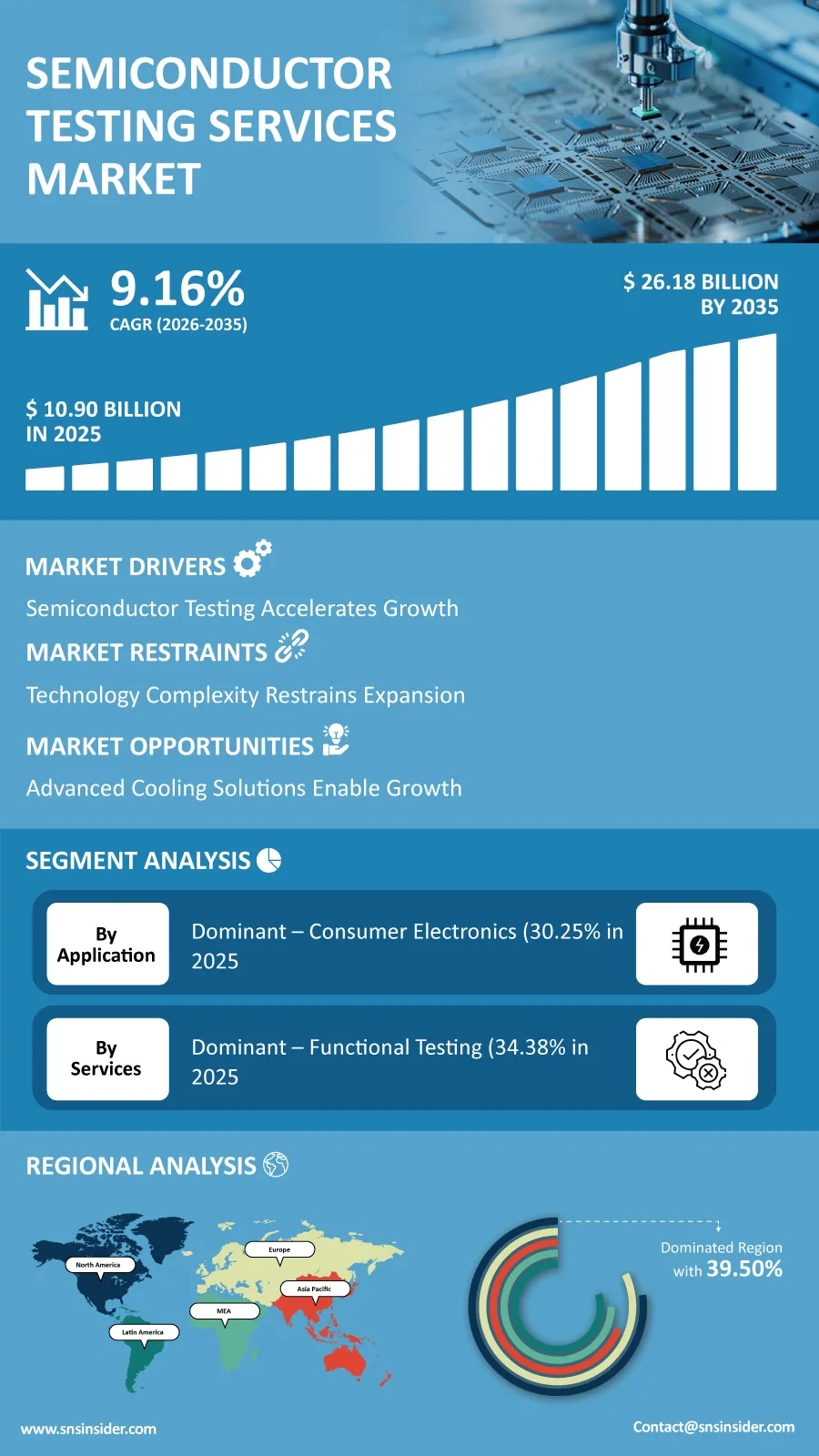

The worldwide market for Semiconductor Testing Services is set to experience rapid growth during the next decade due to increasing emphasis by semiconductor producers on product quality, validation, and reliability through complex chip designs. According to a recent study by SNS Insider, the global Semiconductor Testing Services Market size valued at USD 10.90 billion in 2025, is anticipated to grow to USD 26.18 billion by 2035, registering a CAGR of 9.16% over the 2026–2035 forecast period.

The rise in usage of AI technology, HPC, AVs, 5G infrastructure, and high-tech consumer electronics has raised the complexity of semiconductor components, making their testing a crucial step in the manufacturing process. As new chip technologies emerge, the services of testing firms are being improved to guarantee their reliability while minimizing risks for production and accelerating time-to-market.

In addition, the semiconductor industry has been profiting from constant investments in automated testing solutions, AI-based analytics, advanced packaging testing, and highly skilled engineers. Such innovations allow semiconductor companies to improve production efficiency while following stricter quality requirements.

To Get Detailed Insights on the Semiconductor Testing Services Market – Request a Sample Report

Advanced Validation Technologies Continue to Strengthen Market Growth

The fast pace of development within semiconductor fabrication technologies is making an increasing need for highly sophisticated testing methods, which would be able to guarantee validation of smaller, high-performing, and heterogeneous chips. Advanced functional, reliability, burn-in, and packaging level tests have been implemented in order to accommodate needs of applications demanding outstanding accuracy and reliability.

Another trend that has been contributing to growth of the market through outsourcing of testing services is the development of OSAT (Outsourced Semiconductor Assembly and Testing). This technology allows semiconductor companies to optimize their manufacturing expenses and at the same time gain access to special testing knowledge.

Additionally, inspection techniques through artificial intelligence, predictive analytics, and automated defect detection have been changing the testing process in that they increase efficiency, decrease turnaround times, and make manufacturing processes more efficient.

Key Market Insights Highlight Shifting Demand Patterns

Package technology wise, the Wafer Level Chip Scale Package (WLCSP) Testing is likely to hold 31.25% share of total revenue of the global market by 2025 due to extensive use of this technology in consumer electronics, telecommunication, and computing applications. The Flip Chip Package Testing technology segment is predicted to register fastest growth until 2035 driven by rising need for advanced packaging technologies for AI processors, automotive electronic chips, and high-performance computing.

Application wise, consumer electronics are expected to generate 30.25% revenue of the market by 2025 as production of smartphones, wearables, and connected devices continues to grow in number. The automotive segment is predicted to exhibit highest growth rate throughout the forecast period as electric vehicle technologies, ADAS, and autonomous driving technologies see increase in semiconductor content.

Service type wise, functional testing is estimated to constitute 34.38% revenue of the market by 2025 because of its importance in assessing performance of the chip prior to commercial use. Specialized testing services are expected to see highest growth as demand for advanced semiconductor packaging technologies and customized validation continues to rise.

As far as end users are concerned, OEM is expected to capture 39.50% of the total market revenue in 2025 owing to its large-scale emphasis on reliability and quality of products. The Contract Testing & Assembly Companies are expected to grow at the fastest rate in the coming years due to outsourcing of testing processes by the companies manufacturing semiconductors.

Artificial Intelligence and Advanced Packaging Drive Testing Innovation

In line with the evolution of semiconductor devices, there have been changes in testing methods that are shifting from traditional validation approaches. Artificial intelligence, machine learning, and predictive analytics are allowing testing providers to detect defects while enhancing yield management and cutting down manufacturing costs.

The fast adoption of next-generation packaging solutions, heterogeneous integration, and chiplets technology has also resulted in the increased need for testing that will be able to validate complicated semiconductor structures. Such innovations are anticipated to continue driving market development in the future.

The semiconductor industry is concurrently developing automated testing tools, digital twins, and data-driven quality control systems to boost productivity and accelerate development of the next generation of semiconductor products.

North America Secures 39.50% Global Market Revenue in 2025 as Asia Pacific Expands at a 10.74% CAGR Through 2035

In the year 2025, North America is anticipated to hold 39.50% of the worldwide market share revenue owing to its advanced semiconductor manufacturing processes, strong OEM operations, significant investment in R&D activities, and increased demand from the computing industry, automotive, telecom, and consumer electronics sectors.

The Asia Pacific region is forecasted to witness the highest growth rate among all regions in terms of its CAGR, which will be 10.74% until 2035. The reason for this rapid development is rapid expansion in semiconductor manufacturing operations, significant investment in advanced packaging plants, high production of consumer electronic products, and increasing demand for AI chips.

With the continued expansion of the capacity for semiconductor manufacturing by governments and private institutions, there is likely to be an increased demand for high-quality testing services in both established and developing manufacturing industries.

Industry Participants Focus on Advanced Testing Capabilities

The competitive environment continues to be highly dynamic with major firms focusing on the development of new generation test technologies, packaging test technology, automation solutions, and AI-based test systems. Collaboration, scaling up, and technological advancements are key to boosting the global semiconductor testing capabilities.

Key companies operating in the global Semiconductor Testing Services Market include JCET Group Co., Ltd., Taiwan Semiconductor Manufacturing Company Limited, Unisem, ASE Group, Amkor Technology, Siliconware Precision Industries Co., Ltd., Powertech Technology Inc., Bluetest Testservice GmbH, Micross, Integra Technologies, Presto Engineering, UL Solutions, EAG Laboratories, Criteria Labs, ATS Engineering, Advantest Corporation, STATS ChipPAC, Test Research, Inc. (TRI), ASE Test Limited, and National Instruments Corporation.

An SNS Insider analyst Sushant Kadam commented, “Increasing semiconductor complexity, rapid AI adoption, and growing demand for high-performance electronic systems are making advanced testing services indispensable across the semiconductor value chain. Companies investing in automation, advanced packaging expertise, and intelligent validation technologies will be well positioned to capitalize on the market's long-term growth opportunities.”

About the Author

Get in touch