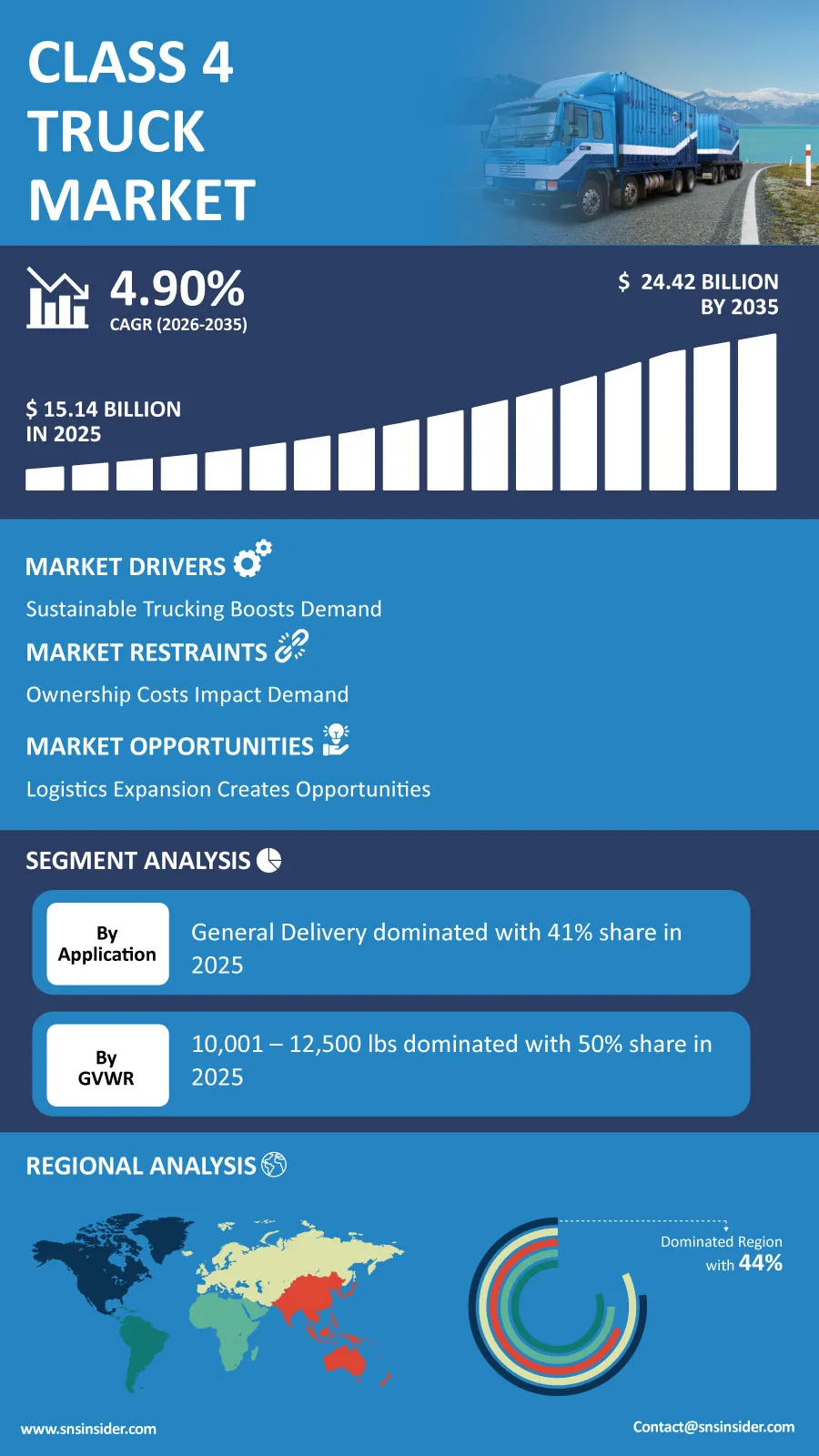

The global Class 4 Truck Market is entering a new phase of steady expansion as commercial fleet operators accelerate investments in efficient medium-duty transportation solutions to support urban logistics, infrastructure development, and sustainable freight operations. “According to a recent study by SNS Insider, the global Class 4 Truck Market size valued at USD 15.14 billion in 2025, is anticipated to grow to USD 24.42 billion by 2035, registering a CAGR of 4.90% over the 2026–2035 forecast period.”

Rapid development of regional distribution systems, increased need for last-mile deliveries, and ongoing fleet upgrades bode well for Class 4 trucks on a global scale. Companies in various industries, such as logistics, retailing, construction, utility companies, and municipalities have started to favor medium-duty trucks that provide the perfect balance of cargo-carrying capability, maneuverability, and efficiency.

Moreover, the sector of commercial transportation is slowly moving towards more environmentally friendly transport. With the implementation of tighter restrictions on greenhouse gas emissions and benefits provided to low emission commercial vehicles, there is an increase in the availability of hybrid and electric Class 4 trucks.

To Get Detailed Insights on the Class 4 Truck Market – Request a Sample Report

Fleet Modernization and Urban Logistics Create New Growth Opportunities

The evolution of urban freight transport systems continues to change the purchasing needs for the fleet. Businesses have begun to prioritize vehicles that are able to drive in highly urbanized areas while staying productive, flexible, and inexpensive to operate.

Digitalization is another trend that is taking shape within the industry. Fleets are increasingly incorporating connected vehicle solutions, predictive maintenance software, route optimization tools, and telematics to maximize utilization of assets and reduce downtime.

Fleet owners are increasingly looking at investments into the infrastructure for charging stations for electric vehicles alongside technological developments in batteries and other forms of alternative propulsion systems as another avenue to explore.

Finally, government incentives aimed at sustainable mobility and the adoption of new propulsion systems are prompting businesses to renew their fleets with advanced and environmentally-friendly Class 4 trucks.

Key Market Insights Reflect Evolving Commercial Transportation Demand

By propulsion type, conventional trucks accounted for approximately 50% of global market revenue in 2025, supported by their established reliability, widespread service infrastructure, and strong acceptance across commercial transportation applications.

Hybrid-powered Class 4 trucks are expected to emerge as the fastest-growing propulsion category during the forecast period as fleet operators seek improved fuel efficiency and lower emissions.

General delivery represented the largest application segment, contributing approximately 41% of market revenue in 2025 due to rising parcel volumes, expanding e-commerce fulfillment networks, and increasing demand for efficient urban freight transportation.

Refrigerated transportation is anticipated to witness the strongest growth through 2035 as pharmaceutical distribution, grocery delivery, and temperature-controlled logistics continue expanding globally.

The 10,001–12,500 lbs gross vehicle weight category has maintained market leadership with nearly 50% revenue share in 2025, while heavier Class 4 vehicle configurations are expected to gain momentum as commercial operators require greater payload flexibility.

Diesel-powered trucks continued to dominate the fuel segment with 56% market share during 2025, whereas electric trucks are projected to record the highest growth rate over the coming decade.

Technology Innovation and Sustainability Continue Reshaping Fleet Strategies

Fleet operators are increasingly considering operational efficiency and sustainability considerations. Manufacturers are addressing this by constantly improving safety systems, driver assistance features, lighter materials, and fuel-efficient drivetrains in vehicles.

The increased use of fleet management solutions that offer connection facilities allows companies to track vehicle performance, schedule maintenance, plan routes, and minimize costs. Such solutions are becoming increasingly important for companies with large commercial fleets operating in complex distribution networks.

Manufacturers are putting considerable effort into electric mobility, battery performance, battery charging capability, and hybrid vehicles to address new customer demands and regulations. With commercial transportation becoming increasingly technology-based, Class 4 trucks with improved connectivity and advanced operational capacities will be in high demand.

North America Accounted for 44% Market Share in 2025; Asia Pacific Forecast to Expand at the Highest CAGR by 2035

The North American region will hold around 44% share of the worldwide Class 4 Truck Market in 2025 owing to well-established logistics infrastructure, strong presence of e-commerce, significant investment in commercial fleets, and wide-scale usage of medium-duty trucks. The modernization of transportation networks and favorable policies of the governments in the region will aid in maintaining dominance in the coming years.

The Asia Pacific region will witness the fastest growth during the forecast period owing to the developments taking place on account of urbanization, industrialization, and e-commerce which are affecting the freight transport systems in the region. Favorable policies regarding transportation and infrastructure development in countries such as China and India will create a conducive environment for future growth.

Europe is continuously gaining strength with the increasing adoption of low-emission commercial vehicles, whereas the Latin America and the Middle East & Africa regions offer emerging potential due to the development of transportation infrastructure.

Industry Leaders Strengthen Competitive Position Through Product Innovation

Competition within the global Class 4 Truck Market remains dynamic as manufacturers continue introducing technologically advanced vehicles designed to improve fuel economy, enhance driver safety, and support evolving commercial transportation requirements. Strategic investments in electrification, intelligent fleet technologies, and sustainable vehicle platforms are expected to define competitive differentiation over the next decade.

Key companies operating in the global Class 4 Truck Market include Ford Motor Company, General Motors, Stellantis, Isuzu Motors Ltd., Hino Motors Ltd., Daimler Trucks North America LLC, Volvo Group, Navistar International Corporation, Mitsubishi Fuso Truck and Bus Corporation, PACCAR Inc., Iveco, MAN Truck & Bus AG, Scania AB, Tata Motors, Mahindra & Mahindra Ltd., Freightliner, Chevrolet, Ram Trucks, International Trucks, and Hercules Truck & Bus Co.

An SNS Insider analyst Santosh Bhul commented, "Growing urban freight demand, commercial fleet modernization, and accelerating investment in sustainable transportation technologies are creating favorable long-term opportunities for the Class 4 Truck Market. Manufacturers that combine electrification, digital connectivity, and operational efficiency will be well positioned to capture future industry growth."

About the Author

Get in touch