Vascular Closure Devices Market Report Scope & Overview:

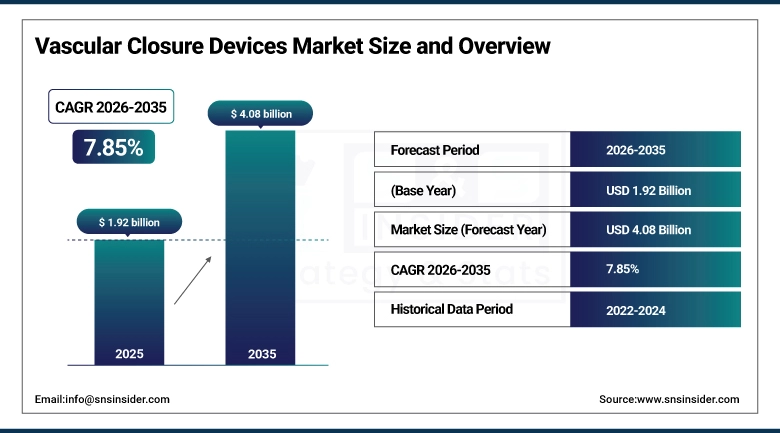

The Vascular Closure Devices Market was estimated at USD 1.92 Billion in 2025 and is expected to reach USD 4.08 Billion by 2035, growing at a CAGR of 7.85% from 2026–2035.

The global vascular closure devices (VCD) market is experiencing robust and sustained growth, driven by the escalating global burden of cardiovascular diseases responsible for approximately 17.9 million deaths annually according to the WHO and the consequent surge in interventional cardiovascular and peripheral vascular procedures that require reliable, rapid hemostasis at arterial and venous access sites. Vascular closure devices encompassing suture-mediated, clip-based, collagen-plug, and external compression systems are deployed to achieve hemostasis at puncture sites following catheterisation procedures including percutaneous coronary intervention (PCI), transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair (EVAR), cardiac electrophysiology, and peripheral arterial interventions. Compared to conventional manual compression that requires 15–30 minutes of sustained pressure and prolonged bed rest, VCDs achieve hemostasis in minutes, enabling early patient ambulation, dramatically shorter hospital stays, and same-day discharge benefits that are compelling both clinically and economically as healthcare systems globally seek to maximise procedural throughput and reduce hospitalisation costs. The market's growth is reinforced by a powerful combination of rising PCI procedural volumes with Germany performing more than 1,600 PCI procedures per million inhabitants annually and the U.S. conducting over 1.5 million cardiac catheterisations per year technological advancement in device design, and expanding reimbursement coverage under programmes including Medicare Advantage that incentivise VCD adoption.

This illustrates the compounding structural alignment of an aging global cohort at risk for progressive cardiovascular disease burden, continuing increase in rates of interventional cardiovascular procedures in which transcatheter interventions such as TAVR and LAAC have become routine approaches for vastly growing patient populations, and that device-based vascular closure provides clinical-and-economic preferable post-procedural care over manual compression rendering VCD adoption effectively a permanent institutional preference once established into practice.

Market Size and Forecast:

-

Market Size in 2025: USD 1.92 Billion

-

Market Size by 2035: USD 4.08 Billion

-

CAGR: 7.85% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vascular Closure Devices Market - Request Free Sample Report

Vascular Closure Devices Market Trends:

-

Rapid expansion of large-bore vascular closure devices including Teleflex's MANTA system driven by the explosive growth of transcatheter structural heart procedures including TAVR and LAAC that require arterial closure at sheath sizes of 14–25 French, well beyond the capability of conventional small-bore VCD platforms.

-

Growing adoption of venous vascular closure devices exemplified by Haemonetics' VASCADE MVP and Cordis' MYNX CONTROL Venous VCD for multi-access electrophysiology and structural heart procedures where venous puncture site closure is increasingly preferred over manual compression for its efficiency and patient comfort advantages.

-

Accelerating shift toward same-day discharge protocols across catheterisation laboratories and cardiac surgical centres, creating direct clinical incentive for VCD adoption as device-based closure is an enabling technology for the rapid ambulation that same-day discharge programmes require.

-

Integration of digital health and remote monitoring capabilities into vascular closure system ecosystems as exemplified by Medtronic's 2025 partnership with a telehealth provider for post-procedure monitoring expanding VCD value propositions beyond the catheterisation laboratory into the post-procedure care continuum.

-

Growing radial access approach adoption in interventional cardiology driven by its lower bleeding complication rates relative to femoral access creating sustained demand for radial-specific external compression VCD platforms and shaping the product innovation priorities of leading VCD manufacturers.

-

Expanding VCD adoption in Asia Pacific markets driven by China's National Medical Products Administration acceptance of 61 innovative device dossiers in 2023 and growing catheterisation laboratory infrastructure investment creating rapidly developing national markets for both locally manufactured and imported VCD platforms.

-

Increasing use of bioabsorbable closure device materials that eliminate permanent implant retention at the access site, reducing long-term complications and improving patient acceptance of device-based closure relative to permanent suture or clip retention systems.

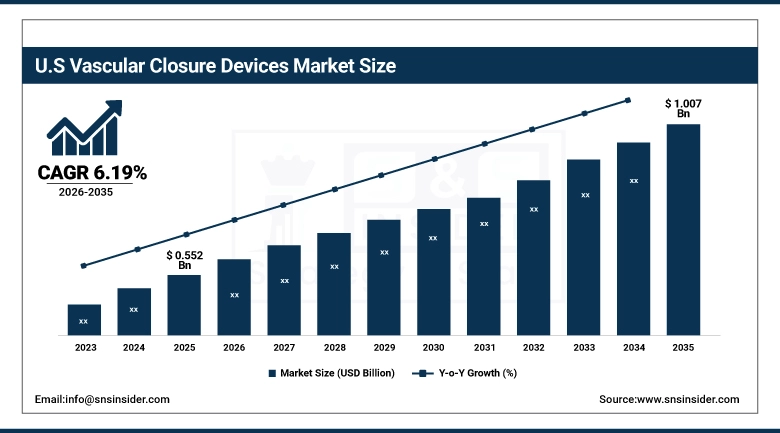

U.S. Vascular Closure Devices Market

U.S. Vascular Closure Devices Market was valued at USD 0.552 Billion in 2025 and is expected to reach USD 1.007 Billion by 2035, registering a CAGR of 6.19% during 2026–2035.

The U.S. is the largest vascular closure devices (VCDs) market in the world driven by highest absolute volume of interventional cardiovascular procedures globally, over 1.5 million cardiac catheterisations performed annually, most favorable reimbursement climate for VCD adoption via Medicare Advantage and private payer coverage; andactive presence among major VCD innovators including Abbott, Medtronic, Teleflex, Haemonetics & Terumo whose ongoing investment in R&D continues to contribute innovation within a robust product development pipeline. Abbott's products designed to close vessels confirmed the direct link from U.S. PCI procedural volume growth (of 17%) to VCD market revenue -- and the company's ability to capture that increased volume -- as a substantial contributor to its commercial performance within the context of 12.5% medical devices growth with all other segments either flat or at best modestly positive. The expanding U.S. structural heart intervention programme that includes TAVR, LAAC and transcatheter mitral valve procedures is forcing a distinction in premium demand tier for large-bore VCD systems commanding average selling prices at significantly greater levels compared to traditional small-bore femoral closure devices.

The AMBULATE trial's demonstration of a 54% reduction in time to ambulation when VASCADE MVP replaced manual compression in venous access site management combined with the August 2024 full U.S. market release of VASCADE MVP XL for multi-access venous closures using 10–15 French sheaths exemplifies the clinical evidence-driven commercial momentum in the U.S. VCD market, where compelling peer-reviewed procedural efficiency data translates directly into rapid institutional adoption and sustained revenue growth for devices that demonstrably improve the patient care pathway and catheterisation laboratory workflow efficiency through the 2026–2035 forecast period.

Vascular Closure Devices Market Segment Insights:

-

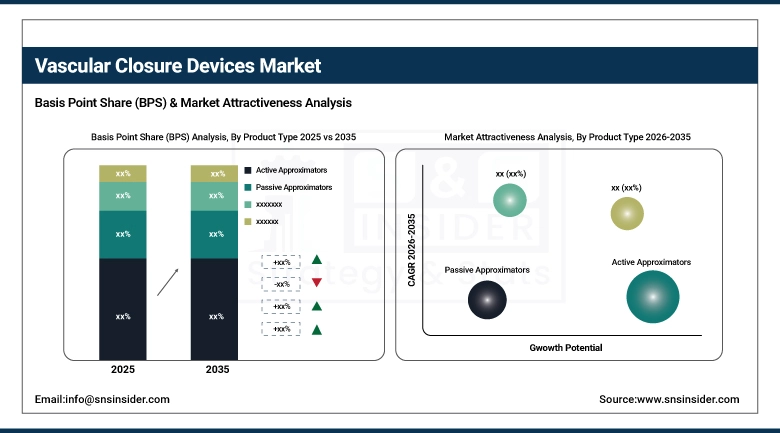

Based on Product Type, Active Approximators accounted for the largest market share (54%) in 2025; Large-Bore Closure Devices expected to be the fastest-growing product type (CAGR).

-

Based on Access Type, Femoral Access dominated with the largest share in 2025; Radial Access expected to be the fastest-growing access type as radial-first procedural adoption expands.

-

Based on Procedure, Interventional Cardiology accounted for the largest market share in 2025; Endovascular Surgery expected to be the fastest-growing procedure segment (CAGR).

-

Based on End-User, Hospitals dominated with the largest share in 2025; Ambulatory Surgical Centers expected to be the fastest-growing end-user segment (CAGR of 7.8%).

Vascular Closure Devices Market Segment Analysis:

By Product Type: Active Approximators dominate, Large-Bore grows fastest

Active approximators encompassing suture-mediated closure devices (Abbott's Perclose ProGlide, ProStyle) and clip-based systems dominated the Vascular Closure Devices Market in 2025 with approximately 54% of revenues, driven by their superior hemostasis reliability, broad clinical applicability across femoral arterial access sizes from 5–24 French, and the extensive clinical evidence library supporting their use across PCI, TAVR, and peripheral vascular interventions. Suture-mediated active closure systems are the de facto standard for large-bore structural heart access sites, where reliable hemostasis is clinically critical, and their dominant market share reflects decades of clinical adoption, operator training investment, and institutional procedural protocol integration.

Among these, the largest segment are 14–25 French Large-bore vascular closure systems dedicated to transcatheter structural heart procedures requiring arterial closure, which is projected to grow at a double-digit CAGR through 2035, in concert with the spectacular growth of TAVR (trans-catheter aortic valve replacement), endovascular aneurysm repair and other structural heart interventions where reliable large-bore access site management is essential. Teleflex's MANTA large-bore closure device deploys a collagen plug designed for use in large arteriotomies has secured itself a robust clinical position as confirmed by the agreement made by Teleflex to acquire Biotronik's Vascular Intervention business in February 2025 which will upgrade and strengthen its structural heart VCD portfolio even furthere.

By End-User: Hospitals dominate, Ambulatory Surgical Centers grow fastest

Hospitals remained the largest end-user segment in the Vascular Closure Devices Market in 2025 with growing market share as of TAVR, EVAR and complex PCI as their conventional use case have the highest VCD utilisation per case and thus higher device adoption. Hospital level clinical relationships and medical education programmes are the core commercial levers at play for manufacturers of closure devices, as hospital catheter lab purchasing committees and programme directors for interventional cardiology have been identified as the two main institutional decision-makers governing device selection.

The Ambulatory Surgical Centers end-user segment is expected to be the fastest-growing, with a CAGR of approximately 7.8% over the forecast period as lower-complexity interventional cardiology and peripheral vascular procedures continue to migrate from inpatient hospitals to outpatient ASC settings due in part to new CMS reimbursement codes that reward same-day discharge and create direct economic incentives for ASC procedural volume growth. Fifth Generation Film VCDs are a technology enabler for outpatient ASC-based interventional procedures where rapid hemostasis and early ambulation of the patient is operationally necessary to meet efficiency in outpatient care delivery.

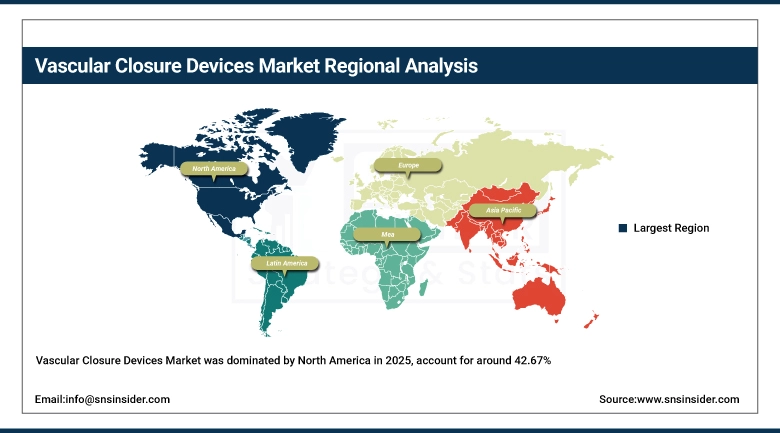

Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

42.67% |

|

Europe |

Germany |

31% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

UAE |

26% |

|

Latin America |

Brazil |

43% |

North America Vascular Closure Devices Market Insights

The global Vascular Closure Devices Market was dominated by North America in 2025, account for around 42.67% of the total revenues worldwide, primarily coming from the U.S.—the largest interventional cardiovascular (IC) procedure market in the world. Global and U.S. market leadership is supported by the most favorable VCD reimbursement policies in world, rapid widespread adoption of structural heart interventions requiring large-bore closure, presence of all the leading commercial VCD manufacturers, and the world's most advanced catheterisation laboratory infrastructure. Canada is an expanding secondary market fueled by increasing procedure volumes and the expansion of minimally invasive cardiovascular interventions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Vascular Closure Devices Market Insights

Asia Pacific is estimated to report the quickest regional CAGR over 2035, owing to quickly developing medical care foundation, expanding cardiovascular illness weight across China, India, Japan and South Korea, rising mindfulness and reception of insignificantly intrusive cardiovascular systems alongside government venture towards Catheterisation Research center limit. In 2023, China's NMPA accepted 61 innovative device dossiers, indicating increasing regulatory throughput for emerging VCD platforms and Terumo's low-double digit cardiovascular revenue growth attests to strong regional demand. MicroPort CardioFlow's approval of the VitaFlow Liberty TAVI in early 2025 is a testament to how quickly demand for premium large-bore VCDs fueled by the structural heart intervention market is growing.

Europe Vascular Closure Devices Market Insights

Europe is a well-established, technically advanced VCD market, with an annual PCI procedure rate >1,600 per million inhabitants in Germany, making it the highest per-capita level of VCD consumption in the world. The MDR transition in Europe has raised the regulatory bar for VCD manufacturers while preserving clinical evidence requirements that keep premium products ahead of low-cost substitutes. Other important European markets are France, the UK, Italy and the Netherlands, each with mature interventional cardiology programs and increasing volumes of structural heart interventions.

Latin America and MEA Vascular Closure Devices Market Insights

Latin America and MEA are growing VCD markets, driven by expanding cardiovascular disease burden, improving healthcare infrastructure, and growing awareness of minimally invasive procedural advantages. Brazil leads Latin American revenues with approximately 43% of regional share, driven by its large cardiovascular patient population and growing interventional cardiology infrastructure. The UAE leads MEA adoption through its advanced healthcare system, high-income patient demographic, and active medical tourism sector attracting cardiovascular patients from across the region.

Market Growth Drivers: Rising interventional cardiovascular procedure volumes and structural heart programme expansion

The primary structural growth drivers for the Vascular Closure Devices Market are increasing global cardiovascular disease burden creating significant future demand for interventional cardiovascular procedures with over 17.9 million CVD deaths worldwide yearly in conjunction with rapid growth of transcatheter intervention programmes globally including TAVR, LAAC, and transcatheter mitral valve repair which represent an emergent high-volume segment that is rapidly growing premium opportunity space for advanced large-bore VCD systems. The AMBULATE trial's 54% decrease in time to ambulation provides convincing evidence that device-based closure is superior clinically and economically to manual compression, establishing an institutional adoption momentum that is effectively irreversible and propelling the market's strong CAGR through 2035.

Abbott's Q1 2025 confirmation that vessel closure products were a key contributor to its 12.5% medical devices revenue growth combined with Teleflex's February 2025 strategic acquisition of Biotronik's Vascular Intervention business to complement its MANTA large-bore closure portfolio collectively demonstrate that leading medical device companies are investing aggressively in VCD market position, viewing vascular closure as a durable, high-growth commercial franchise directly linked to the secular growth of interventional cardiovascular medicine through the 2026–2035 forecast period.

Market Restraints: Device-related complications, high product costs, and radial access shift reducing femoral VCD demand

A significant restraint on the Vascular Closure Devices Market is the potential for device-related vascular complications such as arterial pseudoaneurysm, arteriovenous fistula and access site infection that which although less common than complications from prolonged manual compression in high-risk patients still introduce clinical hesitation among operators not accustomed to VCD techniques and institutional risk/cost assessments associated with procedure selection. Even as this cost decreases, the per-unit costs of VCDs can be high relative to traditionally-mounted compression, creating needs for justification of use in health care systems straining under limited device budgets (especially relevant in developing markets where procedure-cost consciousness limits utilization to higher-complexity cases). Growing adoption of non-VCD technologies such as trans radial access in PCI that only require external compression haemostasis, rather than VCD deployment, is part of a structural shift driving down demand for femoral access VCDs per PCI procedure.

Market Opportunities: Large-bore structural heart closure, venous closure expansion, and Asia Pacific market development

Rapid growth of transcatheter structural heart interventions (TAVR, LAAC, & emerging transcatheter mitral and tricuspid valve programs) offer a compelling near-term premium growth opportunity for the VCD market by virtue of the universal large-bore arterial access closure requirements of all these procedures with purpose-engineered devices commanding substantially higher average selling prices than conventional small-bore femoral VCDs as their key clinical differentiator. Emerging venous closure devices fill a new application category for VCDs, developing devices specifically for vascular access site closure in electrophysiology (EP), structural heart and peripheral venous procedures to expand the total addressable opportunity of the VCD market segment beyond its previous arterial closure concentration. We see strong long-term commercial growth opportunities in Asia Pacific VCD that are backed by an under-penetrated, large opportunity set where investment into catheterisation laboratory infrastructure is accelerating and structural heart programmes are being rapidly deployed.

Recent Developments:

-

February 2025: Teleflex entered a definitive agreement to acquire Biotronik's Vascular Intervention business, complementing its MANTA Large Bore Closure device portfolio and strengthening its competitive position in the rapidly growing structural heart access site closure market.

-

August 2025: Abbott Laboratories launched a new vascular closure device designed to enhance patient recovery times and reduce access site complications, reflecting Abbott's sustained commitment to VCD portfolio innovation and its strategy to maintain leadership in both small-bore and large-bore closure segments.

-

August 2024: Haemonetics released the VASCADE MVP XL Mid-Bore Venous Vascular Closure System for full U.S. market commercial launch, addressing multi-access venous closures using 10–15 French sheaths in electrophysiology and structural heart procedures.

-

July 2024: Cordis received FDA approval for the MYNX CONTROL Venous VCD and was awarded a national agreement with Premier Inc., establishing strong institutional purchasing support for its venous closure portfolio across Premier's member healthcare system network.

-

September 2025: Medtronic unveiled a partnership with a leading telehealth provider to integrate remote monitoring capabilities into its vascular closure device ecosystem, extending its VCD value proposition beyond the catheterisation laboratory into post-procedure patient care management.

Vascular Closure Devices Market Key Players:

-

Abbott Laboratories

-

Teleflex Incorporated

-

Haemonetics Corporation

-

Terumo Corporation

-

Medtronic plc

-

Boston Scientific Corporation

-

Cardinal Health Inc.

-

Becton, Dickinson and Company (BD)

-

B. Braun Melsungen AG

-

Johnson & Johnson MedTech

-

Cordis (Cardinal Health)

-

Vasorum Ltd.

-

INVAMED

-

Vivasure Medical Ltd.

-

Merit Medical Systems Inc.

-

Vascular Solutions (Teleflex)

-

TZ Medical Inc.

-

Transluminal Technologies LLC

-

InVivo Therapeutics Holdings Corp.

-

Tricol Biomedical Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.92 Billion |

| Market Size by 2035 | USD 4.08 Billion |

| CAGR | CAGR of 7.85% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Passive Approximators, Active Approximators, External Hemostatic Devices) • By Access Type (Femoral, Radial, Others) • By Procedure (Interventional Cardiology, Interventional Radiology, Endovascular Surgery) • By End Use (Hospitals, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, Teleflex Incorporated, Haemonetics Corporation, Terumo Corporation, Medtronic plc, Boston Scientific Corporation, Cardinal Health Inc., Becton, Dickinson and Company (BD), B. Braun Melsungen AG, Johnson & Johnson MedTech, Cordis (Cardinal Health), Vasorum Ltd., INVAMED, Vivasure Medical Ltd., Merit Medical Systems Inc., Vascular Solutions (Teleflex), TZ Medical Inc., Transluminal Technologies LLC, InVivo Therapeutics Holdings Corp., Tricol Biomedical Inc. |

Frequently Asked Questions

North America dominated the Vascular Closure Devices Market in 2025 with approximately 42.67% of global revenues, led by the United States the world's highest-volume interventional cardiovascular procedure market supported by the most favourable VCD reimbursement policies, rapid structural heart programme expansion, and the commercial presence of leading VCD innovators including Abbott, Medtronic, Teleflex, and Haemonetics.

Active Approximators encompassing suture-mediated and clip-based closure systems dominated the market in 2025 with approximately 54% of global revenue, driven by their superior hemostasis reliability, broad clinical applicability across arterial access sizes, and extensive procedural adoption in PCI, TAVR, and peripheral vascular interventions.

Rising global interventional cardiovascular procedure volumes driven by escalating CVD burden, the rapid expansion of structural heart interventions including TAVR and LAAC creating premium large-bore VCD demand, and the clinical and economic superiority of device-based closure over manual compression enabling same-day discharge protocols are the primary structural growth drivers through 2035.

The Vascular Closure Devices Market was valued at USD 1.92 billion in 2025.

The Vascular Closure Devices Market is expected to grow at a CAGR of 7.85% from 2026 to 2035.

Get in Touch