Pain Management Market Report Scope & Overview:

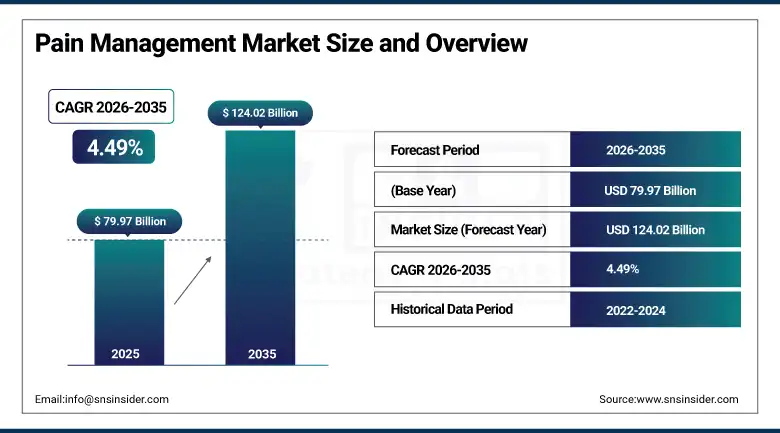

The Pain Management Market was valued at USD 79.97 Billion in 2025 and is expected to reach USD 124.02 Billion by 2035, growing at a CAGR of 4.49% from 2026–2035, sustaining steady long-term growth across both established and emerging healthcare markets.

The pain management market is experiencing steady growth due to the increase in prevalence rates of chronic pain disorders, an increase in the number of aging people, and technological developments in pain management therapies. More than 20% of adults worldwide suffer from chronic pain, a major contributor to decreased quality of life and healthcare system burdens with 24.3% of adults reporting chronic pain of at least three months in duration during the year 2023. Non-opioid drugs are gaining popularity in pain therapy due to the current global opioid crisis which has pushed many doctors and patients into searching for safer options, with neuromodulation devices including spinal cord stimulators and TENS being extensively used in clinical practice due to their effectiveness in managing chronic pain conditions, especially neuropathy and back pain disorders.

In 2024, the FDA approved a new monoclonal antibody treatment for chronic migraine, which represents one of the latest instances where the biologic route to treating pain problems has become more common. This reflects the trend among drug companies to focus on biologics that get to the root of the problem behind chronic pain problems instead of just providing a mask for it, since pharmaceutical companies realize that they need to distinguish themselves from commoditized small molecule drugs.

Market Size and Forecast

-

Market Size in 2026E: USD 83.55 Billion

-

Market Size by 2035: USD 124.02 Billion

-

CAGR: 4.49% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

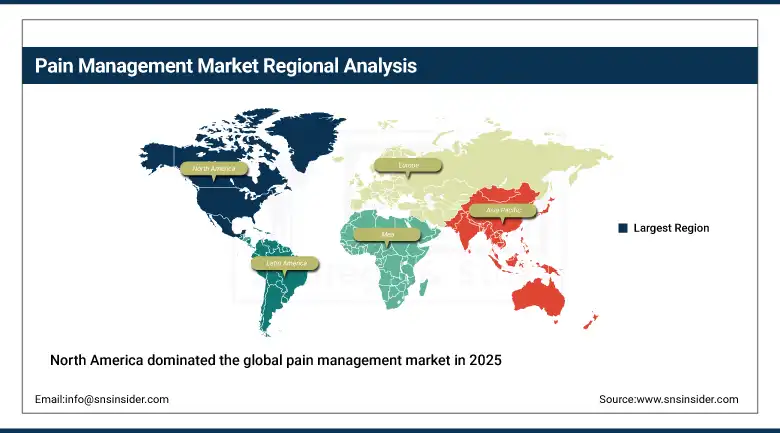

Largest Region: North America

To Get more information On Pain Management Market - Request Free Sample Report

Pain Management Market Trends

-

Non-opioid drug adoption is accelerating as the global opioid crisis pushes practitioners toward safer treatment alternatives.

-

Neuromodulation devices including spinal cord stimulators are gaining adoption for chronic neuropathic and back pain.

-

Regenerative medicine applications including stem cell therapies are expanding for musculoskeletal pain treatment.

-

AI-integrated pain management systems are enabling precision treatment planning and remote patient monitoring.

-

Monoclonal antibody therapies are reshaping migraine treatment through targeted, biologic-based therapeutic mechanisms.

The U.S. Pain Management Market Outlook

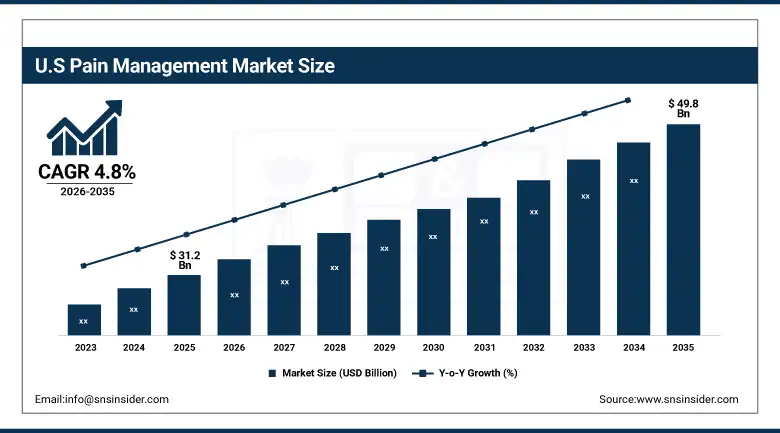

The U.S. Pain Management Market was valued at approximately USD 31.2 Billion in 2025 and is projected to reach approximately USD 49.8 Billion by 2035, expanding at a CAGR of 4.8% during 2026–2035.

Due to the high percentage of adults suffering from chronic pain, which is around 20%, the U.S. is among those countries that carry a huge burden of painful conditions, thanks to the availability of modern medical devices for pain treatment, like neuromodulators, as well as a trend towards non-opioid pain treatments. In addition, the country leads the development and registration of new pain therapy methods, like FDA-approved in 2024 the first drug based on a monoclonal antibody against migraines.

In March 2023, Pfizer Inc. got a marketing authorization from the US Food & Drug Administration for ZAVZPRET, the first nasal spray with calcitonin gene-related peptide receptor antagonism intended to use as an acute therapy of migraines with/without aura in adults. It was proved by a positive result of the Phase 3 trial, where ZAVZPRET showed better effects than a placebo in terms of pain freedom within two hours after its administration.

Pain Management Market Segment Analysis

-

By Type, NSAIDs dominated the market with a 34% share in 2025, while antimigraine therapies are predicted to show the fastest growth through monoclonal antibody innovation.

-

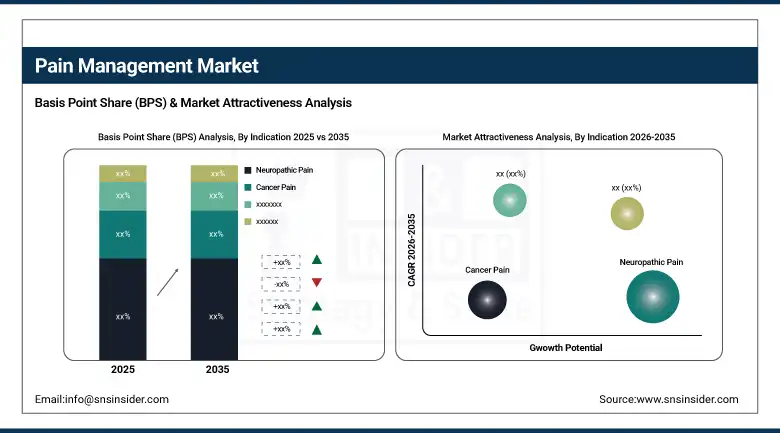

By Indication, neuropathic pain dominated the market through delegated conditions including diabetic neuropathy, while musculoskeletal pain was the fastest-growing segment through rising back pain and osteoarthritis prevalence.

-

By Mode of Purchase, over-the-counter segment dominated the pain management market in 2025, while the prescription-based segment is expected to register the fastest CAGR during the forecast period.

-

By End-User, hospitals & clinics segment dominated the pain management market in 2025. The pharmaceutical companies segment is projected to witness the fastest CAGR during the forecast period.

By Type, NSAIDs dominate, antimigraine therapies grow fastest

NSAIDs segment dominated the pain management market with a market share of 34% in 2025, mainly due to their efficacy, cost-effectiveness, and availability. The drugs are widely used for arthritis and musculoskeletal disorders, as they can reduce pain, inflammation, and fever, with their easy availability over the counter and established safety profiles making them a first-line treatment option that drives growth in the pain management sector as more patients seek NSAIDs for relief, contributing significantly to overall market revenue across both acute and chronic pain treatment protocols worldwide.

The antimigraine category is anticipated to register the highest growth rate during the forecast period on account of rising instances of a disease, which impacts over 12% of the world's total population. Monoclonal antibody-based products, recently approved by the FDA, are bringing about a paradigm shift in migraine therapy by offering precise relief, thus fueling quick adoption as consumers look out for specialized treatment options for their condition. As health insurance coverage increases for the biologic-based migraine medicines, the demand is set to continue driving the growth of the segment.

By Indication, neuropathic pain dominates, musculoskeletal pain grows fastest

In 2025, the neuropathic pain management solutions segment dominated the market due to delegated neuropathic conditions, diabetic neuropathy, and postherpetic neuralgia. These diseases are chronic and complicated, afflicting around 7-10% of the population worldwide, hence research and development remains high, making neuropathic pain one of the largest markets within the broader pain management landscape, with pharmaceutical companies continuing to invest heavily in next-generation anticonvulsant and antidepressant formulations specifically targeting nerve-related pain mechanisms.

The musculoskeletal pain market segment grew the fastest, and it is fueled by the increase in diseases like back pain and osteoarthritis, which affects more than 1.7 billion people globally. Innovations in minimally invasive procedures and regenerative medicine continue to fuel this growth, as the need to manage such musculoskeletal pain becomes ever so popular with a population that continues to age and engage in physically active lifestyles.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Asia Pacific |

China |

44.8% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Pain Management Market Insights

North America dominated the global pain management market in 2025, accounting for approximately 41% of total market revenue, bolstered by its advanced healthcare systems, high levels of awareness, and significant investments in research and development. With around 20% of adults affected by chronic pain, the region is also burdened with a large number of pain-related conditions, while the availability of advanced technologies such as neuromodulation devices and an increasing shift toward non-opioid therapies further strengthens the market.

The U.S. takes the lead in the development and approval of new pain management treatments, including the monoclonal antibody for migraine approved by the FDA in 2024, further cementing North America’s position as a global leader in the area. Canada and Mexico contribute supplementary regional demand through their own growing chronic pain treatment infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Pain Management Market Insights

Europe is a significant pain management market where established healthcare infrastructure, growing geriatric population, and increasing adoption of non-opioid therapies collectively sustain regional demand. Germany accounts for a substantial share of European revenues through its large pharmaceutical sector and advanced clinical research infrastructure, alongside a strong domestic medical device manufacturing base supporting neuromodulation therapy adoption.

The United Kingdom’s established National Health Service treatment protocols and France’s growing neuromodulation device adoption contribute substantial secondary regional demand. European regulatory frameworks continue shaping biologic and monoclonal antibody therapy approval pathways across the region’s major pharmaceutical markets, with the European Medicines Agency increasingly coordinating approval timelines with FDA decisions for breakthrough pain therapies.

Asia Pacific Pain Management Market Insights

The Asia Pacific region is expected to have the fastest growth throughout the forecast period. The reason for this growth is due to the large, aging population, the increasing incidence of lifestyle-related diseases, and improvement in healthcare infrastructure. The region is highly plagued with musculoskeletal disorders, especially widespread back pain and arthritis, which greatly affect its population across both urban and rural communities experiencing rapid demographic transition.

With increased awareness about the available pain management alternatives and increased disposable incomes, advanced therapies are increasingly being used. Government programs that enhance healthcare access and investments in the production of medical devices are promoting the market, with most of these developments taking place in populous countries like China and India, with rapidly developing pharmaceutical industries capable of producing both branded and generic pain management formulations domestically.

MEA & Latin America Pain Management Market Insights

The Middle East and Africa pain management market is expanding through growing healthcare infrastructure investment in the UAE and Saudi Arabia, where rising chronic disease prevalence is creating new demand for advanced pain treatment options. South Africa’s growing healthcare access initiatives contribute secondary regional demand.

Latin America’s pain management market is developing through growing healthcare access in Brazil and Mexico, where rising chronic pain prevalence and expanding insurance coverage are gradually increasing demand for both OTC and prescription pain treatment options across the region’s major population centers.

Market Dynamics

Growth Drivers: Rising chronic pain prevalence and non-opioid therapy innovation fueling sustained market expansion

Chronic pain, a fact that affects 1 in 5 adults globally, is one of the significant drivers of the pain management market. Conditions such as arthritis, fibromyalgia, neuropathic pain, and cancer-related pain are on the increase with the aging population, sedentary lifestyles, and lifestyle-related diseases, with the growing burden of chronic pain demanding effective pain management solutions that drive demand for both pharmacological and non-pharmacological treatments across diverse care settings spanning primary care through specialist pain clinics.

In a market where increased attention has been drawn to opioid-based treatments amid the global opioid crisis, there is an overall shift to safer alternatives. Innovations such as neuromodulation technologies including spinal cord stimulators and wearable pain management solutions address chronic and acute pain conditions better and cause fewer side effects, with regenerative medicine and biologics such as monoclonal antibodies representing promising avenues for less invasive pain relief that increasingly appeal to both prescribers and patients seeking alternatives to long-term opioid dependency.

Restraints: High treatment costs and inconsistent reimbursement policies limiting advanced therapy access

One of the limitations that affect the pain management industry is the high cost associated with the advanced medical devices that make the treatment approach costly and unaffordable for a number of people around the world. For example, advanced treatments like neuromodulation medical devices, regenerative medicine, and biologics can be expensive not only due to the initial expenses but also in terms of maintaining them, since there are no clear reimbursement policies for such treatments.

This challenge is quite significant, particularly in low- and middle-income countries, because healthcare infrastructure and insurance coverage are quite less developed, and hence the adoption of innovative pain management solutions is not widespread. Patients in these markets often remain dependent on lower-cost generic medications even when newer, more targeted therapies could offer superior clinical outcomes, creating a persistent treatment access gap between developed and developing healthcare systems.

Opportunities: Biologics innovation and AI-integrated precision treatment creating expanded pain management market categories

The market also benefits from expanding applications of regenerative medicine, such as stem cell therapies, for the treatment of musculoskeletal pain. Rapid advancements in biologics and personalized medicine are driving innovation in the pharmaceuticals segment, with recent regulatory approvals and collaborations reshaping the market landscape as biologic-based solutions increase market presence across multiple chronic pain indications beyond migraine, including emerging applications in chronic back pain and post-surgical pain management.

Pain management systems are now AI-integrated, which allows for precision treatment and monitoring, creating new opportunity for vendors capable of demonstrating measurable improvement in treatment personalization and patient outcome tracking. As more therapies move toward targeted, mechanism-specific intervention rather than broad symptomatic relief, vendors with strong biologics pipelines stand to capture disproportionate growth within the broader pain management category, particularly as payers increasingly demand outcomes data justifying premium pricing for these advanced treatment modalities.

Recent Developments:

-

2024: The FDA approved a novel monoclonal antibody therapy for chronic migraine, marking an increase in biologic-based pain management solutions entering the U.S. market.

-

2023: Pfizer Inc. received U.S. FDA approval for ZAVZPRET, a nasal spray and the first calcitonin gene-related peptide receptor antagonist for acute treatment of migraines with or without aura in adults.

-

2023: Janssen Pharmaceuticals, a subsidiary of Johnson & Johnson, received European Commission conditional marketing authorization for TALVEY as a monotherapy treatment for relapsed and refractory multiple myeloma patients.

Pain Management Market Key Players are:

-

Pfizer Inc.

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Eli Lilly and Company

-

Teva Pharmaceutical Industries Ltd.

-

Abbott Laboratories

-

Boston Scientific Corporation

-

Medtronic plc

-

GlaxoSmithKline plc

-

Novartis AG

-

Sanofi S.A.

-

AbbVie Inc. (Allergan)

-

AstraZeneca plc

-

Bayer AG

-

Purdue Pharma L.P.

-

Endo Pharmaceuticals Inc.

-

Zogenix Inc.

-

Takeda Pharmaceutical Company Limited

-

Merck & Co. Inc.

-

Bristol Myers Squibb Company

-

Nevro Corp.

Pain Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 79.97 Billion |

| Market Size by 2035 | USD 124.02 Billion |

| CAGR | CAGR of 4.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Non-Steroidal Anti-Inflammatory Drugs, Anticonvulsants, Sedatives, Narcotics, Antimigraine Specialists, Antidepressants, Others) • By Indication (Neuropathic Pain, Cancer Pain, Facial Pain and Migraine, Musculoskeletal Pain, Fibromyalgia, Chronic Back Pain, Joint Pain, Headache, Post-Operative Pain) • By Mode of Purchase (Over-the-Counter, Prescription-Based) • By End-User (Hospitals & Clinics, Pharmaceutical Companies, Medical Device Companies, Research & Academic Institutions, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., Johnson & Johnson (Janssen Pharmaceuticals), Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., Abbott Laboratories, Boston Scientific Corporation, Medtronic plc, GlaxoSmithKline plc, Novartis AG, Sanofi S.A., AbbVie Inc. (Allergan), AstraZeneca plc, Bayer AG, Purdue Pharma L.P., Endo Pharmaceuticals Inc., Zogenix Inc., Takeda Pharmaceutical Company Limited, Merck & Co. Inc., Bristol Myers Squibb Company, and Nevro Corp. |

Frequently Asked Questions

The Pain Management Market is expected to grow at a CAGR of 4.49% from 2026 to 2035.

The Pain Management Market was valued at USD 79.97 Billion in 2025.

Increasing prevalence of chronic pain conditions, a growing geriatric population, shift toward non-opioid and minimally invasive therapies, and advancements in biologics and AI-integrated pain management technologies are the primary growth factors sustaining continued market expansion across both developed and emerging healthcare markets.

NSAIDs dominated the market with a 34% share in 2025 through efficacy, cost-effectiveness, and availability.

North America dominated the market in 2025 through advanced healthcare systems and significant research investment.

Get in Touch