Virtual Networking Market Report Scope & Overview:

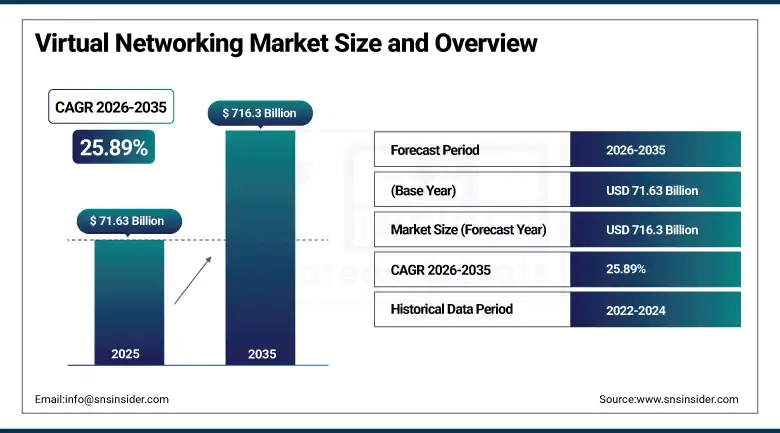

The Virtual Networking Market was valued at USD 71.63 Billion in 2025 and is expected to reach USD 716.3 Billion by 2035, growing at a CAGR of 25.89% from 2026–2035.

The global virtual networking market is advancing at an exceptional pace as enterprises, telecommunications carriers, and cloud providers systematically replace hardware-centric network infrastructure with software-defined, virtualized networking architectures whose programmability, automation, and cloud-native scalability create operational agility and cost efficiency that physical network infrastructure cannot match at equivalent scale. Virtual networking encompasses the full spectrum of software-based network abstraction technologies, from software-defined networking whose centralized control plane separates network intelligence from data plane hardware, through network function virtualization that deploys firewalls, load balancers, and routers as software on commercial servers rather than dedicated appliances, to SD-WAN whose intelligent traffic management optimizes application performance across hybrid WAN environments. Enterprise cloud adoption creating multi-cloud connectivity requirements, remote workforce expansion creating VPN and ZTNA demand, and 5G network infrastructure’s virtualization mandating NFV deployment.

In 2024, Cisco Systems launched its Catalyst SD-WAN platform enhancements incorporating AI-powered network operations that automatically detect and remediate application performance degradations without human intervention, reducing mean time to resolution for enterprise WAN incidents by 85% compared to conventional rule-based monitoring approaches. The capability demonstrated Cisco’s strategy of embedding autonomous network operations intelligence within SD-WAN infrastructure whose self-healing behavior creates operational efficiency gains that justify platform investment above the connectivity cost reduction that SD-WAN’s bandwidth economics provide versus dedicated MPLS WAN alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 90.17 Billion

-

Market Size by 2035: USD 716.3 Billion

-

CAGR: 25.89% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Virtual Networking Market - Request Free Sample Report

Virtual Networking Market Trends

-

AI-powered network operations automation is enabling self-healing virtual networks that detect and remediate performance issues without human intervention.

-

Zero Trust Network Access is replacing conventional VPN architectures by providing identity-verified application-level access without exposing network segments to authenticated users.

-

5G core network virtualization using cloud-native NFV is enabling mobile operators to deploy network slicing for different service quality requirements on shared infrastructure.

-

Multi-cloud networking platforms are enabling enterprises to manage consistent security policies and connectivity across AWS, Azure, and Google Cloud simultaneously.

-

Edge computing network virtualization is extending software-defined networking capabilities from centralized data centres to distributed edge infrastructure for latency-sensitive applications.

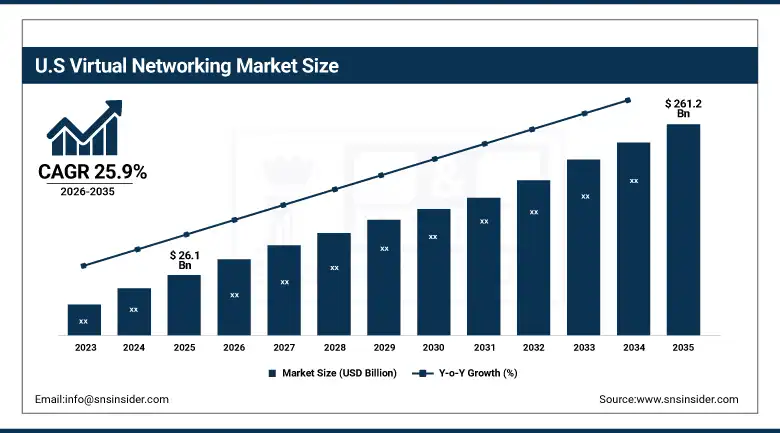

The U.S. Virtual Networking Market Outlook

The U.S. Virtual Networking Market was valued at approximately USD 26.1 Billion in 2025 and is expected to reach approximately USD 261.2 Billion by 2035, growing at a CAGR of approximately 25.9%.

The United States leads North American virtual networking revenues through the world’s highest enterprise cloud adoption rate, the most extensive SD-WAN deployment base across retail, financial services, and healthcare sectors, and the concentration of virtual networking technology leaders including Cisco, VMware by Broadcom, Juniper Networks, and Palo Alto Networks whose innovation investment defines global market capability. The federal government’s Zero Trust Architecture mandate under OMB M-22-09 creates structured government procurement of ZTNA and virtual networking solutions across civilian and defense agencies.

In 2023, VMware by Broadcom launched VMware NSX enhancements providing AI-assisted micro-segmentation policy generation that automatically creates network security zones based on observed workload communication patterns without requiring manual policy authoring. The enhancement addressed the principal operational barrier to NSX micro-segmentation deployment, where the manual effort of defining tens of thousands of security policy rules for complex multi-tier application environments created implementation timelines of months that enterprises whose dynamic cloud workloads change continuously found impractical to maintain without automation assistance.

Virtual Networking Market Segment Analysis

-

By Component, solutions segment dominated the virtual networking market with the largest share in 2025, while services are growing rapidly as implementation complexity and managed virtual networking services create sustained professional engagement.

-

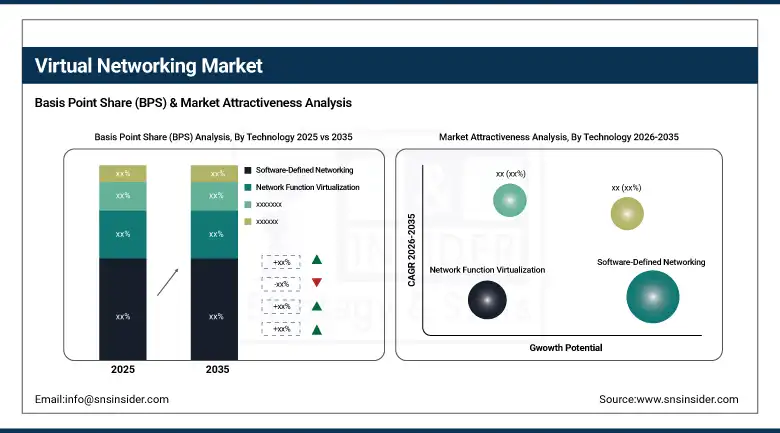

By Technology, software-defined networking segment dominated the virtual networking market with approximately 42% market share in 2025 through enterprise data centre adoption, while SD-WAN segment is projected to register the fastest CAGR of around 24.5% during 2026–2035 driven by hybrid WAN and cloud connectivity demand.

-

By Deployment, cloud-based segment dominated the virtual networking market with the largest share in 2025 and is also the fastest growing, driven by cloud-native virtual networking services eliminating on-premise hardware investment.

-

By End User, IT & Telecom segment dominated the virtual networking market with the largest share in 2025 through carrier NFV and enterprise network virtualization, while the Healthcare segment is growing rapidly driven by telemedicine connectivity and EHR network security requirements.

By Technology, SDN dominates, SD-WAN grows fastest

Software-Defined Networking retained the dominant technology position with the largest share of the virtual networking market in 2025. SDN’s commercial primacy reflects its foundational adoption across enterprise data centres and cloud provider infrastructure, where the separation of network control and data planes creates programmable network infrastructure whose automated configuration, traffic policy enforcement, and topology management capabilities substantially reduce the operational complexity and human error risk of conventional individually managed network device deployments. Enterprise data centre SDN deployments using VMware NSX, Cisco ACI, and Juniper Contrail create software-defined network fabrics whose microsecond-precision traffic management, automated security zone creation, and workload-following policy mobility enable the application portability and network security granularity that multi-tenant cloud-native architectures require across hybrid enterprise infrastructure.

SD-WAN is growing fastest because the hybrid WAN connectivity requirements of enterprises operating across multiple cloud providers, branch offices, and remote workforce locations create management complexity and cost inefficiency in legacy MPLS WAN architectures that SD-WAN’s application-aware traffic steering, cloud-native connectivity, and centralized management platform address cost-effectively. Each enterprise that replaces dedicated MPLS circuits with SD-WAN over broadband internet connections achieves 40 to 60% WAN connectivity cost reduction while improving cloud application performance through direct cloud breakout capability.

By End User, IT & Telecom dominates, healthcare grows fastest

IT and telecommunications retained the dominant end-user position with the largest share of the virtual networking market in 2025. Telecommunications carriers’ systematic NFV deployment for virtualizing network functions including EPC, IMS, and edge computing in 5G core network architecture creates the most commercially significant single virtual networking procurement category. Enterprise IT’s progressive SD-WAN, SDN, and ZTNA adoption across their distributed network infrastructure creates consistent above-GDP technology procurement growth. The IT and telecom sector’s role as both the infrastructure provider enabling other sectors’ virtual networking and the direct end-user of virtual networking for its own network operations sustains the segment’s revenue leadership.

Healthcare is growing fastest because the combination of telemedicine infrastructure investment creating secure high-bandwidth clinical video connectivity requirements, electronic health record system network security demands whose HIPAA compliance obligations specify detailed access control and encryption, and medical IoT device proliferation creating network segmentation requirements collectively create growing virtual networking investment across hospital networks, health system data centres, and telehealth platforms. Each health system deploying zero trust network access for clinical staff remote EHR access and each hospital implementing network microsegmentation to isolate medical device networks from clinical IT infrastructure creates healthcare virtual networking procurement.

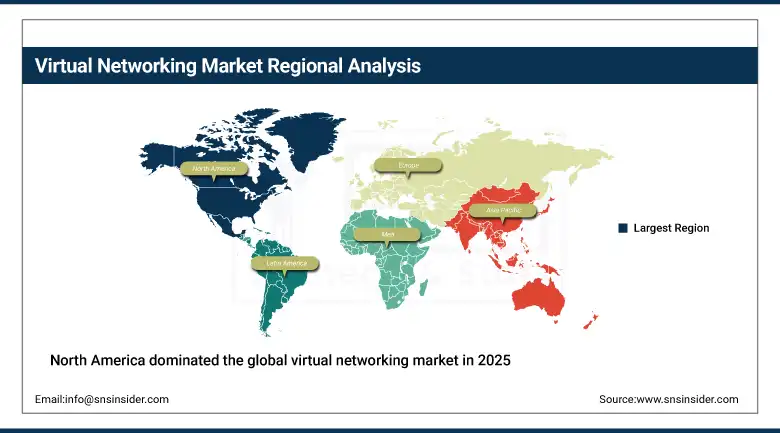

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Virtual Networking Market Insights

North America dominated the global virtual networking market in 2025, driven by the highest enterprise cloud adoption rate, the most extensive SD-WAN deployment base, and the concentration of virtual networking technology leaders. The United States accounts for approximately 82.5% of North American revenues through Cisco’s SD-WAN and SDN commercial leadership, VMware NSX’s enterprise data centre dominance, and Palo Alto Networks’ ZTNA market position. The federal Zero Trust Architecture mandate is creating structured government virtual networking procurement above commercial enterprise adoption.

Canada contributes supplementary North American revenues through its growing enterprise cloud adoption, the financial services sector’s SD-WAN deployment for branch connectivity optimization, and the government’s progressive adoption of ZTNA for public sector network security. Canadian telecommunications carriers’ 5G core NFV deployment creates network virtualization procurement aligned with commercial enterprise SD-WAN investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Virtual Networking Market Insights

Europe is a significant virtual networking market where GDPR’s data protection requirements create demand for virtual networking solutions with granular traffic visibility, encryption compliance, and cross-border data flow control capabilities that software-defined network policy management efficiently provides. Germany accounts for approximately 22.4% of European revenues through its large enterprise technology sector’s SD-WAN adoption, the automotive industry’s connected factory network virtualization, and Deutsche Telekom’s NFV-based 5G core deployment.

The United Kingdom’s financial services sector’s ZTNA investment, France’s enterprise cloud-first strategy creating SD-WAN demand, and the EU’s NIS2 Directive network security requirements collectively sustain European virtual networking market development. Pan-European telecommunications carriers’ network virtualization programmes create large carrier-grade NFV procurement that sustains European regional market scale above enterprise-only consumption.

Asia Pacific Virtual Networking Market Insights

Asia Pacific is the fastest-growing regional virtual networking market, driven by 5G infrastructure rollout’s NFV requirements across China, Japan, South Korea, and India, rapid enterprise cloud adoption creating SD-WAN demand, and government digital transformation programmes creating institutional virtual networking procurement. China accounts for approximately 44.8% of Asia Pacific revenues through its massive 5G deployment whose virtualized core network architecture creates domestic NFV procurement at global scale.

India is the most commercially dynamic emerging market within Asia Pacific, where the telecommunications sector’s 5G expansion, rapidly growing enterprise cloud adoption, and IT industry’s SD-WAN deployment for distributed workforce connectivity collectively create above-regional-average virtual networking growth. South Korea’s advanced 5G network and Japan’s enterprise SD-WAN adoption contribute premium secondary regional demand.

MEA & Latin America Virtual Networking Market Insights

The UAE leads MEA revenues through its technology-forward enterprise digital transformation, the government’s smart city network infrastructure investment, and the telecommunications sector’s advanced 5G virtualized network deployment. Saudi Arabia’s Vision 2030 digital infrastructure investment creates growing NFV and SD-WAN procurement across government and enterprise sectors.

Brazil leads Latin American revenues through its large enterprise technology sector’s SD-WAN adoption, the telecommunications sector’s progressive network virtualization investment, and the financial services industry’s ZTNA deployment. Mexico and Colombia contribute growing secondary demand through enterprise digital transformation and carrier network modernization investment.

Market Dynamics

Growth Drivers: Enterprise cloud migration creating SD-WAN connectivity demand and 5G network virtualization mandating carrier NFV infrastructure investment

The virtual networking market’s exceptional growth is driven by the structural alignment between enterprise cloud adoption’s WAN connectivity requirements and SD-WAN’s architecture whose cloud-native connectivity and application-aware traffic management directly solve the performance and cost challenges that cloud migration creates for legacy MPLS WAN networks. Each enterprise that migrates workloads to cloud platforms creates SD-WAN adoption motivation whose WAN cost reduction, cloud application performance improvement, and centralized management efficiency together justify platform investment. The global SD-WAN market’s expanding beyond WAN replacement into secure access service edge creates a virtual networking platform whose cloud-delivered security and connectivity convergence expands addressable market well beyond conventional WAN management scope.

5G carrier network virtualization creates the most commercially significant single virtual networking demand category, where each 5G core network deployed on cloud-native NFV infrastructure creates hundreds of millions of dollars of virtual networking software and platform procurement from the carrier’s technology suppliers. The global 5G infrastructure investment cycle, whose annual capex exceeds USD 200 billion across all carriers combined, creates consistent above-market virtual networking procurement growth whose commercial scale is independent of enterprise digital transformation investment cycles whose discretionary spending fluctuates with economic conditions.

Restraints: Network performance and latency concerns in virtualized environments and skilled professional shortage constraining enterprise virtual networking deployment velocity

Software-defined network and NFV deployments’ computational overhead from hypervisor processing of network functions that dedicated hardware ASICs perform at lower latency creates performance limitations for time-sensitive network applications including industrial real-time control, financial trading, and ultra-reliable low-latency communications whose network requirements exceed what current general-purpose server NFV can deliver at cost-competitive economics. Each enterprise network application whose latency sensitivity creates ASIC hardware specification preference represents a virtual networking adoption limitation whose resolution depends on continued server CPU performance improvement and NFV platform optimization progress.

Network engineering talent shortage in SDN, NFV, and SD-WAN creates implementation quality risk, deployment timeline extension, and ongoing operational risk for organizations deploying virtual networking without sufficient in-house expertise to design, configure, and troubleshoot software-defined network environments whose operational complexity differs substantially from the CLI-managed hardware networks that the existing network engineering workforce was trained to operate.

Opportunities: ZTNA adoption as VPN replacement and network-as-a-service creating high-growth virtual networking commercial frontiers

Zero Trust Network Access’s progressive replacement of conventional VPN as the enterprise remote access standard represents the most commercially significant near-term virtual networking opportunity. Each enterprise that migrates from VPN to ZTNA eliminates the implicit trust of network-level access that VPN architecture provides in favor of identity-verified, application-level access whose granularity prevents the lateral movement that VPN-based breaches typically enable. The documented superiority of ZTNA’s security architecture combined with its improved application performance and management simplicity creates compelling migration motivation whose adoption is progressively supported by corporate cyber insurance requirements for zero trust implementation.

Network-as-a-service delivery models, where virtual networking is consumed as cloud-delivered services with per-user or per-site subscription pricing rather than capital investment in network hardware and software, represent a commercial model transformation creating above-market growth in accessible addressable market by enabling SME and mid-market enterprise adoption at economics that traditional network infrastructure investment prevented. Each NaaS provider whose cloud-delivered SD-WAN, firewall, and connectivity services eliminate hardware procurement and network engineering requirements creates a growing addressable enterprise customer base.

Recent Developments:

-

2024: Cisco launched Catalyst SD-WAN platform enhancements incorporating AI-powered network operations that automatically detect and remediate application performance degradations, reducing enterprise WAN incident mean time to resolution by 85% versus conventional rule-based monitoring approaches.

-

2023: VMware by Broadcom launched NSX enhancements with AI-assisted micro-segmentation policy generation that automatically creates network security zones based on observed workload communication patterns, eliminating manual policy authoring for complex multi-tier application environments.

-

2023: Juniper Networks launched its AI-Native Networking Platform integrating Mist AI’s self-driving network operations across wireless, wired, and SD-WAN networking domains, enabling enterprises to manage converged network infrastructure through a unified AI-powered operations platform.

Virtual Networking Market Key Players are:

-

Cisco Systems Inc. (SD-WAN, ACI)

-

VMware Inc. (NSX, VeloCloud)

-

Juniper Networks Inc. (Mist, Contrail)

-

Huawei Technologies Co. Ltd.

-

Nokia Corporation (Nuage Networks)

-

Palo Alto Networks Inc. (Prisma)

-

Fortinet Inc.

-

Aruba Networks (HPE)

-

Ericsson AB

-

NEC Corporation

-

Broadcom Inc.

-

Microsoft Corporation (Azure Virtual Network)

-

Amazon Web Services Inc. (AWS VPC)

-

Google LLC (Google Cloud VPC)

-

Oracle Corporation (OCI Networking)

-

Zscaler Inc.

-

Cato Networks Ltd.

-

Versa Networks Inc.

-

Ribbon Communications Inc.

-

Aviatrix Systems Inc.

Virtual Networking Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 71.63 Billion |

| Market Size by 2035 | USD 716.3 Billion |

| CAGR | CAGR of 25.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Technology (Software-Defined Networking, Network Function Virtualization, Virtual Private Network, SD-WAN, Network Virtualization Platform, Others) • By Deployment (Cloud-Based, On-Premise, Hybrid) • By End User (IT & Telecom, BFSI, Healthcare, Government & Defense, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cisco Systems Inc. (SD-WAN, ACI), VMware Inc. (NSX, VeloCloud), Juniper Networks Inc. (Mist, Contrail), Huawei Technologies Co. Ltd., Nokia Corporation (Nuage Networks), Palo Alto Networks Inc. (Prisma), Fortinet Inc., Aruba Networks (HPE), Ericsson AB, NEC Corporation, Broadcom Inc., Microsoft Corporation (Azure Virtual Network), Amazon Web Services Inc. (AWS VPC), Google LLC (Google Cloud VPC), Oracle Corporation (OCI Networking), Zscaler Inc., Cato Networks Ltd., Versa Networks Inc., Ribbon Communications Inc., and Aviatrix Systems Inc. |

Frequently Asked Questions

The Virtual Networking Market is expected to grow at a CAGR of 25.89% from 2026 to 2035.

The Virtual Networking Market was valued at USD 71.63 Billion in 2025.

Enterprise cloud migration creating SD-WAN connectivity demand, 5G network virtualization mandating carrier NFV investment, ZTNA replacing conventional VPN for enterprise remote access, and network-as-a-service enabling SME virtual networking adoption are the primary growth factors.

The Software-Defined Networking segment dominated with the largest share in 2025.

North America dominated the Virtual Networking Market in 2025 through the highest enterprise cloud adoption rate.

Get in Touch