Vegan Food Market Report Scope & Overview:

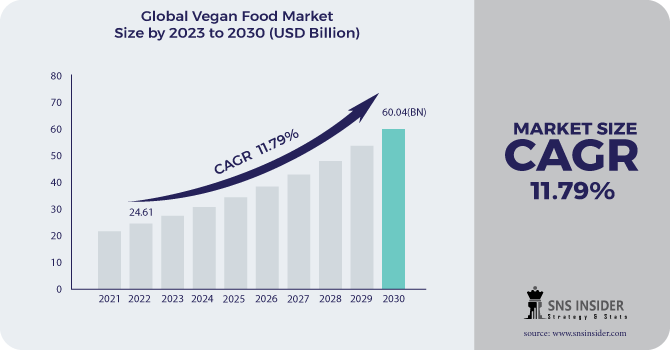

Vegan Food Market size was valued at $24.61 billion in 2022 and is expected to reach $60.04 billion by 2030, registering a CAGR of 11.79% from 2023 to 2030.

Vegan food items are by and large dairy-free or meat-free food items that are gotten or handled from plant-based sources. Meat substitutes are items that look like real meat in taste, flavor, and appearance however are more grounded than meat. Such items are progressively being utilized as alternatives for normal meat and meat items. They are essentially made out of fixings like soy, wheat, and others. Tofu is presumably the most well-known meat substitute and is generally utilized as an option for pork, chicken, hamburger, and different meats. Likewise, dairy-free food and drink items are ready from sources like almond, soy, rice, coconut, and others. Prominently drank dairy elective-based items are milk, frozen yogurt, cheddar, margarine, and others.

Expansion in stoutness rates everywhere, and development in medical issues, for example, heart infections, hypertension, diabetes, asthma, and others, have elevated the general well-being awareness among shoppers. This has brought about expansion sought after for various sorts of good food items including vegetarian food items. Additionally, over the recent years, there has been a flood in a number of the vegan populace all over the planet explicitly in created areas like North America and Europe. This arrangement of the populace is either lactose narrow-minded or exceptionally cognizant about food consumption. In this manner, flood in several vegetarian populace combined with ascend in the number of well-being cognizant purchasers drive the interest for vegan food items.

Market Dynamics:

Market Driver:

-

The rising occurrences of constant infections address

-

Different non-government associations (NGOs) are spreading mindfulness

Market Restraints:

-

The significant expense of vegan food items and their related lack block the market development

-

Buyers need to embrace exhortation from medical services experts

Market Opportunities:

-

The plant-based food space is set to fill quickly before long.

-

Ongoing send-offs in the space from large food players

Market Challenges:

-

The plant-based offering is altogether more costly than its creature-based partners.

Impact of Covid-19:

The interest in vegan food was ascending before the explosion of the COVID-19 pandemic one year prior, vegan, vegan, and flexitarian eating fewer cars were rising quickly. Furthermore, concerns concerning planetary manageability, individual well-being, and the mortal creature's treatment flooded this expanded consideration towards plant-based diets, and presently apparently the pandemic has just cultivated this pattern.

Market Estimations:

By Product Type:

Dairy options were the biggest item section in 2018 and represented over half of the worldwide income. Around 65% of the worldwide populace is lactose prejudice, which is a key variable supporting the interest in dairy elective food things. Accessibility of various items, for example, cheddar, yogurt, frozen yogurt, and bites, has likewise drawn in non-vegans and extended the purchaser base of this portion.

Furthermore, producers in the market have presented various quality food things in various flavors with alluring bundling arrangements. This is additionally prone to add to section development. Among such items, plant-based cheddar represented the biggest offer in dairy choices. Expanding its item portfolio alongside rising instances of lactose bigotry is supposed to fuel its interest.

By Distribution Channel:

In light of the dispersion channel, the Vegan Food market is fragmented into disconnected and on the web. Among the dissemination channel, the disconnected section records the higher-worth vegan food portion of the overall industry. A portion of the key retailers, for example, the huge, little retailer including the specialty stores have been considered in the disconnected stores of vegetarian food items. The development of store/hypermarket fragment in the dairy elective market can be credited to the expansion in the reception of stores and hypermarkets in both the experienced and developing business sectors. Besides, the one-stop arrangement given by these retail designs makes them an exceptionally well-known choice for looking for shoppers. Moreover, these retail designs offer a wide scope of items at a serious cost to clients and are typically situated in effectively available regions, which adds to in general engaging quality of this fragment. Additionally, the specialty stores likewise satisfy quick satisfaction for purchasers as items purchased can be brought back home without holding up time.

Key Market Segmentation:

By Product Type:

- Dairy Alternative

- Meat Substitute

- Others

By Distribution Channel:

- Online Sales Channels

- Offline sales channels

.png)

Regional Analysis:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

Key Players:

Sun Opta Inc., Whitewave Foods Company Inc., Hain Celestial Group Inc., Bhlue Diamond Growers, Archer Daniel Midland Company, Organic Valley Corporative, Panos Brand LLC., Pascual Group, Earth’s Own Food Company Inc., Living Harvest Food Inc.

Bhlue Diamond Growers-Company Financial Analysis

Growing Alertness of Animal Cruelty is Driving the Vegan Food Market Growth

The worldwide vegetarian food market is supported by the developing mindfulness of seeing the creature’s well-being as well as brutality in the food business, which has prompted a critical shift towards plant-based food items and away from creature-based items. The developing notoriety of the vegetarian diet and the arising pattern of the following veganism has brought about a sped-up interest in vegan food. For example, the rising reception of this eating regimen by significant big names has improved the market development as an ever-increasing number of fans are beginning to embrace this eating routine.

In the West, a rising extent of the populace has quit devouring meat, accordingly embracing elective food, like vegetarian items. Further, the rising attention to the advantages of eating these items plays a critical influence on the reception of vegetarian food, consequently, working with the market development. Before long, the rising reception of a vegan diet in arising districts and item broadening are supposed to move the development of the market forward.

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 24.61 Billion |

| Market Size by 2030 | US$ 60.04 Billion |

| CAGR | CAGR 11.79% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Dairy Alternative, Meat Substitute, and others) • by Distribution Channel (Offline and Online) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Sun Opta Inc., Whitewave Foods Company Inc., Hain Celestial Group Inc., Bhlue Diamond Growers, Archer Daniel Midland Company, Organic Valley Corporative, Panos Brand LLC., Pascual Group, Earth’s Own Food Company Inc., Living Harvest Food Inc. |

| Key Drivers | •The rising occurrences of constant infections address. •Different non-government associations (NGOs) are spreading mindfulness. |

| Restraints | •Buyers need to embrace exhortation from medical services experts. |

Frequently Asked Questions

Ans: The Vegan Food market size was valued at $22.02 billion in 2021

Ans: The rising occurrences of constant infections addressed and different non-government associations (NGOs) are spreading mindfulness are driving the market growth.

Ans: Vegan food market is segmented into product types and distribution channels.

Ans: The Vegan food market incorporates the development of the retail channel, the development of food and drinks, and ascend in veganism.

Ans: Manufacturers, Research Institutes, university libraries, suppliers, and distributors of the product.

Get in Touch