Hyper Converged HCI Solutions Market Report Scope & Overview:

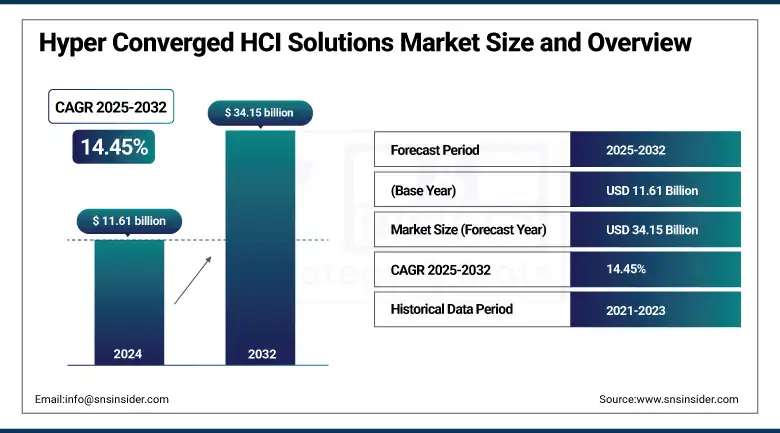

The Hyper Converged HCI Solutions Market size was valued at USD 11.61 billion in 2024 and is expected to reach USD 34.15 billion by 2032, expanding at a CAGR of 14.45% over the forecast period of 2025-2032.

The Hyper-Converged Infrastructure (HCI) Solutions Market is rapidly expanding as organizations seek streamlined, scalable, and cost-effective IT infrastructure. By integrating compute, storage, and networking into a unified, software-defined platform, HCI simplifies operations and enhances performance across data centers and edge environments. The increasing adoption of hybrid cloud, virtualization requirements, and digital transformation initiatives is driving the market. Businesses are using HCI for cost-effective backup and disaster recovery, workload consolidation, and agility. New capabilities such as support for Kubernetes and AI-guided automation are also driving adoption. North America is the dominating region in the market, whereas Asia Pacific is expected to be emerging as the fastest-growing region due to growing cloud and data center spending.

To Get more information On Hyper Converged HCI Solutions Market - Request Free Sample Report

According to research, as of 2024, over 58% of enterprises globally have implemented or are piloting HCI solutions, with many reporting up to a 40% reduction in infrastructure costs due to streamlined management and reduced hardware expenditures.

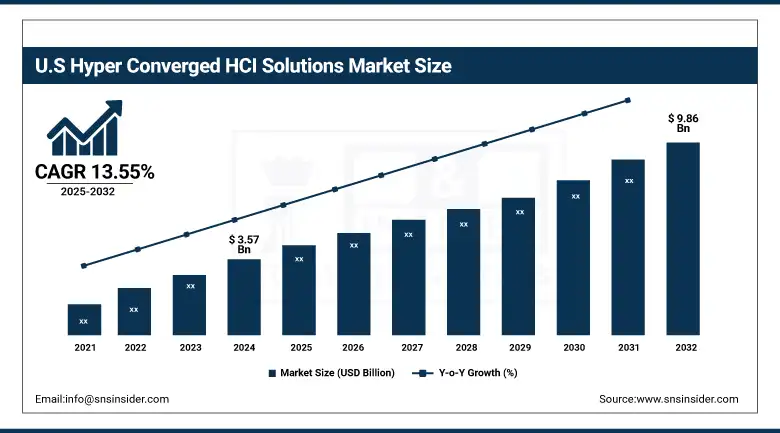

The U.S Hyper Converged HCI Solutions Market size reached USD 3.57 billion in 2024 and is expected to reach USD 9.86 billion in 2032 at a CAGR of 13.55% from 2025 to 2032.

The US hyper-converged infrastructure (HCI) solutions market is the most significant market due to the early and high adoption of the virtualization technology in the US, hybrid cloud strategies, and software-defined infrastructure. American enterprises are spending significantly on digital transformation, edge computing, and refreshing legacy systems, as major factors that fuel the adoption of HCI. The existence of big market players like Dell Technologies, VMware, Cisco, and Nutanix helps speed up product innovations, customer onboarding, and market penetration. Strong enterprise needs for easy-to-manage IT, solid disaster recovery, and scalable infrastructure also drive growth.

Market Dynamics:

Drivers:

-

Rising Enterprise Shift Toward Simplified and Scalable Infrastructure Accelerates Technology Deployment Globally.

Enterprises are increasingly shifting toward simplified, software-defined infrastructure to eliminate legacy complexities and reduce operating costs. HCI consolidates calculation, storage, and networking control into a single tool set, simplifying scale and operational agility. This represents an increasing interest in hybrid cloud support, edge deployments, and virtual desktop infrastructure (VDI). The recent announcements, such as VMware’s vSAN Max and Nutanix GPT integration, show some performance and automated enhancements. Enterprises are now adopting HCI for a variety of goals, such as ultra-fast disaster recovery, consolidated workloads, and AI readiness, such that it is becoming a standard for digital transformation and next-generation data center strategies.

Restraints:

-

Lack of Skilled IT Professionals and High Initial Deployment Costs Hamper Rapid Market Adoption Across SMEs.

Despite increasing demand, many small and medium enterprises (SMEs) struggle with the high upfront costs and lack of skilled personnel required to deploy and manage HCI environments effectively. Advanced HCI solutions demand expertise in virtualization, hybrid cloud orchestration, and software-defined storage resources often unavailable to smaller IT teams. This complexity acts as a barrier, particularly in developing economies. While vendors are launching simplified or managed HCI offerings, cost concerns and resource constraints still limit adoption among cost-sensitive customers.

Opportunities:

-

Growing Edge Computing and 5G Deployment Open New Use Cases for Hyper-Converged Infrastructure Platforms.

The proliferation of edge computing and 5G networks is opening new opportunities for hyper-converged infrastructure to support latency-sensitive and distributed workloads. As enterprises deploy applications closer to the data source, compact and scalable HCI nodes are ideal for edge sites due to their modular design and simplified management. Vendors like HPE and Scale Computing have launched edge-optimized HCI solutions integrated with AI/ML capabilities and real-time analytics support. The demand for autonomous systems, smart cities, and IoT-driven services further enhances this growth trajectory, making edge HCI an emerging frontier for service innovation and infrastructure decentralization.

Challenges:

-

Complex Integration with Legacy Systems and Existing Infrastructure Creates Operational and Compatibility Challenges.

Integrating HCI solutions with legacy infrastructure remains a major challenge for enterprises undergoing digital transformation. Many organizations operate with outdated systems and fragmented IT environments, making it difficult to unify operations under a single HCI architecture. Compatibility issues with older storage arrays, networking protocols, and application stacks often require costly customization or migration. These technical limitations can delay deployments and lead to suboptimal performance. Vendors focus on API integration, yet aligning with legacy systems remains a challenge, limiting seamless scalability and ROI potential.

Segment Analysis:

By Component

The hardware segment dominated the market with a 62.27% share of revenue in 2024, driven by demand for integrated appliances that bundle compute, storage, and networking into a single chassis. Major players like Dell Technologies (VxRail) and Cisco (HyperFlex) are continuously launching performance-optimized hardware platforms for hybrid cloud and edge deployments. Rising investments in private data centers and latency-sensitive applications are fueling the preference for appliance-based HCI systems.

The software segment is projected to grow at the highest CAGR of 15.25%, propelled by the shift toward software-defined infrastructure. Vendors like Nutanix (AOS) and VMware (vSAN) are enabling flexible, hardware-agnostic HCI platforms that support hybrid and multi-cloud strategies. The rapid rise of containerized applications, the need for lifecycle automation, and the increasing demand for platform-agnostic scalability are accelerating software adoption. This trend makes the software component essential for future-ready, agile enterprise IT environments.

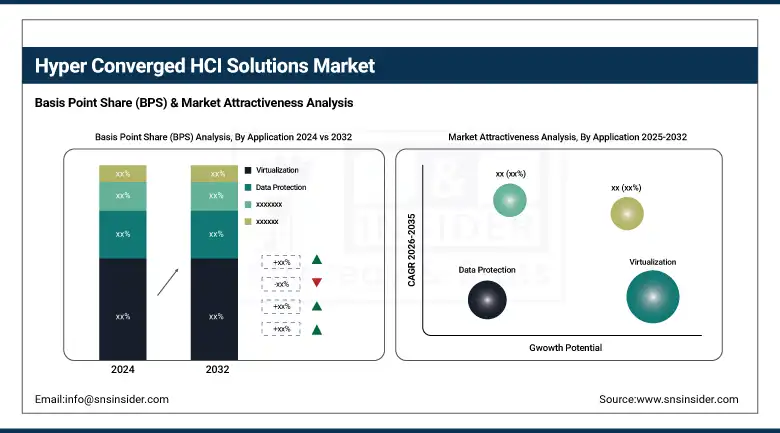

By Application

The virtualization segment accounted for the largest revenue share at 31.30% in 2024, owing to high demand for server consolidation, VDI, and application mobility. Companies like Nutanix and VMware have optimized their platforms for virtual workload management, streamlining provisioning and performance. The rise in remote work and hybrid workforce models has further strengthened the use of virtualization in HCI as a core use case, delivering cost efficiency and operational agility.

The data protection segment is expected to register the highest CAGR of 15.67% through 2032. Growing concerns about ransomware, compliance (e.g., GDPR, HIPAA), and disaster recovery are boosting demand for built-in backup and replication features. Firms like Cohesity and Veeam are enhancing data protection as-a-service, integrated into HCI stacks for seamless, end-to-end coverage.

By Enterprise Size

Large enterprises dominated the market with a 65.38% revenue share in 2024, attributed to their scale, complex workloads, and need for centralized governance across distributed IT environments. Solutions like Cisco HyperFlex and VMware Cloud Foundation are tailored for enterprise deployments, providing high performance, compliance, and scalability. With digital transformation accelerating, large enterprises remain the primary adopters of HCI for modernizing core infrastructure.

SMEs are expected to grow at the fastest CAGR of 15.12% over the forecast period, as vendors deliver cost-effective and easy-to-manage HCI solutions tailored to small business needs. Companies like Scale Computing and StarWind offer subscription-based platforms with reduced operational complexity. HCI’s plug-and-play deployment, lower total cost of ownership, and cloud compatibility are attracting a growing base of SME adopters.

By End Use

The BFSI segment led the market with a 24.58% revenue share in 2024, driven by stringent compliance mandates and the need for high-availability infrastructure. Institutions are deploying HCI to support real-time analytics, fraud detection, and secure transactions. Vendors like Nutanix and Fortinet are offering specialized financial-grade HCI platforms with layered security and robust data governance, enabling continuous operations in banking and insurance environments.

The healthcare segment is projected to grow at the fastest CAGR of 16.33% during 2025–2032, supported by growing telemedicine, EMR/EHR systems, and diagnostic imaging workloads. HCI helps hospitals meet HIPAA compliance, protect sensitive patient data, and streamline performance across clinical systems. Solutions like HPE SimpliVity are designed for healthcare environments with built-in backup and rapid disaster recovery, driving adoption in hospitals and medical research facilities.

Regional Analysis

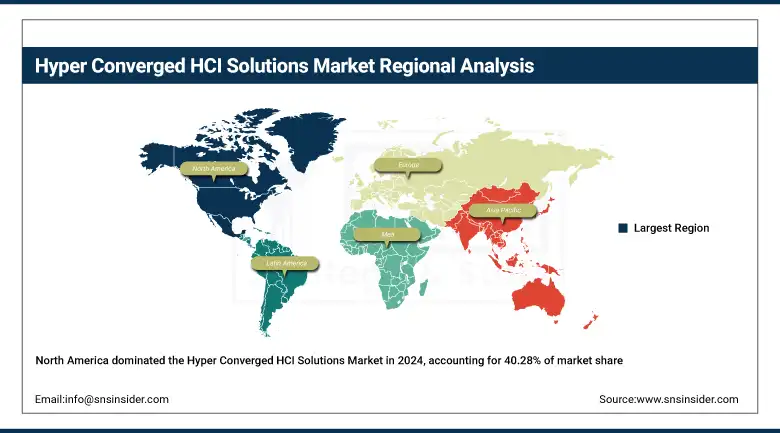

North America held the largest share of the Hyper-Converged HCI Solutions Market in 2024, accounting for 40.28% of global revenue. This dominance is attributed to the early adoption of virtualization technologies, the strong presence of key players like VMware, Nutanix, and Cisco, and widespread cloud migration. Additionally, enterprise focus on IT modernization and data center consolidation continues to fuel HCI adoption across industries. The United States is the dominant country in this region due to its mature IT infrastructure, large-scale enterprise demand, and continuous investments in hyper-converged and hybrid cloud technologies from market leaders like Dell EMC and HPE.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe represents a substantial portion of the market, driven by digital transformation efforts across banking, healthcare, and manufacturing sectors. The rise of data localization regulations such as GDPR and the growing emphasis on secure, scalable, and cost-efficient infrastructure have accelerated HCI deployment across mid-sized and large enterprises in the region. Germany dominates the European market due to its strong industrial base, investment in smart manufacturing, and leadership in Industry 4.0 initiatives, all of which demand robust, virtualized infrastructure.

Asia Pacific is the fastest-growing region in the market, with a share of 22.28% in 2024 and an accelerating CAGR. Rapid digitalization, increasing SME cloud adoption, and government-backed smart infrastructure projects are fueling market growth. Enterprises are leveraging HCI for scalable, secure deployments in sectors like finance, education, and e-commerce. China leads the region with aggressive investments in cloud infrastructure, edge computing, and smart city deployments. Its digital economy and initiatives like “New Infrastructure” heavily support hyper-converged technology adoption.

The Middle East & Africa and Latin America are experiencing steady growth in HCI adoption, fueled by data center modernization, cloud initiatives, and rising demand for scalable, cost-efficient infrastructure across banking, telecom, and public sectors. The UAE leads in MEA due to cloud-first strategies, while Brazil dominates Latin America through strong digital transformation and enterprise-driven deployments.

Key Players

The major key players of the Hyper Converged HCI Solutions Market are Nutanix, Inc., Dell EMC, Cisco Systems, Inc., Hewlett-Packard Enterprise (HPE), Microsoft Corporation, Huawei Technologies Co., Ltd., NetApp, Inc., IBM Corporation, Scale Computing, StarWind Software, Inc., and others.

Key Developments

-

In May 2025, Dell Technologies introduced next-gen VxRail HCI appliances featuring Intel Xeon Scalable processors and integrated VMware vSAN ESA, designed to enhance performance and scalability across edge and data center deployments.

-

In April 2025, Nutanix launched Cloud Native AOS, offering enterprise-grade storage and data services for Kubernetes environments. The update adds support for Dell PowerFlex and Pure Storage FlashArray, enhancing AI integration and flexibility for mission-critical workloads.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 11.61 Billion |

| Market Size by 2032 | USD 34.15 Billion |

| CAGR | CAGR of 14.45% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Hardware, Software, Services) •By Application (Virtualization, Data Protection, Cloud Computing, Remote Office/Branch Office, Others) •By Enterprise Size (Small and Medium Enterprises, Large Enterprises) •By End-User (BFSI, Healthcare, IT and Telecommunications, Government, Education, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Nutanix, Inc., Dell EMC, Cisco Systems, Inc., Hewlett-Packard Enterprise (HPE), Microsoft Corporation, Huawei Technologies Co., Ltd., NetApp, Inc., IBM Corporation, Scale Computing, StarWind Software, Inc. |

Frequently Asked Questions

The market is projected to grow at a CAGR of 14.45% from 2025 to 2032.

The Hyper Converged HCI Solutions Market size was valued at USD 11.61 billion in 2024.

The major growth driver is the rising enterprise shift toward simplified, scalable, software-defined infrastructure, which helps reduce legacy system complexity and operational costs while enabling hybrid cloud and edge computing capabilities.

By Component, the Hardware segment dominated the market with a 62.27% revenue share in 2024, driven by demand for integrated compute-storage-networking appliances, especially for private and hybrid cloud deployments.

North America dominated the Hyper Converged HCI Solutions Market in 2024, accounting for 40.28% of global revenue. This leadership is driven by early virtualization adoption, a mature IT ecosystem, and the presence of leading HCI vendors such as VMware, Cisco, and Dell EMC.

Get in Touch