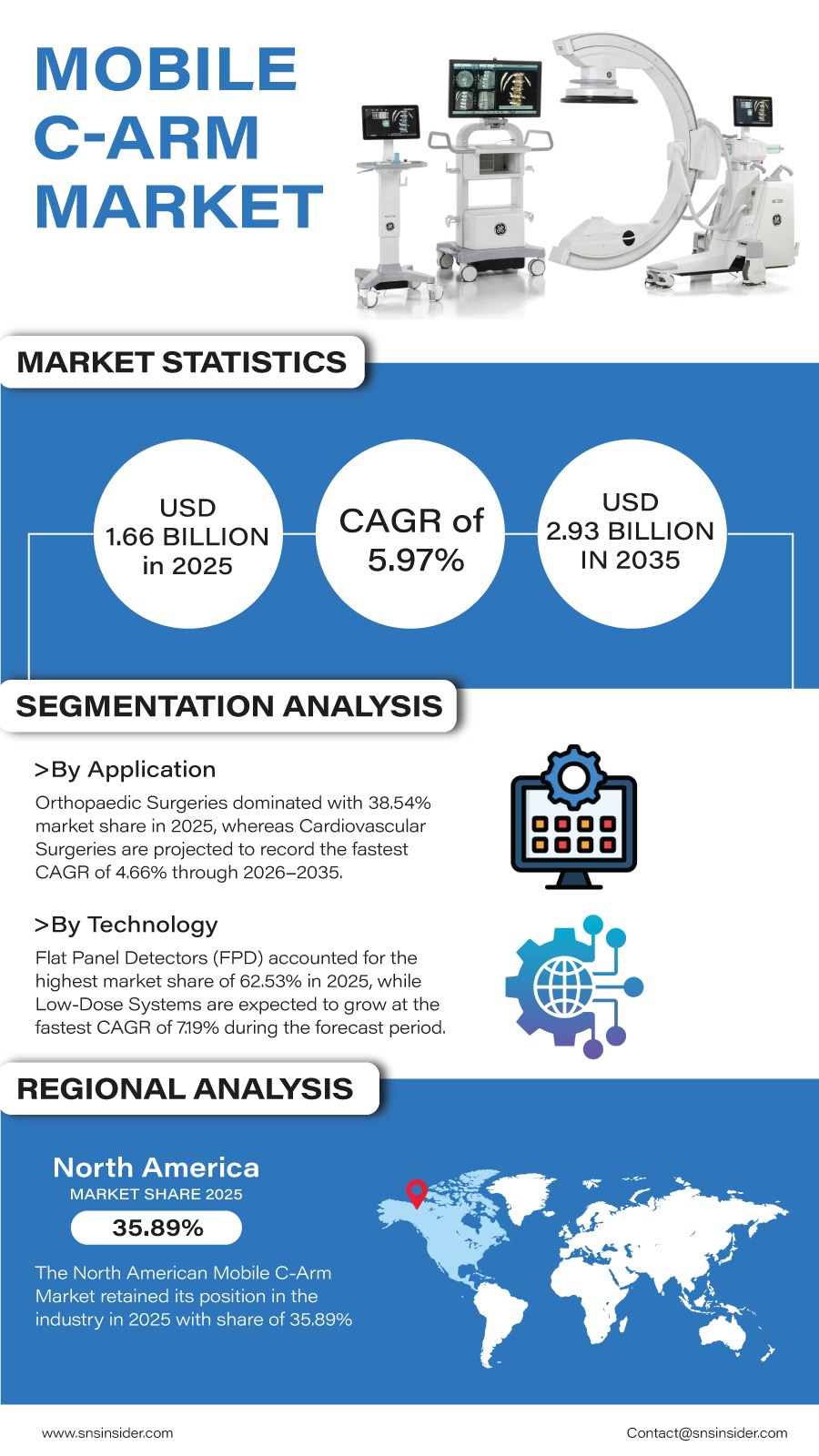

The global Mobile C-arm Market is expected to witness sustained growth as healthcare providers increasingly invest in advanced imaging systems that improve surgical precision and clinical efficiency. “According to a recent study by SNS Insider, the global Mobile C-arm Market size valued at USD 1.66 billion in 2025, is anticipated to grow to USD 2.93 billion by 2035, registering a CAGR of 5.97% over the 2026–2035 forecast period.”

Increased use of minimally invasive techniques in orthopedics, cardiology, pain treatment, and neurosurgery has created an increased demand for real-time imaging technologies. More operating theaters are being renovated to incorporate mobile imaging equipment that offers more flexibility and improved visualization during complicated surgeries.

Improved results from surgery while minimizing time and radiation exposure have made healthcare organizations prefer to update their facilities with new mobile c-arm machines featuring digital imaging technology.

To Get Detailed Insights on the Mobile C-arm Market – Request a Free Sample Report

Next-Generation Imaging Technologies Continue to Transform Surgical Care

Advanced technology developments have brought changes to the world of surgery imaging. New-generation mobile C-arm devices are fitted with smart image processing software, innovative detectors, improved radiation control, and integration with digital networks, thus facilitating more effective workflow processes.

Another trend to increase the demand for advanced imaging solutions is the growing popularity of hybrid ORs. Also, the development of such equipment is being driven by the increasing demand for mobility, ergonomic design, and high-quality images in both major medical institutions and ambulatory surgery centers.

With the increasing focus of healthcare systems on precision surgeries, the development of smaller and user-friendly platforms is currently a priority for manufacturers.

Key Market Insights Highlight Emerging Opportunities

Among product categories, full-size Mobile C-arm systems accounted for 70.63% of global market revenue in 2025, reflecting their extensive use across hospitals and specialized surgical departments for complex procedures requiring advanced imaging performance.

Meanwhile, mini Mobile C-arm systems are expected to register the fastest growth through 2035, expanding at a CAGR of 6.22%, driven by increasing utilization in outpatient orthopedic practices and ambulatory surgical environments.

Technology innovation continues to shape market dynamics. Flat Panel Detector (FPD) systems represented 62.53% of total market revenue in 2025, supported by superior image quality, faster image acquisition, and improved workflow efficiency. At the same time, low-dose imaging systems are projected to record the fastest growth at a CAGR of 7.19%, reflecting increasing emphasis on patient safety and radiation management.

Application trends further demonstrate the market's evolution. Orthopedic surgeries accounted for 38.54% of global revenue in 2025, maintaining their position as the largest clinical application segment. However, cardiovascular procedures are anticipated to witness the fastest growth, expanding at a CAGR of 4.66% throughout the forecast period, supported by increasing demand for minimally invasive cardiac interventions.

From an end-user perspective, hospitals captured 66.74% of total market revenue in 2025, while ambulatory surgical centers are expected to emerge as the fastest-growing segment, advancing at a CAGR of 6.34%, reflecting the continued migration of surgical procedures toward outpatient settings.

Increasing Surgical Volumes Drive Equipment Modernization

Healthcare organizations throughout the world are increasingly investing in surgical imaging solutions to enhance accuracy and efficiency. An increase in procedures within orthopedics, trauma medicine, vascular procedures, pain management, and neurosurgery is increasing the demand for more advanced intraoperative imaging solutions.

The growing integration of artificial intelligence, workflow automation, and digital connectivity into imaging systems is further supporting market expansion by helping clinicians optimize image acquisition, reduce procedure times, and enhance clinical decision-making.

Regional Markets Continue to Expand

The share of North America in the global market revenues was 35.89%, which is attributed to advanced healthcare facilities, increased preference for minimally invasive surgeries, and investment in imaging equipment. Reimbursement and innovation continue to be major factors in the dominance of this region.

On the other hand, Asia Pacific is expected to be the most promising region and is expected to grow at the highest CAGR of 7.47% until 2035. Investments in the health care sector, modernization of hospitals, increased surgery numbers, and the need for advanced imaging equipment provide many opportunities for growth.

Industry Leaders Focus on Innovation and Clinical Efficiency

Competition in the Mobile C-Arm market is still dynamic, with firms investing heavily in product development, imaging quality, AI incorporation, and workflow technologies. Product launches, medical alliances, and globalization will play a critical role in competitive strategies.

Leading companies operating in the global Mobile C-arm market include Siemens Healthineers, GE HealthCare, Philips, Ziehm Imaging, Canon Medical Systems, Hologic, Shimadzu Corporation, Medtronic, FUJIFILM Holdings, and United Imaging Healthcare.

An SNS Insider analyst Parry Kardani commented, "The future of surgical imaging will be defined by greater precision, smarter workflow automation, and broader accessibility of advanced visualization technologies. As healthcare providers continue expanding minimally invasive procedures, demand for next-generation Mobile C-arm systems is expected to remain strong across hospitals and outpatient surgical facilities."

An Infographic Representation of the Global Mobile C-arm Market

About the Author

Get in touch