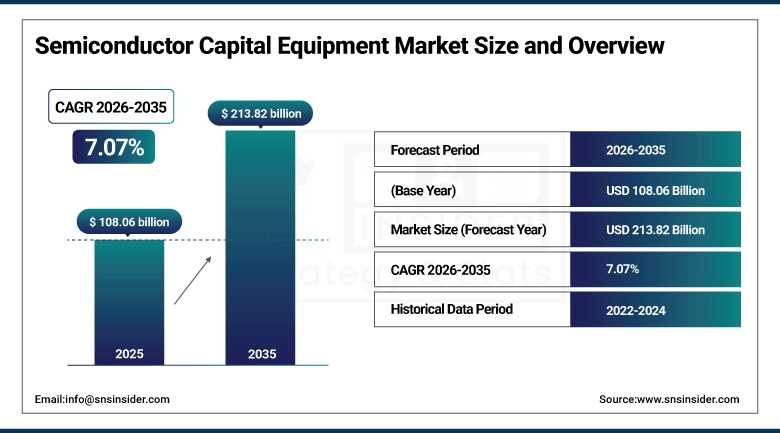

As per the SNS Insider Report titled, Semiconductor Capital Equipment Market by Technology Node, by Wafer Size, by Distribution Channel, by Application, and Region | Global Forecast 2026-2035, “The global Semiconductor Capital Equipment Market size valued at USD 108.06 billion in 2025, is anticipated to grow to USD 213.82 billion by 2035, registering a CAGR of 7.07% over the 2026–2035 forecast period.”

Key Takeaways

-

≥28nm technology node accounted for nearly 33.50% of the market share in 2025, driven by continued demand for mature-node semiconductor manufacturing across automotive, industrial, and consumer electronics applications.

-

3nm and below technology nodes are projected to witness the fastest growth during 2026–2035 as chip manufacturers increasingly invest in advanced semiconductor fabrication technologies for AI, HPC, and next-generation mobile devices.

-

300mm wafer size dominated the market with a 39.00% revenue share in 2025 owing to its widespread use in high-volume semiconductor manufacturing and cost-efficient production capabilities.

-

≥450mm wafer size is expected to register the fastest growth through 2035 due to increasing industry focus on improving wafer throughput and reducing manufacturing costs at advanced fabrication facilities.

-

Direct Sales held approximately 54.50% share in 2025, supported by strong partnerships between semiconductor equipment manufacturers and large integrated device manufacturers (IDMs) and foundries.

-

Distributors/VARs are anticipated to emerge as the fastest-growing distribution channel segment during the forecast period due to expanding semiconductor manufacturing ecosystems and growing regional equipment demand.

-

Logic IC Manufacturing represented nearly 30.40% of the market revenue in 2025 owing to increasing global demand for processors, AI chips, and advanced computing devices.

-

Logic IC Manufacturing is also projected to record the strongest growth through 2035 as advanced node investments accelerate across high-performance computing and artificial intelligence applications.

-

Asia-Pacific captured around 45.50% of total market revenue in 2025 and is expected to strengthen its market position further through 2035 supported by expanding semiconductor fabrication capacity and government-backed chip manufacturing initiatives.

-

North America accounted for approximately 23.90% of the global market share in 2025 driven by strong investments in advanced semiconductor technologies and domestic chip production programs.

Why Semiconductor Capital Equipment Market is Growing?

The Semiconductor Capital Equipment Market is witnessing fast expansion because of the increase in demand for advanced semiconductors in sectors like artificial intelligence, automotive, consumer electronics, cloud computing, and telecommunications. Semiconductor companies are making huge investments in the latest technology to facilitate the need for smaller, faster, and energy-efficient semiconductors.

The use of AI chips, supercomputers, electric cars, and 5G networks has increased demand for advanced semiconductor equipment. Major foundry and integrated circuit manufacturers have begun to build more manufacturing capacities to cater to the latest technological nodes in the form of 5nm, 3nm, and below 3nm semiconductors.

Government programs focused on enhancing their domestic semiconductor manufacturing ability are also contributing to market expansion. Several countries based in the Asia-Pacific, North America, and Europe regions have begun to invest in semiconductor production facilities.

The evolution of technology in lithography tools, wafer manufacturing equipment, deposition methods, and semiconductor packaging systems will further help in the growth and success of the market.

Semiconductor Capital Equipment Market Statistics

-

Semiconductor companies globally are investing more in capital expenditure towards advanced node manufacturing and capacity expansion.

-

Rising demands for AI chips, data center chips, and advanced memory components are fueling the deployment of next generation semiconductor manufacturing equipment.

-

Advanced lithography solutions like EUV equipment are essential for semiconductor manufacturing below 3nm.

-

Asia Pacific dominates the global capacity in terms of semiconductor manufacturing facilitated by active foundry capacity expansion activities.

-

Government-backed semiconductor manufacturing efforts are resulting in increased investments in domestic manufacturing facilities.

-

Demand from the automotive semiconductor market is facilitating capacity expansion in mature-node manufacturing facilities around the world.

-

Advancements in packaging technology are creating fresh opportunities in semiconductor manufacturing equipment.

Emerging Trends

A few notable trends impacting the Semiconductor Capital Equipment Market include the use of extreme ultraviolet (EUV) technology in addition to wafer processing technologies for chip manufacturing. Semiconductor manufacturers are concentrating on boosting their output efficiency as well as yield optimization along with transistor density.

The shift towards 3 nm and below process nodes is a new market trend driven by a need for energy-efficient and fast semiconductors. There are increased investments being made in packaging technologies, such as chiplet integration and 3D stacking of chips in logic and memory semiconductor fabrication.

Further, significant investments are also being made in smart semiconductor fabs that are automated with the help of AI technologies. Supply chain localization, sustainable operations, and energy-efficient manufacturing of semiconductors are a few other areas of interest that are expected to impact the future growth trajectory of the market.

Top 10 Companies

-

ASML Holding NV

-

Applied Materials Inc.

-

Tokyo Electron Limited

-

Lam Research Corporation

-

KLA Corporation

-

SCREEN Holdings Co., Ltd.

-

Hitachi High-Tech Corporation

-

ASM International

-

Canon Inc.

-

Nikon Corporation

About the Author

Get in touch