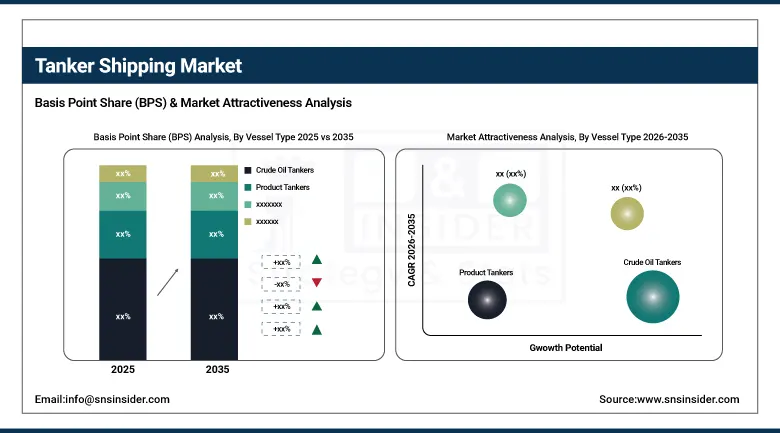

By Vessel Type, Crude Oil Tankers dominated the market with 52.00% share in 2025, while Product Tankers are projected to witness the fastest growth with 9.58% CAGR during the forecast period.

-

By Vessel Size, Large Tankers (VLCC/ULCC) dominated the market with 37.56% share in 2025, while Medium Tankers (Suezmax/Aframax/LR2) are projected to witness the fastest growth with 10.75% CAGR during the forecast period.

-

By Mode Of Transportation, In-Land dominated the market with 54.00% share in 2025, while Coastal projected to witness the fastest growth with 9.93% CAGR during the forecast period.

By Vessel Type, Crude Oil Tankers dominated, while Product Tankers are fastest growing.

The Crude Oil Tankers segment held a revenue share of 52.00% in 2025 owing to increasing demand for long-haul crude transportation across Asia, Europe and North America. The growing offshore oil production activities and the expanding refinery trade networks are underpinning large scale deployment of VLCC and ULCC fleets.

Product Tankers are anticipated to witness the highest CAGR of 9.58% during the forecast period due to increasing global trade of refined petroleum products and increasing regional refinery capacity expansions. The demand for flexible fuel transportation networks and shorter regional shipping routes is driving the deployment of fleets. In 2026 a few shipping operators announced investments in digitally monitored product tanker fleets integrated with automated cargo management systems.

By Vessel Size, Large Tankers (VLCC/ULCC) dominated, while Medium Tankers (Suezmax/Aframax/LR2) are fastest growing.

The Large Tankers (VLCC/ULCC) segment held the highest market share of 37.56% in 2025, fueled by the strong demand for crude oil transportation on intercontinental trade routes. These vessels provide better economies of scale, lower per-barrel transportation costs and higher operating efficiency for long-haul crude shipments.

Medium Tankers (Suezmax/Aframax/LR2) are expected to register the highest CAGR of 10.46% during the forecast period, owing to increasing regional oil trade activities and increasing flexibility requirements in mid-sized ports and diversified trade routes. Medium-capacity vessels are also supported by growing geopolitical trade realignments. In 2025–2026 several tanker operators added to their digitally connected Aframax and Suezmax fleets with predictive maintenance technologies.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.00% |

|

Europe |

Germany |

28.00% |

|

Asia Pacific |

China |

24.00% |

|

Middle East & Africa |

UAE |

5.00% |

|

Latin America |

Brazil |

6.00% |

North America Tanker Shipping Market Insights

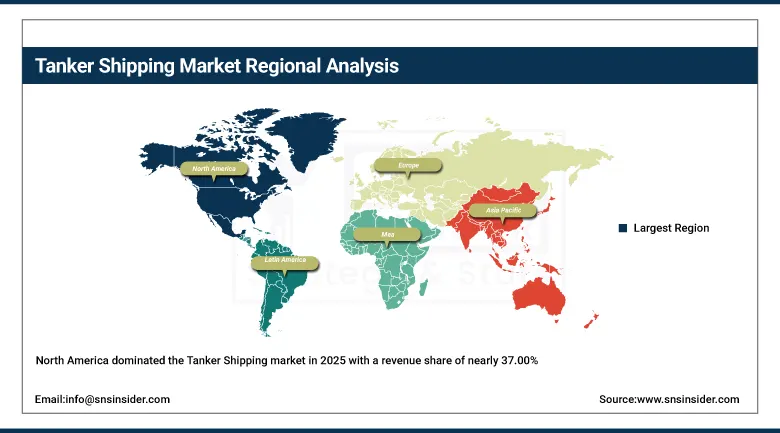

North America dominated the Tanker Shipping market in 2025 with a revenue share of nearly 37.00%, owing to increased crude oil exports, strong LNG shipping infrastructure, and rapid adoption of digital maritime technologies in the U.S. and Canada. Fleet operators are increasingly adopting AI-driven voyage analytics, predictive engine maintenance systems and cloud-enabled cargo monitoring technologies to improve fuel efficiency and reduce operational disruptions. The regional market is growing owing to continued investment in Gulf Coast export terminals and upgrades of maritime logistics infrastructure.

In 2026, a few North American shipping companies improved the rollout of AI-driven route optimization and live fleet tracking platforms for crude oil tanker operations

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Tanker Shipping Market Insights

Europe accounted for approximately 28.00% share in 2025 due to rising maritime sustainability initiatives, increasing investments in low-emission tanker fleets, and growing adoption of digital shipping technologies. Countries such as Germany, Norway, and the Netherlands are creating smart port infrastructure, automated vessel management systems, and AI-based emission monitoring platforms to improve shipping efficiency and environmental compliance.

In 2025-2026 several European tanker operators are fast-tracking the deployment of dual-fuel tanker vessels equipped with sophisticated carbon emission tracking technologies.

Asia Pacific Tanker Shipping Market Insights

Asia Pacific is projected to witness the highest CAGR of 12.09% during the forecast period attributed to rising imports of crude oil, growing refinery infrastructure and increasing energy demand across China, India, Japan and South-east Asia. Shipping companies are increasingly adopting AI-based cargo planning systems, digital fleet management platforms and predictive maritime analytics to improve operational productivity and cargo turnaround efficiency. Regional demand is still supported by fast growth in regional trade routes and refinery export activity.

In 2026, Asia Pacific shipping operators invested more in AI-integrated tanker fleet optimization and smart maritime logistics systems.

Middle East & Africa and Latin America Tanker Shipping Market Insights

The Middle East & Africa market is expected to see stable growth in the coming years due to rising crude oil exports, growing investments in maritime infrastructure and increasing deployment of smart tanker fleet technologies across GCC countries. The expansion of large scale oil export terminals and modernization of shipping logistics network continues to support the market expansion across the region.

Latin America is expected to have a market share of 6.00% in 2025, owing to the increasing offshore oil production activities and increasing regional petroleum trade through Brazil and Mexico. Improvements in the operational efficiency of tanker operations are also being propelled by the growing adoption of cloud-based cargo tracking systems and digital fleet monitoring technologies.

Market Dynamics

Growth Drivers: Increasing demand for crude oil transportation across the world Growth in digital maritime logistics.

The tanker shipping market is growing fast with the increasing global demand for transportation of crude oil, LNG and refined petroleum. Increasing crude demand in Asia and the Middle East is driving higher deployment of VLCC, Suezmax and product tanker fleets as refinery capacities expand across the regions, resulting in greater long-haul crude transportation requirements. Shipping companies are increasingly implementing AI-driven route optimisation platforms, predictive maintenance systems, and cloud-based vessel performance analytics to enhance operational efficiency, fuel optimisation, and cargo management.

In 2025–2026, several global tanker operators adopted AI-based voyage planning systems, in conjunction with emissions monitoring and real-time fleet tracking technologies.

Restraints: Fluctuation in freight rates and strict environmental laws.

Tanker shipping companies still have operational challenges despite positive trade growth, volatile freight rates, rising vessel construction costs, and strict environmental regulations imposed by international maritime organisations. “To meet IMO emission standards and carbon reduction targets will require significant capital investment in cleaner fuel technologies and fleet modernisation. Smaller shipping companies may struggle to deploy advanced digital shipping technologies and low-emission vessel infrastructure.

In 2026, several regulators raised the maritime emissions compliance standards for international tanker fleets plying major trade lanes.

Opportunities: Development of smart shipping infrastructure, low-emission tanker technologies.

There are significant possibilities for growth within the global tanker shipping industry thanks to increased investment in smart infrastructure and sustainable tankers. The use of fleet analytics based on AI, auto navigation systems, cargo digital management tools, and remote vessel monitoring tools has helped shipping companies gain better insights into their operations while reducing fuel usage. The commercialization of LNG tankers and dual-fuel tankers is further helping the industry transform.

By 2025, there were many maritime technology vendors that launched an AI-based tanker optimization solution, which included predictive voyage management.

Recent Developments

-

2026: Frontline plc announced a strategic fleet renewal initiative involving the sale of eight older ECO VLCCs and acquisition of nine latest-generation scrubber-fitted ECO VLCC newbuildings to improve fleet efficiency and emissions compliance.

-

2026: Teekay Corporation expanded its tanker fleet modernization strategy through acquisition of additional Aframax and Suezmax tankers while divesting older vessels to strengthen operational efficiency and reduce average fleet age.

-

2026: Scorpio Tankers Inc. strengthened investments in advanced tanker technologies and strategic maritime energy initiatives while benefiting from elevated product tanker demand and higher global freight rates amid Middle East trade disruptions.

-

2025: Teekay Tankers Ltd. acquired modern LR2 and Suezmax vessels while expanding digitally monitored tanker operations and strengthening balance-sheet flexibility through fleet renewal initiatives.

Tanker Shipping Market Key Players are:

-

Frontline plc

-

Euronav NV

-

Scorpio Tankers Inc.

-

Teekay Corporation

-

International Seaways Inc.

-

DHT Holdings Inc.

-

Bahri

-

Mitsui O.S.K. Lines Ltd.

-

Nippon Yusen Kabushiki Kaisha

-

Stena Bulk AB

-

Hafnia Limited

-

Tsakos Energy Navigation Ltd.

-

Ardmore Shipping Corporation

-

Navig8 Group

-

Okeanis Eco Tankers Corp.

-

TORM plc

-

MOL Chemical Tankers Pte. Ltd.

-

Kuwait Oil Tanker Company

-

COSCO Shipping Energy Transportation Co. Ltd.

-

Overseas Shipholding Group Inc.

Tanker Shipping Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.83 Billion |

| Market Size by 2035 | USD 48.93 Billion |

| CAGR | CAGR of 8.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Retail Automation Assessment, Smart Checkout Technology Trends, AI-Enabled Retail Infrastructure Analysis, DROC & SWOT Analysis, Investment Trends, Supply Chain Evaluation, Consumer Transaction Technology Assessment, and Future Market Opportunity EvaluationChain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Vessel Type (Crude Oil Tankers, Product Tankers, Chemical Tankers) • By Vessel Size (Large Tankers (VLCC/ULCC), Medium Tankers (Suezmax/Aframax/LR2), Small & Handy Tankers (MR/Handysize/Coastal)) • By Mode Of Transportation(Deep sea, Costal, In Land) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Frontline plc, Euronav NV, Scorpio Tankers Inc., Teekay Corporation, International Seaways Inc., DHT Holdings Inc., Bahri, Mitsui O.S.K. Lines Ltd., Nippon Yusen Kabushiki Kaisha, Stena Bulk AB, Hafnia Limited, Tsakos Energy Navigation Ltd., Ardmore Shipping Corporation, Navig8 Group, Okeanis Eco Tankers Corp., TORM plc, MOL Chemical Tankers Pte. Ltd., Kuwait Oil Tanker Company, COSCO Shipping Energy Transportation Co. Ltd., Overseas Shipholding Group Inc. |

Frequently Asked Questions

The Tanker Shipping Market was valued at USD 20.83 billion in 2025.

The market is projected to reach USD 48.93 billion by 2035.

The market is expected to expand at a CAGR of 8.92% during the forecast period.

North America dominated the global market owing to expanding crude oil exports, advanced maritime logistics infrastructure, and increasing adoption of AI-enabled fleet optimization technologies.

Crude Oil Tankers accounted for the largest revenue share of 52.00% in 2025.

Get in Touch