Incinerator Market Size to Exceed $22.70 Billion by 2035 | SNS Insider

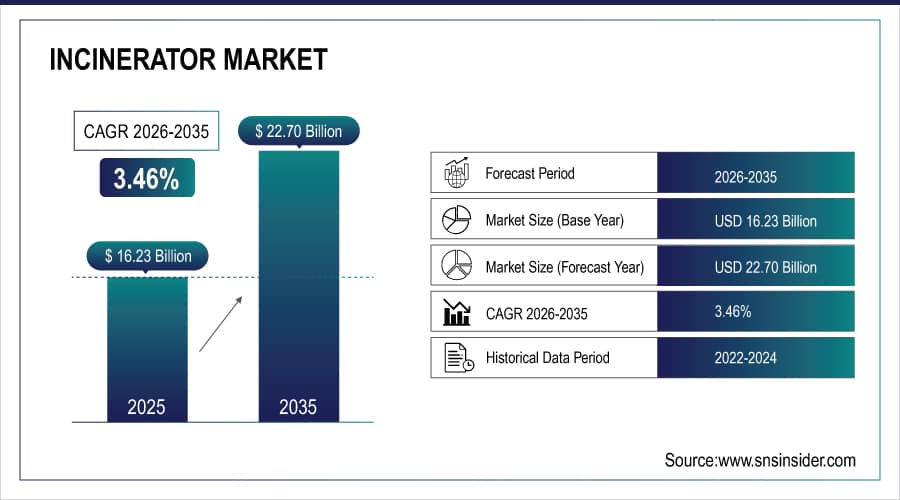

As per the SNS Insider Report titled, Incinerator Market by Waste Type, by Application, by Control Technology, by Operating Capacity, by Technology, by Region, and Global Forecast 2026-2035, “The global Incinerator Market size valued at USD 16.23 billion in 2025, is anticipated to grow to USD 22.70 billion by 2035, registering a CAGR of 3.46% over the 2026–2035 forecast period.”

Key Takeaways

-

Municipal Solid Waste accounted for nearly 44% of the market share in 2025, driven by rapid urbanization, increasing waste generation, and growing investments in waste management infrastructure globally.

-

Biomedical Waste is projected to witness the fastest growth during 2026–2035 due to rising healthcare activities, stricter waste disposal regulations, and growing concerns regarding infectious waste management.

-

Energy Recovery dominated the application segment with approximately 37% revenue share in 2025 owing to the increasing adoption of waste treatment systems that generate usable heat and electricity.

-

Environmental Protection is expected to register the fastest growth through 2035 as governments and industries focus on reducing landfill dependence and minimizing environmental pollution.

-

Flue Gas Treatment Systems held approximately 41% share in 2025, supported by stringent emission standards and increasing deployment of advanced pollution control technologies.

-

Heat Recovery Systems are anticipated to emerge as the fastest-growing control technology segment during the forecast period as operators seek to improve energy efficiency and operational profitability.

-

Large Scale (Over 200 tons/day) facilities represented nearly 45% of market revenue in 2025 due to their widespread use in municipal waste processing and waste-to-energy projects.

-

Medium Scale (51–200 tons/day) incinerators are expected to witness the fastest growth through 2035 as developing regions invest in scalable waste management infrastructure.

-

Mass Burn Incineration captured around 36% of total market revenue in 2025 owing to its capability to process large volumes of mixed municipal waste with minimal pre-treatment requirements.

-

Fluidized Bed Incineration is projected to record the fastest growth from 2026 to 2035 due to its higher combustion efficiency, lower emissions, and suitability for diverse waste streams.

-

Asia Pacific captured around 39% of total market revenue in 2025, supported by rising urban populations, increasing waste generation, and large-scale investments in waste treatment infrastructure.

Why Incinerator Market is Growing?

The Incinerator Market is growing at a steady rate owing to growing global waste generation, rising environmental concerns and increasing regulations related to waste disposal. The rapid urbanization, industrialization and population growth have increased the municipal, industrial and health care waste generation considerably, which calls for efficient waste treatment technologies.

Governments around the world are therefore concentrating on sustainable waste management strategies to reduce reliance on landfills and address the environmental problems caused by uncontrolled waste disposal. The incineration technologies provide an effective solution by decreasing the waste volume considerably and allowing the energy recovery from the combustible materials.

Municipalities and industrial operators are increasingly opting for incineration systems in order to generate electricity and heat and to manage waste streams. This dual advantage of waste reduction and energy generation is attracting a great deal of investment in developed and developing economies.

Furthermore, the rising healthcare expenditures and the expansion of medical infrastructure are driving the demand for biomedical waste incineration systems. Stringent regulations governing the management and disposal of hazardous and infectious waste are driving healthcare facilities to adopt advanced incineration technologies.

Incinerator Market Statistics

-

Municipal solid waste is still the largest waste handled by incineration facilities worldwide.

-

Waste-to-energy projects are gaining traction as governments look to achieve renewable energy and circular economy goals.

-

Growth of healthcare sector is increasing the demand for biomedical waste treatment and disposal systems.

-

Modern incineration plants are integrating flue gas treatment technologies as standard features to comply with stringent emission standards.

-

Large scale incineration plants constitute a majority of installed waste processing capacity globally.

-

Asia Pacific continues to see large investments in municipal waste management infrastructure as a result of rapid urbanization and industrial growth.

-

Industrial facilities are increasingly using incineration systems to safely treat hazardous and non-recyclable waste streams.

Emerging Trends

The Incinerator Market is experiencing various disruptive trends such as the integration of advanced emission control systems, digital monitoring technologies, and high-efficiency energy recovery solutions. Operators are increasingly turning to smart monitoring platforms that allow for real-time emissions monitoring, predictive maintenance, and operational optimization.

Fluidized bed incineration technologies are becoming more popular because of more efficient combustion, fewer emissions and increased fuel flexibility when compared to conventional systems. These systems are particularly suited to processing industrial, biomass and special waste streams.

Another important trend is the growth of waste-to-energy facilities. Governments and utility providers are putting money into modern incineration plants which convert municipal waste into electricity and district heating, helping to meet renewable energy targets and cut landfill use.

Also, increasing environmental regulations are encouraging the use of advanced flue gas treatment and carbon reduction technologies. With the world moving toward sustainability goals, future incineration systems will likely be designed to achieve optimal energy recovery and minimal environmental impact.

Top 10 Companies

-

Veolia Environment S.A.

-

Hitachi Zosen Corporation

-

Babcock & Wilcox Enterprises, Inc.

-

Martin GmbH

-

Keppel Seghers

-

Covanta Holding Corporation

-

Wheelabrator Technologies Inc.

-

Mitsubishi Heavy Industries Ltd.

-

SUEZ Group

-

China Everbright Environment Group Limited

About the Author

Get in touch