Abrasives Market Report Scope & Overview:

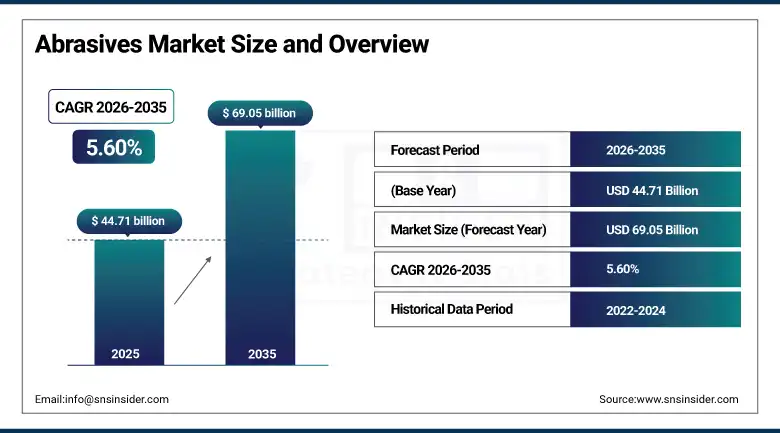

The Abrasives Market was valued at USD 44.71 Billion in 2025 and is expected to reach USD 69.05 Billion by 2035, growing at a CAGR of 5.60% from 2026 to 2035.

Abrasive products are some of the earliest types of industrial materials used by man throughout his history of manufacturing processes, and even as technology advanced, they continued to play an important role in manufacturing. In today’s industry, abrasives continue to feature prominently in all kinds of applications where material removal, shaping, smoothing, and cleaning is done with a degree of accuracy and precision. Abrasives include such diverse products ranging from traditional grinding wheels and cutting-off discs to coated abrasive tapes and sheets to superabrasive products made using diamond and cubic boron nitride which possess characteristics necessary for machining new advanced engineering materials. Due to a wide array of end use applications that range from automotive body work to semiconductor wafer finishing, the market’s structural diversity is such that its resilience throughout different business cycles is more than that of any single industry application.

Saint-Gobain Specialty Grains and Powders launched the Lumeos platform with its first product AZ25L, an alumina-zirconia abrasive grain engineered for heavy-duty grinding performance with reduced environmental impact, in December 2024.

Market Size and Forecast

-

Market Size in 2026E: USD 47.15 Billion

-

Market Size by 2035: USD 69.05 Billion

-

CAGR: 5.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Abrasives Market - Request Free Sample Report

Abrasives Market Trends

-

Demand for superabrasive diamond and cubic boron nitride tools is increasing in automotive, semiconductor, and advanced ceramics manufacturing due to superior precision and durability.

-

Industry 4.0-enabled automated grinding and polishing systems are improving abrasive efficiency, reducing waste, and enhancing surface quality consistency.

-

Eco-friendly abrasives with low-VOC binders, halogen-free formulations, and sustainable materials are gaining popularity due to rising environmental regulations.

-

Growth in electric vehicle manufacturing is creating new demand for specialized abrasives used in batteries, motors, and lightweight metal components.

-

Advanced semiconductor manufacturing and larger wafer processing are increasing demand for high-precision abrasive materials and CMP applications.

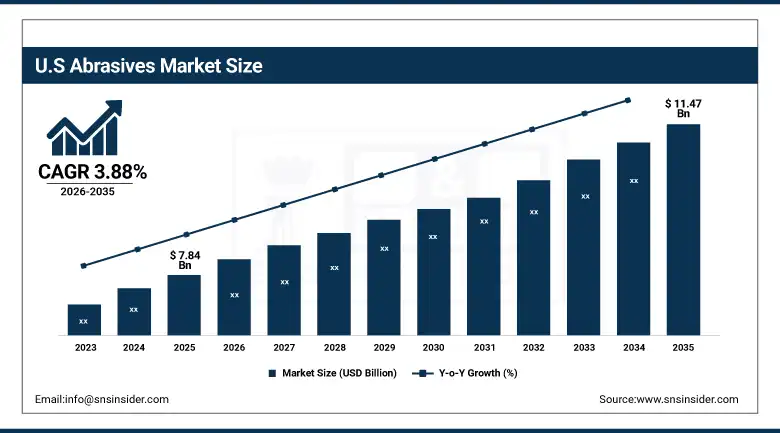

The U.S. Abrasives Market Outlook

The U.S. Abrasives Market was valued at approximately USD 7.84 Billion in 2025 and is expected to reach approximately USD 11.47 Billion by 2035, growing at a CAGR of approximately 3.88%.

The United States ranks as the second largest global abrasives market based on value due to the high volume of automotive, aerospace, and metalworking industries within the country that require abrasive solutions ranging from bonded grinding wheels and cut-off discs to precision coated abrasive belts and even superabrasive tooling for machining aerospace alloys. As manufacturing capacities within the nation get reshored and enhanced in terms of industrial capabilities as a result of increased focus on supply chain resilience after the COVID-19 crisis and government incentives through policies such as the CHIPS Act and the Inflation Reduction Act, there will be additional demand for abrasives in the nation through the expansion of new manufacturing plants.

3M Company expanded its Cubitron II structured abrasive grain product line in the United States in 2025, introducing new precision-shaped grain geometries for both coated abrasive and bonded abrasive applications targeting the growing demand for abrasive products that combine higher material removal rates with cooler cutting temperatures in metal fabrication and weld seam grinding applications.

Abrasives Market Segment Analysis

-

By Source, the synthetic segment dominated the abrasives market with 65.24% share in 2025, while the natural segment is the fastest growing source during 2026 to 2035.

-

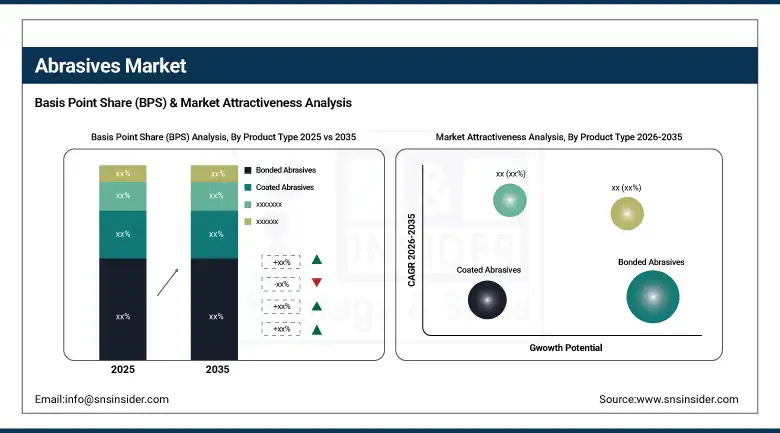

By Product Type, the bonded abrasives segment dominated the abrasives market with 50.34% share in 2025, while the super abrasives segment is the fastest growing product type during 2026 to 2035.

-

By Material, the aluminum oxide segment dominated the abrasives market with 40.26% share in 2025, while the boron carbide segment is the fastest growing material during 2026 to 2035.

-

By Application, the automotive segment dominated the abrasives market with 35.22% share in 2025, while the electrical & electronics segment is the fastest growing application during 2026 to 2035.

By Product Type, bonded abrasives dominate, super abrasives grow fastest

Bonded abrasives retained the dominant product position with 50.34% of market revenue in 2025. Bonded abrasive wheels, discs, segments, and sticks represent the traditional workhorse of industrial metal grinding, cutting, and surface preparation across metal fabrication, construction, foundry, and general manufacturing applications globally. Their commercial ubiquity reflects decades of manufacturing process optimization that has embedded bonded abrasive specifications into the tooling standards, quality procedures, and operator training of manufacturing operations across virtually every industrialized economy. Their commercial dominance reflects both their extremely broad applicability across the widest range of workpiece materials and surface geometry types and their competitive cost per unit of material removed in high-stock-removal applications.

Superabrasives are growing fastest as their unique combination of extreme hardness, precision grain geometry control, and exceptional tool life enables manufacturing process performance levels that conventional abrasive materials cannot approach. Diamond abrasive tools for glass, ceramic, stone, and composite material cutting, and cubic boron nitride wheels for hardened steel and nickel superalloy grinding, each address applications where their performance advantages justify price premiums of ten to one hundred times equivalent conventional abrasive tooling.

By Application, automotive dominates, electrical & electronics grows fastest

Automotive applications generated 35.22% of abrasives market revenue in 2025. The automotive industry's comprehensive use of abrasive processes across body panel surface preparation, engine component precision grinding, cylinder bore honing, transmission gear lapping, glass edge finishing, and paint defect correction creates one of the highest per-vehicle abrasive material consumption profiles among all manufactured product categories.

Electrical and electronics is growing fastest, driven by the combined demand of semiconductor wafer lapping and chemical mechanical planarization, precision grinding of electronic component substrates, and the expanding manufacturing base for EV battery electrode materials and power electronics components whose surface finishing requirements are creating new abrasive application categories. Each successive semiconductor technology node requires more precise and chemically selective abrasive planarization, increasing the per-wafer abrasive process cost and driving investment in engineered abrasive slurry and pad product development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

42.84% |

|

Middle East & Africa |

UAE |

18.73% |

|

Latin America |

Brazil |

43.84% |

North America Abrasives Market Insights

The North American abrasives market had about 17.84% share of worldwide Abrasives revenue in 2025, with US holding around 82.47% revenue share of the regional market. The regional market stands out due to the presence of higher-than-average superabrasives use compared to the aggregate abrasives consumed due to the prevalence of high-quality manufacturing activities within aerospace, medical devices, semiconductor equipment, and automobile industries which require the use of superabrasives. In addition, manufacturing reshoring facilitated by federal government industrial policies is increasing demand for abrasives through new manufacturing facilities arising from the transition to electric automobiles, semiconductor production, and renewable energy equipment production.

Europe Abrasives Market Insights

Europe accounted for about 22.84% of worldwide Abrasives revenues in 2025, mainly driven by Germany, France, Italy, and Poland, which together possess the third-largest cluster of mechanical engineering, automotive, and metalworking industries in the world. Germany contributed about 28.47% of revenue to Europe because of its dominance in the global mechanical engineering, automotive, and precision tooling manufacturing industries whose stringent performance requirements for abrasives have helped maintain their market prices above average on a per-unit basis compared to global average market values. In Europe, manufacturers like Saint-Gobain, Tyrolit, and Wendt have remained technically superior due to their product innovation for high-performance bonded abrasives and superabrasives.

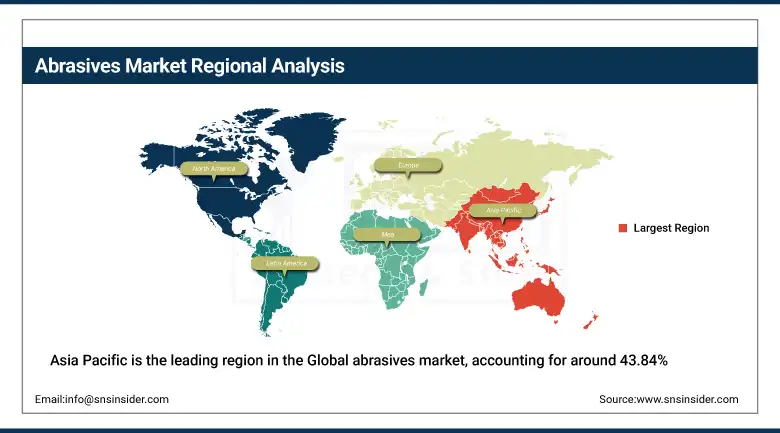

Asia Pacific Abrasives Market Insights

Asia Pacific is the leading region in the Global abrasives market, accounting for around 43.84% of the market revenues worldwide. China holds approximately 42.84% of the revenue share of Asia Pacific due to being not only the world's leading abrasive manufacturer but also the biggest consumer of abrasives owing to the large scale of manufacturing activity in the country within the sectors of automotive, construction, metals, and electronics, which in turn creates strong demand for abrasives and enables the development of a sizeable and growing local abrasives manufacturing industry along with considerable abrasives imports of high quality products. The high-end demand from Japan and South Korea arises from the presence of precision manufacturing industry within semiconductors, automotive parts, and industrial machinery manufacturing, necessitating the use of superabrasives and engineered abrasives.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Abrasives Market Insights

The Middle East and Latin America represent regions experiencing growth in abrasives market demand due to increasing activities in the construction sector, industrial sector, and automotive manufacturing that drive increased use of abrasives. In Latin America, Brazil emerges as the leading country in abrasives revenues accounting for about 43.84% of the regional revenues because of the presence of a robust automotive manufacturing, metal working and mining industry, and a construction industry with high abrasive use that translates to the most important commercial market for abrasives in Latin America. Mexico acts as an additional regional consumer market for abrasives owing to its maquiladora sector and growing aerospace machining industry which generates increased demand for higher performing abrasives. In the Middle East, the increasing demand for construction abrasive products emanates from infrastructure construction driven by the vision programs in Saudi Arabia and the UAE.

Market Dynamics

Growth Drivers: Rising global manufacturing activity and increasing demand for high-performance precision machining are driving abrasives market growth.

Growth in the abrasives industry is driven by the growth of manufacturing output in the key consuming end markets on a global scale. Recovery in global automobile manufacturing to levels above those seen before the pandemic, aerospace manufacturing growth in Airbus and Boeing, expansion of capabilities for semiconductors manufacturing, and an increase in construction activities within programs of urbanization in developing economies together help maintain growth in demand for abrasives which is positively correlated with industrial production indices. Growth in value outstrips growth in volume as the ongoing transition towards the use of more advanced materials like steel alloys, titanium, nickel superalloys, and silicon carbide composites necessitates the use of superabrasive cutting tools to make machining commercially feasible.

Restraints: Competition from low-cost abrasive manufacturers and replacement by alternative material removal technologies are restraining abrasives market growth.

Asian abrasive producers of commodity abrasives, especially from China and India, possess economies of scale in the manufacturing process and materials processing to offer extremely aggressive prices on conventional fused aluminum oxide and silicon carbide bonded and coated abrasives, thus putting pressure on margins of abrasive producers in the Western world in commodity grades. The processes of laser cutting, water jet cutting, and electric discharge machining, when applicable, can act as partial substitutes for the conventional processes using abrasives in applications where their capital equipment economics favor this approach and their materials processing is justified by their higher per operation cost compared with abrasives.

Opportunities: Growth in EV manufacturing and advanced semiconductor production is creating strong demand for high-value superabrasive solutions in precision machining applications.

The transition to the manufacture of electric vehicles has generated some unique superabrasive needs in relation to the grinding and finishing of lamination stacks for EV motor rotors, the honing of the EV motor housings, and the finishing of power electronic cooling plates that have different geometric and surface quality requirements compared to traditional ICE parts, favoring abrasive engineering solutions. The semiconductor chemical mechanical planarization (CMP) technique is becoming increasingly abrasive-intensive because the fabrication of advanced nodes requires additional CMP steps per wafer, greater abrasive selectivity between target and neighboring materials, and stringent post-CMP surface quality standards, prompting investments by such manufacturers as Cabot Microelectronics and DuPont in slurry and pad products.

Recent Developments:

-

2025: 3M Company expanded its Cubitron II structured abrasive grain portfolio with new precision-shaped grain geometries for metalworking coated and bonded abrasive applications, achieving higher material removal rates at lower grinding temperatures that reduce workpiece heat damage risk and extend abrasive product life relative to conventional fused alumina products.

-

2024: Saint-Gobain Specialty Grains and Powders launched the Lumeos platform with its inaugural AZ25L alumina-zirconia abrasive grain engineered for heavy-duty grinding with reduced environmental impact, addressing the dual commercial requirements of performance and sustainability that advanced manufacturing customers increasingly impose on abrasive material procurement decisions.

Abrasives Market Key Players are:

-

3M Company

-

Saint-Gobain SA

-

Robert Bosch GmbH

-

Tyrolit Group (Swarovski)

-

Carborundum Universal Ltd. (Murugappa Group)

-

Fujimi Inc.

-

Noritake Co. Ltd.

-

Wendt Group

-

PFERD (August Rüggeberg GmbH)

-

sia Abrasives Industries AG

-

Cabot Microelectronics (CMC Materials)

-

DuPont de Nemours Inc.

-

Hermes Abrasives Ltd.

-

Mirka Ltd.

-

Walter Surface Technologies

-

KREBS & RIEDEL Schleifscheibenfabrik GmbH

-

Asahi Diamond Industrial Co. Ltd.

-

DEERFOS Co. Ltd.

-

Nihon Kenshi Co. Ltd.

-

VSM AG

Abrasives Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 44.71 Billion |

| Market Size by 2035 | USD 69.05 Billion |

| CAGR | CAGR of 5.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Synthetic, Natural) • By Product Type (Bonded Abrasives, Coated Abrasives, Super Abrasives, Others) • By Material (Aluminum Oxide, Silicon Carbide, Cubic Boron Nitride, Diamond, Boron Carbide, Others) • By Application (Automotive, Metal Fabrication & Metalworking, Construction & Infrastructure, Electrical & Electronics, Aerospace & Defense, Wood & Furniture, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Company, Saint-Gobain SA, Robert Bosch GmbH, Tyrolit Group (Swarovski), Carborundum Universal Ltd. (Murugappa Group), Fujimi Inc., Noritake Co. Ltd., Wendt Group, PFERD (August Rüggeberg GmbH), sia Abrasives Industries AG, Cabot Microelectronics (CMC Materials), DuPont de Nemours Inc., Hermes Abrasives Ltd., Mirka Ltd., Walter Surface Technologies, KREBS & RIEDEL Schleifscheibenfabrik GmbH, Asahi Diamond Industrial Co. Ltd., DEERFOS Co. Ltd., Nihon Kenshi Co. Ltd., VSM AG |

Frequently Asked Questions

Asia Pacific dominated the Abrasives Market in 2025, holding approximately 43.84% of global revenues.

The automotive segment dominated the Abrasives Market with 35.22% share in 2025.

The primary growth factors are expanding global manufacturing output across automotive, aerospace, construction, and electronics sectors generating abrasive volume demand, the premium performance requirements of advanced manufacturing processes for superabrasive tooling creating value growth above volume growth, electric vehicle and semiconductor manufacturing transitions creating new abrasive demand profiles, and Industry 4.0 automated grinding system adoption improving abrasive utilisation efficiency.

The Abrasives Market was valued at USD 44.71 Billion in 2025.

The Abrasives Market is expected to grow at a CAGR of 5.60% from 2026 to 2035.

Get in Touch