Ultralight and Light Aircraft Market Key Insights:

To Get More Information on Ultralight and Light Aircraft Market - Request Sample Report

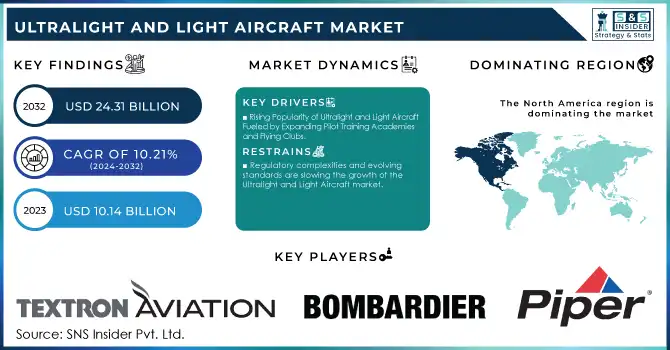

The Ultralight and Light Aircraft Market Size was valued at USD 10.14 billion in 2023 and is expected to reach USD 24.31 billion by 2032 with an emerging CAGR of 10.21% over the forecast period 2024-2032.

The Ultralight and Light Aircraft Market is experiencing rapid growth, driven by the rise of Urban Air Mobility (UAM) and electric vertical takeoff and landing (eVTOL) aircraft technologies. Companies like Lift Aircraft, led by Matt Chasen, are at the forefront of this shift, developing electric-powered ultralight aircraft that can be operated by virtually anyone, including tourists. Lift's Hexa eVTOL aircraft, a one-seater weighing 430 pounds with 18 propellers, qualifies as a "powered ultralight" under FAA rules, allowing non-pilots to operate the craft for short, scenic flights in less congested areas.

The aviation industry has long been a significant contributor to global CO2 emissions, accounting for nearly 2% of total global emissions. The adoption of electric aircraft is set to revolutionize the sector by offering more environmentally friendly transportation. Battery-powered aircraft systems are up to 95% more efficient than traditional jet engines, especially during taxiing, waiting, or taking off, contributing to significant cost savings and reduced maintenance costs. This aligns with the broader trend of green aviation solutions and is expected to contribute to the growing adoption of eVTOLs and ultralight aircraft.

The demand for these aircraft is supported by existing regional airport infrastructure, which can be leveraged to support Regional Air Mobility (RAM) and UAM without the need for massive new investments. In Europe, 50% of people live within a 30-minute drive of regional airports, while in the USA, 90% of people have access to a regional airport within the same timeframe. These airports are ideal locations for short-distance air travel powered by electric aircraft. With the rise of electric-powered ultralight aircraft, green propulsion technologies, and significant reductions in operating costs (estimated at 10-15% compared to traditional aircraft), the Ultralight and Light Aircraft Market is poised for substantial growth in the coming years, particularly in recreational, tourism, and urban air mobility sectors.

Market Dynamics

Drivers

- Rising Popularity of Ultralight and Light Aircraft Fueled by Expanding Pilot Training Academies and Flying Clubs

As aviation, enthusiasts and prospective pilots turn to ultralight aircraft for training, this demand continues to surge. Ultralight aircraft are particularly popular in pilot training programs, as they require less complex certification and are easier to manage than traditional aircraft, making them an ideal choice for newcomers to aviation. According to the EAA, ultralights provide a more accessible entry point into flying with a simpler set of rules under the FAA's ultralight guidelines, eliminating the need for a pilot’s license for some models, which further encourages growth in the sector. Organizations like the EAA (Experimental Aircraft Association) are actively promoting the benefits of ultralight aircraft through educational programs and guides for aspiring pilots. These aircraft are also featured in numerous flying clubs and training facilities due to their relatively low training costs and affordability. For example, ultralight pilot training is more accessible, with training times often averaging 10-20 hours, and costs for ultralight pilot training can range from USD 1,500 to USD 3,000, which is significantly lower compared to traditional aircraft training. The growing number of flying clubs and training academies worldwide is driving the demand for ultralight aircraft. In particular, the AOPA (Aircraft Owners and Pilots Association) reports that there are many clubs offering affordable memberships and aircraft access, which support both recreational and pilot training activities. The rise in ultralight aircraft adoption for training and recreation is further supported by organizations like Sport Aviation Center, highlighting the increasing number of enthusiasts entering the world of aviation. This trend is expected to continue, fueling market growth in the Ultralight and Light Aircraft Market, supported by a steady influx of new pilots and aviation enthusiasts seeking affordable, accessible, and efficient flying experiences.

Restraints

- Regulatory complexities and evolving standards are slowing the growth of the Ultralight and Light Aircraft market.

With varying regulations across regions, manufacturers and operators face substantial challenges in compliance with authorities like the FAA (Federal Aviation Administration) in the U.S. and EASA (European Union Aviation Safety Agency) in Europe. This includes requirements for aircraft certifications, safety standards, and operational regulations that vary by country and aircraft type. In particular, ultralight aircraft are subject to a range of regulatory requirements that can hinder their widespread adoption. For instance, the FAA in the U.S. has set specific weight, speed, and operational restrictions for Light Sport Aircraft (LSA) and ultralight aircraft. These aircraft cannot exceed certain maximum weights or exceed maximum speeds, which restricts their capabilities. Additionally, the pilot must adhere to stringent licensing and medical certification rules, which differ significantly from commercial aircraft pilots. This makes it difficult for non-professional pilots to enter the market without significant time and financial investment in training and certification. According to Skybrary, ultralight aircraft are subject to much less stringent regulations in some countries, but in others, they are treated similarly to light aircraft requiring full certification.

Global regulatory inconsistencies further complicate the situation for manufacturers and operators. For example, while some countries may offer more relaxed rules for ultralights, regions like Europe require stricter oversight for both ultralight and light aircraft, making it harder for new manufacturers to enter the market. As stated in Aeroplane Tech, international manufacturers must navigate the complex matrix of these regulations, which can be a costly and time-consuming process. Furthermore, the rise of eVTOL (electric vertical takeoff and landing) aircraft has added a new layer of complexity to the regulatory landscape, with agencies scrambling to develop guidelines and safety standards. Given the regulatory complexity and the need to comply with different aviation authorities, the market faces delays in product development, high certification costs, and limited operational freedom. These challenges can ultimately slow the growth of the Ultralight and Light Aircraft market while increasing the operational hurdles for existing and prospective aircraft operators.

Segment Analysis

By Platform

In 2023, the Light Aircraft segment captured the largest market share of around 73% in the Ultralight and Light Aircraft market. This growth is driven by the rising demand for small, efficient aircraft that offer lower operational costs, fuel efficiency, and ease of maintenance compared to traditional aircraft. Light aircraft are increasingly used in pilot training, flying clubs, and recreational flying due to their user-friendly controls and affordability. Additionally, their applications in sectors like agriculture, aerial photography, and tourism contribute to their market dominance. Technological advancements, such as electric propulsion and innovations in materials, further enhance their appeal. Light aircraft also benefit from less stringent regulatory requirements, making them attractive to both private and commercial operators. This combination of factors solidifies the segment’s leading position in the market.

By Operation

In 2023, the CTOL (Conventional Take-Off and Landing) segment captured the largest revenue share of approximately 49% in the Ultralight and Light Aircraft market. CTOL aircraft are favored for their versatility, ease of operation, and ability to take off and land on short, unprepared runways, making them ideal for both recreational and commercial use. Their popularity in pilot training, flying clubs, and leisure aviation contributes significantly to their market share. Additionally, the widespread adoption of CTOL aircraft in agricultural, survey, and tourism applications boost their demand. The relatively lower acquisition and operational costs, combined with fewer regulatory hurdles compared to other aircraft types, further support the CTOL segment’s market leadership.

Regional Analysis

North America accounted for the largest share of around 40% of the Ultralight and Light Aircraft market in 2023, with the United States being the key driver. The U.S. has a well-established aviation industry, with numerous pilot training academies and flying clubs that prefer light aircraft due to their ease of operation and lower maintenance costs. Regulatory support from the FAA and a large recreational flying community further boost market growth. Canada also plays a significant role, with growing demand for ultralight aircraft, particularly in recreational flying. Both countries benefit from a developed aviation infrastructure, making them favorable markets for light aircraft. As a result, North America's combination of strong demand, regulatory frameworks, and established industry infrastructure allows it to dominate the global market.

Asia-Pacific is the fastest-growing region in the Ultralight and Light Aircraft market, projected to experience rapid growth over the forecast period from 2024 to 2032. Key countries such as China, India, Japan, and Australia are driving this expansion. China and India are witnessing significant increases in general aviation activities, fueled by rising disposable incomes, growing tourism, and an increasing number of pilot training academies. Japan and Australia have well-established aviation industries, with a growing preference for light aircraft in both recreational and training sectors. Additionally, supportive government policies and infrastructure development in these countries are helping boost the market. With a young population, a rising middle class, and increased interest in aviation, Asia-Pacific is set to outpace other regions, becoming a major player in the ultralight and light aircraft market in the coming years.

Do You Need any Customization Research on Ultralight and Light Aircraft Market - Inquire Now

Key Players

Some of the major players in Ultralight and Light Aircraft Market with Products:

- Textron Aviation Inc. (Cessna 172, Cessna 208 Caravan)

- Bombardier Inc. (Learjet 75, Bombardier Global 7500)

- Cirrus Design Corporation (Cirrus SR22, Cirrus Vision Jet)

- Piper Aircraft, Inc. (Piper Archer, Piper Seminole)

- Pilatus Aircraft Ltd. (Pilatus PC-12, Pilatus PC-24)

- Lancair Aerospace (Lancair Legacy, Lancair 320)

- Vulcanair S.p.A. (Vulcanair V1.0, Vulcanair V1.0P)

- Honda Aircraft Company, LLC (HondaJet HA-420)

- Advanced Tactics Inc. (AT-802U, Advanced Tactical Aircraft)

- Embraer Group (Embraer Phenom 100, Embraer Phenom 300)

- Evektor Aerotechnik (Evektor EV-55 Outback, Evektor SportStar)

- Air Tractor Inc. (Air Tractor AT-802, Air Tractor AT-502)

- Flight Design General Aviation GmbH (Flight Design CTLS, Flight Design F2)

- Pipistrel D.O.O. (Pipistrel Virus SW, Pipistrel Panthera)

- Aviation Partners, Inc. (Super 80 Winglets, 737 Winglets)

- Icon Aircraft (Icon A5)

- Van's Aircraft (RV-7, RV-10)

- Mooney International (Mooney M20V Acclaim Ultra, Mooney M20R Ovation)

- Robinson Helicopter Company (R22, R44)

- LSA Aircraft (LSA-1, LSA-2)

List of suppliers for raw materials and components in the Ultralight and Light Aircraft Market:

- Hexcel Corporation

- Solvay SA

- General Electric (GE) Aviation

- Pratt & Whitney (Raytheon Technologies)

- Honeywell Aerospace

- Garmin Ltd.

- Textron Systems (Bell)

- Collins Aerospace (Raytheon Technologies)

- MAG Aerospace

- Continental Motors

- ULPower Aero Engines

- Superior Air Parts

- Boeing (Through its Suppliers)

- DowDuPont (now separate entities)

- Aircraft Spruce & Specialty Co.

- BAE Systems

- GKN Aerospace

- Ametek Aerospace & Defense

- Magellan Aerospace

- Siemens AG

Recent Developments

-

May, 2024 – Embraer, Eve Air Mobility, and Groupe ADP signed a Memorandum of Understanding (MoU) to enhance operations at Paris-Le Bourget Airport, focusing on innovation, sustainable development, and preparing for low-carbon aviation. The collaboration includes new aircraft maintenance facilities, eVTOL operations, and the development of hydrogen infrastructure for Embraer's Energia aircraft family.

-

March, 2024 – Pipistrel appointed Wulf Aviation as its first distributor in Mexico, expanding its global presence. Wulf Aviation will manage sales of Pipistrel’s ultralight, light sport, and type-certified aircraft across Mexico, starting with a Pipistrel Explorer for demonstrations.

-

January 11, 2024 – Cirrus Aircraft introduced the SR Series G7, featuring advanced touchscreen displays, new safety systems, premium amenities, and the Cirrus IQ mobile app. This new generation of their best-selling aircraft offers improved visibility, legroom, and enhanced convenience, redefining personal aviation.

-

September 19, 2024 – Microsoft Flight Simulator 2024 revealed its complete aircraft lineup, featuring 95 aircraft, including 45 new additions and 50 enhanced models from MSFS 2020. The diverse selection includes everything from historical classics to advanced prototypes.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 10.14 Billion |

| Market Size by 2032 | USD 24.31 Billion |

| CAGR | CAGR of 10.21% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Light Aircraft, Ultralight Aircraft) • By Operation (CTOL, VTOL) • By System (Aero structures, Avionics, Engine, Cabin Interiors, Landing Gear, Others) • By Technology(Manned, Unmanned), By End-Use(Civil, Military & Government) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Textron Aviation Inc., Bombardier Inc., Cirrus Design Corporation, Piper Aircraft, Inc., Pilatus Aircraft Ltd., Lancair Aerospace, Vulcanair S.p.A., Honda Aircraft Company, LLC, Advanced Tactics Inc., Embraer Group, Evektor Aerotechnik, Air Tractor Inc., Flight Design General Aviation GmbH, Pipistrel D.O.O., Aviation Partners, Inc., Icon Aircraft, Van's Aircraft, Mooney International, Robinson Helicopter Company, and LSA Aircraft. |

| Key Drivers | • Rising Popularity of Ultralight and Light Aircraft Fueled by Expanding Pilot Training Academies and Flying Clubs |

| Restraints | • Regulatory complexities and evolving standards are slowing the growth of the Ultralight and Light Aircraft market. |

Frequently Asked Questions

Ans: Light Aircraft segment is dominating in Ultralight and Light Aircraft Market in 2023

Ans: North America region dominated the Ultralight and Light Aircraft Market.

Ans: The increasing demand for affordable and efficient pilot training solutions, along with the growth of flying clubs and recreational aviation, is driving the Ultralight and Light Aircraft market.

Ans: The growth rate of the Ultralight and Light Aircraft Market is 10.21% over the forecast period 2024-2032.

Ans: The market size of the Ultralight and Light Aircraft Market was valued at USD 10.14billion in 2023.

Get in Touch