Chemical Tankers Market Report Scope & Overview:

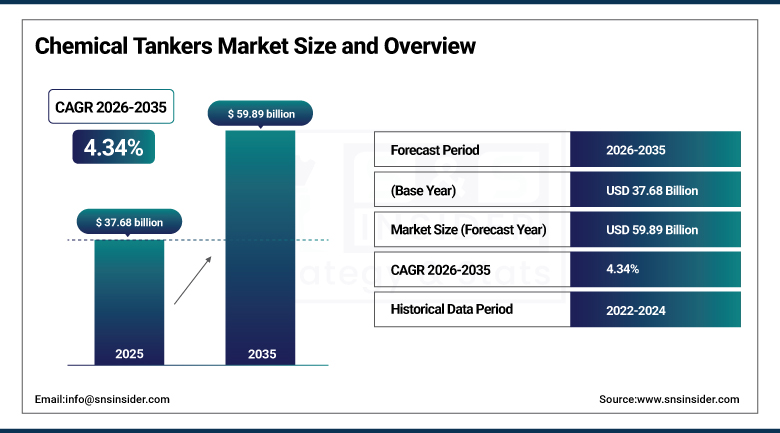

The Chemical Tankers Market was valued at USD 37.68 Billion in 2025 and is expected to reach USD 59.89 Billion by 2035, growing at a CAGR of 4.34% from 2026–2035.

The global chemical tankers market is growing at a steady and commercially broad-based pace. Chemical tankers are specialized marine vessels designed to transport liquid chemicals in bulk. The market is experiencing a shift with fleet size expansion driven by rising demand for specialized chemical transportation, high utilization rates in key regions reflecting strong trade flows, and technological advancements including eco-friendly coatings and digital monitoring across major operators. Export and import volumes of chemicals continue to grow with the Middle East emerging as a dominant exporter, while tanker charter rates for stainless steel tankers saw fluctuations peaking before stabilizing, indicating dynamic market conditions.

In December 2023, Stolt Tankers pioneered the use of a revolutionary durable hull coating on one of its chemical tankers. The new technology enhances fuel efficiency, reduces maintenance costs, and extends the life of chemical tanker hulls, ensuring that the products transported are maintained under the safest and most efficient conditions. The development reflects the commercial pressure on chemical tanker operators to reduce operational costs through advanced hull coating technologies whose fouling resistance reduces propulsion fuel consumption that represents the largest variable operating cost in chemical tanker economics.

Market Size and Forecast

-

Market Size in 2026E: USD 39.32 Billion

-

Market Size by 2035: USD 59.89 Billion

-

CAGR: 4.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Chemical Tankers Market - Request Free Sample Report

Chemical Tankers Market Trends

-

Green shipping fuel transition is accelerating as IMO 2030 and 2050 decarbonization targets drive LNG, methanol, and ammonia-ready chemical tanker newbuilding demand.

-

Digital fleet management adoption is improving chemical tanker efficiency through voyage optimization, predictive maintenance, and real-time cargo monitoring systems.

-

Middle East petrochemical export growth is increasing chemical tanker trade volumes, especially on Middle East–Asia Pacific and Middle East–Europe routes.

-

Specialty chemical and pharmaceutical-grade cargo demand is boosting stainless steel tanker requirement due to strict purity and contamination control needs.

-

IMO Type 2 fleet renewal is accelerating as aging vessels are replaced with eco-design chemical tankers offering better efficiency and cargo segregation capability.

The U.S. Chemical Tankers Market Outlook

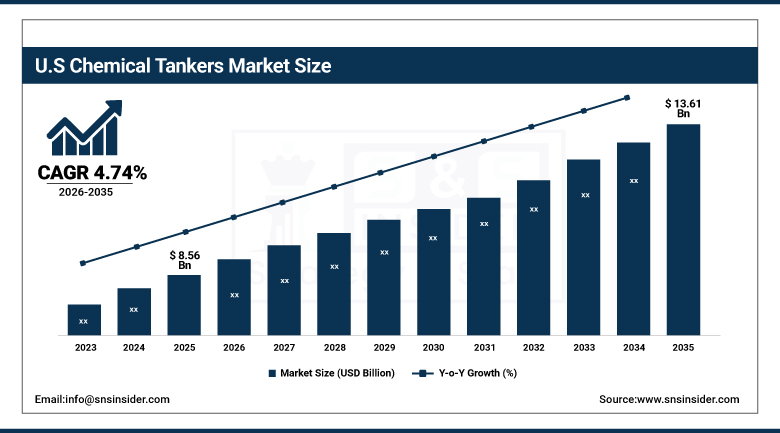

The U.S. Chemical Tankers Market was valued at approximately USD 8.56 Billion in 2025 and is expected to reach approximately USD 13.61 Billion by 2035, growing at a CAGR of approximately 4.74%.

The U.S. is the most commercially significant chemical tankers market within North America’s dominant revenue position. Stolt-Nielsen’s U.S. operations, Odfjell’s Houston commercial presence, Chembulk Tankers, and UNIVAR’s chemical logistics collectively define the domestic chemical tanker commercial environment. The U.S. Gulf Coast’s extraordinary petrochemical complex creates the world’s most commercially significant chemical export loading programme whose ethylene derivatives, methanol, and bulk chemical export volumes sustain above-average Gulf Coast chemical tanker utilization. U.S. shale gas feedstock’s cost advantage creates domestic chemical production whose export competitiveness drives chemical tanker freight demand that compounds with global chemical trade growth.

Odfjell SE announced the construction of six new methanol-fuelled chemical tankers in 2024 with Hyundai Mipo Dockyard, representing a USD 390 million investment in next-generation eco-efficient vessels designed to meet IMO 2030 decarbonization requirements. The newbuilding programme reflects the commercial recognition that the aging global chemical tanker fleet’s progressive replacement with modern eco-efficient vessels is structurally necessary for maintaining competitive commercial positioning as emissions regulation progressively penalizes older higher-carbon-intensity vessels.

Chemical Tankers Market Segment Analysis

-

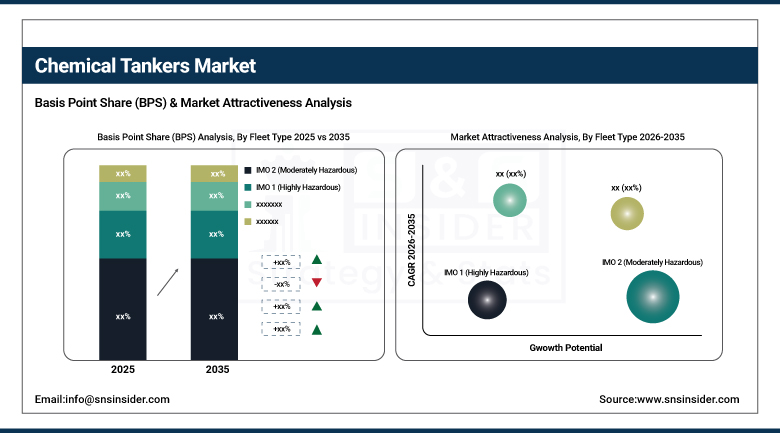

By Fleet Type, the IMO 2 segment dominated the market with approximately 52% share in 2025, while the IMO 1 segment is the fastest growing.

-

By Fleet Size, the deep-sea chemical tankers segment dominated the market with approximately 58% share in 2025, while the coastal chemical tankers segment is the fastest growing.

-

By Product Type, the organic chemicals segment dominated the market with approximately 46% share in 2025, while the vegetable oils & fats segment is the fastest growing.

-

By Fleet Material, the coated/epoxy-coated segment dominated the market with approximately 62% share in 2025, while the stainless-steel segment is the fastest growing.

By Fleet Type, IMO 2 dominates, IMO 1 grows fastest

IMO 2 chemical tankers retained the dominant fleet type position with approximately 52% of the chemical tankers market in 2025. IMO 2’s commercial primacy reflects its position as the most commercially versatile fleet category whose capability to transport moderately dangerous chemicals including organic acids, alcohols, glycols, and petroleum-derived chemical products serves the broadest range of cargo opportunities. The IMO 2 fleet’s balance of specialized cargo handling capability, commercially accessible construction cost relative to IMO 1, and broad cargo approval list creates the most commercially flexible vessel specification that maximizes cargo booking opportunity across diverse chemical product trade flows.

IMO 1 is the fastest-growing fleet type because the highly hazardous chemical trade’s specialty products including chlorinated solvents, toxic acids, reactive chemicals, and hazmat-classified specialty organics require IMO 1 vessel capability whose double-hull construction, independent tank systems, and enhanced safety equipment create commercial barriers that sustain premium charter rates. Each new specialty chemical production facility that generates highly hazardous chemical export creates IMO 1 vessel demand whose limited global fleet creates commercial concentration among technically qualified operators.

By Product Type, organic chemicals dominate, vegetable oils grow fastest

Organic chemicals retained the dominant product type position with approximately 46% of the chemical tankers market in 2025. Organic chemical trade’s commercial primacy reflects the extraordinary scale of global petrochemical industry’s export flows whose methanol, ethylene oxide, propylene oxide, styrene monomer, and acrylonitrile collectively create the most commercially significant liquid chemical cargo category in seaborne trade.

Vegetable oils and fats is the fastest-growing product type because the extraordinary global expansion of palm oil, soybean oil, and rapeseed oil production for food, biofuel, and oleochemical feedstock creates above-average growth in clean product tanker demand for food-grade vegetable oil transport. The global biofuel mandate’s progressive adoption creates vegetable oil feedstock trade whose aggregate with food industry demand creates commercial cargo volumes that compound with each new biofuel facility commissioned.

By Fleet Material, coated dominates, stainless steel grows fastest

Coated chemical tankers retained the dominant fleet material position with approximately 62% of the chemical tankers market in 2025. Epoxy and phenolic epoxy coated steel tank construction creates commercially accessible vessel specification whose lower capital cost relative to stainless steel alternatives creates favorable economics for commodity chemical transport. The approved coating system’s compatibility with the majority of traded chemical products including organic chemicals, inorganic acids, and petroleum derivatives creates broad cargo approval lists that sustain coated vessel’s commercial versatility.

Stainless steel chemical tankers are the fastest-growing fleet material because pharmaceutical-grade chemical, food additive, and ultra-high-purity specialty chemical trade’s growth creates above-average demand for stainless steel cargo containment whose contamination-free delivery capability creates premium charter rates and long-term contract preference among quality-sensitive chemical shippers. Each pharmaceutical company that specifies stainless steel tanker transport for API precursors and excipients creates structured demand that sustains premium stainless steel charter pricing above coated alternatives.

By Fleet Size, deep-sea dominates, coastal grows fastest

Deep-sea chemical tankers retained the dominant fleet size position with approximately 58% of the chemical tankers market in 2025. The 10,000-50,000 DWT deep-sea vessel’s role in intercontinental chemical trade between major production and consumption centers, U.S. Gulf to Europe, Middle East to Asia Pacific, and Southeast Asia to Western markets, creates the most commercially significant aggregate freight revenue in the chemical tanker industry.

Coastal chemical tankers are the fastest-growing size segment because Asia Pacific’s extraordinary intra-regional chemical trade growth, European short-sea chemical distribution, and Middle Eastern coastal chemical supply chain development create above-average coastal vessel demand. Each new chemical plant in India, Vietnam, or Indonesia that requires coastal distribution of produced chemicals to domestic consumption centers creates coastal tanker demand whose aggregate across the rapidly industrializing Asia Pacific region creates above-average fleet utilization.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

44.2% |

|

Latin America |

Brazil |

44.2% |

North America Chemical Tankers Market Insights

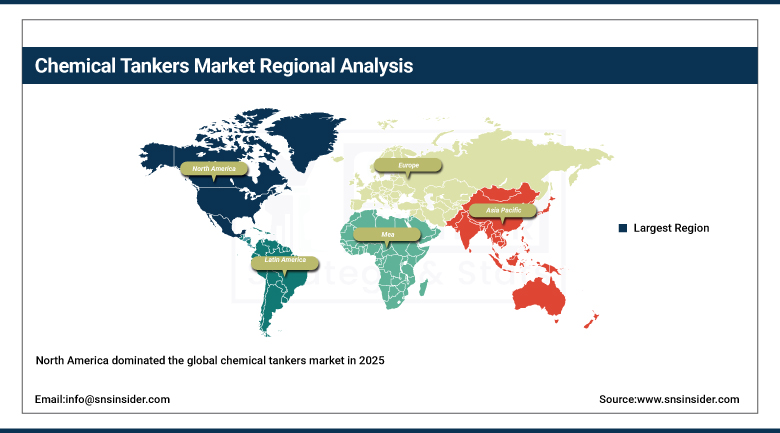

North America dominated the global chemical tankers market in 2025 as the largest chemical production and export region. The United States accounts for approximately 87.4% of North American revenues through its U.S. Gulf Coast’s extraordinary petrochemical export programme, Stolt-Nielsen and Odfjell’s commercial hub operations, and the shale gas feedstock advantage that creates competitive chemical export economics. The U.S. Chemical Manufacturers Association’s documentation of 40% global chemical export share from U.S. Gulf Coast facilities reflects the commercial scale whose chemical tanker demand sustains North America’s market leadership.

Canada contributes approximately 12.6% of North American revenues through its chemical industry’s St. Lawrence trade lane activity, the petrochemical complex’s domestic chemical distribution, and the resource sector’s chemical supply logistics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chemical Tankers Market Insights

Europe is a technically sophisticated chemical tankers market where Rhine and European inland chemical tanker trades, North Sea and Baltic coastal chemical distribution, and deep-sea import procurement create diverse fleet deployment. Germany accounts for approximately 22.3% of European revenues through its chemical industry’s Rhine River barge trade, BASF’s Ludwigshafen complex creating the world’s largest chemical site’s logistics requirement, and the export chemical trade’s North Sea loading programme.

The Netherlands, Belgium, and the UK are significant secondary markets where Rotterdam’s role as Europe’s principal chemical import hub, the major European chemical terminal infrastructure, and the coastal tanker distribution network create consistent chemical tanker freight demand.

Asia Pacific Chemical Tankers Market Insights

Asia Pacific is the fastest-growing regional chemical tankers market, driven by China’s extraordinary chemical production expansion, India’s petrochemical industry growth, South Korea’s chemical export, and Southeast Asia’s industrialization creating growing chemical import demand. China accounts for approximately 44.8% of Asia Pacific revenues through its position as both the world’s largest chemical producer and consumer, whose intra-regional trade and import procurement collectively create the most commercially significant Asia Pacific chemical tanker demand.

South Korea’s Lotte Chemical and Hanwha Solutions’ chemical export, India’s chemical industry’s coastal distribution, and Singapore’s chemical terminal hub create significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional commercial momentum.

MEA & Latin America Chemical Tankers Market Insights

Saudi Arabia leads MEA revenues at approximately 44.2% through SABIC’s and Saudi Aramco’s extraordinary petrochemical export programme, the Jubail and Yanbu industrial city’s chemical production whose deep-sea tanker loading creates the Middle East’s most commercially significant chemical export trade. Brazil leads Latin American revenues at approximately 44.2% through Braskem’s chemical production, the petrochemical complex’s coastal distribution, and the agricultural chemical import demand.

UAE’s ADNOC Distribution chemical export and the growing Gulf petrochemical industry’s tanker demand create significant MEA secondary markets whose combined freight activity reflects the extraordinary scale of Middle Eastern chemical production investment.

Market Dynamics

Growth Drivers: Global chemical trade volume growth and Middle East petrochemical export expansion creating freight demand

Global chemical trade volume growth is the chemical tankers market’s most commercially certain structural growth driver. The ICIS estimate that global liquid chemical seaborne trade exceeds 200 million tons annually, growing at 3-4% per annum, creates proportional chemical tanker freight demand whose commercial scale sustains fleet investment and charter market activity. Each new petrochemical plant that creates chemical export volume creates long-duration tanker demand whose contract of affreightment establishes structured commercial relationships that sustain fleet investment confidence. The chemical industry’s geographic restructuring toward Middle Eastern and Asian production, whose distance from European consumption creates longer average voyage distances, creates ton-mile demand growth that exceeds volume growth in commercial impact.

Middle Eastern petrochemical export expansion through SABIC, ARAMCO, and ADNOC’s capacity investment programmes is creating above-average trade lane activity on long-haul chemical routes whose employment sustains above-average deep-sea tanker utilization and charter rates. Each new Middle Eastern ethane cracker or methanol plant that begins chemical export creates tanker demand whose duration reflects the 30-year operational life of petrochemical facilities whose amortized freight demand sustains long-term commercial relationships with major chemical tanker operators.

Restraints: IMO decarbonization regulation creating fleet replacement investment and chemical cargo price volatility moderating trade volumes

IMO’s CII (Carbon Intensity Indicator) regulation and the progressive tightening toward 2030 and 2050 targets create capital investment requirement for fleet operators whose older vessels’ carbon intensity above CII rating thresholds creates either vessel speed reduction, retrofitting investment, or early retirement that reduces fleet productivity. Each older vessel that cannot meet tightening CII requirements creates either commercial restriction or replacement procurement whose aggregate across the aging chemical tanker fleet creates capital expenditure pressure that moderates fleet expansion investment.

Chemical feedstock and product price volatility, driven by crude oil price cycles and supply disruption events, creates periodic reductions in chemical production utilization and trade volume that moderate freight demand. Each chemical plant curtailment during low-margin periods creates cargo availability reduction that affects tanker utilization rates and charter market dynamics whose commercial impact creates revenue volatility for tanker operators.

Opportunities: Green methanol tanker fleet development and stainless-steel tanker premium market

Green methanol as a marine fuel creates dual commercial opportunity for chemical tanker operators whose newbuilding programmes specify methanol dual-fuel propulsion that simultaneously enables methanol cargo transport and green fuel consumption. Each methanol dual-fuel chemical tanker creates operational flexibility whose green fuel adoption creates regulatory compliance advantage and potential premium commercial positioning in emissions-conscious cargo owner procurement.

Stainless steel tanker premium market expansion driven by pharmaceutical, food-grade, and ultra-high-purity specialty chemical trade growth represents the most commercially value-accretive fleet segment. Each new pharmaceutical company that specifies stainless steel maritime transport for API precursors creates contract of affreightment relationships whose premium charter rate substantially exceeds coated vessel economics.

Recent Developments:

-

2026: Odfjell SE continued fleet modernization with eco-design stainless steel chemical tankers and invested in digital cargo tracking systems to improve operational efficiency and safety compliance.

-

2025: MOL Chemical Tankers increased global chemical tanker capacity through newbuilding deliveries and long-term charter contracts supporting Asia–Middle East petrochemical trade expansion.

-

2025: Navig8 Chemical Tankers enhanced its chemical tanker pool operations with improved voyage optimization systems and stronger participation in global MR tanker charter markets.

Chemical Tankers Market Key Players are:

-

Stolt-Nielsen Limited

-

Odfjell SE

-

Navig8 Group

-

MISC Berhad

-

Bahri (National Shipping Company of Saudi Arabia)

-

MOL Chemical Tankers Pte. Ltd.

-

Iino Kaiun Kaisha Ltd.

-

Ardmore Shipping Corporation

-

Maersk Tankers

-

Team Tankers International Ltd.

-

Stena Bulk AB

-

Nordic Tankers A/S

-

Teekay Tankers Ltd.

-

Hafnia Limited

-

MTM Ship Management

-

Navig8 Chemical Tankers

-

Scorpio Group

-

d’Amico International Shipping

-

International Seaways, Inc.

-

Pacific Basin Shipping Ltd.

Chemical Tankers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.68 Billion |

| Market Size by 2035 | USD 59.89 Billion |

| CAGR | CAGR of 4.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fleet Type (IMO 1/Highly Hazardous, IMO 2/Moderately Hazardous, IMO 3/Low Hazard) • By Fleet Size (Inland Chemical Tankers 1,000–4,999 DWT, Coastal Chemical Tankers 5,000–9,999 DWT, Deep-Sea Chemical Tankers 10,000–50,000 DWT) • By Fleet Material (Stainless Steel, Coated/Epoxy-Coated, Phenolic Epoxy) • By Product Type (Organic Chemicals, Inorganic Chemicals, Vegetable Oils & Fats, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Stolt-Nielsen Limited, Odfjell SE, Navig8 Group, MISC Berhad, Bahri (National Shipping Company of Saudi Arabia), MOL Chemical Tankers Pte. Ltd., Iino Kaiun Kaisha Ltd., Ardmore Shipping Corporation, Maersk Tankers, Team Tankers International Ltd., Stena Bulk AB, Nordic Tankers A/S, Teekay Tankers Ltd., Hafnia Limited, MTM Ship Management, Navig8 Chemical Tankers, Scorpio Group, d’Amico International Shipping, International Seaways, Inc., Pacific Basin Shipping Ltd. |

Frequently Asked Questions

The Chemical Tankers Market is expected to grow at a CAGR of 4.34% from 2026 to 2035.

The Chemical Tankers Market was valued at USD 37.68 Billion in 2025.

Rising demand for chemicals across pharmaceuticals, agriculture, and manufacturing driving efficient and advanced chemical transportation solutions.

IMO 2 dominated the Chemical Tankers Market with approximately 52% share in 2025, while IMO 1 is the fastest growing segment.

Get in Touch