Veterinary Point Of Care Diagnostics Market Report Scope & Overview:

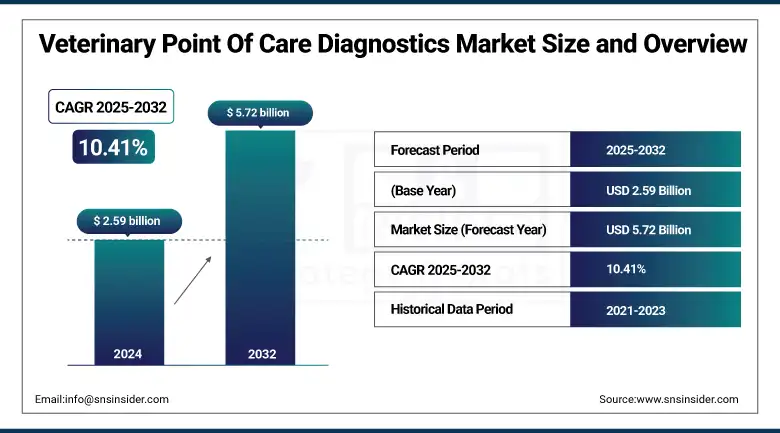

The veterinary point of care diagnostics market size was valued at USD 2.59 billion in 2024 and is expected to reach USD 5.72 billion by 2032, growing at a CAGR of 10.41% over 2025-2032.

The veterinary point of care diagnostics market is experiencing substantial momentum due to a combination of technological innovations, increased pet ownership, and growing demand for rapid and accessible animal health solutions. As veterinarians and livestock handlers increasingly prioritize real-time testing, the global veterinary point of care diagnostics market is being driven by higher diagnostic usage across both companion and livestock animals. Rising incidences of zoonotic diseases, coupled with growing awareness of preventive animal care, are pushing demand for field-based and in-clinic diagnostics.

To Get more information On Veterinary Point Of Care Diagnostics Market - Request Free Sample Report

Regulatory backing in developed markets such as the U.S. veterinary point of care diagnostics market, including FDA-approved PoC testing devices, is supporting adoption. R&D spending by leading veterinary point of care diagnostics companies, such as IDEXX Laboratories and Zoetis, is intensifying, especially in the areas of microfluidic, immunodiagnostic, and molecular platforms. Additionally, robust supply chain availability and increasing venture capital investments in animal health technology startups are further strengthening the market.

Innovations in portable analyzers, real-time imaging tools, and cloud-integrated diagnostic platforms are among the top veterinary point of care diagnostics market trends propelling long-term veterinary point of care diagnostics market growth. A deeper veterinary point of care diagnostics market analysis reveals that increasing rural outreach by diagnostic service providers and rising demand for disease surveillance in livestock are also expanding the veterinary point of care diagnostics market share globally.

In 2024, Zoetis introduced a next-generation digital cytology platform integrated with AI to enhance rapid disease detection, indicating a strong R&D-driven direction in the veterinary point of care diagnostics market.

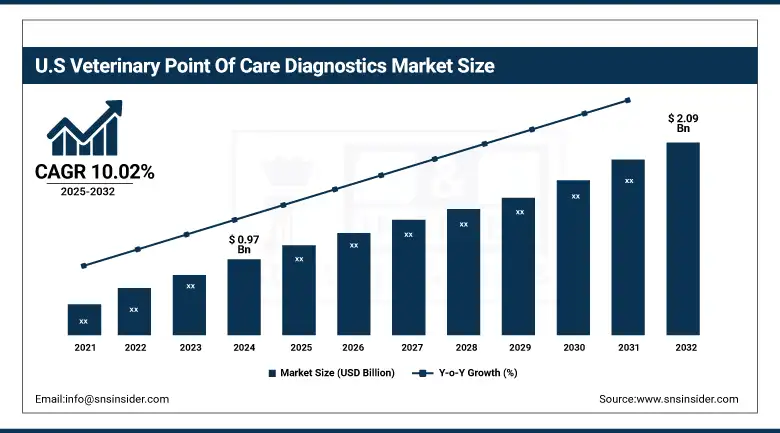

The U.S. veterinary point of care diagnostics market size was valued at USD 0.97 billion in 2024 and is expected to reach USD 2.09 billion by 2032, growing at a CAGR of 10.02% over 2025-2032. U.S. held the largest share in the regional market, covering more than 40% of the global veterinary point of care diagnostics market share, and was primarily attributed to the presence of a robust number of veterinary clinics, expanding companion animal base, and soaring adoption of advanced diagnostic techniques. In Canada, mobile veterinary diagnostics and preventive pet healthcare awareness are on the rise. In addition, the availability of key veterinary point of care diagnostics companies, including IDEXX Laboratories, Zoetis, and Heska Corporation, is expected to contribute to regional innovation and product availability.

Market Dynamics:

Drivers:

-

The Rising Demand for Rapid Diagnostic Turnaround in Animal Healthcare, Especially in Companion Animal Segments

The veterinary point of care diagnostics market is surging with respect to the demand for rapid diagnostic results in the animal health sector, particularly the companion animal industry. Growing awareness about preventative and routine diagnostics is boosting the uptake of veterinary compliance and adoption of portable testing devices. Rise of Pet Insurance Covers, Disposable Incomes. Pet insurance coverage and the trend of increased disposable incomes are benefiting each other by boosting diagnostic spending.

According to the American Pet Products Association, U.S consumers spent more than USD 38 billion on veterinary care in 2023, of which a considerable share went into diagnostic services. Manufacturers are upscaling lab-on-chip technologies and miniaturized analyzers on the supply side. With their demand for in-clinic testing, companies such as Heska and Virbac are broadening their PoC testing offerings.

Furthermore, the World Organisation for Animal Health (WOAH) in its policies of control/eradication of diseases, has highlighted the early identification of the infected animals, furthermore confirming the dividends of PoC diagnostics within global veterinary practice. Substantial R&D investments are also being reported, such as Mars Petcare’s Waltham Petcare Science Institute’s ongoing support for the development of real-time diagnostic technology for the control of infectious diseases. Moreover, increasing penetration of smart diagnostic systems with AI incorporation is promoting user adoption, which is in turn propelling the growth of veterinary point of care diagnostics market on the back of technology and demand.

Restraints:

-

The High Initial Cost of Devices and Testing Kits, Which Can Be Prohibitive for Smaller Clinics, Especially in Developing Regions

The veterinary point-of-care diagnostics market is hindered by several significant shortcomings. Among other barriers, the high cost of devices and testing kits is one of the major obstacles faced, which limits their purchase by small clinics, particularly in developing regions. Furthermore, in contrast to human diagnostics, veterinary diagnostic tests are rarely subject to standardised regulatory control, resulting in inconsistent product validation and a lack of professional confidence in some test outcomes.

The decentralized nature of veterinary services globally adds complexity to consistent adoption, with many rural practices yet to make the switch from centralized labs for budgetary reasons. Less than 40% of veterinary practices in low-income areas use PoC diagnostic tools regularly, according to a Vetnosis report. Supply-side constraints, including a limited pool of trained technicians to run tests and interpret results in the field, also impact the accuracy and implementation of diagnosis. In addition, low animal diagnostics prices and lack of insurance for testing in many markets also reduce the incentives for testing. Furthermore, the FDA approval process of new PoC devices, in particular non-optical methods of molecular testing, delays manufacturers’ time-to-market. This extends lead times for innovation, despite high levels of R&D spend, disjuncting the worlds of development and deployment.

Segmentation Analysis:

By Product

Consumables, reagents, and kits held the largest share in the veterinary point of care diagnostics market in 2024 with a share of 58%. Due to their high frequency of usage, low cost, and practicality, they are indispensable for day-to-day diagnostics both in the veterinary hospital and at the field level. These are reagents, test strips, and rapid diagnostic kits for diseases such as parvovirus, leptospirosis, among others. The products category that is growing the fastest is that of instruments and devices, as innovative and technology-driven development of portable analyzers, imaging systems, and integrated devices, which facilitate rapid testing and decision making. Small-point-of-care diagnostic platforms are important in the veterinary practice setting, particularly high-volume urban and suburban practices.

By Test Type

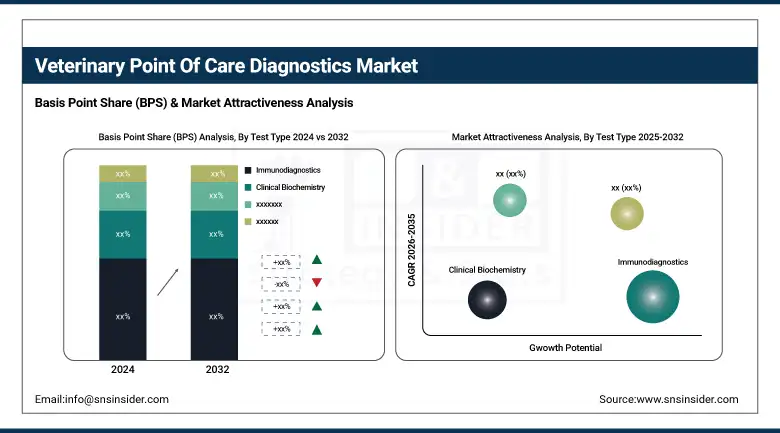

Immunodiagnostics accounted for the largest share of the veterinary point of care diagnostics market in 2024, with a 37% market share. These tests are commonly used because they provide fast and accurate results for infectious diseases, hormone levels, and other biomarkers. The increasing incidence of zoonotic and infectious diseases and the implementation of lateral flow assays are the factors responsible for their dominance. Further, the market for molecular diagnostics is growing rapidly as veterinarians look for high-end, high-specificity diagnostic solutions for early pathogen detection and screening for genetic disease. The emergence of miniaturised PCR systems and isothermal amplification methods was improving the capacity for field- and clinic-based molecular testing, particularly for high-value animals and herd health initiatives.

By Animal Type

Companion Animals was the largest segment in the global veterinary point of care diagnostics market, 60% share of which was held by it in 2024. The dominance is attributed to an increase in rate of pet ownership, rise in humanization of pets, and surge in awareness about preventative health care. Routine medical health check-ups and frequent diagnostics for diseases like diabetes, kidney disease, and infections add to this trajectory. Whereas, the demand for livestock animals is anticipated to propel at the fastest CAGR on account of increasing demand of animal protein, economic losses faced by countries owing to the outbreaks which are undiagnosed and government focus on early disease detection using PoC tools particularly in agriculture and its allied industry, further, in the developing economies having a considerable distributive and large livestock population.

By Sample Type

The blood/plasma/serum samples segment dominated the market in 2024, accounting for around 56% of the veterinary point of care diagnostics market. These sample types are powerful and cover a multitude of PoC diagnostic modalities such as immunodiagnostic testing, hematology, and molecular testing. Many blood-based tests are critical for infectious disease, inflammation, metabolic disorder, and organ function in companion as well as livestock animals. The urine sample type is the most rapidly expanding, gaining prevalence in diagnoses of renal diseases, urinary tract infections, and metabolic diseases like diabetes. Increasing use of automated urinalysis devices and test strips in veterinary clinics and indoor use is driving growth, particularly in geriatric pet care and routine wellness programs.

By Application

In 2024, infectious diseases dominated the veterinary point of care diagnostics market applications with around 48% share of the total market. Growing fears over zoonotic infections and the rapid spread of disease among herds and pets are fueling demand for quick diagnostics that can be deployed on-site or in clinics. These comprised tests on parvovirus, leptospirosis, feline leukemia, and bovine tuberculosis. Heredity disorder and congenital disorders are the highest growing applications, as the use of genetic screening kits and PoC devices is increasing. This is particularly the case in the pet owner and breeder community, who are increasingly looking for ways to detect inherited conditions and congenital defects, particularly in purebred animals and high-value animals, stimulating segment growth.

By End Use

Veterinary hospitals and clinics were the leading end-user segment in 2024 and accounted for 68% share of the veterinary point of care diagnostics industry. These are facilities where infrastructure for a higher level of diagnostic work exists and trained personnel and equipment capable of conducting screening right in the facility. Rise in pet visits and rise in veterinarians’ awareness of early detection and disease prevention favor segment dominance. The fastest growing end-use segment is home care settings, led by an increasing trend of tele-veterinary services, direct-to-consumer diagnostics, and pet owners' inclination for convenience. The easy-to-use test kits and portable hand-held devices for home use might facilitate early detection of diseases outside the conventional health care system and subsequent monitoring.

Regional Analysis:

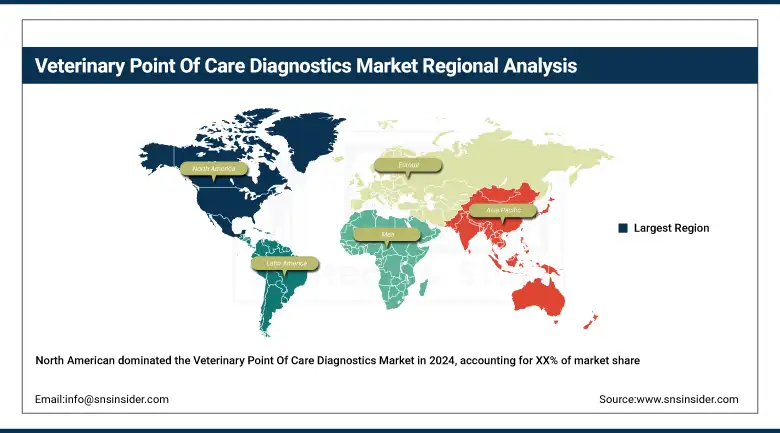

The North American region accounted for the largest share of the global veterinary point of care diagnostics market in 2024, driven by its well-established veterinary healthcare system, increasing pet adoption, and high expenditure on animal healthcare.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe was the second-largest region in the veterinary point of care diagnostics market in 2024, owing to the implementation of animal health monitoring laws and increasing need for quick tests for herd animal health management. In the region, Germany and the UK stand out in terms of strong networks of veterinarians and investments in precision veterinary medicine. For instance, expanding livestock industry in Germany drives the need for quick testing of infectious diseases. Demand is increasing in France and Spain for home-use diagnostic kits. Furthermore, research in animal diagnostics and disease surveillance funded by the EU across the EU region is helping to drive the market, particularly in molecular diagnostics.

Asia Pacific is the fastest-growing region in the global veterinary point of care diagnostics market, due to the growing pet humanisation, rising income, and the surge in livestock population. China and India play an important role because of their high cattle populations and veterinary infrastructure supported by the government. China is being led by demand for herd health diagnostics and the increasing prevalence of zoonotic diseases, while India is investing in diagnostics vans and rural veterinary programs. Japan and South Korea are also penetrating the advanced diagnostics research and development market for companion animals. Introduction of affordable diagnostic kits also continues to propel the market penetration in ASEAN Member States and Australia.

Key Players:

IDEXX Laboratories, Zoetis, Heska Corporation, Virbac, Thermo Fisher Scientific, Mindray, Woodley Equipment, FUJIFILM Corporation, Getein Biotech, Eurolyser Diagnostica, Randox Laboratories, AniPOC, Carestream Health, NeuroLogica, bioMérieux, Biotangents, Esaote, GE Healthcare, Skyla Corporation, Scil Animal Care, Abaxis, Bionote, Chison Medical Technologies, IDvet, and QGenda.

Recent Developments:

In June 2025, eight veterinary clinics in Victoria, Australia, began trialling the AI-powered Atrio Pet Pulse wearable ECG monitor, enabling 24-hour cardiac rhythm tracking in dogs and facilitating early detection of heart disease at the point of care.

In June 2025, Zoetis introduced AI Masses, enhancing its Vetscan Imagyst analyzer with deep‑learning cytology analysis for lymph node and skin lesions, delivering results in minutes to support rapid in-clinic cancer screening and streamline workflows.

| Report Attributes | Details |

| Market Size in 2024 | USD 2.59 billion |

| Market Size by 2032 | USD 5.72 billion |

| CAGR | CAGR of 10.41% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Consumables, Reagents, Kits, Instruments and Devices, and Others (software platforms, diagnostic accessories, and disposables used in PoC testing setups)) • By Test Type (Immunodiagnostics, Clinical Biochemistry, Molecular Diagnostics, Hematology, Urinalysis, and Others (microbiology-based methods, rapid strip tests, and emerging nanotechnology-based diagnostic methods)) • By Animal Type (Companion Animals (Dogs, Cats, Horses, and Others – rabbits, ferrets, guinea pigs, exotic pets), Livestock Animals (Cattle, Swine, Poultry, and Others – sheep, goats, aquaculture species like fish)) • By Sample Type (Blood/Plasma/Serum, Urine, Fecal, and Others (saliva, skin scrapings, nasal swabs, and other tissue samples)) • By Application (Infectious Diseases, Non-Infectious Conditions, Hereditary and Congenital Disorders, Acquired Health Conditions, and Others (nutritional deficiencies, toxicological screenings, and wellness assessments)) • By End Use (Veterinary Hospitals and Clinics, Diagnostic Laboratories, Home Care Settings, and Others (mobile veterinary units, research institutes, NGOs involved in animal welfare)) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | IDEXX Laboratories, Zoetis, Heska Corporation, Virbac, Thermo Fisher Scientific, Mindray, Woodley Equipment, FUJIFILM Corporation, Getein Biotech, Eurolyser Diagnostica, Randox Laboratories, AniPOC, Carestream Health, NeuroLogica, bioMérieux, Biotangents, Esaote, GE Healthcare, Skyla Corporation, Scil Animal Care, Abaxis, Bionote, Chison Medical Technologies, IDvet, and QGenda. |

Frequently Asked Questions

Portable PoC tools enable faster diagnosis in remote and field settings, improving disease detection and timely treatment decisions.

Immunodiagnostics, molecular diagnostics, and microfluidics-based testing platforms are gaining popularity due to speed and accuracy.

Key trends include the adoption of AI-powered analyzers, telemedicine integration, and the shift from lab-based to in-field diagnostics.

Key growth drivers include rising demand for rapid, on-site testing, growing pet insurance penetration, and the expansion of companion animal healthcare.

The global veterinary PoC diagnostics market was valued at USD 2.59 billion in 2024, with steady growth driven by increased pet ownership and animal health awareness.

Get in Touch