Wine Market Report Scope & Overview:

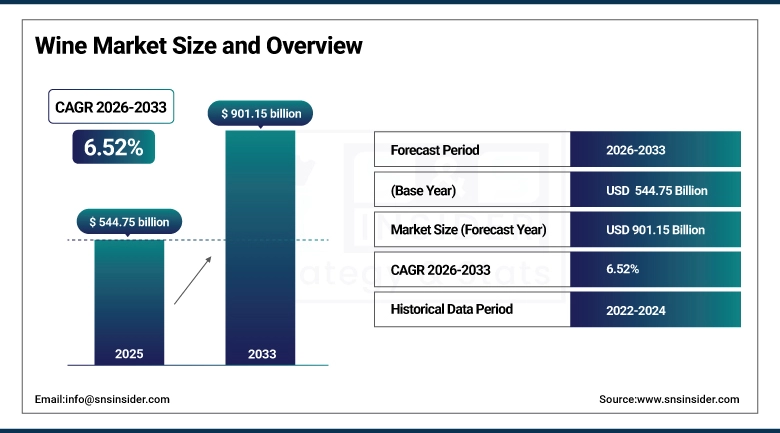

The Wine Market Size was valued at USD 544.75 Billion in 2025E and is projected to reach USD 901.15 Billion by 2033, growing at a CAGR of 6.52% during the forecast period 2026–2033.

The Wine Market analysis offers a detailed study of consumption trends and evolving consumer preferences to understand market growth. It divides the market into product type (red, white, rosé, sparkling, dessert & fortified, and others), packaging (glass bottles, cans, tetra packs, bag-in-box and others), price range (economy, mid-range premium luxury), end user (household HoReCa industrial) distribution channel (supermarkets convenience stores online store specialty stores duty-free). Growing demand for premium wines and online sales contribute to growth.

Red and sparkling wines reached a consumption of 220 million cases in 2025, reflecting growing consumer preference for premium, celebratory, and diverse wine varieties.

Market Size and Forecast:

-

Market Size in 2025: USD 544.75 Billion

-

Market Size by 2033: USD 901.15 Billion

-

CAGR: 6.52% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Wine Market - Request Free Sample Report

Wine Market Trends:

-

Rising urbanization and a more developed home social drinking culture are also boosting sales of ready to drink and premium wines in both the on-trade and off trade.

-

Innovative formats-packaging, such as lighter weight glass bottles, cans and bag-in-box designs-provide convenience, portability and longer shelf life for today’s consumers.

-

Increasing interest in different grape varieties is indicative of shifting palates that have been opened up to the world and carried down the path of international fusion wine flights.

-

E-commerce players and subscription wine clubs are beginning to be important channels for brands who can use them to access consumers directly with curated paths.

-

Trends for healthier drinking, which include low-alcohol natural and organic wines, are encouraging producers to develop new concepts and reach environmentally and/or health-conscious consumers.

U.S. Wine Market Insights:

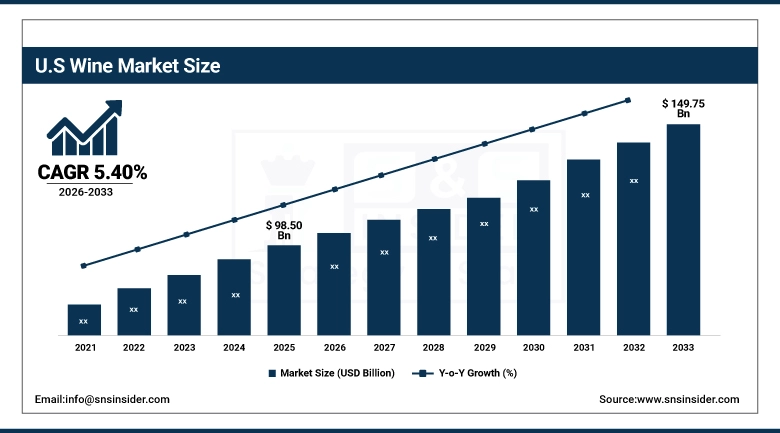

The U.S. Wine Market is projected to grow from USD 98.50 Billion in 2025E to USD 149.75 Billion by 2033 at a CAGR of 5.40%. It is led by premium and sparkling wines, household consumption, gifting occasions and novel packaging, and growing penetration in HoReCa and foodservice across the country.

Wine Market Growth Drivers:

-

Rising premiumization and celebratory culture are boosting demand for diverse, ready-to-serve, and high-quality wines.

Wine Market growth is encouraged by premiumization and increasing demand for a variety of ready-to-serve wines. In 2025, wine consumption in the world amounted to some 1.45 billion cases and is expected rise to 2.35 billion boxes by 2033. Opportunities in both developed and emerging markets with innovative packaging, exclusive grape varieties, sparkling and rosé variants and increased investment from producers catering to urban homes, celebrations, HoReCa/foodservice channels globally.

Rising demand for premium and sparkling wines drove consumption of 520 million cases in 2025, fueled by celebrations, urban households, and HoReCa channels.

Wine Market Restraints:

-

High prices and strict alcohol regulations are limiting consumption, especially among young and price-sensitive urban consumers.

The growth of Wine Market is limited by High Cost and Stringent Alcohol Rules. In 2025, cost-conscious urban millennials reduced wine consumption by some 25%, and nearly a fifth of Asia-Pacific homes went low-alcohol or no-alcohol. Small and medium wineries struggle to compete with the market presence of major premium brands, while restrictions on labeling, import duties, and alcohol content also hinder market growth. Affordability and regulatory hurdles still dampen the wine market despite an increasing interest in wine globally.

Wine Market Opportunities:

-

Increasing demand for organic, low-alcohol, and sustainably produced wines creates lucrative opportunities for premium and niche launches.

Rising demand for organic, low-alcohol and sustainable wines is bolstering market growth. In 2025, the world consumed more than 120 million cases of premium and niche wines-demand is projected to grow beyond 250 million cases by 2033. Urban dwellers that are conscious about what they consume and grow demand for natural wines, and an increasingly sustainable future, innovative packaging, special grape varieties or the move toward sparkling and rosé options have given these wines greater convenience and attractiveness in households and HoReCa.

Organic, low-alcohol, and sustainably produced wines accounted for 18% of new wine product launches in 2025, driven by health-conscious urban consumers and growing demand for eco-friendly, clean-label beverages.

Wine Market Segmentation Analysis:

-

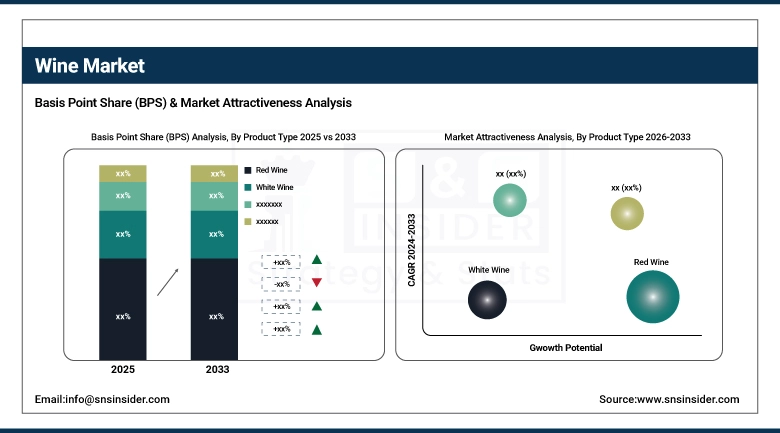

By Product Type, Red Wine held the largest market share of 38.25% in 2025, while Sparkling Wine is expected to grow at the fastest CAGR of 7.12%.

-

By Packaging, Glass Bottles dominated with a 62.48% share in 2025, while Bag-in-Box is projected to expand at the fastest CAGR of 7.85%.

-

By Price Range, Mid-range wines accounted for the highest market share of 42.31% in 2025, and Premium wines are projected to record the fastest CAGR of 8.03%.

-

By End User, Household segment held the largest share of 55.12% in 2025, while HoReCa / Foodservice users are expected to grow at the fastest CAGR of 7.48%.

-

By Distribution Channel, Supermarkets & Hypermarkets dominated with a 46.38% share in 2025, while Online Retail is projected to record the fastest CAGR of 8.21%.

By Product Type, Red Wine Dominates While Sparkling Wine Expands Rapidly:

Red Wine sector dominated the Product Type segment with 550 million cases consumed in 2025, driven by strong household preference, widespread availability, and cultural familiarity across developed and emerging markets. It is far and away the number one when it comes to value and volume. The Sparkling Wine sector is the fastest growing Product Type segment owing to an increase in celebratory occasions, consumers’ inclination toward premium and luxurious beverages, and increasing penetration across urban households including HoReCa due to innovation such as Prosecco and Rosé Sparkling.

By Packaging, Glass Bottles Lead While Bag-in-Box Expands Rapidly:

Glass Bottles sector dominated the Packaging segment with around 850 million cases in 2025, due to tradition, premium perception, and suitability for storage and gifting. Glass is also equated with quality which has helped maintain demand for the material both in homes and restaurants. Bag-in-Box sector is the fastest growing Packaging segment, which is a very convenient and also cost-effective way of packaging as compared to others. Increasing acceptance on casual and at home drinking occasions, and easy storage, is prompting swift adoption among urban people.

By Price Range, Mid-Range Wines Dominate While Premium Expands Rapidly:

Mid-range sector dominated the Price Range segment with 610 million cases consumed in 2025, offering a balance of quality and affordability. Daily consumption is mainly in the household and HoReCa channels. Premium sector is the fastest-growing Price Range segment, driven by higher disposable incomes, aspirational lifestyles and celebratory drinking culture. Sales are also fueled by wine clubs, internet sales and gift-giving trends that entice the consumer to enjoy premium varietals and limited-quantity labels.

By End User, Household Dominates While HoReCa / Foodservice Expands Rapidly:

Household sector dominated the End User segment with around 800 million cases in 2025, driven by increasing at-home entertaining, casual meals, and gifting occasions. Scores of wines, shop-at-home convenience and broad retail availability give it status. HoReCa/Foodservice sector is the fastest growing End-User segment driven by an increase in eating out, premiumization trends in restaurants and increasing urban tourism. Bars, cafes and hotels are broadening their wine repertoire, by increasing the consumption of sparkling, rosé and premium wines.

By Distribution Channel, Supermarkets & Hypermarkets Dominate While Online Retail Expands Rapidly:

Supermarkets & Hypermarkets sector dominated the Distribution Channel segment with 710 million cases sold in 2025, benefiting from convenience, wide assortment, and promotional campaigns. They are the preferred vehicle for daily shopping, and bulk purchase or stock-up. Online Retail sector is growing as the fastest Distribution Channel segment on the back of e-commerce adoption, subscription wine clubs and ease of home delivery. City-based wines and high-end vino purchasers are among the groups now using digital as a prime source for curated ranges, private labels and to get product delivered direct to the door.

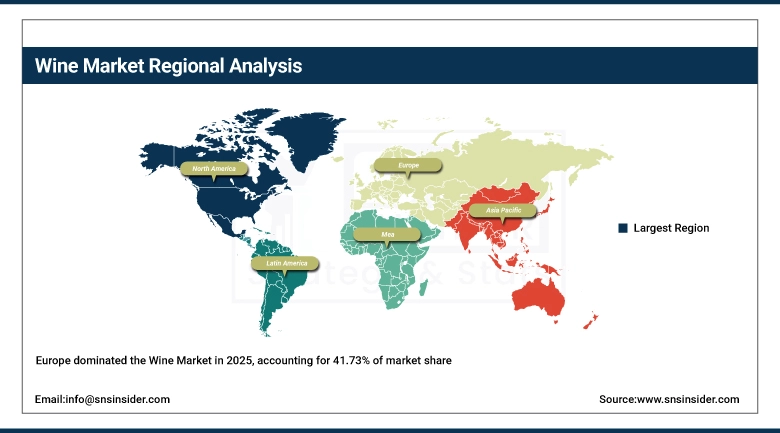

Wine Market Regional Analysis:

Europe Wine Market Insights:

Europe dominated the Wine Market with a 41.73% share in 2025, recording consumption of 570 million cases. Germany was the leader with 150 million cases, followed by France at 130 million cases and Italy at 110 million cases. Household consumption at 320 million cases was the biggest segment while HoReCa accounted for 190 million cases. Increasing consumer demand for premium and sparkling products, gifting culture and a long tradition of wine has driven growth across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

-

Germany Wine Market Insights:

In 2025 Germany drank 150 million cases of wine, 85 million in households and 65 million on premises (HoReCa/foodservice). Red wine dominated the market. An emerging young audience opting for premium, sparkling wines and higher frequencies of gifting occasions, wine tourism is driving growth in households, restaurants and bars across the country.

North America Wine Market Insights:

North America drank more than 310 million cases of wine last year with the US drinking 260 million cases, and Canada producing a 50 million. Demand was led by household consumption, and then HoReCa and foodservice channels. Urbanization, the premiumisation trend and increased interest in sparkling, rosé and ready to serve wines are all important growth drivers. Creative packaging, selected mixes and the online retail surge also are helping drive consumption in homes, restaurants and bars.

-

U.S. Wine Market Insights:

In 2025, U.S. people drank more than 260 million, 175 million at home and 85 million in HoReCa/foodservice. Growth is fueled by premium and sparkling wines, gifting occasions, beverage packaging innovations and curated assortments; and climbing on-premise adoption across restaurants, bars and quick-service providers nationwide.

Asia-Pacific Wine Market Insights:

Asia-Pacific is the fastest growing region in Wine Market with a CAGR of 8.16% owing to increasing disposable incomes, urban middle class populations and rising preference for premium, sparkling & ready-to-serve wines. In 2025, China consumed more than 120 million cases and India over 45 million cases. Growing demand for both sparkling and rosé wines According to research, the consumer segment market in Russia values innovation packaging, luxuryand niche assortments plus high penetration into on-trade, off-trade and HoReCa channels.

-

China Wine Market Insights

China drank over 120 million cases of wine in 2025 with a split of circa 85m cases domestic and around 35 million in HoReCa/foodservice. Growth is driven by rapid urbanisation, the rise of middle-class incomes and an increasing desire for premium, sparkling and ready-to-drink wines along with craft, thanks to innovative packaging, curated assortments and wider adoption in restaurants/bars.

Latin America Wine Market Insights:

Latin America is projected to consume more than 55 million cases of wine in 2025, with Brazil topping the list at 22 million cases, followed by Argentina (18 million) and Chile (9 million). In households, consumption was 33 million cases and HoReCa/foodservice were 22 million cases. Increased consumption of high-quality, sparkling and ready-to-drink wines and new packaging are stimulants for growth in restaurants, bars and urban homes throughout the region.

Middle East and Africa Wine Market Insights:

The Middle East and Africa Wine Market would devour more than 15 million cases of wine by the year 2025 in the UAE (5 million cases) and South Africa (4 million cases). Household consumption stood at 9 million cases and of HoReCa/foodservice type was 6 million cases. Premium, sparkling and 'ready-to-drink' wines coupled with new packaging formats is driving growth across households, restaurants and bars.

Wine Market Competitive Landscape:

E. & J. Gallo Winery dominated this industry, publishing over 140 million cases per year in 2025. Founded in 1933, Bronco Wine Co. boasts nearly 90 years of winemaking in addition to thousands of acres of vineyards across California. Its wines are sold in 50+ countries, through a network of domestic and HoReCa channels. Steady development in varietals, premium wines and sparkling, supported by targeted mergers and alliance makes it a formidable leader in the market.

-

In February 2025, E. & J. Gallo Winery launched a new line of organic and low-alcohol wines under its Barefoot brand, targeting health-conscious and urban consumers seeking premium, ready-to-serve options.

Constellation Brands Inc., controls the North American market and will produce over 120 million cases of wine in 2025. The company, established in 1945, brings together generations of know-how with its extensive range of products, offering premium wines and sparkling and imported. Strong market presence is maintained by wide distribution networks in the U.S., Canada, and Mexico and by strategic brand purchases and marketing steps focused on urban homes and HoReCa.

-

In April 2025, Constellation Brands introduced a sparkling rosé collection under the Kim Crawford label, designed for celebratory occasions and on-the-go consumption, with innovative 375ml glass bottles for portability.

The Wine Group LLC is the world’s third largest wine producer with a production of more than 90 million cases in 2025. Founded in 1981, it is backed by decades of expertise in volume and premium wine making. The company has broad distribution in the U.S., Europe and other emerging markets and is concentrated on the popular varietals; packaging innovation; and adding to its product portfolio. Strong brand recognition, competitive pricing and an entryway into large retailers and foodservice operators reinforce its leadership.

-

In January 2025, The Wine Group launched a sustainable Bag-in-Box packaging line for its Franzia wines, focusing on convenience, eco-friendly consumption, and growing demand for at-home entertaining.

Wine Market Key Players:

Some of the Wine Market Companies are:

-

E. & J. Gallo Winery

-

Constellation Brands, Inc.

-

The Wine Group LLC

-

Treasury Wine Estates

-

Pernod Ricard SA

-

Viña Concha y Toro

-

Castel Frères

-

Grupo Peñaflor

-

Accolade Wines

-

LVMH Moët Hennessy Louis Vuitton

-

Marqués de Riscal

-

Bodegas Torres

-

Banfi S.r.l.

-

Champagne Louis Roederer

-

Antinori

-

Jacob’s Creek (Treasury Wine Estates)

-

Hardy Wine Company

-

Robert Mondavi Winery

-

Famille Perrin

-

Moët & Chandon

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 544.75 Billion |

| Market Size by 2033 | USD 901.15 Billion |

| CAGR | CAGR of 6.52% From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Red Wine, White Wine, Rosé Wine, Sparkling Wine, Dessert & Fortified Wine, Others) • By Packaging (Glass Bottles, Cans, Tetra Packs, Bag-in-Box, Others) • By Price Range (Economy, Mid-range, Premium, Luxury) • By End User (Household, HoReCa/Foodservice, Industrial) • By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Duty-Free & Travel Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | E. & J. Gallo Winery, Constellation Brands, Inc., The Wine Group LLC, Treasury Wine Estates, Pernod Ricard SA, Viña Concha y Toro, Castel Frères, Grupo Peñaflor, Accolade Wines, LVMH Moët Hennessy Louis Vuitton, Marqués de Riscal, Bodegas Torres, Banfi S.r.l., Champagne Louis Roederer, Antinori, Jacob’s Creek (Treasury Wine Estates), Hardy Wine Company, Robert Mondavi Winery, Famille Perrin, Moët & Chandon |

Frequently Asked Questions

Europe dominated the Wine Market with a 41.73% share in 2025.

Red Wine dominated the market in 2025, while Sparkling Wine is projected to grow at the fastest CAGR of 7.12%.

Growth is driven by rising premiumization, celebratory culture, increasing household consumption, innovative packaging, sparkling and rosé wine trends, and adoption in HoReCa/foodservice channels.

The market was valued at USD 544.75 Billion in 2025E and is projected to reach USD 901.15 Billion by 2033.

The Wine Market is expected to grow at a CAGR of 6.52% during 2026–2033.

Get in Touch