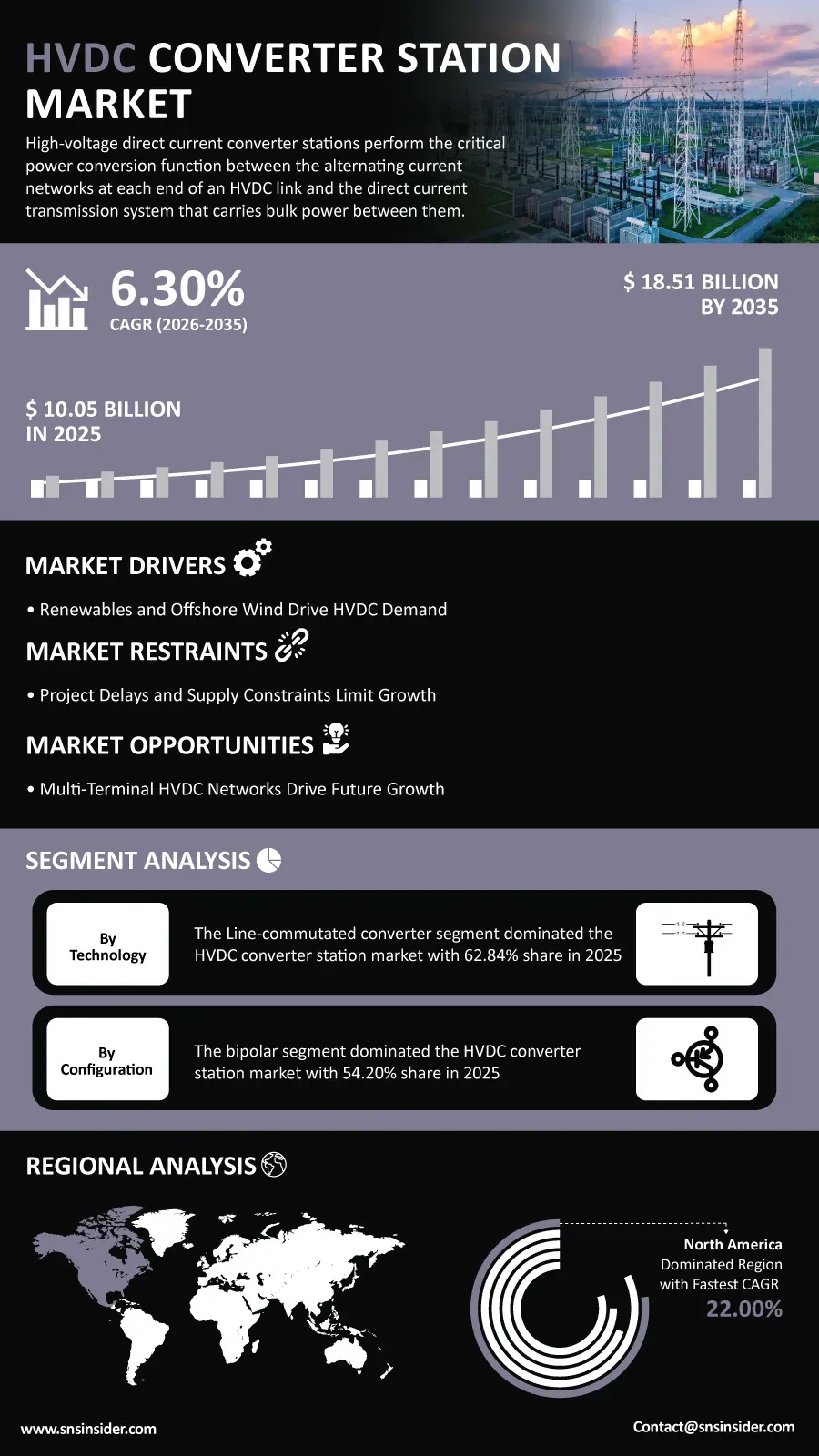

The global HVDC Converter Station Market is poised for steady expansion over the coming decade as utilities, transmission operators, and governments accelerate investments in modern power infrastructure to support renewable energy integration and long-distance electricity transmission. According to a recent study by SNS Insider, the global HVDC Converter Station Market size valued at USD 10.05 billion in 2025, is anticipated to grow to USD 18.51 billion by 2035, registering a CAGR of 6.30% over the 2026–2035 forecast period.

With greater interconnections of the electricity networks and generation plants built at a larger distance from demand centers, there is a rise in the importance of converter stations in electricity systems. Converter stations allow for the effective interconversion of the AC system and DC system of electricity, providing for the effective transmission of power over long distances.

Goals related to energy transition, modernizing power grids, and fast expansion of offshore wind projects drive transmission network operators to invest in HVDC technology. The growing need for power transmission technologies that are flexible, controllable, and large-scale ensures that there is ongoing demand for converter stations equipment providers.

To Get Detailed Insights on the HVDC Converter Station Market – Request a Sample Report

Renewable Energy Expansion Drives Long-Term Market Growth

The increasing trend towards decarbonizing energy supply is leading to a significant increase in the requirements for the development of the latest transmission infrastructure that will allow transmitting power generated by renewable sources located far away from population centers.

Development of offshore wind power plants is likely to become one of the key drivers of HVDC penetration in the industry. Increasing the distance from coast to coast and increasing size of projects makes conventional AC solutions uneconomical; hence, HVDC solutions are gaining more attention from project developers.

At the same time, national authorities support the development of initiatives aimed at increasing the capacity of the transmission infrastructure for improving energy security and grid stability as well as satisfying the increasing demand for power generation.

Key Market Insights Highlight Shifting Demand Patterns

By technology, line Commutated Converters (LCC) based converter systems are expected to generate 62.84% of the worldwide market revenue in 2025 owing to their extensive history of successful installations, low costs for higher power ratings, and capability of large transmission installations. Voltage Source Converters (VSC) converters are likely to witness the highest growth until 2035 due to rising focus on grid flexibility, reactive power management, and offshore renewable integration.

Based on configuration, bipolar systems are anticipated to contribute 54.20% of market revenue in 2025 owing to their operational reliability and widespread use in long-distance transmission networks. Multi-terminal configurations are forecast to experience the fastest growth as utilities pursue more interconnected and resilient HVDC network architectures.

In terms of power rating, the 1000 MW to 3000 MW segment is expected to account for 35.80% of market revenue in 2025, supported by extensive deployment across regional transmission projects. Systems above 3000 MW are projected to witness the highest growth rate as countries invest in ultra-high-capacity transmission corridors.

By application, long-distance power transmission is forecast to represent 42.84% of market revenue in 2025 due to ongoing investments in interregional energy transfer infrastructure. Offshore wind farm grid integration is expected to emerge as the fastest-growing application segment as global offshore renewable installations continue expanding.

Digital Technologies Enhance Grid Reliability and Efficiency

Technological innovation is transforming the HVDC converter station landscape. Utilities are increasingly incorporating artificial intelligence, digital twins, predictive maintenance systems, and advanced monitoring platforms to improve operational performance and asset management.

Modern converter stations are being designed with modular architectures and advanced control systems that support faster fault detection, enhanced reliability, and optimized power flow management. These capabilities are becoming increasingly important as power networks grow more complex and renewable energy penetration rises.

Manufacturers are also focusing on improving converter efficiency, reducing equipment footprints, and enhancing system flexibility to support future multi-terminal and grid-forming applications.

Asia Pacific Captures 36.00% of Global HVDC Converter Station Market, with China Contributing 46.28% of Regional Revenue

The Asia Pacific region will continue to be the most dominant and rapidly growing market during the forecast period. The region will command a market share of about 36% owing to heavy transmission investment in countries like China, India, and several other developing economies.

Europe is also an important market due to its strong offshore wind power generation, electricity trading between nations, and investments made towards energy security. Projects planned to connect offshore North Sea wind generation to onshore power grids will lead to high demand for converter stations.

North America is witnessing growth in HVDC installations as utilities build their power grids to increase transmission capacity and improve grid efficiency.

Industry Participants Focus on Innovation and Network Expansion

Competition within the HVDC converter station market remains centered on technological innovation, project execution capabilities, and the development of next-generation transmission solutions. Industry leaders are investing heavily in advanced converter technologies, digital grid solutions, and multi-terminal network capabilities to address evolving utility requirements.

Key companies operating in the global HVDC Converter Station Market include Hitachi Energy Ltd. (ABB Power Grids), Siemens Energy AG, GE Vernova Inc., Mitsubishi Electric Corporation, Toshiba Corporation, NR Electric Co. Ltd., C-EPRI Electric Power Engineering Co. Ltd., XJ Group Corporation, Bharat Heavy Electricals Ltd. (BHEL), Hyosung Heavy Industries Corp., Alstom SA (GE Grid), Nissin Electric Co. Ltd., Prysmian Group, Nexans SA, LS Electric Co. Ltd., Crompton Greaves Power (CG Power), TBEA Co. Ltd., China Electric Equipment Group, Nari Technology Co. Ltd., and Eaton Corporation PLC.

An SNS Insider analyst Sushant Kadam commented, “The accelerating transition toward renewable energy, combined with growing demand for long-distance electricity transmission and grid modernization, is creating substantial opportunities for HVDC converter station providers. Companies that invest in advanced converter technologies, digital grid capabilities, and scalable network solutions will be best positioned to benefit from the next phase of global transmission infrastructure development.”

About the Author

Get in touch