Wealth Management Platform Market Size & Overview:

Get more information on Wealth Management Platform Market - Request Sample Report

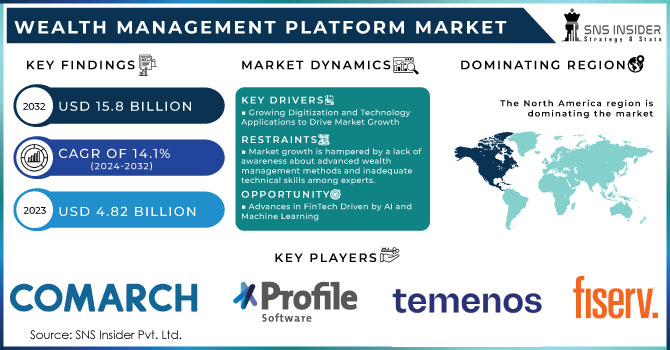

Wealth Management Platform Market was valued at USD 4.49 Billion in 2023 and is expected to reach USD 13.1 Billion by 2032, growing at a CAGR of 12.67% from 2024-2032.

The Wealth Management Platform Market is witnessing significant growth, with the rise of digital transformation in the financial services industry coupled with the increasing demand for personalized investment solutions. From 2024 onwards, platforms are begin to deploy advanced technologies like AI and big data analysis to provide bespoke advisory, risk control, and portfolio management. The low-cost, automated financial advice offered by AI-powered robo-advisors tends to attract younger, tech-oriented investors in droves. These platforms are also improving customer experiences by leveraging data to provide personalized financial products in addition to dynamic portfolio management.

The changing regulatory landscape is one of the major growth factors. The increasing focus on compliance with regulations such as MiFID II and GDPR urges the need for an advanced wealth management platform which aids in ensuring regulatory compliance along with operational efficiency handshake. In addition, the low interest rates for deposits and the growing number of high-net-worth (HNWIs), as well as ultra-high-net-worth individuals (UHNWIs) around the world, are providing a fillip to the market as these clients seek complex wealth management services.

The wealth management platform market is especially increasing in North America and corresponds to the high concentration of wealth and rapid adoption of digital technologies in this area, in particular, the United States. Europe — with its stringent regulatory system and increasing desire for sustainable investment opportunities — is a large part of the equation as well.

Looking ahead, it is clear that the market will continue to evolve, largely driven by automation powered increasingly by AI-based and machine learning solutions. They will modernize operations and solve the security and compliance problem with strict data protection laws.

Wealth Management Platform Market Dynamics

Drivers

-

The integration of AI, machine learning, and big data analytics enhances decision-making, portfolio management, and risk assessments

-

Robo-advisors are making wealth management services more accessible and affordable, attracting younger and tech-savvy investors

-

Rising interest in ESG (Environmental, Social, and Governance) investing is pushing platforms to offer sustainable and socially responsible investment choices

An increase in ESG (Environmental, Social, and Governance) investing is a major trend affecting the wealth management platform market. The demand for sustainable and socially responsible investment options has skyrocketed, as more investors look to align their financial portfolios with their personal values. As a result, wealth management platforms have begun embedding ESG considerations into their investment solutions to offer clients a diverse portfolio of sustainable investments.

Both consumer preference and regulatory starts have been what has principal this shift. A growing number of investors are showing a taste for investments that deliver financial value but also create a measurable social or environmental benefit, especially millennials and Gen Z. Treadmill, is very aware of global issues and expects financial platforms to meet those expectations around climate, social equity, and governance.

In addition to consumer demand, governments and regulators across the globe are activating policies that promote or mandate enhanced transparency and disclosure on ESG metrics. One example of this is the EU SFDR, Sustainable Finance Disclosure Regulation, which requires financial institutions to report in detail how the ESG requirements are met by their investment products. Such regulations are promoting market conditioning that paves the way for platforms to create/offer ESG-aligned investment products. As platforms for wealth management continually evolve, many already include advanced ESG scoring models to help clients evaluate and select investments by an overall sustainability or social responsibility metric. These can be anything from renewable energy to socially responsible corporations to fair labor or gender equality. In addition, a few platforms are using the power of artificial intelligence and big data analytics to facilitate tracking the real-time impact of ESG investments on lines of ESG events that are beneficial for investors to refine their investment decisions and enhance their value over the years.

The long-lasting effect of increasing term acceptance of ESG factors is changing the way wealth is being managed which inevitably leads to platforms that cater to this demand will take a bigger share of the market. And this trend is rising which has resulted in the growth of the wealth management, wealth management platform market in the upcoming years.

Restraints

-

The cost of implementing advanced wealth management platforms, especially for small firms, limits market adoption.

-

The risk of cyber threats and data breaches raises concerns over the security of sensitive financial data.

-

Integrating new platforms with legacy systems often results in technical and operational difficulties, hindering growth.

The technical and operational complexity of integrating wealth management platforms with legacy systems is one of the main challenges inhibiting market growth. Wealth management firms operate on outdated software and infrastructure, built long before the advent of cloud-based solutions or artificial intelligence (AI) and big data analytics. Migrating away from these legacy systems to more modern platforms requires a significant amount of technical knowledge, time, and money. One of the biggest challenges is realizing backward compatibility across systems. Older platforms might not be compatible with newer technologies, resulting in silos or inconsistencies that can break the seamless operation of wealth management functionalities. They usually involve re-architecting or reconfiguring the existing IT system, making the entire integration process resource-consuming and time-consuming. During the integration phase, or post-integration which can drive customer experience down and they might lose their trust in the platform. Furthermore, the process of data migration from legacy systems and into new platforms is inherently complex and high in occurrences of error. Inaccurate transfer of vast amounts of historical financial data: Old systems may have old formats or utilize databases that are not compatible. This could also pose security risks and complicate to integration process as improper driving of data would put sensitive client data at stake.

A significant problem, of course, is that legacy systems cannot often scale and be flexible enough to support modern wealth management solutions. The demands of customers who want real time insights, personalized recommendations, and ESG (Environmental, Social, and Governance) investment options cannot be met with legacy systems, which might lack the capacity to manage the required data without massive updates, which will push back the implementation of new platforms. But no matter how these challenges manifest themselves, there is a growing desire in the market for solutions that can bridge between those legacy infrastructure stacks and new technology stacks, and help facilitate smoother transitions so that system integration friction is reduced.

Wealth Management Platform Market Segment Analysis

By Advisory Mode

The human advisory mode segment dominated the market and held the largest revenue share of 54.28% in 2023. Security concerns are one of the reasons to prefer human advisory over robo-advisory amongst various HNWIs across the world. In addition, human advisory services also make it easier to foster relationships with clients, communicate wealth management strategies, and communicate wealth management plans more effectively. The trends, however, are changing a little slowly, and clients are beginning to believe in the hybrid advisory model than the human advisory model.

The robo-advisory segment is expected to register the highest CAGR during the forecast period. Robo advisors are typically accurate, efficient, and more accessible than other modes. Thus, the robo-advisory platform is slowly but surely evolving into a low-cost alternative for many of the risk & compliance management firms, due to the affordability it provides because of its user-friendly features, low-cost fee model, and low/zero account minimums. Robo advisory segment will also be blessed with new growth opportunities owing to several influencing factors including ever-strengthening competition, changing client needs, and fast changing market scenario.

By Deployment

The cloud segment dominated the market and represented a significant revenue share of 58.0% in 2023. It is expected to grow across at a CAGR which is the fastest among all and will continue to hold its dominance during the prediction timeframe. Many companies across the globe are adopting cloud-based solutions due to the advantages they provide—scalability, agility, 24*7 availability of data, etc. The S-Cloud platform, with its ability to be cost-efficient and scalable, enables firms to build a wealth management platform for the future at an accelerated pace. Moreover, financial advisory firms around the world are now concentrating on implementing cloud-based solutions as part of their strategy to save costs in business operations.

The On-Premise deployment is anticipated to grow at a moderate CAGR of 10.8% during the forecast period. Many organizations are still inclined toward the on-premise deployment of solutions as they want to have maximum control of all the systems and data. The on-premise deployment model also enables organizations to have greater control over how software is implemented. On-premise solutions offer the assurance that business data is kept and taken care of in-house; however, the caveat is that businesses need to hire dedicated, in-house IT personnel as well to handle support and maintenance.

By Application

In 2024, the portfolio, accounting & trading management segment dominated the market and held the largest share of the Market. As the demand for portfolio management & trading solutions is skyrocketing; portfolio, accounting, & trading management solutions are enabling trading managers to focus on collaborative processes and deliver better customer service. Portfolio, accounting & trading managers are feeling extreme pressure to manage the data of their customers and are thus aggressively adopting wealth management solutions. Portfolio, accounting & trading management platforms are also being used by wealth managers for their client's financial data for the best decision-making solution that they can support them with.

The financial advice management segment is estimated to grow at the highest CAGR during the forecast period. The global financial advice & management market is projected to propel in terms of its adoption due to increased focus on digitization, operational optimization, and enriched customer relationships by several businesses across the globe, which is expected to boost the demand for financial advice & management solutions shortly. These days many wealth management firms are leveraging kind of wealth management software to serve their multiple clients in a better manner. Integrated fintech solutions in financial advice and management assist financial managers in collaborating with clients to develop optimal investment proposals, identify and analyze financial goals, and effectively deliver financial advice.

Need any customization research on Wealth Management Platform Market - Enquiry Now

Regional Analysis

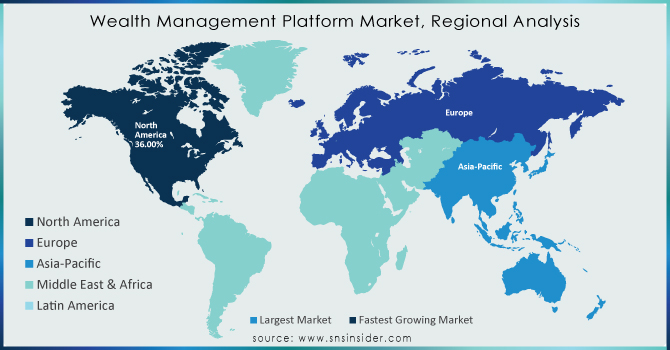

In 2023, the North American wealth management software market had the largest share of more than 36.81%. There has been a steady rise in High-Net-Worth Individuals (HNWIs) in the region. These HNWIs are increasingly taking out subscriptions for high-end financial advisory solutions. Some of the main market players are also located in North America. Another factor for the growth in the regional market is digitalization, as many North American countries are digitalizing their financial sector.

The Asia Pacific wealth management software market is expected to grow at the highest CAGR over the forecast period. The growing adoption of digital platforms in the region generally suffices the roi-robo advisors in the region. Novel analytics and sophisticated algorithms have led techno-savvy customers to utilize robo-advisory tools to effectively fulfill their investment requirements. In addition, the growing number of SMEs in emerging economies like China, Japan, and India can provide opportunities for the market to grow. Furthermore, increasing implementation of the new IT infrastructure by the SMEs in the region is anticipated to fuel the demand for digital financial services owing to the need to increase their operating capabilities.

The underlying weight of Japan's wealth management software is anticipated to expand rapidly over the years ahead. Japan is another key driver for the market, as it has seen major growth in demand for retirement planning and wealth preservation strategies due to its aging population. In wealth management, technology-driven solutions are being used more than ever to facilitate service delivery and client engagement. Along with this trend, the cultural background of Japanese people being conscious of investment further backs up the trend where wealthy clients prefer more tailored approaches to wealth management.

Key Players

The major key players along with their products are

-

Fidelity Investments – Fidelity Wealth Management Platform

-

Charles Schwab – Schwab Intelligent Portfolios

-

UBS – UBS SmartWealth

-

JPMorgan Chase – J.P. Morgan Private Bank Platform

-

Goldman Sachs – Marcus by Goldman Sachs (Investment Solutions)

-

BlackRock – Aladdin WealthTech

-

Morgan Stanley – Morgan Stanley Wealth Management

-

Vanguard – Vanguard Personal Advisor Services

-

Addepar – Addepar Wealth Management Platform

-

Citi Private Bank – Citi Private Bank Wealth Management Services

-

BNP Paribas Wealth Management – Wealth Management Platform

-

State Street Global Advisors – State Street Global Advisors Solutions

-

Santander Private Banking – Santander Wealth Management Platform

-

Envestnet – Envestnet Wealth Management Solutions

-

TDAmeritrade – TDAmeritrade Institutional

-

Cognizant – Wealth Management Platform Solutions

-

Temenos – Temenos Wealth Management Software

-

SEI Investments – SEI Wealth Platform

-

S&P Global – S&P Capital IQ Pro for Wealth Management

-

Raymond James – Raymond James Private Client Group Services

Recent Developments

In September 2024, KFin Technologies introduced mPower Wealth, a comprehensive platform designed for wealth managers, family offices, and asset managers. The platform integrates front, mid, and back-office functions and is designed to support multi-asset and multi-currency portfolios, with a focus on AI-driven insights and robust compliance features

| Report Attributes | Details |

| Market Size in 2023 | USD 4.49 Billion |

| Market Size by 2032 | USD 13.1 Billion |

| CAGR | CAGR of 12.67% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

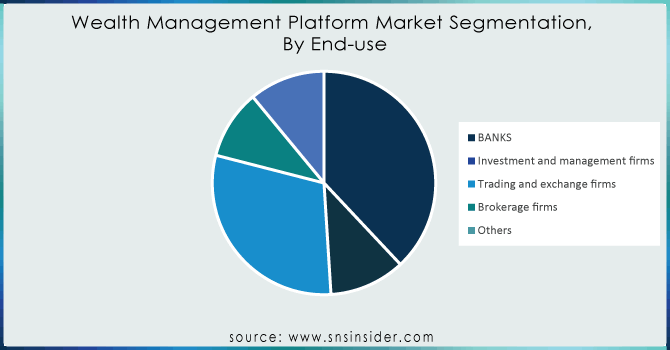

| Key Segments | • By Advisory Mode (Human Advisory, Robo Advisory, Hybrid) • By Organization Size (Large Enterprises, Small & Medium Enterprises) • By Application (Financial Advice & Management, Portfolio, Accounting, & Trading Management, Performance Management, Risk & Compliance Management, Reporting, Others) • By Deployment (Cloud, On-premise) • By End-use (Banks, Investment Management Firms, Trading & Exchange Firms, Brokerage Firms) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles |

Fidelity Investments, Charles Schwab, UBS, JPMorgan Chase, Goldman Sachs, BlackRock, Morgan Stanley, Vanguard, Addepar, Citi Private Bank, BNP Paribas Wealth Management, State Street Global Advisors, Santander Private Banking, Envestnet, TDAmeritrade, Cognizant, Temenos, SEI Investments |

| Key Drivers | •The integration of AI, machine learning, and big data analytics enhances decision-making, portfolio management, and risk assessments •Robo-advisors are making wealth management services more accessible and affordable, attracting younger and tech-savvy investors •Rising interest in ESG (Environmental, Social, and Governance) investing is pushing platforms to offer sustainable and socially responsible investment choices |

| Market Restraints | •The cost of implementing advanced wealth management platforms, especially for small firms, limits market adoption. •The risk of cyber threats and data breaches raises concerns over the security of sensitive financial data. •Integrating new platforms with legacy systems often results in technical and operational difficulties, hindering growth. |

Frequently Asked Questions

Ans Wealth Management Platform Market was valued at USD 4.49 Billion in 2023 and is expected to reach USD 13.1 Billion by 2032, growing at a CAGR of 12.67% from 2024-2032.

Ans- the CAGR of the Wealth Management Platform Market during the forecast period is 12.67% from 2024-2032.

Ans- the North America dominated the market and represented a significant revenue share in 2023

Ans- one main growth factor for the Wealth Management Platform Market is

- The integration of AI, machine learning, and big data analytics enhances decision-making, portfolio management, and risk assessments

Ans- Challenges in the Wealth Management Platform Market are

- The cost of implementing advanced wealth management platforms, especially for small firms, limits market adoption.

- The risk of cyber threats and data breaches raises concerns over the security of sensitive financial data.

Get in Touch