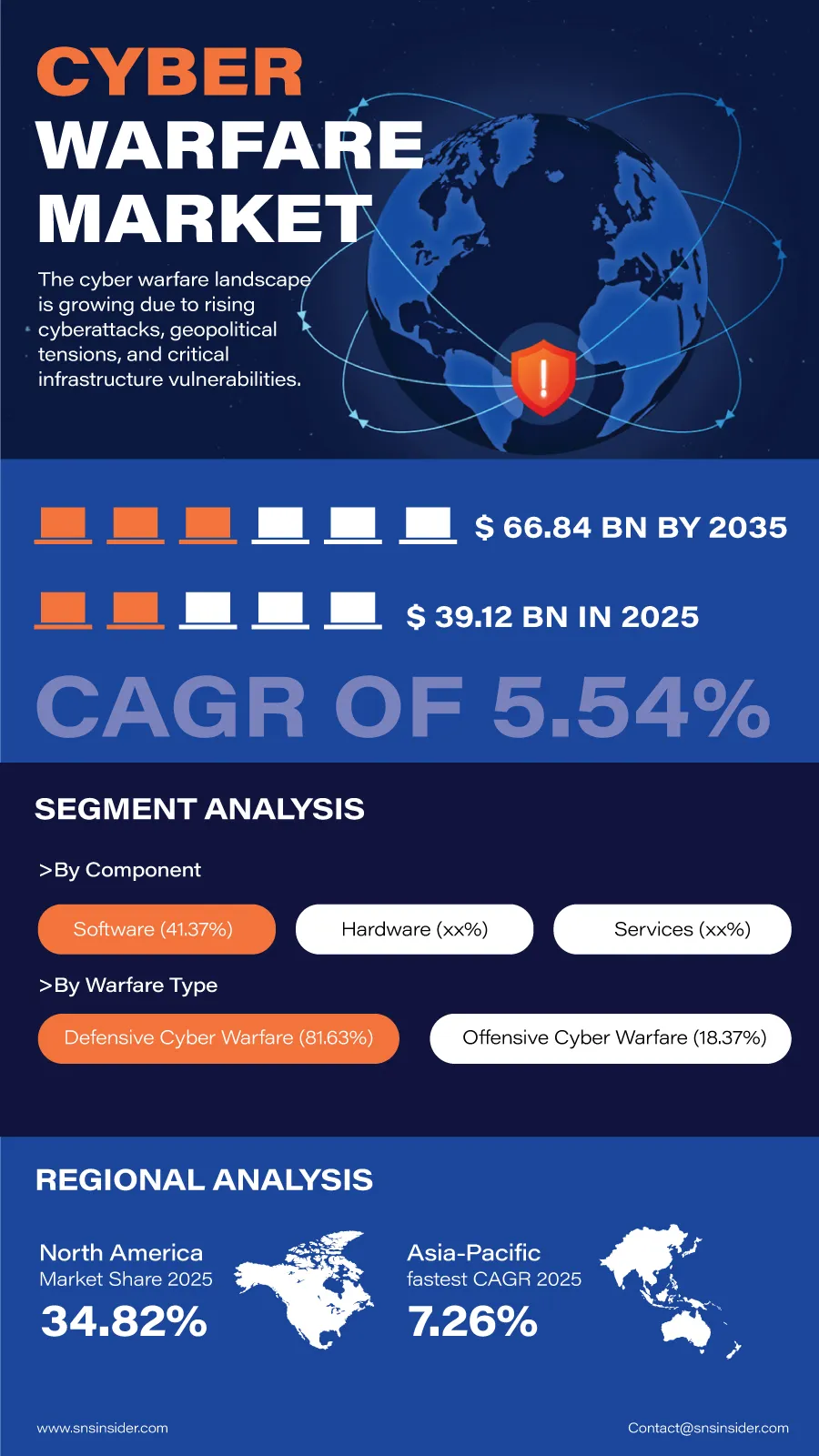

The global Cyber Warfare Market is poised for sustained growth over the coming decade as governments strengthen national cyber resilience, modernize defense capabilities, and expand investments in digital security infrastructure. According to a recent study by SNS Insider, the global Cyber Warfare Market size valued at USD 39.12 billion in 2025, is anticipated to grow to USD 66.84 billion by 2035, registering a CAGR of 5.54% over the 2026–2035 forecast period.

Rapid advancements in cybersecurity have elevated cyberspace as a key area of national security along with land, water, air, and space. The rise in cases of cyber espionage, ransomware, and attacks against government organizations and critical infrastructures is leading to an increased push for advanced technology in cybersecurity.

As more and more organizations depend upon cloud computing, connected devices, and artificial intelligence, the need for cybersecurity has emerged as a strategic necessity. Collaboration between public and private sectors, along with increasing regulations, keeps enhancing the demand for cyber warfare technology and solutions.

National Security Priorities Continue to Drive Market Expansion

Defense spending by governments around the world has increased in relation to cybersecurity programs that help mitigate cyber threats. Today’s militaries are developing more and more offensive and defensive capabilities in relation to cyber security, while also acquiring more advanced tools to detect and react to the evolving cyber threats.

Due to the fact that zero trust architecture is becoming more popular in the field of cybersecurity, more and more organizations are now able to increase their resistance to various types of attacks. Such technologies allow security teams to identify vulnerabilities and shorten the time needed to deal with the situation.

Also, increased collaboration between countries in terms of cybersecurity, investment in people, and critical infrastructure protection will provide new opportunities for vendors of such technologies.

Key Market Insights Highlight Shifting Demand Patterns

Based on component, software held 41.37% of global market revenue in 2025 due to rising demand for AI-driven threat detection, cyber intelligence platforms, and automated incident response solutions. Software is also expected to remain the fastest-growing component segment through 2035 as organizations prioritize scalable and continuously updated security capabilities.

By warfare type, defensive cyber warfare generated 81.63% of market revenue in 2025, reflecting widespread investment in protecting government networks, military systems, and enterprise infrastructure. Offensive cyber warfare is forecast to register the fastest growth with a CAGR of 6.82% as nations continue expanding strategic cyber capabilities.

In terms of application, government and defense organizations held a share of 36.72% of market revenue in 2025 owing to sustained military modernization and national cybersecurity initiatives. Critical infrastructure protection is projected to emerge as the fastest-growing application segment, supported by increasing efforts to secure energy, transportation, telecommunications, and water systems.

By end user, defense and military organizations dominated with a 34.62% of global revenue in 2025 because of ongoing investments in cyber operations and digital warfare capabilities. BFSI and corporate enterprises are expected to witness the fastest growth through 2035 as cybersecurity becomes a board-level priority for financial institutions and global businesses.

An Infographic Representation of the Global Cyber Warfare Market

AI and Advanced Analytics Transform Modern Cyber Defense

The field of artificial intelligence is changing the face of cyber warfare with its ability to create predictive threat intelligence, behavior analysis, automated malware detection, and quick incident response. Artificial intelligence tools can assist in analyzing large amounts of security data and detecting new attack vectors that may not have been noticed by conventional means.

Technology companies are also integrating advanced analytics tools, cloud-based security platforms, and identity management into cyber defense systems. This is making processes more efficient while also speeding up decision making within both military and civilian cyber security systems.

As cyber threats continue evolving in complexity and scale, organizations are increasingly adopting proactive security models focused on resilience, continuous monitoring, and rapid recovery.

Regional Markets Demonstrate Strong Strategic Investment

The share of North America in the global market revenue is forecast to be 34.82% in 2025, due to substantial government spending on cybersecurity solutions, high level of defensive capability, and presence of established security technology vendors. Further developments in modernization of the military cyber operations and cybersecurity protection systems ensure the leadership in the region.

Asia Pacific will be the leader in terms of growth rate, with CAGR of 7.26% throughout 2035. Geopolitical tensions, expansion of digital infrastructure, development of cyber capabilities, and increased government spending on cybersecurity projects in the region ensure high demand.

As digital transformation accelerates worldwide, governments across both developed and emerging economies are expected to continue strengthening cyber defense strategies to safeguard national security and economic stability.

Industry Participants Focus on Advanced Cyber Defense Innovation

The competitive landscape remains highly dynamic as the top players in the defense and cybersecurity industries keep on investing in AI, cyber intelligence, secure communication technologies, cloud security, and advanced threat detection systems. The formation of strategic alliances with governments plays a crucial role in increasing cyber resilience in the world.

Key companies operating in the global Cyber Warfare Market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, The Boeing Company, Airbus Defence and Space, Thales Group, BAE Systems plc, General Dynamics Corporation, L3Harris Technologies Inc., Booz Allen Hamilton, Leidos Holdings, Inc., SAIC, Palantir Technologies Inc., CrowdStrike Holdings, Palo Alto Networks, ManTech International, CACI International, Leonardo S.p.A., Saab AB, and Kratos Defense & Security Solutions.

An SNS Insider analyst Santosh Bhul commented, “Cyber warfare has become an indispensable pillar of modern national defense as governments confront increasingly sophisticated digital threats. Organizations that advance AI-enabled cybersecurity, resilient infrastructure protection, and integrated cyber defense capabilities will be well positioned to capitalize on growing global demand over the coming decade.”

About the Author

Get in touch