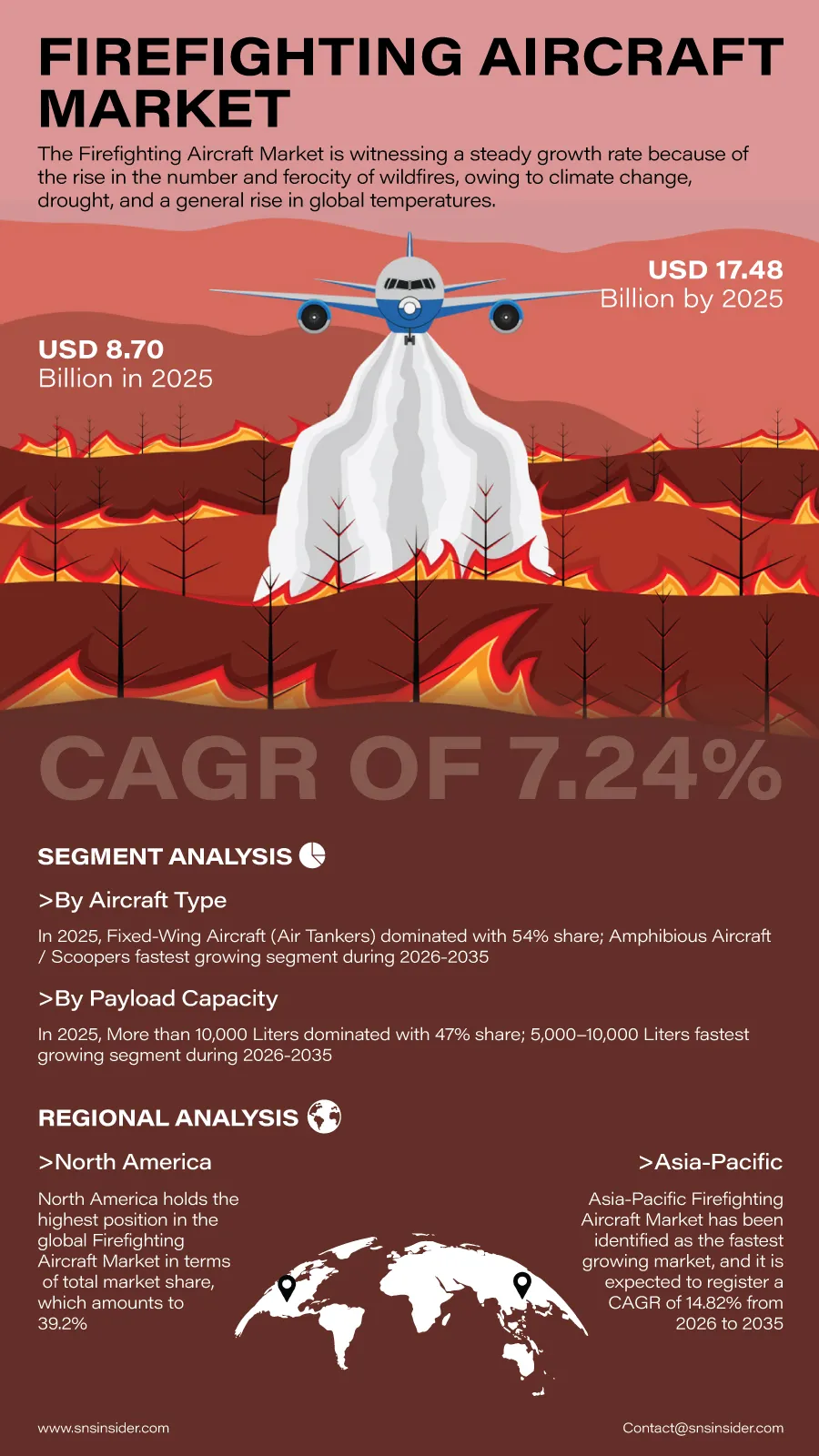

The global Firefighting Aircraft Market is poised for sustained expansion as governments and emergency management agencies strengthen aerial firefighting capabilities to address increasingly severe wildfire events. According to a recent study by SNS Insider, the global Firefighting Aircraft Market size valued at USD 8.70 billion in 2025, is anticipated to grow to USD 17.48 billion by 2035, registering a CAGR of 7.24% over the 2026–2035 forecast period.

The rising number of long wildfire seasons, along with the shift in climatic changes and growth of the wildland urban interface, is leading to a need for customized aircrafts that would serve as firefighting equipment. Public authorities have been focusing on purchasing aircrafts that would respond quickly to fire-related disasters.

Aircraft manufacturers have also been coming up with more technologies that will help increase mission efficiency through intelligent navigation, thermal vision, and real-time situation awareness. The technologies have been of great benefit to firefighters who have managed to improve their aerial coordination through them.

Fleet Modernization Continues to Create New Growth Opportunities

Global governments are enhancing their strategies for disaster preparedness by replacing old fire-fighting airplanes with newer models that have better capabilities regarding payload capacity, fuel consumption, and flexibility. Programs on wildfire management have resulted in favorable circumstances for buying such aircrafts.

Collaboration between various government agencies and organizations offering aerial firefighting services privately is increasingly contributing to the growth of the market. Deployment of the fleets based on contractual agreements allows increasing firefighting efforts in the most critical times of wildfires occurrence.

At the same time, advances in digital wildfire monitoring, artificial intelligence, and aerial mapping technologies are improving mission planning, allowing firefighting teams to respond more effectively to evolving fire conditions.

Key Market Insights Highlight Shifting Demand Patterns

By aircraft type, fixed-wing aircraft (air tankers) are forecast to dominate the total revenue share at 54% in 2025, owing to their capacity to carry huge amounts of water and retardants in a vast area of wildfires. The amphibious aircraft and scoopers will experience the fastest growth rate up to 2035, as agencies look for quicker turnarounds using the nearby lakes or reservoirs.

Based on payload capacity, aircraft capable of carrying more than 10,000 liters are forecast to represent 47% of market revenue in 2025, reflecting their importance in combating large-scale forest fires. The 5,000–10,000-liter segment is anticipated to witness the fastest growth owing to its balance between operational flexibility and suppression efficiency.

In terms of application, fire suppression through water and retardant dropping is expected to contribute 62% of market revenue in 2025. Meanwhile, surveillance and fire mapping are projected to experience the strongest growth as emergency agencies increasingly deploy advanced imaging technologies to improve wildfire detection and operational planning.

By end user, government and forestry agencies are anticipated to account for 59% of market revenue in 2025, supported by continued public investment in wildfire preparedness. Private aerial firefighting operators are forecast to grow at the fastest pace as outsourcing becomes an increasingly important component of emergency response strategies.

Advanced Technologies Strengthen Wildfire Response Capabilities

There is an increasing advantage of the incorporation of the use of new-age surveillance tools for the provision of real-time intelligence while on firefighting operations. Thermal cameras, infrared cameras, satellite communication, and communication tools have assisted firefighters to better understand the nature of fires and allocate air support accordingly.

Multi-role aircraft capable of supporting fire suppression, reconnaissance, rescue operations, and logistical support are also gaining popularity as emergency management organizations seek greater versatility from aerial assets while optimizing fleet utilization.

Regional Markets Continue Expanding Fire Management Investments

North America is anticipated to represent 39.2% of the worldwide market revenue share by 2025, driven by the adoption of effective wildfire management services, government funding, and efficient firefighting aircraft throughout the U.S. and Canada.

The Asia Pacific region is estimated to be the fastest-growing region over the forecast period due to the increased number of wildfires, disaster management programs, increasing aerial firefighting investment, and fleet replacement programs.

As countries continue strengthening emergency preparedness and forest protection programs, investments in specialized firefighting aircraft are expected to accelerate across both developed and emerging economies.

Industry Participants Focus on Innovation and Fleet Expansion

The competition is still intense as manufacturers keep working on the upgrade of their aircrafts in terms of technology and fire-fighting capabilities. They keep improving the payload capacity of their aircrafts, improving the performance of aircrafts, and creating surveillance systems for emergency situations.

Key companies operating in the global Firefighting Aircraft Market include Lockheed Martin Corporation, De Havilland Aircraft of Canada Limited, Textron Inc. (Bell Helicopter), Airbus SE, Boeing Company, Leonardo S.p.A., Viking Air Ltd., ShinMaywa Industries, Ltd., Beriev Aircraft Company, Conair Group Inc., Coulson Aviation, Bridger Aerospace Group Holdings, Inc., Erickson Incorporated, Aero-Flite, Inc., 10 Tanker Air Carrier, LLC, Neptune Aviation Services, Inc., Air Tractor Inc., Dauntless Air, Inc., HeliQwest Aviation, and Kaman Corporation.

An SNS Insider analyst Santosh Bhul commented, “The increasing intensity of wildfire events, combined with continued investments in fleet modernization and advanced aerial firefighting technologies, is creating long-term growth opportunities for the industry. Manufacturers delivering higher operational efficiency, mission versatility, and next-generation surveillance capabilities will be well positioned as governments strengthen wildfire response infrastructure worldwide.”

About the Author

Get in touch