Artificial Intelligence In Supply Chain Market Growth & Statistics:

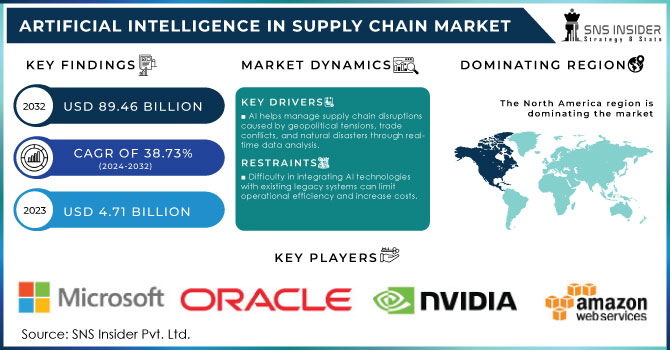

AI in Supply Chain Market size was valued at USD 4.71 billion in 2023 and is expected to reach USD 89.46 billion by 2032, growing at a CAGR of 38.73% from 2024-2032.

AI in the Supply Chain market has seen explosive growth as firms introduce AI-driven instruments to improve logistics, procurement, inventory management, and demand forecasting. For instance, machine learning, predictive analytics, natural language processing, and robotic process automation are used to improve supply chain management. Supply chains have become one of the major areas of AI growth for many reasons.

Get more information on Artificial Intelligence (AI) in Supply Chain Market - Request Sample Report

First, global logistics is becoming increasingly complex, and companies need real-time visibility and quick decision-making to deal with such issues as geopolitical tensions, trade wars, and natural disasters. AI tools help firms make accurate predictions about delays, optimize transportation, and manage inventory better, helping them save costs and minimize waste. Second, the demand for personalized goods and services is increasing, and e-commerce firms can use AI tools to meet these demands. Finally, companies use AI-driven platforms to improve the sustainability of their supply chains by optimizing operations to reduce waste and environmental pollution. Companies can determine the most efficient transportation routes to reduce fuel consumption and to lower carbon emissions.

Alternatively, businesses can use AI to predict demand much more accurately, lengthening the orders and thus helping to minimize the need for the production of items that will not be sold. For Instance, research states that AI-powered logistics solutions can reduce transportation costs by up to 15% and lower carbon emissions by 5-10% through optimized route planning. Additionally, companies using AI for demand forecasting have improved forecast accuracy by up to 20%, helping them reduce excess inventory and production waste by as much as 30%, directly contributing to more sustainable operations.

Around 60% of supply chain leaders have already adopted AI technologies, and firm demand for AI-driven solutions in supply chains is strong. Supply chain companies are among those most likely to adopt AI-driven solutions quickly. Increased Internet of Things device and sensor deployment rates in warehouses, transportation, and manufacturing have been accompanied by the significant generation of raw data. The AI-advanced division is essential because these platforms make predictive suggestions, helping supply chain firms streamline their operations and respond faster to potential problems.

Additionally, Modular robotics are essential in the Artificial Intelligence in Supply Chain market, providing flexible and scalable automation solutions that boost operational efficiency in warehouses. These robots can be quickly reconfigured for various tasks, such as picking, packing, and sorting, allowing them to adapt to evolving demands. Notable brands in this sector include Boston Dynamics, which offers the versatile Stretch robot designed for efficient material handling, and Kiva Systems known for its mobile robotic systems that optimize warehouse operations and inventory management.

Artificial Intelligence In Supply Chain Market Dynamics

Drivers

-

AI helps manage supply chain disruptions caused by geopolitical tensions, trade conflicts, and natural disasters through real-time data analysis.

-

AI provides predictive insights, enabling faster, more accurate decision-making in logistics and inventory management.

-

AI helps companies forecast demand, manage order fluctuations, and ensure timely deliveries, enhancing customer satisfaction.

Artificial Intelligence in Supply Chain market is essential for demand forecasting, order fluctuation management, and timely deliveries. As a result, all of these benefits lead to increased levels of customer satisfaction. Owing to the incorporation of sophisticated algorithms and machine learning tools, AI can effectively analyze the information stored in the company’s databases about the sales performed and the relevant existing trends within the target market and the propensity of clients for purchasing goods in certain seasons or under particular circumstances. Thus, companies are able to predict the future demand and adjust their inventories accordingly, substantially minimizing the risks of understocking or overstocking. Consequently, the latter effect triggers the subsequent decrease in associated costs, while customer satisfaction is increased due to the enhanced level of product availability.

Furthermore, the capabilities of AI allow for the effective management of order fluctuations, as supply chain resources can be dynamically adjusted in case of sudden changes in the customers’ behaviour, time-dependent demand due to the festive season or other reasons. Finally, AI is vital for timely deliveries of goods, as the currently existing processes of real-time tracking and route optimization can also be enhanced with the new technologies. As a result, AI can optimize both the delivery vans’ routes and the distribution processes in order to arrive at the final destination as quickly as possible, anticipating traffic jams or unfavorable weather conditions. All in all, AI is critical for the efficient functioning of supply chains, which, in turn, leads to better customer satisfaction.

Restraints

-

Difficulty in integrating AI technologies with existing legacy systems can limit operational efficiency and increase costs.

-

A lack of skilled personnel with expertise in AI and data analytics can slow down implementation and optimization efforts.

-

Companies face challenges related to data security and privacy, which can hinder the adoption of AI solutions.

There are a large number of concerns about data security and privacy in the Artificial Intelligence in the Supply Chain market, and they create severe limitations for the confident use of AI technologies. On the one hand, firms accumulate extensive human and machine data. On the other hand, suppliers and logistics companies generate extensive data on anything from on-time deliveries to order frequency. The companies use this information to train AI models, enabling better forecasting, smarter contentment, and efficient product ordering and transport.

The collection and processing of data carry significant risks, as strict regulations like the GDPR and the California Consumer Privacy Act impose stringent data privacy standards on companies. One of the inevitable consequences of data violation or unauthorized information access could be serious legal machinery problems, in addition to a serious blow to a company’s reputation and substantial financial consequences. Therefore, for fear of breaking customer confidence and offending the law, companies are afraid of taking on existent AI solutions that require massive data management or approaches that would need third-party dataset support. Moreover, differently-shaped and multiple-formed modern norms introduce a pretty major challenge to companies’ legal and IT teams, particularly for smaller companies that often have limited personnel and little experience with such levels of regulative pressure. This is, on the whole, a serious avoidance for companies of the prospects of advanced AI use in their supply chains because they cannot leverage big data analytics and machine learning for operational improvement and further enhancement of customer satisfaction.

Here's a table regarding concerns about data security and privacy in the Artificial Intelligence in Supply Chain market:

| Concerns and Impacts | Data Sources | Consequences of Data Breaches |

|

Extensive concerns about data security and privacy create limitations for AI adoption. |

Companies collect extensive human and machine data, while suppliers and logistics companies generate data on deliveries and order frequency. |

Legal challenges, reputational damage, and significant financial losses due to data breaches or unauthorized access. |

|

Stricter regulations like GDPR and the California Consumer Privacy Act impose data privacy standards on companies. |

Data is used to train AI models for improved forecasting, smarter fulfillment, and efficient product ordering and transport. |

Fear of losing customer trust and facing legal penalties deters companies from adopting AI solutions requiring large data management. |

|

Navigating multiple regulations presents challenges for legal and IT teams, especially in smaller companies. |

Limited personnel and experience make it harder for smaller firms to cope with regulatory pressures. |

Overall, these factors hinder the ability to leverage big data analytics and machine learning for operational improvements and enhanced customer satisfaction. |

Artificial Intelligence In Supply Chain Market Segment Analysis

By Offering

In 2023, the software segment led the market, accounting for more than 42.5% of total revenue.AI software delivers a broad array of functionalities within the supply chain, including demand forecasting, inventory optimization, predictive maintenance, and automated decision-making. This adaptability allows businesses to address different challenges and customize solutions to meet their unique needs. Moreover, AI software can be easily scaled to accommodate the size and complexity of different supply chains.

The services segment is expected to experience significant growth with a strong CAGR during the forecast period. For optimal performance, AI supply chain solutions necessitate ongoing maintenance and updates. Service providers offer support packages that ensure AI systems function effectively and address any technical issues that may arise. As end users increasingly look for measurable results from their AI investments, service providers assist businesses in establishing key performance indicators (KPIs) and evaluating the return on investment (ROI) of their AI initiatives, emphasizing the critical importance of AI in enhancing supply chain operations.

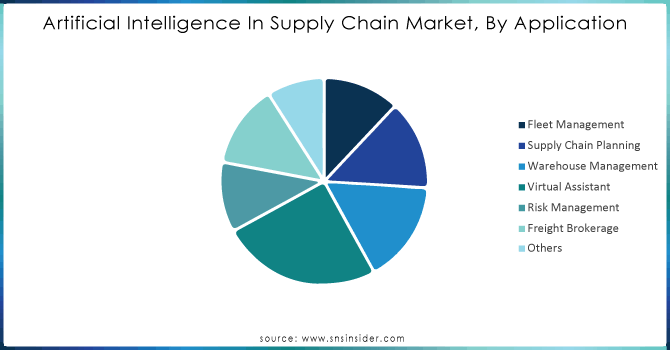

By Application

Supply chain planning segment dominated the market in 2023, with a significant revenue share of 33.5%. AI algorithms analyze historical data, information about sales, and external factors to forecast demand accurately. As a result, companies can maintain the right inventory level and avoid both stockouts and overstocking issues, which are expensive to eliminate. Moreover, AI considers such components as traffic, fuel prices, and delivery requirements when finding the best route and time to transport goods. As a result, transportation expenses are reduced, and items are delivered faster.

Warehouse management is expected to be the most rapidly growing segment at a CAGR during the forecast period. AI systems can perform routine tasks, such as picking, packing, and sorting orders, eliminating mistakes typical for manual work. Additionally, AI algorithms can identify the best picking route and packing type that depends on the size and weight of an element and how faraway it should be delivered. Thus, employees do not need to traverse warehouses and can act faster, as packing is optimized.

Need any customization research on Artificial Intelligence (AI) in Supply Chain Market - Enquiry Now

By End-Use

In 2023, the automotive segment dominated the market, capturing a significant revenue share of 18.2%. The growing demand for Electric Vehicles (EVs) and Autonomous Vehicles (AVs) presents supply chain challenges due to the complexity of their production processes. AI supply chain solutions adeptly manage the intricate networks of suppliers essential for EV and AV manufacturing, ensuring the timely delivery of specialized components. Furthermore, AI-driven quality control systems ensure that these advanced vehicles meet strict safety and performance standards.

The retail segment is anticipated to experience substantial growth with a strong CAGR throughout the forecast period. AI harnesses historical sales data, customer trends, and external factors to improve the accuracy of demand forecasting. This capability enables retailers to maintain optimal inventory levels, thereby avoiding stockouts that can frustrate customers and overstocking that can waste storage space and lead to markdowns. Additionally, AI supports integrated inventory management across both online and physical stores, facilitating seamless order fulfillment regardless of the sales channel. It also provides real-time tracking of goods throughout the supply chain, enhancing transparency and control over retail operations.

Regional Analysis

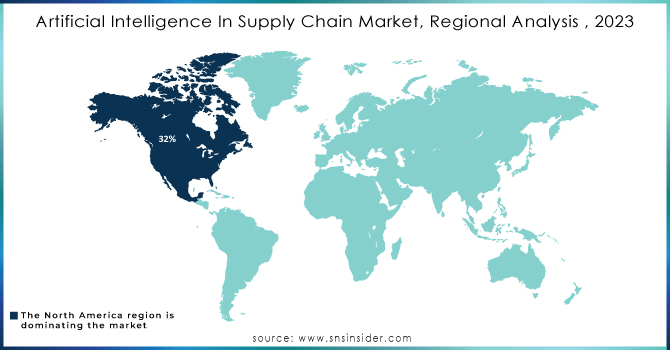

In 2023, North America led the AI in supply chain market share, capturing a significant revenue of 39.2%. Companies in this region face intense competition and the imperative to lower costs while delivering exceptional customer service. AI supply chain solutions streamline task automation, analyze large datasets, and generate actionable insights that enhance efficiency, transparency, and agility throughout the supply chain.

The U.S. is expected to experience the highest growth rate in artificial intelligence in the supply chain market during the forecast period. The manufacturing and logistics sectors in the U.S. are currently grappling with labor shortages, and AI can help by allowing human workers to focus on higher-value tasks that require specialized skills and expertise. Additionally, the U.S. is at the forefront of AI research and development, driving the creation of advanced AI solutions tailored for supply chain applications.

Meanwhile, Canadian artificial intelligence in supply chain market also maintained a strong foothold in North America in 2023. Canadian companies face challenges in managing complex supply chains that often span vast geographical distances. AI improves delivery route optimization by considering factors such as weather conditions and traffic patterns, ensuring efficient and cost-effective transportation of goods across Canada’s extensive landscape.

Key Players

-

IBM - (IBM Watson Supply Chain, IBM Sterling Supply Chain Insights)

-

Microsoft - (Azure AI for Supply Chain, Dynamics 365 Supply Chain Management)

-

SAP - (SAP Integrated Business Planning, SAP Leonardo)

-

Oracle - (Oracle Supply Chain Management Cloud, Oracle AI Applications)

-

Amazon Web Services - (AWS) (AWS IoT, AWS SageMaker)

-

Google Cloud - (Google Cloud AI, Google Cloud Supply Chain Solutions)

-

Siemens - (Siemens Digital Logistics, Siemens Supply Chain Management)

-

C3.ai - (C3 AI Supply Chain Suite, C3 AI Predictive Maintenance)

-

JDA Software - (now Blue Yonder) (Blue Yonder Luminate Platform, Blue Yonder Demand Planning)

-

Kinaxis - (RapidResponse, Kinaxis AI-Enabled Supply Chain Management)

-

Manhattan Associates - (Manhattan Active Supply Chain, Manhattan Active Warehouse Management)

-

SAP Ariba - (Ariba Network, SAP Ariba Procurement Solutions)

-

Alibaba Cloud - (Alibaba Cloud Intelligent Supply Chain, Alibaba Cloud Data Analytics)

-

ClearMetal - (ClearMetal Inventory Optimization, ClearMetal Demand Sensing)

-

Zebra Technologies - (Zebra MotionWorks, Zebra Savanna)

-

NVIDIA - (NVIDIA Clara for Supply Chain, NVIDIA Omniverse)

-

Ineight - (Ineight Supply Chain Software, Ineight Project Management)

-

Llamasoft - (Llamasoft Supply Chain Guru, Llamasoft Demand Planning)

-

Everledger - (Everledger Supply Chain Transparency, Everledger AI-driven Solutions)

-

Logility - (Logility Voyager Solutions, Logility Demand Planning)

Recent Developments

In April 24, SAP SE announced major AI enhancements in its supply chain solutions, aimed at boosting productivity and efficiency in manufacturing by enabling real-time data analysis for better decision-making and streamlined processes.

In April 24, Vitesco Technologies GmbH partnered with DHL Group to strengthen supply chain resilience in the automotive sector by consolidating cargo volumes and optimizing transport solutions for eco-friendliness and cost efficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.71 billion |

| Market Size by 2032 | USD 89.46 billion |

| CAGR | CAGR 38.73 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Hardware, Software, And Services) • By Technology (Machine Learning, Natural Language Processing, Context-Aware Computing, And Computer Vision) • By Application (Fleet Management, Supply Chain Planning, Warehouse Management, Virtual Assistant, Risk Management, Freight Brokerage, And Others) • By End-User Industry (Automotive, Aerospace, Manufacturing, Retail, Healthcare, Consumer-Packaged Goods, Food And Beverages, And Inventory Management, Planning & Logistics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amazon Web Services, Inc., IBM Corporation, Intel Corporation, Logility, Inc., Micron Technology, Inc., Microsoft Corporation, NVIDIA Corporation, Oracle Corporation, SAP SE, Xilinx, Inc. |

| Key Drivers | •AI helps manage supply chain disruptions caused by geopolitical tensions, trade conflicts, and natural disasters through real-time data analysis •AI provides predictive insights, enabling faster, more accurate decision-making in logistics and inventory management. •AI helps companies forecast demand, manage order fluctuations, and ensure timely deliveries, enhancing customer satisfaction. |

| Market Restraints | •Difficulty in integrating AI technologies with existing legacy systems can limit operational efficiency and increase costs. •A lack of skilled personnel with expertise in AI and data analytics can slow down implementation and optimization efforts. •Companies face challenges related to data security and privacy, which can hinder the adoption of AI solutions. |

Frequently Asked Questions

The primary growth tactics of Artificial Intelligence in Supply Chain market participants include merger and acquisition, business expansion, and product launch.

North America dominates artificial intelligence in the supply chain market and will maintain its dominance throughout the projected period.

The segments covered in the Artificial Intelligence in Supply Chain Market report for study are on the Basis of Offering, Technology, Application, and End-user Industry.

Greater visibility and transparency in supply chain data and processes are desired and AI adoption to improve customer service and satisfaction.

The projected market size for the Artificial Intelligence In Supply Chain Market is USD 97 billion by 2032.

Get in Touch