Teen Driver Technology Market Overview

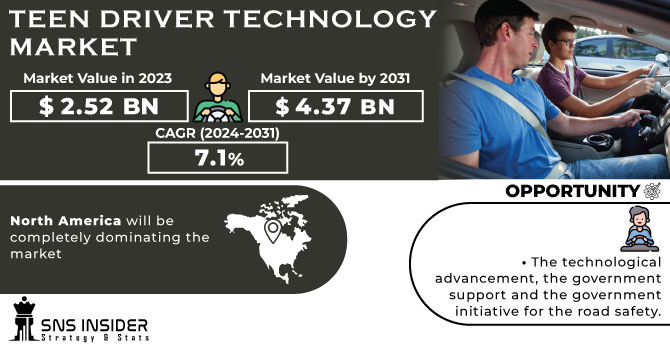

Teen Driver Technology market size was valued at USD 2.52 billion in 2023 and is expected to reach at USD 4.37 billion by 2031, and grow at a CAGR of 7.1% over the forecast period of 2024-2031.

The automotive teen technology is basically recording the records of the driver as well coaching the driver at the same time, the teen technology is an in-built system for the children learning cars as well as a new driver who is trying to learn. It has a powerful system where you can set speed limit alerts, also volume alerts, the major reasons behind this system are to make sure the parents or the guardians keep a record on the children as the teens make poor driving decision which includes speeding over limit, also not using the seat belts, the teen technology also creates a report card which includes the distance covered or any crossed speed limits. The safety for teens while driving and the concern of parents and guardians to make sure their children is not making any mistake or taking bad decisions while driving is the driving factor.

Get more information on Teen Driver Technology Market - Request Sample Report

Impact of Covid 19

During the covid 19 every industry faced an adversity, automotive industry had an immense negative effect due to the rules and regulations of the government also because of the lockdown there were many economic issues for each and every individual which resulted in less demand of the automotive teen testing systems, also the production was hampered as the lockdown rules made it very difficult for the supply chain management to operate as the routes were disrupted, Also the purchasing power of the consumers is the major factor for every industry so did automotive industry the situation of covid 19 had an impact on the automotive test market as there was a change in the buying pattern of the consumers .

Market Dynamics

Drivers

-

The increase in the awareness of the road safety concerns.

-

The rise in the young population all around the globe and the concern of guardian and parents for the safety of their teen children’s.

Restrain

-

Creating the awareness of teen driving technology in the emerging countries.

Opportunities

-

The technological advancement, the government support and the government initiative for the road safety.

Challenges

-

Managing the technological errors caused by the internal or external factors.

-

Lack of skilled labors.

Impact of Russia Ukraine War

There was a stop in production in Europe region due to the lack of supply of parts from Ukraine. The value chain was disrupted due to the Russia Ukraine war, also the supply chain was disrupted which made the OEMs and suppliers to think about the continuation of trade with Russia. This war had an immense impact globally but Russia had to face many issues like loss of infrastructure, skilled labours and many more, it is also said that there will be fluctuations in price. This report will give you an overview about how the Russia Ukraine war had a negative impact on the automotive and the test technology market system.

Impact of ongoing recession

According to the experts Recession will have a negative impact on the automotive industry as we have already seen during the covid 19. Global economic issue brings many problems like change in the buying pattern of the consumers also change in the decision-making regarding expenses, this sums up the overall situation and to conclude the automotive teen driver technology market will have a negative impact due to the less demand caused by the economic barriers.

Market segmentation analysis

The automotive teen driver technology is divided into three segments by type, by features and by the sales channel, by type includes commercial vehicles and the passenger vehicle mostly passenger vehicles are for individual use and the commercial vehicle include for the business purpose, Automotive vehicle mostly is known for the features they provides, features are very important for any automotive industry to grow so the teen driver technology mostly includes system alerts, forward braking system which is very important for the teen driver as they have the poor decision making due to the lack of experience, and the third one is by sales channel which includes aftermarket and the poems .

Market segmentation

By Vehicle Type

-

Commercial Vehicle

-

Passenger Vehicle

By Features

-

Music Volume Alert

-

Speed limit alert

-

Forward automatic braking

-

Forward collision alert

By Sales Channel

-

Aftermarket

-

Original Equipment Market

Regional Analysis

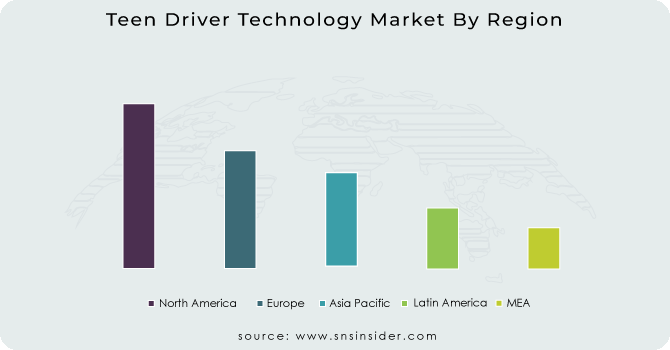

North America will be completely dominating the market due to the rise in the young population and the demand for the vehicles in every house hold as the comfort level is becoming the priority when the mode of transportation is considered. The growth of technological advancement and the awareness of the teen driving technology is the driving factor.

APAC is also expected to grow during the forecast period due to the rules imposed by the government for the safety purpose and the also due to the rise in the accidents. This increases the demand for safety features in the vehicles which ultimately boosts the teen driver technology market.

Get Customized Report as per your Business Requirement - Request For Customized Report

REGIONAL COVERAGE:

North America

-

USA

-

Canada

-

Mexico

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

Asia-Pacific

-

Japan

-

South Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of the Middle East & Africa

Latin America

-

Brazil

-

Argentina

-

Rest of Latin American

Key Players

The major key players are Ford motor company, Toyota Motor sales, Hyundai motor vehicle, general motor vehicle, AAA insurance, Winsonic Electronics Ltd, Mitsubishi electric Corporation, Robert Bosch GmbH, and other players listed in the final report.

Toyota Motor sales-Company Financial Analysis

Frequently Asked Questions

The technological advancement, the government support and the government initiative for the road safety.

This market is divided into 3 segments by type, by feature and by sale channel.

North America will be completely dominating the market due to the rise in the young population and the demand for the vehicles in every house hold as the comfort level is becoming the priority.

The market size for this market will be USD 4.37 billion by the year 2031.

Get in Touch