Automotive Digital Cockpit Market Report Scope & Overview:

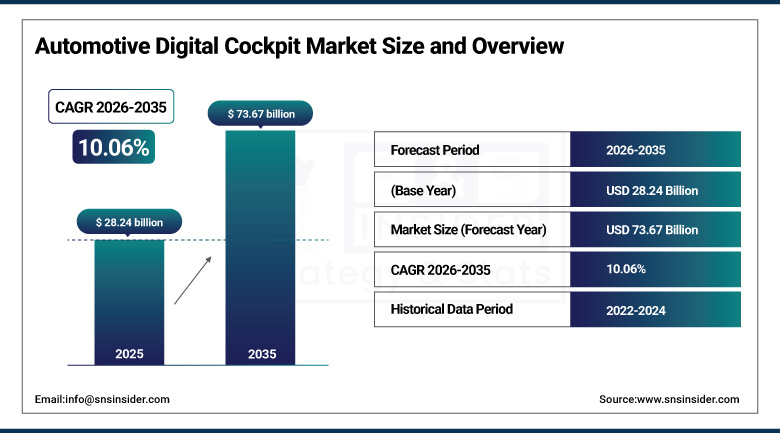

The Automotive Digital Cockpit Market was valued at USD 28.24 Billion in 2025 and is expected to reach USD 73.67 Billion by 2035, growing at a CAGR of 10.06% from 2026 to 2035.

The Automotive Digital Cockpit Market is growing rapidly due to the fact that vehicle platforms are becoming increasingly connected and software defined. Consumers are now asking for larger screens, integrated infotainment systems, digital instrument clusters, and driver monitoring in affordable and luxury cars. The demand for connected in-cabin experience and intelligent Human Machine Interface is constantly increasing while automakers integrate infotainment systems, driver assistance features, and vehicle controls into the domain controller platform in order to reduce bill of materials costs while providing the possibility for over-the-air updates. Today, more than seventy percent of new passenger cars have installed an automotive digital cockpit.

Elektrobit introduced its software-defined vehicle strategy at CES in January 2025 which includes an open source portfolio of cloud-to-cockpit solutions that allow developing next generation of digital ecosystems in cars.

Market Size and Forecast

-

Market Size in 2026E: USD 31.08 Billion

-

Market Size by 2035: USD 73.67 Billion

-

CAGR: 10.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information Automotive Digital Cockpit Market - Request Free Sample Report

Automotive Digital Cockpit Market Trends

-

Carmakers are merging infotainment, driver-assistance, and vehicle controls into domain controller platforms to lower costs.

-

Battery-electric architectures continue accelerating adoption by supplying the power and bandwidth high-resolution displays require.

-

Growth in electric vehicles is accelerating demand for digital interfaces that provide energy insights and real-time vehicle information.

-

AI-integrated driver assist clusters continue accelerating growth driven by autonomous driving and connected vehicle requirements.

-

5G connectivity and cloud-based vehicle interfaces continue enabling real-time updates and over-the-air software enhancements.

United States Automotive Digital Cockpit Market Outlook

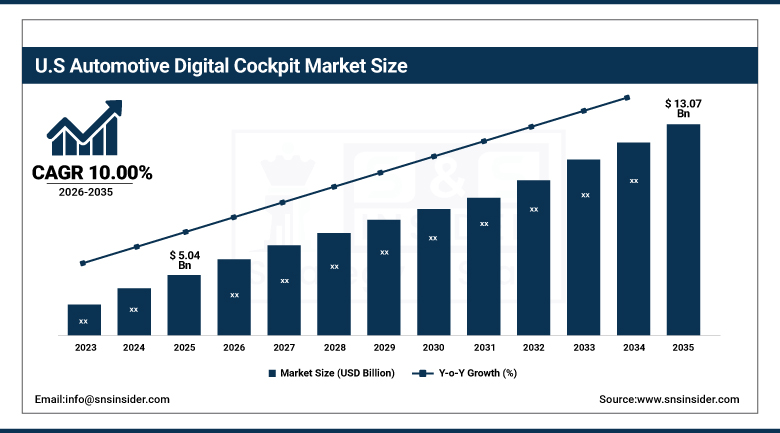

The United States Automotive Digital Cockpit Market was valued at USD 5.04 Billion in 2025 and is expected to reach USD 13.07 Billion by 2035, growing at a CAGR of 10.00% from 2026 to 2035.

The United States was a dominant player in North America in terms of automotive digital cockpit demand, driven by robust consumer expectations for smooth connectivity, AI-powered customization, and entertainment in the country's top automotive markets. The increasing adoption of multi-display architecture, cockpit domain controllers, and enhanced human-machine interface technology to distinguish vehicles kept driving the regional demand through the year.

Qualcomm Technologies, located in San Diego, California, steadily expanded its range of automotive cockpit chipsets and platforms in 2025, further establishing itself as a dominant supplier of computing capabilities in next-generation digital instrument clusters, infotainment systems, and driver monitoring solutions for American and worldwide automakers.

Automotive Digital Cockpit Market Segment Analysis

-

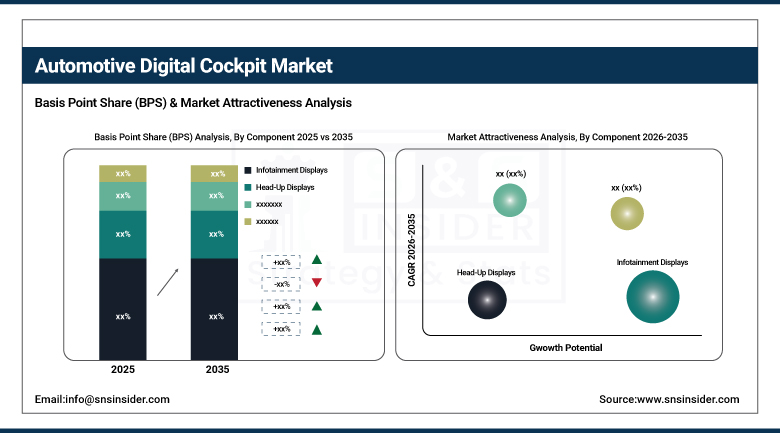

By Component, the Infotainment Displays segment held the largest share in 2025, while the Head-Up Displays segment is the fastest growing, with a CAGR of approximately 15.60%.

-

By Vehicle Type, the Passenger Car segment held approximately 89.90% share in 2025, while the Commercial Vehicle segment is the fastest growing.

-

By Display Size, the 5-10 Inch segment held approximately 62.80% share in 2025, while the Above 10 Inch segment is the fastest growing.

-

By EV Type, the Internal Combustion Engine segment held the larger share in 2025, while the Battery Electric Vehicle segment is the fastest growing, with a CAGR of approximately 16.30%.

By Component, Infotainment Displays led the market, Head-Up Displays grew fastest

The Infotainment Displays segment dominated the component category in 2025, driven by OEM focus on immersive HMI, larger multi-screen layouts, advanced head units, centralized controls, smartphone integration, and continuous OTA-enabled feature enhancements. That expanding connectivity ecosystem continues keeping infotainment displays firmly at the top of the broader component segmentation across nearly every major digital cockpit deployment worldwide.

The Head-Up Displays segment is projected to grow at the fastest CAGR of approximately 15.60% during the forecast period, as augmented reality HUD technology continues expanding beyond premium vehicles into increasingly mainstream vehicle segments. Rising integration of advanced driver assistance systems that benefit from windshield-projected navigation and safety alerts continues pushing this component category's growth rate ahead of the broader component segmentation.

By Vehicle Type, Passenger Car led the market, Commercial Vehicle grew fastest

The Passenger Car segment held the largest vehicle type share in 2025, at approximately 89.90%, anchored by the sheer scale of global passenger vehicle production that continues representing the overwhelming majority of automotive digital cockpit demand. That established, large-volume production base keeps passenger cars firmly at the top of the broader vehicle type segmentation across nearly every major automotive manufacturing region worldwide.

The Commercial Vehicle segment is projected to grow at the fastest CAGR during the forecast period, as fleet operators increasingly adopt digital instrument clusters and driver information systems to improve operational efficiency and safety. Rising commercial vehicle digitalization continues pushing this vehicle type category's growth rate ahead of the broader vehicle type segmentation.

By Display Size, 5-10 Inch led the market, Above 10 Inch grew fastest

The 5-10 Inch segment held the largest display size share in 2025, at approximately 62.80%, widely used across compact, mid-range, and select premium vehicles, and crucial to digital instrument clusters, infotainment displays, and center console applications. That broad applicability across vehicle price tiers keeps this display size firmly at the top of the broader display size segmentation across the majority of digital cockpit installations worldwide.

The Above 10 Inch segment is projected to grow at the fastest CAGR during the forecast period, driven by consumer demand for immersive, high-definition digital cockpit experiences and larger infotainment displays. Rising integration of curved and flexible display technologies into premium and electric vehicles continues pushing this display size category's growth rate ahead of the broader display size segmentation.

By EV Type, Internal Combustion Engine led the market, Battery Electric Vehicle grew fastest

The Internal Combustion Engine segment held the larger EV type share in 2025, anchored by the substantial existing global vehicle fleet that continues representing the majority of current digital cockpit installations. That established, large installed base keeps internal combustion vehicles firmly at the top of the broader EV type segmentation even as electric vehicles capture a growing share of new digital cockpit deployments.

The Battery Electric Vehicle segment is projected to grow at the fastest CAGR of approximately 16.30% during the forecast period, as battery-electric architectures continue accelerating adoption by supplying the power and network bandwidth needed for high-resolution displays and AI functions. Growth in electric vehicles continues accelerating the need for digital interfaces that provide energy insights and real-time vehicle information, pushing this EV type category's growth rate ahead of the broader EV type segmentation.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

38.10% |

|

North America |

United States |

84.90% |

|

Europe |

Germany |

27.60% |

|

Middle East & Africa |

UAE |

26.40% |

|

Latin America |

Brazil |

37.30% |

North America Automotive Digital Cockpit Market Insights

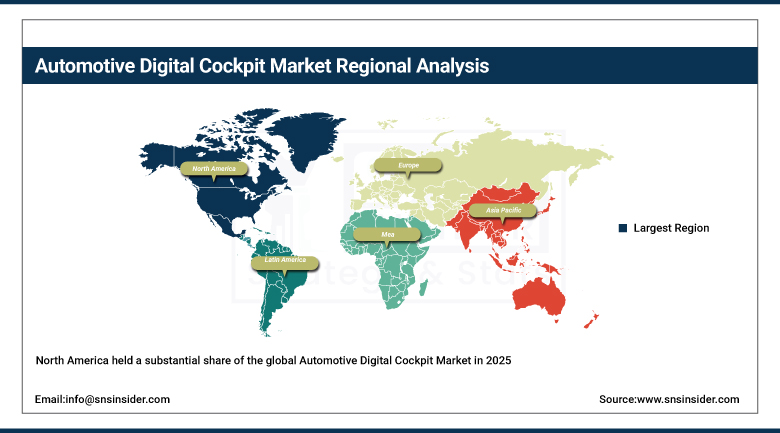

North America held a substantial share of the global Automotive Digital Cockpit Market in 2025, supported by strong consumer expectations for seamless connectivity, AI-driven personalization, and rich infotainment across the region. Automakers integrating multi-display layouts and cockpit domain controllers to differentiate vehicles continued reinforcing regional demand throughout the year.

The United States accounted for roughly 84.90% of regional revenue, reflecting its concentration of leading digital cockpit technology suppliers and software-first automotive OEMs. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding connected vehicle adoption, keeping North America among the more commercially significant regional markets for automotive digital cockpits throughout the year.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Automotive Digital Cockpit Market Insights

The Europe region witnessed a significant market share in the Automotive Digital Cockpit Market in 2025 owing to the prevalence of premium car manufacturing and strict safety regulations in the region. The country of Germany captured about 27.60% of the regional market revenue owing to the presence of premium car manufacturers which invest in digital cockpit solutions.

The countries of France, the United Kingdom, and Italy witnessed a similar trend in terms of market growth, as premium and electric vehicle manufacturing drove the demand for automotive digital cockpit solutions within the regions largest manufacturing hubs.

Asia Pacific Automotive Digital Cockpit Market Insights

Asia Pacific dominated the market for Automotive Digital Cockpit globally in 2025 at an approximate value of 44.20% and also is forecasted to grow at the highest growth rate till 2035 on account of accelerating trends of urbanization along with the increasing disposable incomes of the major economies within the region. In view of the continuous trend of electric mobility that the government of China has been taking, there has been tremendous growth in the sales of the EVs having the head up displays, voice assistants, and infotainment systems.

China contributed about 38.10% of the revenues within the region where the digital cockpit adoption grew up to 66% in 2023 and is anticipated to go up to 80% by 2025 owing to the focus on software and intelligent hardware integration. Japan and South Korea have contributed significantly towards the regional demand for automotive digital cockpit in the region owing to their own automobile electronics and display manufacturing industry.

MEA & Latin America Automotive Digital Cockpit Market Insights

The Middle East and Africa region recorded steady growth in automotive digital cockpit adoption in 2025, driven by expanding vehicle assembly investment and growing consumer demand for premium vehicle features across the Gulf states in particular. The UAE accounted for roughly 26.40% of regional revenue, supported by rising consumer demand for advanced digital cockpit technology.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.30% of regional revenue, where growing domestic vehicle production continued to support category growth. Mexico and Argentina followed a similar trajectory as regional automotive manufacturing capacity expanded further through the remainder of the forecast period.

Growth Drivers: Software-defined vehicle adoption and connected experience demand

Rising demand for connected in-cabin experiences and advanced HMI systems continues to be the central force behind automotive digital cockpit market growth. Automakers moving toward software-driven vehicle platforms, increasing adoption of large displays, integrated infotainment, and driver monitoring technologies continue reinforcing structural demand growth across nearly every major automotive manufacturing region worldwide.

The quick convergence of ADAS, infotainment, and instrument clusters is constantly contributing to cockpit centralization, hence boosting the demand for automotive digital cockpits even more. Progress in terms of graphics processing, centralized computing, and cloud computing is continually improving user interfaces and updating the software continuously, with the growing number of electric vehicle production also boosting demand for such systems.

Restraints: High integration costs and cybersecurity compliance burden

The substantial cost of integrating multiple high-resolution displays, domain controllers, and advanced HMI software continues restricting adoption among cost-sensitive vehicle segments and price-conscious automakers. That cost barrier continues concentrating the most advanced digital cockpit technology within premium and technologically differentiated vehicle categories.

Cybersecurity concerns continue posing a genuine restraint, as increasingly connected, software-driven cockpit systems expand the potential attack surface that automakers must secure against malicious actors. That security requirement continues requiring substantial ongoing investment in encryption, authentication, and intrusion detection capability across the broader digital cockpit ecosystem.

Opportunities: Domain controller consolidation and health monitoring integration

Growing adoption of domain controller platforms that merge infotainment, driver-assistance, and vehicle controls presents substantial opportunity for suppliers positioned to deliver these consolidated, cost-reducing architectures. Suppliers capable of delivering genuinely unified domain controller solutions stand to capture a growing share of demand as automakers continue seeking to lower bill-of-materials costs.

Continued integration of health and wellness monitoring, alongside the rise of mobility-as-a-service and smart city integration, presents a further significant growth avenue for digital cockpit technology providers. Companies capable of delivering genuinely differentiated, health-aware cockpit experiences stand to capture meaningful new revenue streams through 2035.

Recent Developments:

-

2025: AUO and BHTC unveiled a next-generation smart cockpit concept in January featuring advanced LED and MicroLED display technology, showcasing the collaborative innovation happening between display manufacturers and automotive electronics specialists.

-

2025: Hyundai Mobis continued advancing its cockpit domain controller and display technology portfolio, targeting automakers seeking integrated, software-defined digital cockpit platforms for next-generation vehicle models.

Automotive Digital Cockpit Companies are:

-

Robert Bosch GmbH

-

Continental AG

-

Denso Corporation

-

HARMAN International Industries, Incorporated

-

Aptiv PLC

-

Panasonic Corporation

-

Hyundai Mobis Co., Ltd.

-

Qualcomm Technologies, Inc.

-

Elektrobit Automotive GmbH

-

AU Optronics Corp.

-

Behr-Hella Thermocontrol GmbH

-

Samsung Electronics Co., Ltd.

-

Texas Instruments Incorporated

-

NXP Semiconductors N.V.

-

Renesas Electronics Corporation

-

Alpine Electronics, Inc.

-

Pioneer Corporation

-

Magna International Inc.

Automotive Digital Cockpit Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.24 Billion |

| Market Size by 2035 | USD 73.67 Billion |

| CAGR | CAGR of 10.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Infotainment Displays, Head-Up Displays) • By Vehicle Type (Passenger Car, Commercial Vehicle) • By Display Size (5-10 Inch, Above 10 Inch) • By EV Type (Internal Combustion Engine, Battery Electric Vehicle) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Robert Bosch GmbH, Continental AG, Denso Corporation, Visteon Corporation, HARMAN International Industries, Incorporated, Aptiv PLC, Panasonic Corporation, Hyundai Mobis Co., Ltd., Qualcomm Technologies, Inc., Elektrobit Automotive GmbH, AU Optronics Corp., Behr-Hella Thermocontrol GmbH, LG Electronics Inc., Samsung Electronics Co., Ltd., Texas Instruments Incorporated, NXP Semiconductors N.V., Renesas Electronics Corporation, Alpine Electronics, Inc., Pioneer Corporation, Magna International Inc. |

Frequently Asked Questions

The Automotive Digital Cockpit Market is expected to grow at a CAGR of 10.06% from 2026 to 2035.

The Automotive Digital Cockpit Market was valued at USD 28.24 Billion in 2025.

Rising demand for connected in-cabin experiences combined with the shift toward software-defined vehicle platforms is the major growth factor.

The Passenger Car segment held approximately 89.90% share in 2025.

Asia Pacific held the largest share of the Automotive Digital Cockpit Market in 2025, at approximately 44.20%, and was also the fastest-growing region.

Get in Touch