High Temperature Silicone Cable Market Size Analysis:

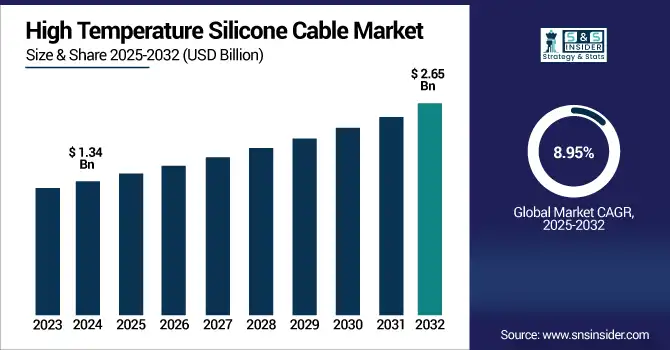

The High Temperature Silicone Cable Market size was valued at USD 1.34 billion in 2024 and is expected to reach USD 2.65 billion by 2032, growing at a CAGR of 8.95% over the forecast period of 2025-2032. High Temperature Silicone Cable Market trends are driven by increasing adoption in electric mobility and automation industries. Advancements in material technology are enhancing cable durability, flexibility, and thermal resistance performance.

To Get more information on High Temperature Silicone Cable Market - Request Free Sample Report

The global High temperature silicone cable market is projected to grow significantly with mitigation of climate change and rapid deployment of renewable energy systems, cables are increasingly required to withstand high environmental extremes conditions. Moreover, the growing stringent safety regulations with respect to industrial and commercial buildings is fuelling the adoption of flame-retardant and high-thermal-endurance cabling. Miniaturization of electronics, combined with the need for space-efficient, high-performance wiring in medical devices and instrumentation, keeps the Wire-to-Wire market in continuous growth, influencing a wide range of sectors.

As of early 2025, over 370 GW of new renewable energy capacity was added globally, according to the IEA, increasing demand for high-temperature and weather-resistant cable infrastructure.

The U.S High Temperature Silicone Cable Market size was valued at USD 0.32 billion in 2024 and is expected to reach USD 0.60 billion by 2032, growing at a CAGR of 8.36% over the forecast period of 2025-2032. U.S. High Temperature Silicone Cable Market is growing due to expanding electric vehicle manufacturing, stringent fire safety codes, industrial automation upgrades, and increasing demand for durable cabling in renewable energy and aerospace sectors.

High Temperature Silicone Cable Market Dynamics:

Drivers:

-

Rising Demand for Heat-Resistant Wiring Drives Growth in Automotive, Aerospace, and Industrial Silicone Cable Market

The global High Temperature Silicone Cable Market growth is mainly driven by increasing demand for dependable, heat-resistant wiring because of its applications in critical sectors such as automotive, aerospace, and energy. Extreme temperatures can seriously affect the performance integrity of electric vehicle cables and those used in the growing field of industrial automation, both of which require cables able to withstand and continue performing in such extreme environments. Additionally, a growing focus on regulation surrounding thermal endurance and fire safety in commercial and industrial infrastructure is accelerating adoption of high-specification silicone insulated cables.

In 2024, global EV production surpassed 18 million units, with high-temperature silicone cables increasingly used in battery packs, charging systems, and thermal management circuits due to sustained exposure to temperatures exceeding 150°C.

Restraints:

-

Material Limitations and Environmental Exposure Challenge High Temperature Silicone Cable Performance in Harsh Applications

There are notable restraints from the high temperature silicone cable market in terms of high thermal stability compared to other specialized materials such as ceramic or fluoropolymer insulations in ultra-in high-temperature applications. Furthermore, the exposure of the cables to UV, ozone or some chemicals can degrade its performance and consequently shorten the life of the cable in harsh environment especially for the renewables which rely on offshore or desert base.

Opportunities:

-

Expanding Green Energy and Medical Tech Drive Demand for Advanced High-Performance Silicone Cable Solutions

There are huge growth opportunities in renewable energy projects most notably solar and wind which tend to be utilizing cables that need to operate in an outdoor environment. Moreover, trend miniaturization of medical and electronic devices raises the demand for miniaturized, flexible high-performance cables, resulting in new applications in precision instrumentation, diagnostics, and healthcare equipment.

The Global Wind Energy Council (GWEC) reported that over 115 GW of new wind capacity was installed globally in 2024, with turbine OEMs specifying high-temp cables for nacelle wiring and grid connections exposed to fluctuating heat and mechanical stress.

Challenges:

-

Navigating Global Compliance and Miniaturization Challenges in High Temperature Silicone Cable Manufacturing

International safety and performance standards like UL, IEC, and RoHS remain an issue for the market, often holding up product approvals and deployment worldwide. Additionally, ensuring the cables are flexible and mechanically sound, as their diameters get smaller for miniaturized applications in medical and wearable devices, is technically difficult and often requires extensive R&D and dedicated production capabilities.

High Temperature Silicone Cable Market Segmentation Analysis:

By Temperature Rating

The Up to 180°C temperature rating segment held the largest market of the global high temperature silicone cable Market share, at 39.8% of total demand in 2024. The biggest part of their domination is that people are widely using these cables in regular applications like consumer electronics, HVAC systems, and low-end industrial wiring where only moderate heat resistance is a requirement. Because they are very flexible, economical, and can be operated under neat totally commercial conditions, they have been widely used in a variety of industries.

From 2025 to 2032, it is anticipated that the 181 °C to 250 °C segment will experience the greatest CAGR. Demand is driven by expanding use in electric vehicles, automation, and robotics where systems need high thermal stability but also mechanical flexibility and mechanical performance reliability.

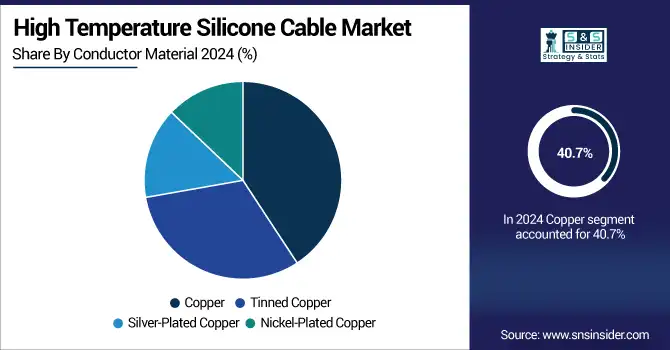

By Conductor Material

Copper held the highest market share of 40.7% in the High-Temperature Silicone Cable Market in 2024. The most common conductor material, copper is available widely, has high electrical conductivity, and is suitable for different high-temperature application. Because of their combination of performance, longevity, and relative ease of installation in traditional stock applications, this trend continues to hold true for industries such as automotive, construction, and general manufacturing, where copper-based silicone wires and cables are in great demand.

The highest CAGR from 2025 to 2032 is predicted for Tinned Copper. Increasing demand for insulation to provide superior corrosion resistance, and longer service life, especially in harsh or humid environments like marine, renewable energy, and outdoor power systems. Moreover, it improves the solderability of the iron which makes it best for precision electronics and control systems.

By End-Use Industry

Automotive & Transportation held the largest share of the High Temperature Silicone Cable Market of 31.2% in 2024 and is expected to witness fastest CAGR between 2025 and 2032 The bulk of this growth is being propelled by the widespread proliferation of EVs (electric vehicles), which are designed to be outfitted with high-performance, heat-resistant cabling for use in battery packs, charging systems and engine components. The growing demand is also propelled by rising adoption of ADAS based systems and onboard electronics. Automotive manufacturers are also increasingly adopting silicone cables where high thermal safety and durability are required to deliver enhanced long-term durability in demanding high vibration, high temperature automotive environments such as in-vehicle under-the-hood and powertrain applications.

By Cable Type

In 2024, Single-Core Cable held a 37.3% share of the High Temperature Silicone Cable Market. While simple, easy to install, and cost-effective, these cables are among the dominant types of cables in use for power transmission, grounding, and basic circuit applications. Sintered ceramics have high thermal stability and insulation properties, which allows them to be used in high-temperature industrial machinery, heating systems, and power distribution units, especially in routing reduction complexity environments.

Multi-Core Cable is expected to exhibit the fastest CAGR during the forecast period of 2025 to 2032. Technology advancement which increases many applications in automation systems, control panels, and compact electronic devices that require multiple signal or power lines in a compact form are some of the factors driving the demand. These cables enhance circuit performance but also save hours on installations too.

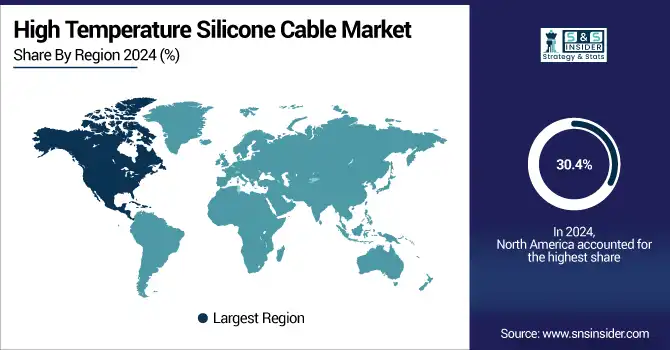

High Temperature Silicone Cable Market Regional Outlook:

The High Temperature Silicone Cable Market in North America accounted for 30.4% of share in 2024 due to the high demand in automotive & transportation, aerospace, industrial automation & machinery, renewable energy, and marine applications among others. Factors such as advanced manufacturing infrastructure, high penetration of electric vehicles and the early implementation of stringent fire safety and performance regulations in the region contributed to the higher adoption of high-performance silicone-insulated cables Apart from this, continuous investments toward grid modernization and solar PV installations along with next-generation medical devices further drive the regional demand.

The U.S. lead in North America on the strength of its EV manufacturing, aerospace technology, and tough standards on industrial and building safety.

The Asia Pacific is expected to see the highest growth rate at a CAGR of 9.55 % from 2025-2032 in the High Temperature Silicone Cable Market, as a result of fast urbanization, rising electric vehicles production, and wind & solar energy projects. Market growth is driven by the region's strong electronics manufacturing base as an export advantage, and the ever-increasing demand for high-performance cabling in automation and smart infrastructure projects. Demand is further bolstered by the government initiatives favoring the adoption of clean energy and imposing better safety standards in all kinds of industrial facilities. In addition, the increasing penetration of medical and diagnostic devices in developing countries provides opportunities for miniaturized heat-resistant silicone cables.

The Asia Pacific market, China led by a large margin as it possesses huge manufacturing capacity for EV, aggressive policies on industrial automation, and is the leader in solar deployment.

The steady growth of Europe market can be attributed to the increasing emphasis on electric mobility, growing integration of renewable energy and organizational level regulations regarding the non-combustible performance of the products in the region. This created demand for high-performance heat-resistant cables, especially from the electric vehicles and industrial facilities modernization sectors. Further, continuous innovations in medical technology and industrial automation are providing a push for cable development. The trend towards superior quality flame retardant silicone insulated cabling solutions are being driven by regulatory frameworks such as the EU CPR directive that are poised to push manufacturers in both the residential and industrial space.

The High Temperature Silicone Cable market in the emerging economies of Latin America and the Middle East & Africa continues to increase, resulting in steady growth due to rapid industrialization, infrastructure development and the numerous renewable energy projects in these regions. In Latin America, the surge in solar and wind energy projects, particularly in Brazil and Chile, is creating demand for rugged, weather-resistant cables. In addition, increasing investments in oil & gas, utilities, and smart city initiatives in the Middle East & Africa are expected to drive demand for high-performance, heat-resistant silicone cabling in such harsh and demanding environments.

Get Customized Report as per Your Business Requirement - Enquiry Now

High Temperature Silicone Cable Companies are:

The Major Players in High Temperature Silicone Cables Market are Prysmian Group, Nexans S.A., LEONI AG, Sumitomo Electric, Furukawa Electric Co., Ltd., LAPP Group, TPC Wire & Cable Corp., HELUKABEL GmbH, Belden Inc., General Cable, Igus GmbH, Eland Cables, SAB Bröckskes GmbH & Co. KG, Alpha Wire, RS PRO (RS Group), Carlisle Interconnect Technologies, Axon’ Cable, Southwire Company, LLC, Draka, Thermal Wire and Cable, LLC.

Recent Developments:

-

In March 2025, Prysmian Group unveiled an industry-first 245 kV high-voltage dynamic cable system tailored for floating offshore wind farms, offering enhanced mechanical durability, reliability, and thermal resistance to overcome harsh sea conditions.

- In December 2024, Nexans secured a pivotal contract with ScottishPower Renewables to supply ~100 km of 275 kV subsea export cables and 55 km onshore cables for the East Anglia TWO offshore wind farm (960 MW capacity), enhancing its role in the offshore renewable sector.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.34 Billion |

| Market Size by 2032 | USD 2.65 Billion |

| CAGR | CAGR of 8.95% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Temperature Rating (Up to 180°C, 181°C to 250°C, and Above 250°C) • By Conductor Material (Copper, Tinned Copper, Silver-Plated Copper, and Nickel-Plated Copper) • By End-Use Industry (Automotive & Transportation, Aerospace & Defense, Industrial Machinery, Energy & Power and Electronics & Appliances) • By Cable Type (Single-Core Cable, Multi-Core Cable, Shielded Cable, and Unshielded Cable) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Prysmian Group, Nexans S.A., LEONI AG, Sumitomo Electric, Furukawa Electric Co., Ltd., LAPP Group, TPC Wire & Cable Corp., HELUKABEL GmbH, Belden Inc., General Cable, Igus GmbH, Eland Cables, SAB Bröckskes GmbH & Co. KG, Alpha Wire, RS PRO (RS Group), Carlisle Interconnect Technologies, Axon’ Cable, Southwire Company, LLC, Draka, Thermal Wire and Cable, LLC. |

Frequently Asked Questions

Ans: North America dominated the High Temperature Silicone Cable Market in 2024.

Ans: The Automotive & Transportation segment dominated the High Temperature Silicone Cable Market in 2024.

Ans: The major growth factor of the High Temperature Silicone Cable Market is the rising demand for heat-resistant and durable cabling solutions in electric vehicles, aerospace, and industrial automation.

Ans: The High Temperature Silicone Cable Market size was USD 1.34 Billion in 2024 and is expected to reach USD 2.65 Billion by 2032.

Ans: The High Temperature Silicone Cable Market is expected to grow at a CAGR of 8.95% from 2025-2032.

Get in Touch