Threat Intelligence Platform Market Report Scope & Overview:

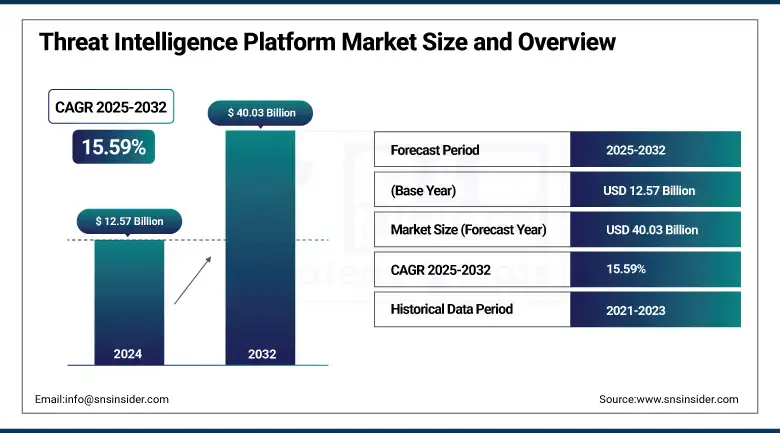

The Threat Intelligence Platform Market size was valued at USD 12.57 billion in 2024 and is expected to reach USD 40.03 billion by 2032, expanding at a CAGR of 15.59% over the forecast period of 2025-2032.

The Threat Intelligence Platform Market is flourishing on account of the growing demand for complex cyber threats across different end-users. These systems enable organizations to identify, analyze, and respond to potential threats by pulling data from many sources and applying sophisticated analytics and AI. The rise of cloud, IOT, and remote work setups has widened the low degree of requirement for real-time, automatic threat detection. The BFSI, IT & telecom, and government are the main adopters. North America dominates, and Asia Pacific is growing the fastest. threat intelligence platform market companies such as IBM, Cisco, and Palo Alto Networks are changing the future of technology with AI-based solutions in security.

To Get more information On Threat Intelligence Platform Market - Request Free Sample Report

According to the research, organizations leveraging advanced threat intelligence platforms have reduced threat detection time by 42%, improved incident mitigation speed by 37% through automation, and now ingest data from over 15 external feeds, underscoring the need for centralized, responsive security solutions.

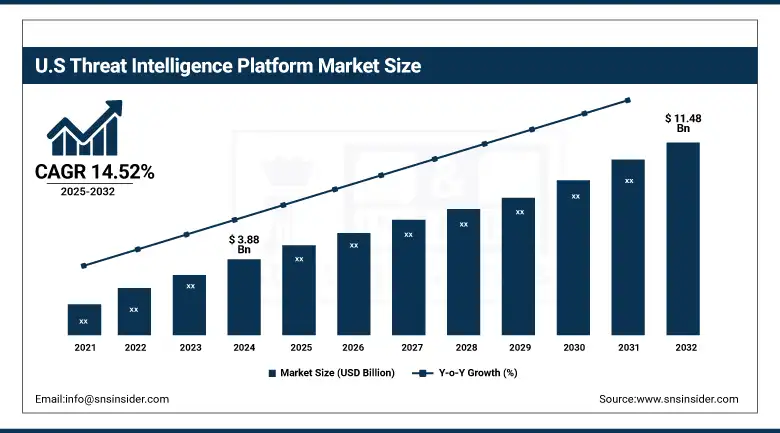

The U.S Threat Intelligence Platform Market size reached USD 3.88 billion in 2024 and is expected to reach USD 11.48 billion in 2032 at a CAGR of 14.52% from 2025 to 2032.

The U.S is the leading country in the Globe Threat Intelligence Platform Market as it has a good cybersecurity infrastructure, high usage of new technologies by the people, and due to heavy investment by organizations in new technologies. Strong Market Penetration and Innovation: Leading cybersecurity vendors such as IBM, Cisco, Palo Alto Networks, and FireEye occupy the market. Factors driving the demand are the increased frequency and complexity of cyberattacks, stringent regulations such as HIPAA and CCPA, and dependence on cloud computing and connected devices. Moreover, attention to national-level cyber defense initiatives by the U.S. government and enterprise demand for real-time threat detection solutions propels market expansion.

Market Dynamics

Drivers:

-

Increasing Frequency and Sophistication of Cyber Threats Drive the Adoption of Advanced Threat Detection Platforms.

Increasing incidents of cyberattacks in BFSI, healthcare, and government, among other sectors, that are rising in terms of occurrence, complexity, and scale, are driving the adoption of threat intelligence. The interconnectedness of cyberattacks is necessitating threat intelligence in place of traditional defense mechanisms. Enterprises are moving from reactionary security models to proactive, intelligence-driven defense plans that protect data and maintain operations. APTs, ransomware, and supply chain attacks are increasing the need for businesses to adopt threat intelligence platforms, enabling them with real-time alerts and predictive analytics. Recent advances have seen the use of AI-based threat analytics and integration with SOAR and SIEM tools for swift response. IBM and Palo Alto Networks have particularly implemented AI capabilities in their security platforms in order to cater to this requirement.

Restraints:

-

High Cost and Complexity of Deployment Limit Adoption Among Small and Medium Enterprises Globally.

Although the demand for cybersecurity is increasing, a large capital outlay to implement a threat intelligence platform is one of the challenges, particularly for SMEs. High implementation complexity, the difficulty of integration with existing legacy systems, and the lack of appropriately trained cybersecurity professionals increase the complexity. Smaller companies often have neither the financial nor the personnel resources necessary to put money into dedicated platforms or managed security services. In addition, the continued cost of operations and maintenance yields a lack of investment. The result is that while the market is controlled by large enterprises, SMEs are left using core or partial security tools, with a major part of the digital ecosystem in vulnerable.

Opportunities:

-

Expanding Cloud and IoT Ecosystems Create Lucrative Growth Prospects for Scalable Security Intelligence Solutions.

Rapid advancements in cloud computing and IoT ecosystems have created a huge opportunity for the threat intelligence platform market. With businesses moving to a combination of hybrid and multi-cloud architectures, the demand for real-time, scalable, and automated threat protection has grown. There's growing interest in platforms featuring API-based integration and flexible deployment options, and the ability to run across environments. Additionally, IoT devices have expanded the attack surface, further emphasizing the demand for contextual threat insights. Recent developments include cloud-native threat detection solutions and extended threat detection and response (XDR) tools that are increasingly being adopted by leading firms like Microsoft, Fortinet, and Cisco.

Challenges:

-

Shortage of Skilled Cybersecurity Professionals Hampers Effective Implementation and Utilization of Threat Intelligence Solutions.

A significant roadblock to the deployment of threat Intelligence platforms is the shortage of cybersecurity experts to operate, make sense of, and act on threat data. As cyber threats continue to change and dependence on AI-based systems increases, security teams need to analyze complex data and make decisions in real time. But a lack of trained workers worldwide means tools are sitting unused and tasks are going undone. The demand for cybersecurity skills greatly outnumbers the supply, delaying the time to resolution of incidents and therefore increasing risk explosure. The talent shortage continues to be a major challenge, particularly for companies with initiatives underway or already in place, for moving to advanced intelligence-driven security models.

Segment Analysis

By Component

The Solution segment leads the market with approximately 63.17% of revenue in 2024 due to growing demand for integrated threat detection, analytics, and automated response capabilities. Vendors like CrowdStrike and Palo Alto Networks have unveiled unified platforms combining threat intel, endpoint security, and SOAR functionality. These solutions enable proactive defense, real-time monitoring, and streamlined incident response. The market favors AI-driven, scalable solutions that centralize intelligence workflows. The dominance of this segment highlights organizations' shift toward comprehensive security architectures that reduce complexity and boost defense effectiveness, key in the continuously evolving threat landscape.

The Services segment is expanding rapidly with a CAGR of 16.14% as managed detection, response, and consulting services gain traction among organizations lacking internal security expertise. Companies such as IBM Security and FireEye offer outsourced SOC-as-a-service, threat intelligence feeds, and incident response retainer packages. These services are enhanced by AI and ML, enabling automated threat analysis and adaptive defense. This trend caters to budget-conscious enterprises seeking flexible, scalable security support, reinforcing services’ role in broadening threat intelligence adoption across various business sizes.

By Deployment

Cloud solutions dominate with 68.83% of revenue in 2024 due to their scalability, rapid deployment, and centralized intelligence sharing. Providers like Microsoft’s Defender Threat Intelligence and Recorded Future offer real-time threat feeds and integration with other cloud-native security tools. These platforms simplify management and lower infrastructure costs. In an era of hybrid work and multi-cloud environments, cloud delivery models are essential for real-time threat visibility, underpinning their market leadership.

On-premises deployments are witnessing faster growth with a projected CAGR of around 16.72%, as organizations in regulated industries demand full control over sensitive data. New secure appliances like Cisco SecureX and Fortinet FortiSIEM are being launched to meet this need. These solutions allow deeper integration with legacy infrastructure and enhanced data sovereignty. As compliance standards tighten, on-premises setups provide a balance of control and performance, driving strong market uptake.

By Enterprise Size

Large Enterprises dominate with about 75.29% of revenue in 2024, facing complex networks and high-stakes cyber risks, and invest heavily in threat intelligence platforms. These organizations deploy enterprise-grade systems supported by vendors like IBM and Splunk, featuring advanced analytics and global threat feeds. Their scale demands comprehensive visibility, making them the primary segment driving market revenues. Additionally, mandatory regulatory requirements compel large enterprises to maintain robust intelligence capabilities.

SMEs are the fastest-growing, with an estimated CAGR of 16.56%, to mitigate cyber risk. Vendors such as Anomali and Recorded Future now offer scalable, subscription-based threat feeds and managed services tailored for smaller budgets. With increasing cyberattacks and regulatory pressure, SMEs benefit from cost-effective, cloud-based threat intelligence solutions, fueling swift adoption and significant segment growth

By Application

Security Information and Event Management (SIEM) leads with approximately 34.29% of revenue in 2024. SIEM-integrated threat intelligence is essential for real-time event correlation and alerting. Platforms like IBM QRadar and Splunk ES now embed contextual threat feeds to enhance detection accuracy and reduce false positives. Recent enhancements include analytics-based alert prioritization and automated patching workflows. This integration reinforces SIEM as the central intelligence hub in comprehensive cybersecurity strategies. A key driver is the regulatory demand for continuous monitoring and incident response.

Business Continuity Planning & Management segment posts fastest CAGR of around 16.57% as it is gaining traction as cyber resilience becomes integral to enterprise security. Vendors such as FireEye, Mandiant, and Palo Alto offer integrated continuity modules with real-time threat visibility for disaster recovery. AI-driven simulation tools stress-test incident response strategies. This threat intelligence platform market trend is driven by the need for uninterrupted operations amid escalating cyber disruption and stricter governance requirements.

By End Use

The BFSI sector leads the market with 32.26% of revenue in 2024, as financial institutions deal with high-value data and strict compliance mandates (e.g., PCI-DSS, SOX). Players like Bank of America and Citi implement platforms from Cisco, Palo Alto, and FireEye, using behavioral analytics, fraud detection, and real-time threat monitoring. Continuous positioning in digital transformation and remote banking further reinforces BFSI dominance.

Healthcare is the fastest-growing segment with a CAGR of around 18.01%, due to rapid digitization (EHRs, telemedicine) and rising ransomware attacks. Solutions geared for healthcare compliance (HIPAA) are now offered, such as Team Cymru’s threat assessment and Cisco Secure Endpoint. This adoption is propelled by increasing API use, third-party risks, and prioritization of patient data protection in a highly regulated environment.

Regional Analysis

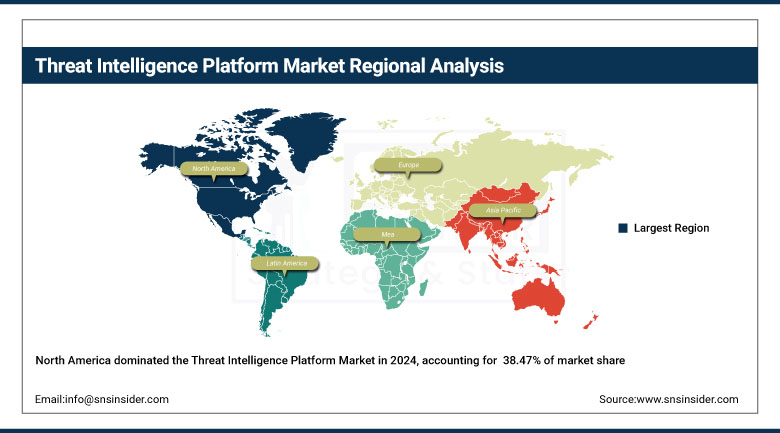

North America dominates with 38.47% of the total revenue, threat intelligence platform market share. This leadership is driven by the presence of major cybersecurity firms, heightened cyber threat levels, advanced technological infrastructure, and strict regulatory frameworks such as HIPAA and CCPA. The market is further propelled by high investment in security R&D and enterprise-level digital transformation across sectors. The United States leads the region due to its early adoption of AI-driven threat intelligence tools, substantial defense and enterprise cybersecurity budgets, and the presence of global market players like IBM, Cisco, and Palo Alto Networks.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is witnessing steady threat intelligence platform market growth due to increased regulatory pressure from GDPR, growing awareness of advanced threats, and higher security spending in sectors like finance, manufacturing, and healthcare. The region's adoption of privacy-first digital policies is encouraging businesses to integrate real-time threat intelligence platforms. Germany dominates the European market due to its strong industrial ecosystem, rising cyber risk exposure in critical infrastructure, and government-backed digital security programs encouraging adoption of threat intelligence platforms.

Asia Pacific is the fastest-growing region, with a projected CAGR of 20.18% during the forecast period. This growth is attributed to rapid digital transformation, a rise in state-sponsored cyberattacks, and growing cybersecurity initiatives by governments in emerging economies. Rising adoption of cloud services and IoT devices is further fueling demand for threat intelligence solutions. China is the regional leader owing to widespread digitization, growing investment in cybersecurity technologies, and national-level strategies to secure critical information infrastructure and combat sophisticated cyber threats.

The Middle East & Africa and Latin America are experiencing gradual growth in the threat intelligence platform market, driven by digital modernization, rising ransomware threats, and expanding online services. The UAE leads MEA with smart city initiatives and cyber resilience efforts, while Brazil dominates Latin America due to its thriving fintech sector and increased cybersecurity investments.

Key Players

The major key players of the Threat Intelligence Platform Market are BAE Systems, Inc., Broadcom (Symantec Corporation), Check Point Software Technologies Ltd., Cisco Systems, Inc., FireEye, Inc., Fortinet, Inc., IBM Corporation, McAfee, LLC, Palo Alto Networks, Inc., Trend Micro Incorporated, and others.

Key Developments

-

In April 2025, IBM announced the release of the X-Force 2025 Threat Intelligence Index, which reported a spike in identity-based attacks and credential compromise, providing more insight into supporting organizations to improve detection and proactive threat capabilities and cybersecurity measures.

-

In April 2025, Palo Alto Networks unveiled its proposed acquisition of Protect AI to enhance its Prisma AIRS platform and combine sophisticated AI-centric security technologies intended to protect the entire AI model and system lifecycle.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 12.57 Billion |

| Market Size by 2032 | USD 40.03 Billion |

| CAGR | CAGR of 15.59% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Solution, Services) •By Deployment (Cloud, On-premise) •By Enterprise Size (Large Enterprises, SMEs) •By Application (Security Information and Event Management, Governance, Risk & Compliance, Business Continuity Planning and Management) •By End-use (BFSI, Government, Healthcare, IT & Telecom, Manufacturing, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BAE Systems, Inc., Broadcom (Symantec Corporation), Check Point Software Technologies Ltd., Cisco Systems, Inc., FireEye, Inc., Fortinet, Inc., IBM Corporation, McAfee, LLC, Palo Alto Networks, Inc., Trend Micro Incorporated. |

Frequently Asked Questions

North America dominated the Threat Intelligence Platform Market in 2024, accounting for 38.47% of total revenue.

The Solution segment, under Component, dominated the market with approximately 63.17% of revenue in 2024.

The major growth factor is the increasing frequency and sophistication of cyber threats across BFSI, healthcare, and government sectors, driving the need for advanced, AI-based threat detection platforms.

The Threat Intelligence Platform Market was valued at USD 12.57 billion in 2024.

The market is expected to grow at a CAGR of 15.59% during the forecast period of 2025–2032.

Get in Touch