Women's Healthcare Market Report Scope & Overview:

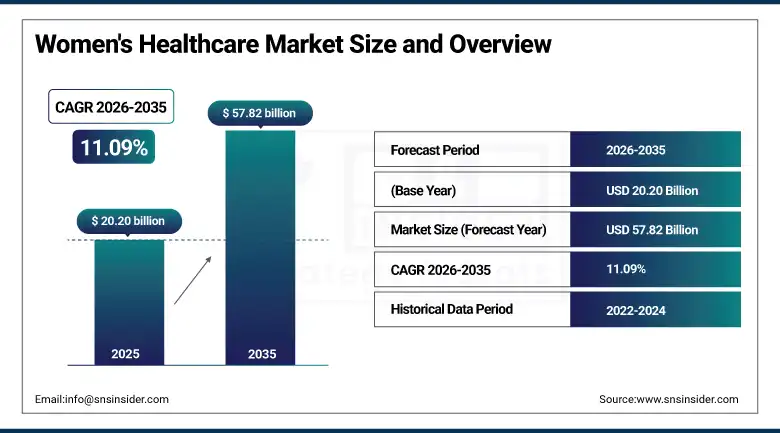

The Women's Healthcare market was valued at USD 20.20 billion in 2025 and is expected to reach USD 57.82 billion by 2035, growing at a CAGR of 11.09% from 2026–2035.

The women's healthcare product portfolio includes all diagnostic, therapy, and prevention products tailored to meet specific female health issues. Women's healthcare products involve all aspects of the health concerns that are particular to women, such as reproduction, delivery of babies, preventive measures and cancer screening tests, treatment and management of menopause, osteoporosis, and mental illness. Women's healthcare checkups have reached over one billion two hundred million through hospitalization, clinics, and telehealth service providers in 2025. The rising number of women accessing healthcare services is mainly attributed to increased awareness regarding the healthcare of women, fertility issues, and preventive measures in the world. Significant advancements in telehealth technologies are contributing immensely to women being able to reach out to experts regardless of where they live. With the help of artificial intelligence technology, women can easily undergo tests for cervical cancer, breast cancer, and endometriosis at their early stages. There are new developments in hormone therapies that enable medical practitioners to diagnose and treat reproductive problems and menopause effectively. The formulation of policies by several countries aimed at ensuring women's healthcare initiatives. In 2025, investments in femtech start-ups companies reached an all-time high.

Women's healthcare visits reached 1.2 billion in 2025. Rising demand for reproductive, fertility, and preventive care is driving sustained market growth across hospitals, clinics, and telehealth service platforms.

Market Size and Forecast

-

Market Size in 2026E: USD 22.44 Billion

-

Market Size by 2035: USD 57.82 Billion

-

CAGR: 11.09% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Women's Healthcare Market - Request Free Sample Report

Women's Healthcare Market Trends

-

Telemedicine use for women’s health consultations has gone mainstream after the pandemic era. Tele-gynecology, fertility counselling, and maternal mental health programs are growing rapidly.

-

AI-driven diagnoses have enhanced early detection of cancers in women. Breast and cervical cancer screenings have seen greater success rates using AI image analysis.

-

Femtech development has been resulting in innovative digital health products for women. Period tracking, fertility monitoring, menopausal health apps, and pelvic floor rehabilitation programs are becoming very popular.

-

Hormonal therapy tailored to individuals is revolutionizing menopause and reproductive health treatments. A precise medicine approach to women’s health is allowing for hormone optimization safely.

-

Workplace women's health programs are experiencing substantial growth in major companies. Fertility care, menopause support, and mental health services are becoming common corporate health benefits.

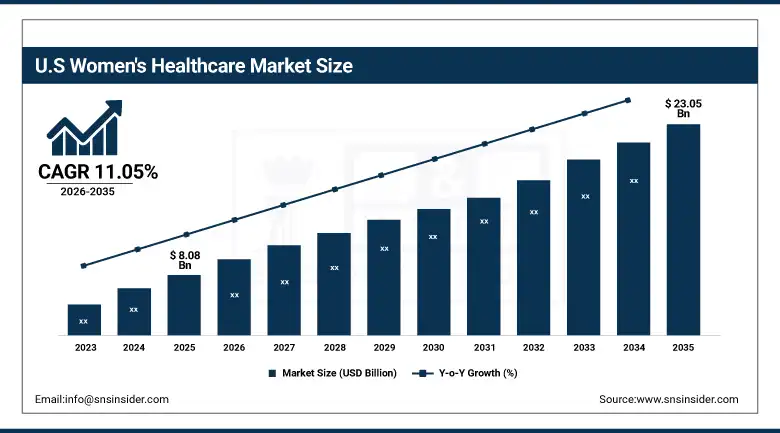

The U.S. Women's Healthcare Market Outlook

The U.S. Women's Healthcare Market was valued at approximately USD 8.08 billion in 2025 and is expected to reach approximately USD 23.05 billion by 2035, growing at a CAGR of 11.05%.

The United States is the largest market for women’s health products and services by revenue. It has the advantage of sophisticated healthcare infrastructure and high per capita healthcare expenditures in the world. Reproductive health data regulation ensures that there are adequate opportunities for telemedicine and femtech platform development.

Funding from government programs under Titles X and CDC women's health ensures continued demand for preventive care services across the country. The occurrence of more than 300,000 breast cancer cases each year provides continuous need for innovative diagnostic tools and treatment solutions. More than 40% of Fortune 500 firms offer fertility insurance coverage to attract employees. The U.S. femtech funding environment remains the world’s most active ensuring constant innovation. FDA approval process is becoming increasingly smooth for women's health products and devices. Expanded Medicaid insurance plans are providing women's healthcare access in many states where it had been previously unavailable.

Women's Healthcare Market Segment Analysis

-

By Age Group, the highest market share was captured by the adults with 52.68%, due to diverse needs regarding reproductive health, oncology, and prevention; the fastest-growing segment was teenagers at a CAGR of 12.14%, due to increasing demands for sexual education, mental health facilities, and online health platforms.

-

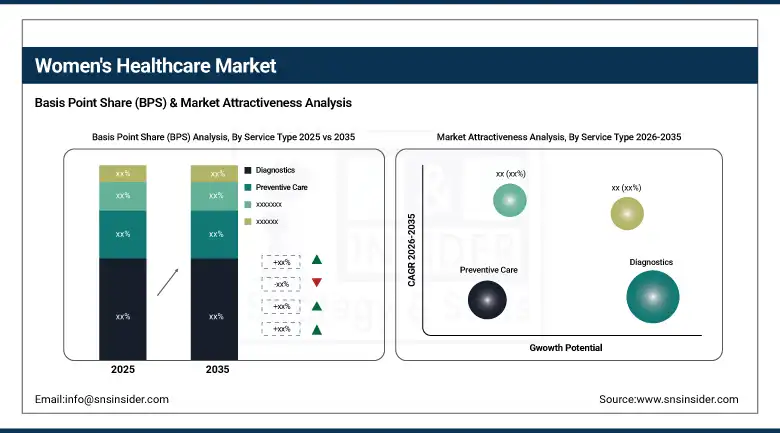

By Service Type, Diagnostics accounted for the largest market share of 41.37% through medical imaging, laboratory analysis, and cancer screening programs; Telehealth was the fastest-growing service with a CAGR of 13.09% due to its digital-only approach that removes any geographical boundaries.

-

By Health Condition, Reproductive Health became the largest category through contraception, infertility, maternity and gynaecology services demands; Oncology is a major market segment through breast and cervical cancers screening and treatment.

-

By End-User, Hospitals & Clinics accounted for the largest end-user segment with a share of 57.84%; Online Platforms were the fastest-growing end-user category at a CAGR of 12.68%.

By Service Type, Diagnostics dominates, Telehealth is expected to grow fastest

Diagnostics retained the dominant service type position with approximately 41.37% of the Women's Healthcare Market in 2025. Mammography, pelvic ultrasound, Pap smear testing, and BRCA genetic testing are core revenue generators. Cervical and breast cancer screening programmes create consistent high-volume diagnostic demand across age groups. AI-powered imaging analysis is improving radiologist throughput and diagnostic accuracy for breast cancer detection. Prenatal diagnostic services including non-invasive prenatal testing are experiencing strong growth. Continuous expansion of national cancer screening programme eligibility is broadening the diagnostic addressable market. Advanced biomarker testing for endometriosis and PCOS is creating new diagnostic categories previously unavailable.

Telehealth services have emerged as one of the fastest-growing service types with their CAGR being 13.09% until 2033. The consultations through telehealth services have become common because of the recent pandemic, as it made such type of consultation normal during cases related to gynecological issues or reproductive health issues. Such services provide convenience as they take away geographic barriers that had been preventing specialist treatment for women living far from major cities or those who were living in rural regions. Postpartum depression and anxiety treatments are highly emerging areas under specialized telehealth services.

By End-User, Hospitals & Clinics dominate, Online Platforms are expected to grow fastest

Hospitals and Clinics remain the largest end-users with approximately 57.84% of the revenues by 2025. These facilities offer the entire range of women's healthcare solutions, from diagnostics to surgical operations. The performance of obstetrics and gynaecology operations necessitates hospital-based infrastructure not possible elsewhere. Leading academic medical centres offer dedicated women's health centres with integrated multidisciplinary care. The consolidation of healthcare systems results in concentration of women's health service volumes into high-intensity hospital-based environments. Diagnostic imaging, laboratory testing, and hospital pharmacy are critical sources of income for women's health services delivery in hospitals. Women's health clinical trials take place mainly at hospitals with academic programme facilities.

Online Platforms experience the highest CAGR in end-user segmentation at 12.68% until 2033. Telehealth providers, such as Maven Clinic, Ovia Health, and Gennev, reach commercial scale in telehealth for women in the US. Direct-to-consumer femtech apps are used by millions of women providing personal health monitoring and coaching. Online prescription of contraception and hormone therapies are challenging traditional clinic visit models. Perinatal and perimenopausal digital mental health platforms show rapid growth. E-commerce of women's health supplements, devices, and wellness products provides an emerging source of additional revenues.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.6% |

|

Europe |

United Kingdom |

26.3% |

|

Asia Pacific |

China |

41.8% |

|

Middle East & Africa |

UAE |

27.9% |

|

Latin America |

Brazil |

44.2% |

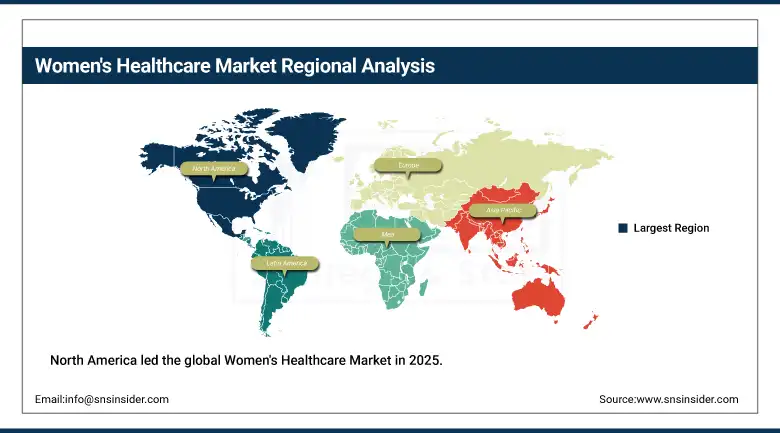

North America Women's Healthcare Market Insights

North America led the global Women's Healthcare Market in 2025. The U.S. accounts for approximately 84.6% of North American revenues. Strong regulatory frameworks protect reproductive health data and telemedicine service delivery. Government programmes support women's preventive care access across income levels. The femtech investment ecosystem is the most active globally, generating sustained product innovation. Major health systems have invested significantly in dedicated women's health centre infrastructure. Canada is growing through expanded provincial telehealth coverage and publicly funded cancer screening expansion. The region is expected to maintain its market leadership position throughout the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Women's Healthcare Market Insights

The European women’s health care space represents a sophisticated market segment characterized by healthcare coverage. Approximately 26.3% of Europe’s revenue comes from the UK. The NHS women’s health care policy has identified endometriosis screening, menopause care, and fertility treatments as priorities. Countries such as Germany, France, and Nordic nations possess state-of-the-art capabilities in terms of gynecologic oncology and reproductive health services. GDPR-compliant femtech platforms are increasingly prevalent in Europe, with a large number of consumers who support privacy measures. Funding from the EU towards women’s health care research is fueling innovation.

Asia Pacific Women's Healthcare Market Insights

The Asia Pacific region is one of the fastest-growing women's healthcare markets worldwide. The reason behind China's dominance in Asia Pacific in terms of revenue generation is the presence of large numbers of people and a developing healthcare sector in the country. The increasing number of women belonging to the affluent classes in India are spending money on private healthcare services and well-being schemes. In Japan, due to an aging female population, there are increased demands for services related to menopause and bone care. South Korea possesses a highly advanced healthcare sector catering to a fitness-conscious demographic of females who demand high-quality medical services. There have been rapid developments in the network of private women's health clinics in Southeast Asia.

MEA & Latin America Women's Healthcare Market Insights

The Middle East and Africa and Latin America represent emerging women’s health markets. The Middle East and Africa revenues share is driven by UAE, which has around 27.9%, owing to the presence of excellent private healthcare facilities. The governments of countries of the GCC region have been making large investments towards increasing maternal and reproductive healthcare services. The objectives of improving women's health outcomes have been set in Saudi Arabia's Vision 2030 plan. The Latin American revenue share is led by Brazil, which accounts for around 44.2% owing to its large population and development of private health sector.

Market Dynamics

Growth Drivers: Rising health awareness, telehealth expansion, and AI-powered diagnostic innovation are driving the global women's healthcare market growth.

Awareness of women's health issues such as reproductive care, prevention, and chronic illness management is growing fast around the globe. Awareness levels are translating to more use of healthcare services and per capita spending on women's health services. Telehealth companies have overcome geography and economics barriers to accessing specialist services in large numbers around the world. Artificial Intelligence-based diagnosis tools are making it easier to diagnose cancers and save money on expensive treatments. Women's health insurance coverage from employer groups is increasing the insured pool of people seeking fertility, menopausal and mental health services. The importance of investment in women's health is gaining momentum in governments' policies. The Femtech industry is inventing new business areas beyond traditional women's clinical services.

Restraints: Healthcare access disparities, data privacy concerns, and reimbursement limitations for telehealth and femtech services are restraining market growth.

Significant disparities in women's healthcare access persist between urban and rural populations globally. Low-income women in both developed and developing markets face financial barriers to care despite growing insurance coverage. Data privacy concerns are limiting adoption of femtech applications that require sensitive personal health data sharing. Reimbursement frameworks for telehealth and digital therapeutics remain inconsistent across national and state-level healthcare systems. Clinical evidence gaps for many femtech applications create uncertainty among clinical adopters and healthcare payer organisations. Regulatory pathways for novel women's health diagnostics and devices vary significantly across international jurisdictions. Workforce shortages in gynaecology, maternal medicine, and women's mental health are constraining clinical capacity in many markets. Cultural and social barriers restrict women's healthcare-seeking behaviour in conservative markets across Africa and the Middle East.

Opportunities: Femtech platform growth, employer health benefit expansion, and AI diagnostics create substantial women's healthcare market growth opportunities.

Femtech is creating an entirely new set of service offerings in the interface of technology and women's health services. Menstrual cycles tracking, menopausal management, and pelvic floor therapy applications are producing commercially valuable users bases across the world. The opening of new channels through the extension of employer benefits to include women's health platforms is creating institutional purchase of women's health platforms. AI-driven genetic predisposition tests for hereditary BRCA and other cancers create high value diagnostics services. Premium personal hormone therapy programs based on constant biomarker monitoring are a premium growth area. Integrated healthcare service models through partnerships between health systems and digital health platforms are increasing access to healthcare services. Virtual clinical trials for women's health conditions are reducing costs and speeding up new products.

Recent Developments:

-

2025: Maven Clinic introduced their virtual women’s health platform into 15 additional countries, having served over 2,000 companies worldwide through employer health programs. Maven’s platform allows remote consultations with gynecologists, fertility doctors, and mental health experts specialized in women's issues.

-

2025: Hologic announced the launch of the advanced version of its Genius AI platform for digital mammography that showed an increased accuracy by 20% compared to traditional mammography readings in breast cancer detection.

-

2025: Organon developed a novel contraceptive implant that can transmit personal health data to a user via an accompanying app.

-

2025: Gennev provided hormone therapy prescribing services through an extended telehealth platform for menopausal health issues. Year-over-year increase in the number of menopause consultations from U.S. employer customers reached 180%.

-

2025: LYNPARZA (olaparib), a drug manufactured by AstraZeneca, was approved for expanded usage in ovarian cancer treatment due to BRCA mutations.

Women's Healthcare Market Key Players are:

-

Hologic Inc.

-

Bayer AG

-

AbbVie Inc.

-

Pfizer Inc.

-

Johnson & Johnson

-

Organon & Co.

-

AstraZeneca plc

-

Merck & Co. Inc.

-

Becton Dickinson and Company

-

Siemens Healthineers AG

-

GE HealthCare Technologies Inc.

-

Maven Clinic

-

Gennev Inc.

-

Ovia Health (Labcorp)

-

Flo Health Inc.

-

Clue (BioWink GmbH)

-

Progyny Inc.

-

CCRM Fertility

-

Kindbody Inc.

-

Tia Inc.

Women's Healthcare Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.20 Billion |

| Market Size by 2035 | USD 57.82 Billion |

| CAGR | CAGR of 11.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Age Group (Adolescents, Adults, Geriatric) • By Service Type (Diagnostics, Treatment & Therapeutics, Preventive Care, Telehealth, Others) • By Health Condition (Reproductive Health, Oncology, Mental Health, Cardiovascular, Bone Health, Others) • By End-User (Hospitals & Clinics, Specialty Centres, Home Care, Online Platforms) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Hologic Inc., Bayer AG, AbbVie Inc., Pfizer Inc., Johnson & Johnson, Organon & Co., AstraZeneca plc, Merck & Co. Inc., Becton Dickinson and Company, Siemens Healthineers AG, GE HealthCare Technologies Inc., Maven Clinic, Gennev Inc., Ovia Health (Labcorp), Flo Health Inc., Clue (BioWink GmbH), Progyny Inc., CCRM Fertility, Kindbody Inc., Tia Inc. |

Frequently Asked Questions

North America dominated the Women's Healthcare Market in 2025.

Diagnostics dominated with approximately 41.37% of revenues in 2025.

Rising health awareness and telehealth expansion are the primary growth drivers. AI-powered diagnostic innovation is further improving early detection rates for cancer and reproductive health conditions.

The Women's Healthcare Market was valued at USD 20.20 billion in 2025.

The Women's Healthcare Market is expected to grow at a CAGR of 11.09% from 2026 to 2035.

Get in Touch