Travel Insurance Market Report Scope & Overview:

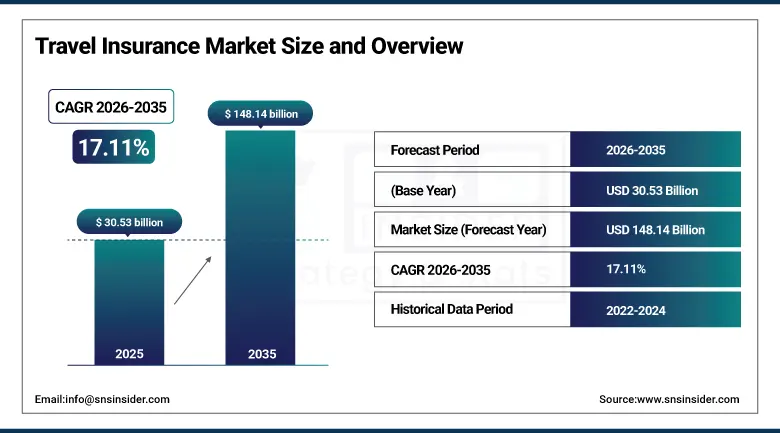

The Travel Insurance Market was valued at USD 30.53 Billion in 2025 and is expected to reach USD 148.14 Billion by 2035, growing at a CAGR of 17.11% from 2026–2035.

The global travel insurance market is experiencing one of its most commercially dynamic periods in history, as the collective memory of pandemic-era trip cancellations, border closures, and emergency medical evacuations has fundamentally and durably shifted the traveller psychology from insurance-optional to insurance-essential across leisure, business, and senior travel segments that were previously characterised by chronically low insurance take-up rates relative to the genuine financial risks that international travel exposes travellers to. The extraordinary pace of global tourism’s post-pandemic recovery, with the UNWTO estimating that international tourist arrivals recovered to approximately 1.3 billion by 2024 and are projected to surpass pre-pandemic peaks through the forecast period, provides both the volume base and the growth trajectory that sustains travel insurance market expansion at rates substantially above those of the broader insurance industry.

Allianz Partners’ 2025 expansion of its Vacation Confidence Index across the USA, Europe, and Asia Pacific to track traveller intent and behaviour trends across major markets represents the most commercially sophisticated consumer insight investment in the travel insurance industry’s recent history, directly informing product innovation, digital channel investment, and pricing strategy decisions whose evidence-based grounding gives Allianz a systematic competitive advantage in the consumer travel insurance segment over rivals whose market intelligence is less rigorously structured.

Market Size and Forecast

-

Market Size in 2026E: USD 35.75 Billion

-

Market Size by 2035: USD 148.14 Billion

-

CAGR: 17.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Travel Insurance Market - Request Free Sample Report

Travel Insurance Market Trends

-

Rising adoption of parametric travel insurance products that trigger automatic payouts upon verifiable events including flight delays exceeding defined durations, airport closures, destination weather events.

-

Growing integration of AI and machine learning across travel insurance operations including automated underwriting that assesses individual risk profiles from travel behaviour and health data, real-time fraud detection.

-

Accelerating adoption of travel insurance through embedded distribution channels including online travel agency booking completion integration, airline seat selection checkout, credit card travel benefit enhancement programmes.

-

Growing consumer awareness and purchasing intention among Generation Z and Millennial travellers whose social media exposure to negative uninsured travel experience content, combined with their digital comfort with comparison and purchase of insurance through app-based platforms.

-

Rising demand for travel insurance products incorporating mental health coverage, adventure sports protection, epidemic and pandemic disruption coverage.

U.S. Travel Insurance Market Outlook

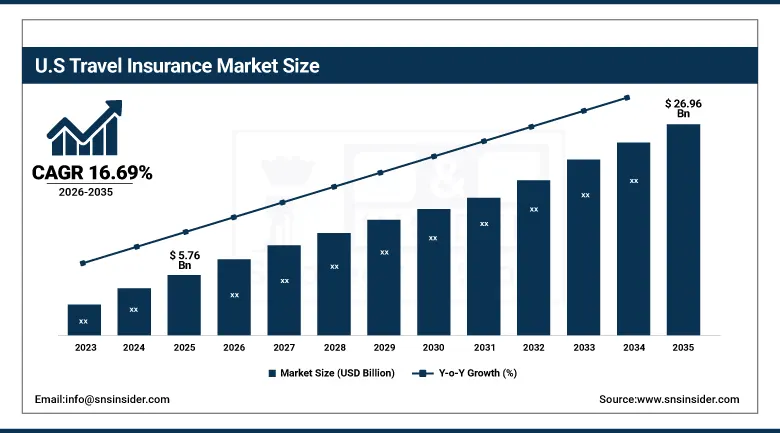

The U.S. Travel Insurance Market was valued at approximately USD 5.76 Billion in 2025 and is expected to reach approximately USD 26.96 Billion by 2035, growing at a CAGR of 16.69%.

The United States travel insurance market is the world’s largest by revenue, sustained by the extraordinary domestic and international travel volume generated by a population of 330 million whose combination of high disposable income, the world’s largest airline network, and a travel culture encompassing leisure, business, and educational travel creates the most commercially valuable and largest-scale travel insurance addressable market in any single country. The U.S. market’s structural growth dynamics are being shaped by the regulatory landscape’s evolution following the COVID-19 period, where consumer protection advocates have successfully pushed for greater policy transparency in cancellation coverage terms, clearer pandemic exclusion disclosure, and simplified claims submission processes that are reducing the consumer frustration that historically limited insurance repeat purchase rates among first-time buyers who experienced difficulty navigating claims processes.

The U.S. Travel Association’s 2025 data confirming that American travellers spent over USD 1.2 trillion on domestic and international travel in 2024, representing a new all-time spending record, defines the protection premium opportunity that travel insurance represents for the industry’s commercial development, as even a modest increase in the proportion of travel expenditure that is covered by comprehensive travel insurance would generate extraordinary premium revenue growth for the carriers positioned to capture that conversion from uninsured to insured travel across the American travel market’s enormous annual expenditure base.

Travel Insurance Market Segment Analysis

-

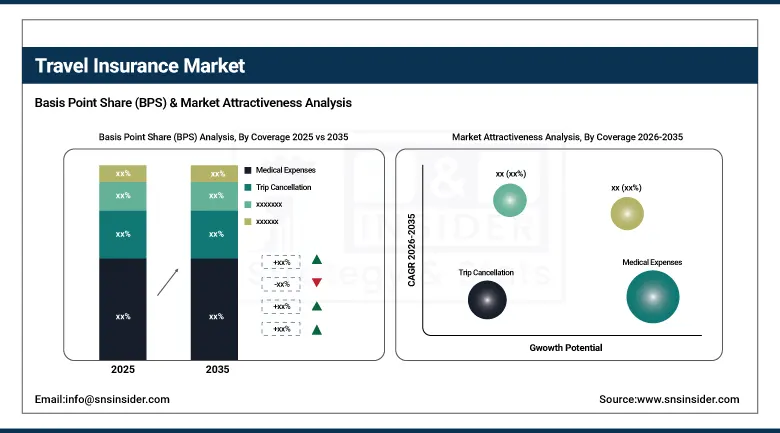

By Coverage, medical expenses dominated with approximately 39% share in 2025 owing to the universal traveller fear of catastrophic foreign medical costs and growing awareness of the financial exposure that uninsured medical emergencies abroad create; trip cancellation is the fastest-growing coverage at a CAGR of approximately 19.37% during 2026–2035 driven by post-pandemic awareness of the financial costs involved when journeys are cancelled or interrupted due to pandemics, natural disasters, and geopolitical events.

-

By Insurance Type, single-trip travel insurance dominated with approximately 59% share in 2025 as the natural choice for travellers making specific planned journeys who assess insurance on a per-trip basis; annual multi-trip travel insurance is the fastest-growing type at a CAGR of approximately 18.17% driven by the growing frequent traveller segment whose cost efficiency advantage of annual coverage over individual trip-by-trip purchase becomes compelling above two to three international trips per year.

-

By Distribution Channel, insurance companies dominated with approximately 30% share in 2025 through their established brand trust, comprehensive product portfolios, and direct consumer relationship infrastructure; banks are the fastest-growing distribution channel at a CAGR of approximately 19.37% driven by the integration of travel insurance within premium banking and credit card products and the growing bank-embedded insurance distribution model.

-

By End User, senior citizens held the largest share of approximately 30% in 2025 given their higher health risk profiles, greater travel frequency, and stronger appreciation of comprehensive medical coverage value; business travellers are the fastest-growing end user at a CAGR of approximately 18.34% driven by corporate travel insurance mandate adoption, the rapid return of international business travel, and growing employer investment in comprehensive travel risk management programmes.

By Coverage, medical expenses dominate, trip cancellation grows fastest

Medical expenses retained the dominant coverage position with approximately 39% of the travel insurance market in 2025, a dominance grounded in the universal and visceral nature of the foreign medical emergency risk that even moderately informed travellers understand as their most potentially catastrophic financial exposure when travelling internationally. The financial consequences of an uninsured serious medical emergency abroad, where hospitalisation costs in the United States alone can exceed USD 10,000 per day and where medical evacuation to the patient’s home country can cost USD 50,000 to USD 300,000 depending on distance and clinical condition, provide a compelling and quantifiable rationale for medical travel insurance that is straightforward to communicate and that creates high coverage motivation across the full demographic spectrum of international travellers. The senior traveller segment’s disproportionate contribution to medical expenses coverage demand reflects both their elevated clinical risk profile and their greater financial sophistication in risk management, as experienced travellers who have either personally experienced or closely witnessed foreign medical emergency events understand the coverage value through concrete experience that provides more powerful purchase motivation than abstract risk communication.

Trip cancellation is the fastest-growing coverage segment at a CAGR of approximately 19.37% through 2035, driven by the pandemic’s dramatic and lasting impact on consumer awareness of the financial losses that trip cancellation creates when uninsured travellers forfeit non-refundable airfare, hotel deposits, tour payments, and cruise fares that aggregate to thousands of dollars per trip and whose loss to a single unexpected cancellation event generates a sharply negative financial and emotional experience that powerfully reinforces subsequent insurance purchase decisions. The structural growth of the trip cancellation segment is further supported by the progressive expansion of ‘cancel for any reason’ policy endorsements that extend coverage beyond the named peril lists of traditional cancellation policies to include the personal, professional, and situational reasons that real-world cancellations most commonly occur for, providing a coverage comprehensiveness that traditional trip cancellation products could not offer and whose higher premium is demonstrably justified by the broader protection scope that travellers find more credible and valuable.

By Insurance Type, single-trip dominates, annual multi-trip grows fastest

Single-trip travel insurance retained the dominant position with approximately 59% of the travel insurance market in 2025, reflecting its natural alignment with the majority of the travelling population who make one to two international journeys per year and for whom the direct and specific connection between a particular trip’s coverage and the premium paid for it makes single-trip insurance the intuitively appropriate and economically rational purchase for their travel frequency level. The single-trip format’s commercial dominance is reinforced by the distribution channel architecture of the travel insurance market, where the majority of policy sales occur at the point of trip booking through airline checkout, online travel agency add-on presentation, and tour operator booking confirmation communication, all of which present single-trip coverage specific to the journey being booked rather than prompting annual policy consideration that requires a more deliberate and long-horizon purchase decision.

Annual multi-trip travel insurance is the fastest-growing type at a CAGR of approximately 18.17% through 2035, propelled by the structural growth of the frequent international traveller segment whose post-pandemic travel intensity has increased substantially as delayed travel ambitions are executed, remote work enables location flexibility that creates more frequent short-trip travel patterns, and the growing senior traveller demographic’s well-funded retirement travel programmes generate two to six international trips per year that make annual policy economics compellingly superior to individual trip purchase at standard single-trip premium rates. World Nomads’ 2024 launch of its Annual Multi-Trip policy across the UK and Ireland through Collinson underwriting, featuring enhanced adventure sports coverage and medical upgrade options, exemplifies the product development investment that leading insurers are directing toward the annual multi-trip format whose growing consumer segment justifies the dedicated product architecture and distribution channel investment required to expand its market penetration beyond the early adopter frequent business traveller segment into the growing leisure frequent traveller market.

By End User, senior citizens dominate, business travellers grow fastest

Senior citizens retained the dominant end user position with approximately 30% of the travel insurance market in 2025, reflecting the demographic segment’s combination of the highest travel frequency, the longest average trip duration, the highest per-trip expenditure, and the greatest medical coverage requirement of any traveller demographic whose multiple chronic health conditions, greater age-associated clinical risk, and higher probability of requiring emergency medical care during travel create both the strongest coverage motivation and the highest per-policy premium generation. The senior travel market’s insurance penetration rate substantially exceeds that of younger traveller demographics, reflecting both the demographic’s higher risk awareness and financial literacy, whose members have had more life experience with unexpected medical costs and insurance value, and the marketing focus that travel insurance providers direct toward this high-value segment whose customer lifetime value and average premium levels make them the most commercially attractive individual purchaser segment in the market.

Business travellers are the fastest-growing end user at a CAGR of approximately 18.34% through 2035, driven by the corporate travel insurance mandate adoption that is progressively making comprehensive travel insurance a standard risk management requirement for employee international travel rather than an optional personal purchase decision. The growth of the business traveller segment reflects multiple converging forces: the rapid recovery and growth of international business travel following COVID-19 pandemic suppression; the growing corporate recognition of duty of care obligations to travelling employees whose medical, security, and evacuation assistance requirements during travel incidents create employer financial and reputational exposure; and the expansion of bleisure travel combining business and leisure components that creates insurance needs spanning both corporate and personal coverage domains.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

21.8% |

|

Asia Pacific |

China |

52.8% |

|

Middle East & Africa |

UAE |

26.7% |

|

Latin America |

Brazil |

38.5% |

North America Travel Insurance Market Insights

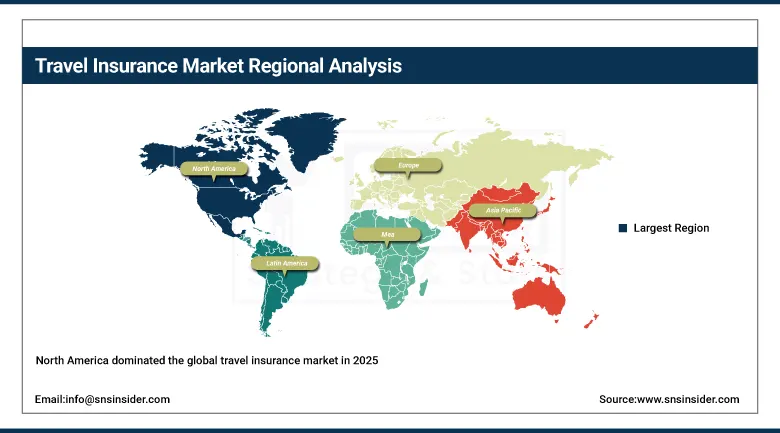

North America dominated the global travel insurance market in 2025 with the United States accounting for approximately 83.4% of North American revenues and representing the world’s single largest national travel insurance market, driven by the country’s extraordinary combination of the highest per-capita international travel expenditure, the most commercially sophisticated travel insurance distribution infrastructure, and the growing consumer awareness of uninsured travel financial risk that post-pandemic experience has embedded across the American travelling population. The U.S. market’s commercial strength is reinforced by the travel insurance industry’s integration into the world’s most developed online travel agency ecosystem, where Expedia, Booking.com, and airline direct booking platforms all present travel insurance at checkout with increasing sophistication in how risk-relevant information is communicated to drive conversion beyond the historically low click-through rates that generic insurance presentation generated. Canada contributes approximately 16.6% of North American travel insurance revenues through a market whose universal healthcare system creates different medical coverage motivation than the U.S. market, but whose large international travel volume and strong adventure travel culture sustain meaningful insurance demand, particularly in the trip cancellation, baggage, and travel delay coverage categories.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Travel Insurance Market Insights

Europe is the world’s second-largest travel insurance market whose commercial characteristics reflect the continent’s distinctive travel patterns, including extraordinary intra-European travel volumes enabled by the Schengen Area’s open borders, the strong cultural tradition of long-haul holiday travel to long-distance destinations, and the mandatory travel insurance requirements that some European countries impose on visitors through visa application processes that create regulatory compliance-driven demand alongside the consumer choice-based purchasing that characterises the North American market. Germany accounts for approximately 21.8% of European travel insurance revenues as the region’s largest national market, reflecting the German population’s high international travel frequency, above-average risk awareness and insurance purchasing discipline that characterise German consumer financial behaviour broadly, and the strong domestic travel insurance distribution infrastructure of Germany’s major insurers including Allianz, ERGO, and Generali whose travel insurance divisions serve both direct consumer and travel agent distribution channels.

Asia Pacific Travel Insurance Market Insights

Asia Pacific is the fastest-growing regional travel insurance market at a CAGR substantially above the global average, driven by the extraordinary pace of international travel growth from China, India, South Korea, Japan, and Southeast Asia whose growing affluent middle-class populations are dramatically increasing their international travel frequency as rising disposable incomes make international destinations increasingly accessible, with the growing recognition among Asian travellers of travel insurance value following regional epidemic and natural disaster events whose uninsured financial consequences became widely discussed in media and social channels. China accounts for approximately 52.8% of Asia Pacific travel insurance revenues through the sheer scale of outbound Chinese tourism, which the China Tourism Academy estimated reached approximately 130 million international departures in 2024, generating a travel insurance demand base whose growth trajectory is among the steepest of any national market globally as Chinese travellers’ insurance awareness and willingness to pay for comprehensive coverage improve alongside their international travel experience accumulation.

MEA & Latin America Travel Insurance Market Insights

The Middle East and Africa and Latin America are growing travel insurance markets where rising international travel volume from rapidly expanding middle-class populations, growing destination countries’ mandating of travel insurance for visitor visa issuance, and the increasing availability of affordable digital travel insurance products through mobile-first platforms that serve the smartphone-heavy consumer populations of both regions are creating expanding insurance penetration across previously underserved traveller demographics. UAE leads Middle East and Africa travel insurance revenues at approximately 26.7% of the regional total through its position as both a major travel hub generating substantial outbound tourism and a major tourist destination attracting millions of international visitors annually, with Dubai’s reputation as a premium travel destination attracting the affluent international traveller segment whose comprehensive travel insurance purchasing propensity exceeds average traveller segments. Brazil leads Latin American travel insurance revenues at approximately 38.5% of the regional total through its combination of a large domestic population with growing international travel ambitions, the regulatory environment that makes travel insurance advisory a standard component of travel agency service in Brazil, and the growing middle class whose first international travel experiences create natural demand for the comprehensive coverage that unfamiliarity with foreign healthcare and claims processes motivates.

Market Dynamics

Growth Drivers: Post-pandemic risk awareness permanently elevating travel insurance purchase motivation, global tourism recovery and growth expanding the insurable travel volume base, and digital platform distribution reducing purchase friction to drive conversion

The primary structural growth drivers for the travel insurance market are the durable shift in consumer risk perception that the pandemic period created, transforming travel insurance from a generally understood but frequently deferred product into one whose purchase is increasingly perceived as a fundamental component of responsible travel planning whose omission feels reckless rather than merely unnecessary. The UNWTO’s projection of international tourist arrivals reaching 1.8 billion by 2030 provides the volume foundation whose continued growth sustains travel insurance revenue expansion as the insurance-eligible travel base expands proportionally. Digital platform integration’s impact on purchase friction reduction is commercially significant: when travel insurance is presented at the moment of booking completion with clear, comparative product description and one-click purchase capability, conversion rates are measurably higher than when insurance purchase requires a separate browsing, comparison, and purchase journey that the majority of consumers defer and never complete.

Restraints: Complex policy exclusions reducing consumer confidence, claims dispute frequency undermining brand trust, and mandatory insurance requirements in some destination visa processes limiting premium pricing power for compliance-motivated purchases

A significant restraint on the travel insurance market is the persistent consumer distrust that complex and legalistic policy exclusion language creates, particularly in the post-pandemic period where the application of epidemic exclusion clauses to COVID-19-related claims generated widespread consumer frustration and media coverage that damaged travel insurance brand perceptions across markets whose customers had purchased policies with reasonable expectations of pandemic disruption coverage that insurers legitimately but unsympathetically denied on technical grounds whose consumer comprehension had never been adequately established at point of sale.

Opportunities: Embedded insurance in travel booking platforms, climate disruption insurance for weather-related cancellations, and parametric insurance products providing instant automated claims payment

Embedded insurance through travel booking platform integration represents the most commercially significant distribution opportunity in the travel insurance market, as the progressive improvement of checkout insurance presentation from basic add-on widget to personalised risk-relevant offer that communicates the specific financial exposure of the journey being booked is demonstrating measurable conversion improvement that every major online travel agency and airline is investing in as a revenue enhancement alongside the consumer protection improvement it represents. Climate change’s growing impact on travel disruption frequency, where extreme weather events including floods, wildfires, hurricanes, and extreme heat are increasingly cancelling and disrupting travel itineraries, is creating growing consumer demand for specialised climate disruption travel insurance products whose coverage specifically addresses the weather-related cancellation and disruption risks that standard trip cancellation policies exclude through weather exclusion clauses.

Recent Developments:

-

2025: Allianz Partners expanded its Vacation Confidence Index across the USA, Europe, and Asia Pacific in 2025, tracking traveller intent and behaviour trends across major markets to shape strategic product innovation and customer engagement programme development, representing the most comprehensive consumer insight investment in the travel insurance industry and directly informing Allianz’s product development and digital channel investment priorities.

-

2024: Allianz Partners announced a long-term extension of its partnership with Iberia in 2024, continuing as the airline’s global travel insurance provider across 13 markets and reinforcing the growing strategic importance of airline-integrated insurance distribution as a key channel for seamless policy access during flight bookings.

-

2024: World Nomads launched its Annual Multi-Trip policy across the UK and Ireland through Collinson underwriting in 2024, featuring enhanced adventure sports coverage and medical upgrade options, addressing the growing frequent traveller market’s demand for comprehensive annual coverage that provides cost efficiency and broad protection across multiple international journeys.

-

2025: Seven Corners expanded its digital platform capabilities with enhanced mobile claim submission, real-time claim status tracking, and AI-powered documentation assistance that reduces average claims processing time by enabling faster and more complete initial submission from travellers in-destination who can access assistance immediately through smartphone interface rather than waiting to return home.

-

2025: AXA Travel Insurance launched an enhanced parametric travel delay product across European markets that automatically triggers compensation payments to policyholders when flight delay data from airport systems exceeds coverage thresholds without requiring claim form submission, demonstrating the commercial feasibility of the instant-payout parametric model that consumer research consistently identifies as the travel insurance product innovation with the highest purchase intent improvement potential.

Travel Insurance Market Key Players

-

Allianz Partners (Allianz SE)

-

AXA SA

-

Generali Group

-

Zurich Insurance Group AG

-

American International Group Inc. (AIG)

-

American Express Company

-

Berkshire Hathaway Specialty Insurance

-

Seven Corners Inc.

-

Travel Insured International (Crum & Forster)

-

World Nomads Group (Collinson)

-

USI Affinity (USI Insurance Services)

-

Battleface

-

Insure & Go Insurance Services (Mapfre)

-

Ping An Insurance (Group) Company of China

-

Tokio Marine Holdings Inc.

-

Assurant Inc.

-

Staysure Group

-

Arch Capital Group Ltd.

-

ERGO Group AG (Munich Re)

-

Tin Leg (Squaremouth)

Travel Insurance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.53 Billion |

| Market Size by 2035 | USD 148.14 Billion |

| CAGR | CAGR of 17.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Coverage (Medical Expenses, Trip Cancellation, Baggage & Personal Belongings, Travel Delay, Others) • By Insurance Type (Single-Trip Travel Insurance, Annual Multi-Trip Travel Insurance) • By Distribution Channel (Insurance Companies, Banks, Insurance Brokers, Insurance Aggregators, Others) • By End User (Senior Citizens, Education Travelers, Business Travelers, Family Travelers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Allianz Partners (Allianz SE), AXA SA, Generali Group, Zurich Insurance Group AG, American International Group Inc. (AIG), American Express Company, Berkshire Hathaway Specialty Insurance, Seven Corners Inc., Travel Insured International (Crum & Forster), World Nomads Group (Collinson), USI Affinity (USI Insurance Services), Battleface, Insure & Go Insurance Services (Mapfre), Ping An Insurance (Group) Company of China, Tokio Marine Holdings Inc., Assurant Inc., Staysure Group, Arch Capital Group Ltd., ERGO Group AG (Munich Re), Tin Leg (Squaremouth) |

Frequently Asked Questions

The Travel Insurance Market is expected to grow at a CAGR of 17.11% from 2026 to 2035.

The Travel Insurance Market was valued at USD 30.53 Billion in 2025.

Ans: The major growth factor is rising global travel demand with increasing awareness about medical protection, trip cancellations, and financial security against travel disruptions.

Medical Expenses dominated with approximately 39% of revenues in 2025.

North America dominated the Travel Insurance Market in 2025, with the United States accounting for approximately 83.4% of North American revenues.

Get in Touch