Get More Information on Wafer Process Control Equipment Market - Request Sample Report

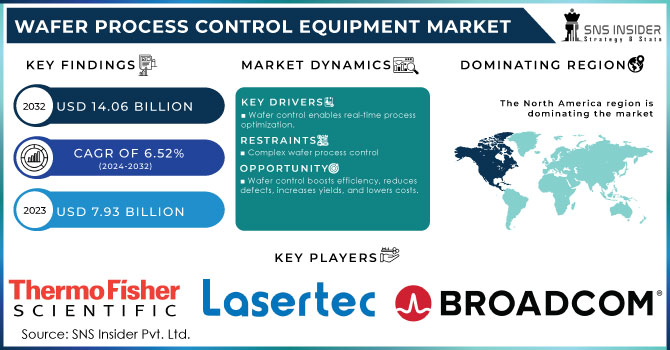

The Wafer Process Control Equipment Market Size was valued at USD 7.93 billion in 2023 and is estimated to reach USD 14.06 billion by 2032 and grow at a CAGR of 6.52% over the forecast period 2024-2032

The increasing need for enhanced production efficiency and quality in the semiconductor manufacturing sector is fueling the growth of the wafer process control equipment market. This tool allows semiconductor manufacturers to effectively optimize their production processes through real-time monitoring and control of manufacturing parameters. The recent euro 135 million investment underlines the increased demand for advanced wafer process control equipment as chip manufacturing becomes more intricate, particularly with the shift towards smaller, more advanced chips for AI applications, pushing traditional quality control methods to their limits. This leads to a disruption in the semiconductor supply chain, requiring creative solutions. The substantial funding secured by the company from investors in both the US and Asia highlights the global recognition of the critical role of wafer process control in modern chip manufacturing. Despite the challenges of increasing production yields and meeting strict quality standards, the industry is poised for significant growth in the market for precise measurement and inspection equipment. With the United States being a leader in semiconductor technology and having made substantial investments in the industry, there is evident opportunity for collaborations between US and European companies.

The semiconductor sector is currently going through a transformative period, mainly due to rising investments in manufacturing capacities. The American semiconductor company is emphasizing the trend by deciding to construct a new facility in Penang, Malaysia, specifically for producing wafer fabrication equipment. The important role of wafer process control equipment in modern chip manufacturing is underscored by the prestigious customers of the company, which include TSMC, Samsung Electronics, and STMicroelectronics. Malaysia is working on strategic plans like the New Industrial Masterplan 2030 and the National Semiconductor Strategy to become a key player in the global semiconductor industry, attracting investments reaching a sum of MYR 587.5 billion (equivalent to US$ 126.3 billion) by the year 2030. These advancements together help drive the growth of the wafer process control equipment market, as the sector aims for increased production yields, enhanced chip quality, and technological progress.

| Report Attributes | Details |

|---|---|

| Key Segments | • By Product Type (Process Control Equipment, Inspection Equipment And Metrology Equipment) • By Application (Foundries, IDMS & Memory Manufactures) |

| Regional Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, ASM Technologies, NXP Semiconductor, Lasertec Corporation,Toray Engineering, Brodcom Inc, KLA Corporation, ASML Holding NV, Hitachi High-Tech Corporation, Applied Materials |

KEY DRIVERS:

Wafer process control equipment facilitates real-time monitoring and adjusting of manufacturing parameters, enabling the optimization of production processes.

The semiconductor industry is characterized by fierce competition and rapid technological progress. Wafer process control equipment is becoming increasingly important for manufacturers to improve production yields and guarantee the production of high-quality chips that are essential for powering modern electronic devices. Specialized equipment like photolithography is exemplified by companies such as ASML due to their dominance in the field. Yet, the industry is faced with challenges due to the intricate geopolitical landscape, as seen in US export controls aimed at China. China's ambitious aim to achieve 70% self-reliance in chips by 2025, despite significant investments in research and development, demonstrates the significant challenges in attaining technological autonomy. The continuous dependence on imports, which amount to approximately USD 400 billion per year, highlights the worldwide interconnection of the semiconductor supply chain and the crucial role of wafer process control equipment in this intricate system.

The cost-effectiveness and quality enhancements enabled by wafer process control equipment boost semiconductor manufacturers' competitiveness in the market.

RESTRAIN:

The intricate nature of wafer process control systems, including their advanced technologies and procedures, may be difficult for manufacturers without the necessary specialized expertise for implementation and operation.

Establishing and upholding wafer process control systems can be expensive, presenting a financial obstacle for semiconductor manufacturers, particularly smaller companies. These systems involve complex technologies and processes, requiring specific skills for successful setup and management, which may be difficult for some manufacturers. Furthermore, the complexity lies in ensuring compatibility with current manufacturing systems and equipment, which could lead to interoperability problems and disruptions in production processes. The semiconductor sector, a crucial element of contemporary technology, is becoming more of a battleground in global politics. Huawei's 7nm chip, manufactured by SMIC, represents China's advancements in chip production, while highlighting the challenges of international supply chains and knowledge sharing. Although China has made significant progress in some types of equipment, its lack of core technologies and excessive dependence on government interference are obstacles to achieving semiconductor independence. On the other hand, the US, previously a leading competitor, is rejuvenating its semiconductor sector with measures such as the CHIPS Act in response to China's aspirations. As countries compete for technological dominance, the market for wafer process control equipment becomes crucial in shaping the effectiveness, quality, and competitiveness of semiconductor production worldwide.

Managing significant amounts of sensitive production data in wafer process control systems raises worries about data security and privacy, requiring strong cyber security measures to address risks.

OPPORTUNITY:

Wafer process control systems enhance production efficiency by optimizing processes and reducing defects, resulting in higher yields and lower costs.

Wafer process control systems drive improved production efficiency by optimizing processes and minimizing defects, resulting in higher yields and reduced costs. Additionally, these systems enable real-time monitoring and adjustment of manufacturing parameters, ensuring consistent product quality and reliability.

Combining wafer process control with Industry 4.0 efforts facilitates seamless connectivity and data sharing, supporting predictive maintenance, remote monitoring, and other intelligent manufacturing techniques.

The integration of wafer process control with Industry 4.0 principles is bringing about a fundamental change in semiconductor manufacturing. Through incorporating technologies such as IoT, AI, and advanced analytics, manufacturers can improve production processes, elevate quality control, and realize substantial cost savings. This integration allows for monitoring in real-time, maintenance predictions, and decision-making based on data, resulting in higher efficiency and flexibility in the end. The larger Industry 4.0 environment, highlighted by firms such as GM, is experiencing fast expansion, with forecasts showing a significant rise in spending in the coming years. The future of chip manufacturing will be shaped by the synergy of wafer process control and Industry 4.0 as the semiconductor industry evolves.

CHALLENGES:

Implementing and keeping up wafer process control systems can be costly, especially for smaller semiconductor manufacturers, creating financial difficulty.

Implementing and maintaining wafer process control systems can incur significant costs, presenting financial obstacles for semiconductor manufacturers, especially smaller firms. Additionally, the complexity of these systems, with their intricate technologies and processes, demands specialized expertise for effective implementation and operation, posing challenges for certain manufacturers.

Ensuring compatibility and integration with current manufacturing systems and equipment can be intricate, causing potential disruptions in production workflows due to interoperability issues.

The conflict between Russia and Ukraine poses significant challenges for the wafer process control market across various equipment segments. Disruptions in the supply chain may cause delays or shortages in essential components for manufacturing process control equipment. Heightened geopolitical tensions could also influence investment decisions, potentially slowing the adoption of innovative technologies. Uncertainty from the conflict may prompt reassessment of purchasing decisions for inspection and metrology equipment among foundries, IDMS, and memory manufacturers. This could lead to delays or alterations in procurement plans as companies navigate economic instability and evaluate their need for high-cost solutions. Overall, the conflict introduces complexities and uncertainties, requiring stakeholders to closely monitor developments and adapt their strategies to mitigate risks and capitalize on emerging opportunities in the evolving geopolitical landscape.

An economic slowdown in the wafer process control market signifies a period of reduced growth or decline in the industry's economic activity. This slowdown can stem from various factors such as demand fluctuations, geopolitical tensions, supply chain disruptions, and shifts in market dynamics. During such times, semiconductor manufacturers might postpone investments in new equipment or technology upgrades, resulting in lower demand for wafer process control solutions. Moreover, uncertainties in the global economy could impact consumer spending, affecting the demand for electronic devices and semiconductor products, indirectly affecting the need for process control equipment. Consequently, companies in the wafer process control market face challenges and must adjust their strategies to navigate the downturn and position themselves for future growth.

By Product Type

In 2023, Wafer Process Control Equipment Market was led by Inspection equipment, holding a 39% share based on product type. Playing a crucial role in guaranteeing the quality and integrity of semiconductor manufacturing process, driving revenue in the market. With advancements in semiconductor technology, it is becoming more crucial to have accurate inspection methods to detect defects and abnormalities in smaller and more intricate components. Tools for inspection such as optical and electron microscopes provide detailed imaging that allows for the identification of small flaws which may impact the functioning of integrated circuits.

By Application

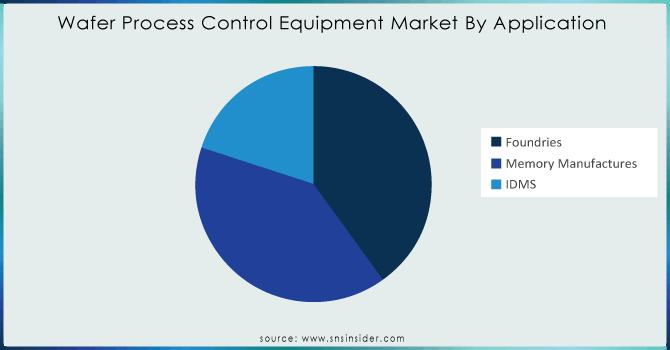

In 2023, foundries held a 38% share of the wafer process control equipment market. Foundries are at the forefront of the market due to their essential role in semiconductor production. These dedicated facilities manufacture integrated circuits for different semiconductor companies, requiring precise process control to maintain uniform quality in their wafers. TSMC and Samsung are in control of the market for wafer processing equipment. Stringent quality control is necessary because of their important function in the production of semiconductors. The significance of wafer process control equipment is in its function of monitoring and enhancing critical production steps like wafer processing and etching. In these foundries, the implementation of advanced process control technologies is motivated by the desire for increased yields and operational efficiency.

Get Customized Report as per Your Business Requirement - Request For Customized Report

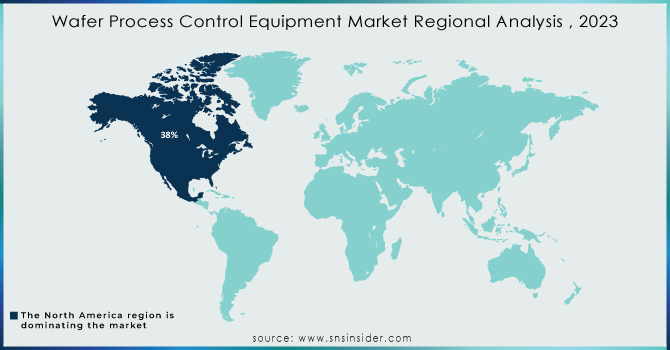

In 2023, North America holds the largest market share in wafer process control equipment worldwide, with a 38% dominance. This leadership is powered by a strong network of major semiconductor companies such as Intel and Applied Materials, along with top-tier research institutions. The area's dedication to technological progress leads to a continual need for state-of-the-art process control solutions to maintain high quality in chip production.

In the wafer process control equipment market, Europe is emerging as a significant competitor, with a 22% market share in 2023 and demonstrating the highest rate of growth. Germany plays a significant role in semiconductor research and development, having a powerful impact in the field. Contrary to popular belief, the UK is experiencing rapid market growth as a result of increased investments in advanced electronics and semiconductor technologies. Europe's cooperation in this sector positions it as a major player in the global wafer process control industry.

The Asia-Pacific Wafer Process Control Equipment Market is expected to experience the fastest compound annual growth rate (CAGR) from 2023 to 2031. This rise is attributed to the region's focus on semiconductor research and development and the increasing demand for advanced electronics. Additionally, China dominates the market with the largest share, while India shows the fastest growth in the Asia-Pacific region for Wafer Process Control Equipment Equipment.

Some of the major players in the Wafer Process Control Equipment Thermo Fisher Scientific, ASM Technologies, NXP Semiconductor, Lasertec Corporation,Toray Engineering, Brodcom Inc, KLA Corporation, ASML Holding NV, Hitachi High-Tech Corporation, Applied Materials and Others players

In October 2023, KLA Corporation, a US-based manufacturer specializing in wafer inspection and metrology equipment, completed the acquisition of Lam Research Corporation, also a US-based manufacturer known for its wafer etching equipment, in a deal valued at $10.5 billion. This acquisition positions the combined entity as the world's largest manufacturer of semiconductor capital equipment

In August 2023, Applied Materials, Inc. and TSMC a prominent Taiwanese semiconductor manufacturer, entered into a partnership agreement aimed at collaborating on the development and commercialization of next-generation wafer process control equipment. Leveraging their respective expertise, the two companies will work together to create advanced equipment that will support TSMC in maintaining its status as the world's largest contract chip manufacturer.

| Report Attributes | Details |

| Market Size in 2023 | US$ 7.93 Billion |

| Market Size by 2032 | US$ 14.06 Billion |

| CAGR | CAGR of 6.52% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Drivers | • Wafer process control equipment facilitates real-time monitoring and adjusting of manufacturing parameters, enabling the optimization of production processes. • The cost-effectiveness and quality enhancements enabled by wafer process control equipment boost semiconductor manufacturers' competitiveness in the market. |

| Challenges | • Implementing and keeping up wafer process control systems can be costly, especially for smaller semiconductor manufacturers, creating financial difficulty. • Ensuring compatibility and integration with current manufacturing systems and equipment can be intricate, causing potential disruptions in production workflows due to interoperability issues. |

Ans: The Wafer Process Control Equipment Market is expected to grow at a CAGR of 6.52%.

Ans: Wafer Process Control Equipment Market size was USD 7.93 billion in 2023 and is expected to Reach USD 14.06 billion by 2032.

Ans: Wafer process control equipment facilitates real-time monitoring and adjusting of manufacturing parameters, enabling the optimization of production processes.

Ans: Wafer process control systems' complexity, with their advanced technologies and procedures, can challenge manufacturers lacking the specialized expertise required for implementation and operation.

Ans: The North America region leads the Wafer Process Control Equipment market due to its significant presence and leadership in semiconductor research, development, and manufacturing.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Wafer Process Control Equipment Market Segmentation, By Product Type

7.1 Introduction

7.2 Process Control Equipment

7.3 Inspection Equipment

7.4 Metrology Equipment

8. Wafer Process Control Equipment Market Segmentation, By Application

8.1 Introduction

8.2 Foundries

8.3 Memory Manufactures

8.4 IDMS

9. Regional Analysis

9.1 Introduction

9.2 North America

9.2.1 Trend Analysis

9.2.2 North America Wafer Process Control Equipment Market by Country

9.2.3 North America Wafer Process Control Equipment Market By Product Type

9.2.4 North America Wafer Process Control Equipment Market By Application

9.2.5 USA

9.2.5.1 USA Wafer Process Control Equipment Market By Product Type

9.2.5.2 USA Wafer Process Control Equipment Market By Application

9.2.6 Canada

9.2.6.1 Canada Wafer Process Control Equipment Market By Product Type

9.2.6.2 Canada Wafer Process Control Equipment Market By Application

9.2.7 Mexico

9.2.7.1 Mexico Wafer Process Control Equipment Market By Product Type

9.2.7.2 Mexico Wafer Process Control Equipment Market By Application

9.3 Europe

9.3.1 Trend Analysis

9.3.2 Eastern Europe

9.3.2.1 Eastern Europe Wafer Process Control Equipment Market by Country

9.3.2.2 Eastern Europe Wafer Process Control Equipment Market By Product Type

9.3.2.3 Eastern Europe Wafer Process Control Equipment Market By Application

9.3.2.4 Poland

9.3.2.4.1 Poland Wafer Process Control Equipment Market By Product Type

9.3.2.4.2 Poland Wafer Process Control Equipment Market By Application

9.3.2.5 Romania

9.3.2.5.1 Romania Wafer Process Control Equipment Market By Product Type

9.3.2.5.2 Romania Wafer Process Control Equipment Market By Application

9.3.2.6 Hungary

9.3.2.6.1 Hungary Wafer Process Control Equipment Market By Product Type

9.3.2.6.2 Hungary Wafer Process Control Equipment Market By Application

9.3.2.7 Turkey

9.3.2.7.1 Turkey Wafer Process Control Equipment Market By Product Type

9.3.2.7.2 Turkey Wafer Process Control Equipment Market By Application

9.3.2.8 Rest of Eastern Europe

9.3.2.8.1 Rest of Eastern Europe Wafer Process Control Equipment Market By Product Type

9.3.2.8.2 Rest of Eastern Europe Wafer Process Control Equipment Market By Application

9.3.3 Western Europe

9.3.3.1 Western Europe Wafer Process Control Equipment Market by Country

9.3.3.2 Western Europe Wafer Process Control Equipment Market By Product Type

9.3.3.3 Western Europe Wafer Process Control Equipment Market By Application

9.3.3.4 Germany

9.3.3.4.1 Germany Wafer Process Control Equipment Market By Product Type

9.3.3.4.2 Germany Wafer Process Control Equipment Market By Application

9.3.3.5 France

9.3.3.5.1 France Wafer Process Control Equipment Market By Product Type

9.3.3.5.2 France Wafer Process Control Equipment Market By Application

9.3.3.6 UK

9.3.3.6.1 UK Wafer Process Control Equipment Market By Product Type

9.3.3.6.2 UK Wafer Process Control Equipment Market By Application

9.3.3.7 Italy

9.3.3.7.1 Italy Wafer Process Control Equipment Market By Product Type

9.3.3.7.2 Italy Wafer Process Control Equipment Market By Application

9.3.3.8 Spain

9.3.3.8.1 Spain Wafer Process Control Equipment Market By Product Type

9.3.3.8.2 Spain Wafer Process Control Equipment Market By Application

9.3.3.9 Netherlands

9.3.3.9.1 Netherlands Wafer Process Control Equipment Market By Product Type

9.3.3.9.2 Netherlands Wafer Process Control Equipment Market By Application

9.3.3.10 Switzerland

9.3.3.10.1 Switzerland Wafer Process Control Equipment Market By Product Type

9.3.3.10.2 Switzerland Wafer Process Control Equipment Market By Application

9.3.3.11 Austria

9.3.3.11.1 Austria Wafer Process Control Equipment Market By Product Type

9.3.3.11.2 Austria Wafer Process Control Equipment Market By Application

9.3.3.12 Rest of Western Europe

9.3.3.12.1 Rest of Western Europe Wafer Process Control Equipment Market By Product Type

9.3.2.12.2 Rest of Western Europe Wafer Process Control Equipment Market By Application

9.4 Asia-Pacific

9.4.1 Trend Analysis

9.4.2 Asia Pacific Wafer Process Control Equipment Market by Country

9.4.3 Asia Pacific Wafer Process Control Equipment Market By Product Type

9.4.4 Asia Pacific Wafer Process Control Equipment Market By Application

9.4.5 China

9.4.5.1 China Wafer Process Control Equipment Market By Product Type

9.4.5.2 China Wafer Process Control Equipment Market By Application

9.4.6 India

9.4.6.1 India Wafer Process Control Equipment Market By Product Type

9.4.6.2 India Wafer Process Control Equipment Market By Application

9.4.7 Japan

9.4.7.1 Japan Wafer Process Control Equipment Market By Product Type

9.4.7.2 Japan Wafer Process Control Equipment Market By Application

9.4.8 South Korea

9.4.8.1 South Korea Wafer Process Control Equipment Market By Product Type

9.4.8.2 South Korea Wafer Process Control Equipment Market By Application

9.4.9 Vietnam

9.4.9.1 Vietnam Wafer Process Control Equipment Market By Product Type

9.4.9.2 Vietnam Wafer Process Control Equipment Market By Application

9.4.10 Singapore

9.4.10.1 Singapore Wafer Process Control Equipment Market By Product Type

9.4.10.2 Singapore Wafer Process Control Equipment Market By Application

9.4.11 Australia

9.4.11.1 Australia Wafer Process Control Equipment Market By Product Type

9.4.11.2 Australia Wafer Process Control Equipment Market By Application

9.4.12 Rest of Asia-Pacific

9.4.12.1 Rest of Asia-Pacific Wafer Process Control Equipment Market By Product Type

9.4.12.2 Rest of Asia-Pacific Wafer Process Control Equipment Market By Application

9.5 Middle East & Africa

9.5.1 Trend Analysis

9.5.2 Middle East

9.5.2.1 Middle East Wafer Process Control Equipment Market by Country

9.5.2.2 Middle East Wafer Process Control Equipment Market By Product Type

9.5.2.3 Middle East Wafer Process Control Equipment Market By Application

9.5.2.4 UAE

9.5.2.4.1 UAE Wafer Process Control Equipment Market By Product Type

9.5.2.4.2 UAE Wafer Process Control Equipment Market By Application

9.5.2.5 Egypt

9.5.2.5.1 Egypt Wafer Process Control Equipment Market By Product Type

9.5.2.5.2 Egypt Wafer Process Control Equipment Market By Application

9.5.2.6 Saudi Arabia

9.5.2.6.1 Saudi Arabia Wafer Process Control Equipment Market By Product Type

9.5.2.6.2 Saudi Arabia Wafer Process Control Equipment Market By Application

9.5.2.7 Qatar

9.5.2.7.1 Qatar Wafer Process Control Equipment Market By Product Type

9.5.2.7.2 Qatar Wafer Process Control Equipment Market By Application

9.5.2.8 Rest of Middle East

9.5.2.8.1 Rest of Middle East Wafer Process Control Equipment Market By Product Type

9.5.2.8.2 Rest of Middle East Wafer Process Control Equipment Market By Application

9.5.3 Africa

9.5.3.1 Africa Wafer Process Control Equipment Market by Country

9.5.3.2 Africa Wafer Process Control Equipment Market By Product Type

9.5.3.3 Africa Wafer Process Control Equipment Market By Application

9.5.2.4 Nigeria

9.5.2.4.1 Nigeria Wafer Process Control Equipment Market By Product Type

9.5.2.4.2 Nigeria Wafer Process Control Equipment Market By Application

9.5.2.5 South Africa

9.5.2.5.1 South Africa Wafer Process Control Equipment Market By Product Type

9.5.2.5.2 South Africa Wafer Process Control Equipment Market By Application

9.5.2.6 Rest of Africa

9.5.2.6.1 Rest of Africa Wafer Process Control Equipment Market By Product Type

9.5.2.6.2 Rest of Africa Wafer Process Control Equipment Market By Application

9.6 Latin America

9.6.1 Trend Analysis

9.6.2 Latin America Wafer Process Control Equipment Market by Country

9.6.3 Latin America Wafer Process Control Equipment Market By Product Type

9.6.4 Latin America Wafer Process Control Equipment Market By Application

9.6.5 Brazil

9.6.5.1 Brazil Wafer Process Control Equipment Market By Product Type

9.6.5.2 Brazil Wafer Process Control Equipment Market By Application

9.6.6 Argentina

9.6.6.1 Argentina Wafer Process Control Equipment Market By Product Type

9.6.6.2 Argentina Wafer Process Control Equipment Market By Application

9.6.7 Colombia

9.6.7.1 Colombia Wafer Process Control Equipment Market By Product Type

9.6.7.2 Colombia Wafer Process Control Equipment Market By Application

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Wafer Process Control Equipment Market By Product Type

9.6.8.2 Rest of Latin America Wafer Process Control Equipment Market By Application

10. Company Profiles

10.1 Thermo Fisher Scientific

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 The SNS View

10.2 ASM Technologies

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 The SNS View

10.3 NXP Semiconductor

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 The SNS View

10.4 Lasertec Corporation

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 The SNS View

10.5 Toray Engineering

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 The SNS View

10.6 Brodcom Inc

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 The SNS View

10.7 KLA Corporation

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 The SNS View

10.8 ASML Holding NV

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 The SNS View

10.9 Hitachi High-Tech Corporation

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 The SNS View

10.10 Applied Materials

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 The SNS View

11. Competitive Landscape

11.1 Competitive Benchmarking

11.2 Market Share Analysis

11.3 Recent Developments

11.3.1 Industry News

11.3.2 Company News

11.3.3 Mergers & Acquisitions

12. USE Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments

By Product Type

Process Control Equipment

Inspection Equipment

Metrology Equipment

By Application

Foundries

Memory Manufactures

IDMS

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Thin-Film Encapsulation Market size was valued at USD 92.5 million in 2022 and is expected to grow to USD 384.66 million by 2030 and grow at a CAGR Of 19.5% over the forecast period of 2023-2030.

The Industrial Metrology Market size was valued at USD 14 billion in 2023 and is expected to grow to USD 23.4 billion by 2031 and grow at a CAGR of 6.6 % over the forecast period of 2024-2031.

The Hearth Market size was valued at USD 9.4 billion in 2022 and is expected to grow to USD 17.14 billion by 2030 and grow at a CAGR of 7.8 % over the forecast period of 2023-2030

The Calibration Services Market size was valued at USD 5.8 billion in 2022 and is expected to grow to USD 8.83 billion by 2030 and grow at a CAGR of 5.4% over the forecast period of 2023-2030.

The Semi-insulating silicon carbide wafer market size was valued at USD 430.3 million in 2022 and is expected to grow to USD 1753.80 million by 2030 and grow at a CAGR Of 19.3 % over the forecast period of 2023-2030.

The Thermal Systems Market size was Valued at USD 39.19 billion in 2023 and is estimated to Reach USD 48.12 billion by 2031 and grow at a CAGR of 2.60% over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd