Industrial Gases Market Report Scope & Overview:

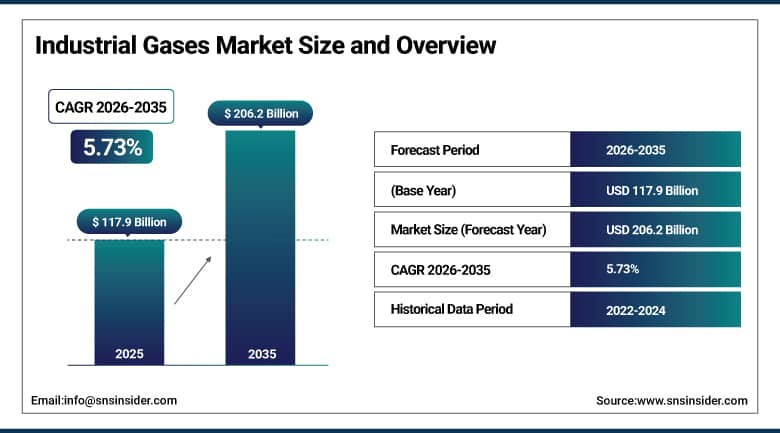

Industrial Gases Market was valued at USD 117.9 billion in 2025 and is expected to reach USD 206.2 billion by 2035, growing at a CAGR of 5.73% from 2026-2035.

Industrial Gases Market is growing due to the rising need for industrial gases in the healthcare, manufacturing, chemical, and energy industry segments. Industrial Gases Market Growth is being driven by the rising use of gases like oxygen, nitrogen, and hydrogen in healthcare, metal manufacturing, and refining industries. Additionally, the growing adoption of the semiconductor and electronics industry is also propelling market growth. Furthermore, clean energy solutions like hydrogen fuel cells and carbon capture technology are also driving market growth.

The U.S. Department of Energy identifies hydrogen as a critical energy carrier for industrial decarbonization, projecting U.S. clean hydrogen demand could reach 50 million metric tons annually by 2050. The DOE's Hydrogen Shot initiative targets a cost reduction to USD 1 per kilogram of clean hydrogen a target that would fundamentally change the economics of hydrogen industrial gas markets.

Industrial Gases Market Size and Forecast

-

Market Size in 2025: USD 117.9 Billion

-

Market Size by 2035: USD 206.2 Billion

-

CAGR: 5.73% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Industrial Gases Market - Request Free Sample Report

Industrial Gases Market Trends

-

Rising demand from manufacturing, metal processing, and chemical industries is driving the industrial gases market.

-

Growing adoption in healthcare, electronics, and energy sectors is boosting market growth.

-

Expansion of applications in welding, cutting, refrigeration, and packaging is fueling consumption.

-

Increasing focus on clean energy solutions and hydrogen-based technologies is shaping adoption trends.

-

Advancements in gas separation, storage, and distribution technologies are enhancing efficiency and safety.

-

Rising demand for oxygen, nitrogen, hydrogen, carbon dioxide, and specialty gases is supporting market expansion.

-

Collaborations between gas producers, industrial users, and technology providers are accelerating innovation and global adoption.

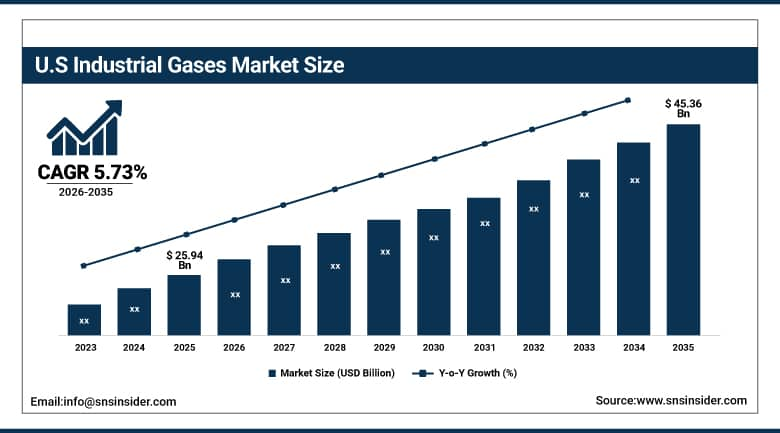

U.S. Industrial Gases Market was valued at USD 25.94 billion in 2025 and is expected to reach USD 45.36 billion by 2035, growing at a CAGR of 5.73% from 2026-2035.

The expansion of the United States Industrial Gases Market can be credited to growing demand from the healthcare industry, manufacturing sector, chemical sector, and energy sector. The increasing use of oxygen in the healthcare industry, and nitrogen and hydrogen in refinery and metal industries is propelling the consumption of industrial gases. Additionally, there is an increase in the manufacturing of semiconductors and electronics that is adding to the growing demand for purified gases.

The U.S. Department of Energy's Regional Clean Hydrogen Hubs program has committed USD 7 billion to eight regional hub projects across the U.S. that will collectively produce millions of metric tons of clean hydrogen annually. The American Iron and Steel Institute reports that U.S. steel production consumed over 10 billion cubic feet of industrial oxygen annually for basic oxygen furnace steelmaking operations.

Industrial Gases Market Segment Analysis

-

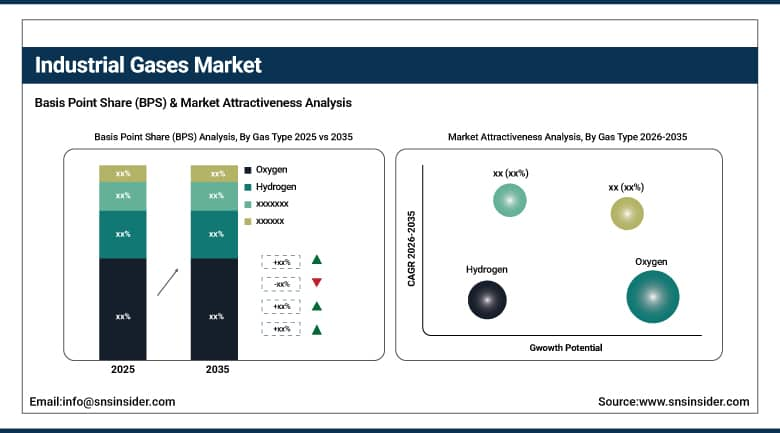

By Gas Type, Oxygen segment dominated the Industrial Gases Market in 2025 with 34% share; Hydrogen segment fastest growing (CAGR).

-

By End-Use Industry, Manufacturing segment dominated the Industrial Gases Market in 2025 with 29% share; Healthcare segment fastest growing (CAGR).

By Gas Type, Oxygen segment dominates, Hydrogen growing fastest

Oxygen held the dominant gas type position in the Industrial Gases Market in 2025, due to the critical importance of this element in more industries than any other industrial gas. The production of steel, the manufacture of chemicals, the production of glass, the purification of water, and their application in medicine all involve the use of oxygen in amounts greater than those used by any other industrial gas. Medical oxygen use has increased considerably since the outbreak of the coronavirus pandemic, when the importance of oxygen in hospitals became apparent and hospitals invested in both tank-based and onsite oxygen production capabilities.

Hydrogen is the fastest-growing gas type, due to investments being made in hydrogen through the energy transition into decarbonized fuels as feedstocks for producing green ammonia and green steel, as well as other industries which cannot be electrified. Hydrogen use in industrial processes, such as hydrogen cracking and hydrogen treatment, for purposes of refining crude oil into other products, is already large and will increase as refiners increase the complexity of their refineries. The demand for hydrogen generated through new applications such as hydrogen fuel cell automobiles, power generation, and decarbonized industries provides a long-term demand growth trend that will ensure the continued expansion of hydrogen markets well beyond the forecast period until 2035.

By End-Use Industry, Manufacturing segment dominates, Healthcare growing fastest

Manufacturing dominates the Industrial Gases Market due to the Wide-Scale and Continuous Utilization of gases like oxygen, nitrogen, argon, and acetylene in crucial industrial applications such as welding, cutting, metalworking, heat treating, and chemical processing. Such gases play a critical role in boosting productivity, maintaining quality, elevating safety measures, and facilitating precise manufacturing processes. The quick pace of industrialization in both emerging and established markets, coupled with robust growth in the automobile, machinery, and heavy engineering industries, will greatly enhance the demand. Moreover, growing automation, the establishment of large-scale production units, and the deployment of advanced manufacturing technologies will also bolster the significance of industrial gases in the manufacturing sector.

Healthcare is the fastest-growing end-use segment in the Industrial Gases Market, owing to the rapid rise in the demand for oxygen, anesthetic gases, and respiratory support devices. The growing incidence of chronic respiratory disorders like COPD, asthma, and sleep apnea, along with aging demographics across the globe, is contributing to the increased use of industrial gases. Additionally, improvements in medical gas delivery systems, portable oxygen therapy equipment, and efforts towards enhancing healthcare standards and emergency response capabilities are driving their adoption in healthcare, making it a dominant high-potential application field.

Industrial Gases Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

85% |

|

Europe |

Germany |

25% |

|

Middle East & Africa |

Saudi Arabia |

40% |

|

Latin America |

Brazil |

48% |

Asia Pacific Industrial Gases Market Insights

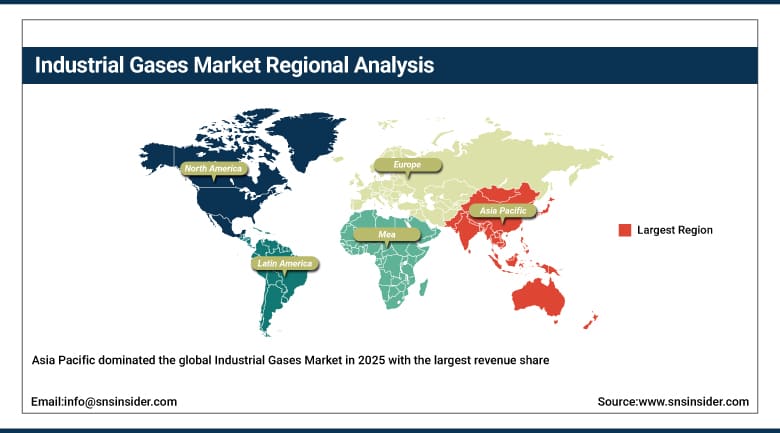

Asia Pacific dominated the global Industrial Gases Market in 2025 with the largest revenue share, driven by China's enormous steel, chemical, and electronics manufacturing industries, India's rapidly expanding manufacturing sector, Japan's advanced industrial gas technology, and Southeast Asia's growing manufacturing base. China is the world's largest single consumer of industrial oxygen for steel production, the largest consumer of hydrogen for ammonia and methanol synthesis, and a rapidly growing market for semiconductor-grade specialty gases as domestic chip manufacturing capacity expands. India's industrial growth across pharmaceuticals, specialty chemicals, and food processing is creating growing industrial gas demand that Air Liquide, Linde, and domestic Indian companies are competing to serve through new production investment.

China's Ministry of Industry and Information Technology has designated hydrogen as a strategic energy technology under its 14th Five-Year Plan, with national targets for fuel cell vehicle deployment and industrial hydrogen adoption that are driving domestic production and distribution infrastructure investment. India's government production-linked incentive scheme for specialty chemicals a major industrial gas consumer has attracted USD 3 billion in private sector investment that directly creates new industrial gas procurement demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Industrial Gases Market Insights

The North America Industrial Gases Market is experiencing healthy growth due to high demand from the healthcare, manufacturing, chemicals, and energy industries. The region has well-developed industrial facilities and a high degree of technological adoption, such as automation and renewable energy. The growing need for oxygen and specialty gases in the healthcare sector, along with hydrogen in refineries and energy production, is fostering market growth. Moreover, the growth in the manufacture of semiconductors and the food industry is aiding consumption.

Europe Industrial Gases Market Insights

The Europe Industrial Gases Market is growing steadily owing to the high demand from industries such as manufacturing, healthcare, chemicals, and energy. The advanced industrial infrastructure and stringent environmental norms in Europe are promoting the usage of environment-friendly and efficient gases, such as hydrogen and low-carbon fuels. High consumption of oxygen in hospitals and increased demand for gases in metal fabrication, food preservation, and electronics manufacturing are further fueling the market growth. Besides, the emphasis on decarbonization and the use of renewable energy sources is positively influencing the demand for industrial gases in various sectors.

Middle East & Africa and Latin America Industrial Gases Market Insights

The Middle East and Africa and Latin America Industrial Gases Market is experiencing consistent growth because of the increasing levels of industrialization, infrastructure, and energy production. The increased consumption of oxygen, nitrogen, and hydrogen gases is being driven by increased demand from the health care industry, oil and gas sector, and metals industry. The presence of a significant petrochemicals and refining sector in the Middle East region contributes positively towards market growth, while the food processing and mining sectors contribute to growth in Latin America.

Industrial Gases Market Growth Drivers:

-

Manufacturing sector expansion and clean hydrogen energy transition creating sustained global industrial gases market growth

The industrial gases market's growth is anchored in the fundamental indispensability of its products across industries that are themselves growing globally. Manufacturing capacity expansion driven by nearshoring, semiconductor investment, automotive electrification, and chemical industry growth in Asia creates direct industrial gas demand that scales proportionally with production volume. The hydrogen energy transition is adding an entirely new demand category on top of the traditional industrial market: green and blue hydrogen for energy applications represents demand that was negligible a decade ago and is projected to grow to tens of millions of metric tons annually within the forecast period. The convergence of regulatory decarbonization pressure and economic hydrogen production incentives is pulling private capital into hydrogen infrastructure investment at a pace that will transform the hydrogen industrial gas market's scale over the next decade.

The International Energy Agency projects global hydrogen demand will grow to 150 million metric tons annually by 2030 in its Net Zero scenario, with clean hydrogen from renewable and low-carbon production routes accounting for the majority of growth. BloombergNEF estimates green hydrogen production costs will fall below USD 2 per kilogram by 2030 in regions with abundant renewable resources, making green hydrogen economically competitive with grey hydrogen in those markets.

Industrial Gases Market Restraints:

-

Limited hydrogen infrastructure and high capital costs constraining clean hydrogen industrial gas market scale-up

The transition from conventional industrial gases to clean hydrogen faces infrastructure constraints that no amount of investment enthusiasm can resolve overnight. Hydrogen production, storage, and distribution require purpose-built infrastructure that does not share compatibility with natural gas systems dedicated pipelines, cryogenic storage tanks, and specialized compression equipment that must be constructed from scratch in most markets. The chicken-and-egg dynamics of hydrogen markets where producers need customers before committing to large production capacity, and customers need supply certainty before investing in hydrogen-capable equipment create market development friction that government programs are trying to address through coordinated demand and supply development, but that still delays the commercial deployment timelines that optimistic projections assumed.

Industrial Gases Market Opportunities:

-

Carbon capture utilization and green hydrogen economy creating transformative industrial gases market opportunities globally

Carbon capture utilization and storage is creating new industrial gas market opportunities at a scale that most gas industry analysis has underweighted. Industrial CO2 capture at power plants, cement plants, and steel mills generates large volumes of CO2 that require industrial gas handling expertise compression, purification, transport, and injection that the major industrial gas companies are uniquely positioned to provide. Enhanced oil recovery using captured CO2 creates commercial demand for CO2 transport and injection services at oilfield scales. The food and beverage carbonation and packaging markets represent additional CO2 utilization demand that is growing with global consumer goods production. As CCUS technology scales through regulatory support and commercial maturity, the industrial gas companies that build CCUS service capabilities will access a significant new market segment that leverages their existing infrastructure and customer relationships.

Recent Developments:

-

2025: Air Products announced commercial operations at its NEOM Green Hydrogen Project Phase 1 in Saudi Arabia, producing green ammonia from renewable-powered electrolysis at a scale of 650 tonnes of green hydrogen daily one of the world's largest operational green hydrogen production facilities, demonstrating that multi-hundred-tonne-per-day green hydrogen production is commercially achievable.

-

2025: Linde plc expanded its semiconductor specialty gas production capacity with a new electronic gases facility in Malaysia serving the rapidly growing Southeast Asian semiconductor manufacturing ecosystem, producing ultra-high-purity nitrogen trifluoride, tungsten hexafluoride, and specialty etch gases for advanced chip fabrication processes.

-

2026: Air Liquide completed commissioning of its hydrogen liquefaction plant expansion at its Port-Jérôme facility in France, adding 30 tonnes per day of liquid hydrogen production capacity serving industrial mobility and energy applications, as part of the company's Horizon 2025 commitment to triple liquid hydrogen production capacity across its European network.

Industrial Gases Market Key Players

Some of the Industrial Gases Market Companies

-

Air Liquide

-

Linde plc

-

Praxair

-

Messer Group

-

Air Products & Chemicals

-

Taiyo Nippon Sanso Corporation

-

Mitsui Chemicals

-

SOL Group

-

Showa Denko K.K.

-

Iwatani Corporation

-

Gulf Cryo

-

Ellenbarrie Industrial Gases

-

Buzwair Industrial Gases

-

INOX Air Products

-

Coregas Pty Ltd

-

Air Water Inc.

-

Matheson Tri-Gas

-

SIAD Group

-

Leland Limited

-

Universal Industrial Gases

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 117.9 Billion |

| Market Size by 2035 | USD 206.2 Billion |

| CAGR | CAGR of 5.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Gas Type (Oxygen, Nitrogen, Hydrogen, Carbon dioxide, Acetylene, Argon) •By End-Use Industry (Healthcare, Manufacturing, Metallurgy & Glass, Food & Beverage, Retail, Chemicals & Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Air Liquide, Linde plc, Praxair, Messer Group, Air Products & Chemicals, Taiyo Nippon Sanso Corporation, Mitsui Chemicals, SOL Group, Showa Denko K.K., Iwatani Corporation, Gulf Cryo, Ellenbarrie Industrial Gases, Buzwair Industrial Gases, INOX Air Products, Coregas Pty Ltd, Air Water Inc., Matheson Tri-Gas, SIAD Group, Leland Limited, Universal Industrial Gases |

Frequently Asked Questions

Ans: Asia Pacific led the Industrial Gases Market in the region with the highest revenue share in 2025.

Ans: Expansion of the manufacturing & metal industry which drives the market growth.

Ans: The Oxygen segment dominated the Industrial Gases Market in 2025.

Ans: The Industrial Gases Market is expected to grow at a CAGR of 5.73% from 2026 to 2035.

Ans: The Industrial Gases Market was valued at USD 117.9 billion in 2025.

Get in Touch