Accounts Receivable Automation Market Report Scope and Overview:

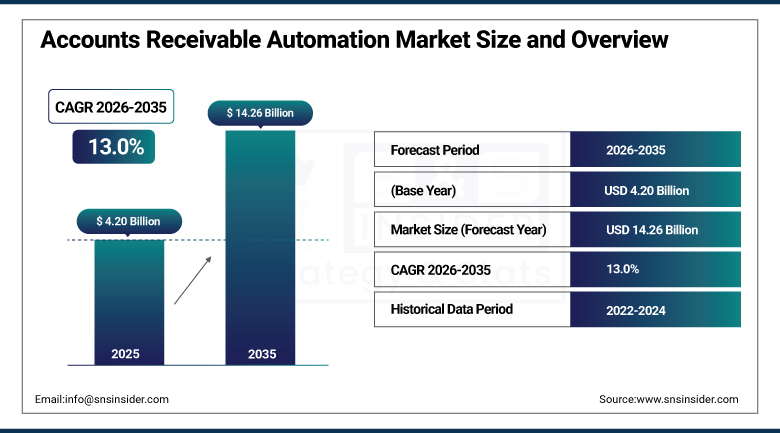

The Accounts Receivable Automation Market was valued at USD 4.20 Billion in 2025 and is projected to reach USD 14.26 Billion by 2035, registering a CAGR of 13.0% from 2026 to 2035.

The Accounts Receivable Automation Market Growth is stimulated by high requirements for quicker payment processing, better cash flow management, and less manual work within accounting. Companies use AI and machine learning as well as intelligent workflows to improve the process of invoice processing, payments tracking, and customer credit management. Also, the widespread use of cloud-based finance management systems, enterprise-level digitalization, and an increased focus on efficiency make for rapid development of the market. Moreover, growing numbers of transactions and attempts to decrease payment delay and mistakes contribute to the automation of accounts receivable processes.

AI-powered cash application tools achieved 90% straight-through processing rates in 2025, reducing manual intervention by 75% and accelerating dispute resolution by 65% through automated workflows, reflecting the genuinely rapid maturation of machine-learning-driven accounts receivable automation capability across enterprise finance departments.

Market Size and Forecast

-

Market Size in 2026E: USD 4.75 Billion

-

Market Size by 2035: USD 14.26 Billion

-

CAGR: 13.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Accounts Receivable Automation Market - Request Free Sample Report

Accounts Receivable Automation Market Trends

-

Machine-learning engines now ingest live payment signals, dispute frequencies, and even email sentiment to flag credit risk weeks before bureau downgrades.

-

Many businesses, regardless of size or industry, continue recognizing the transformative potential of accounts receivable automation but often lack in-house expertise to implement complex systems effectively.

-

Rising adoption of digital payment methods and expansion of shared service centers continue accelerating demand for cloud-based finance automation software.

-

Growing complexity of billing processes across enterprises continues driving demand for increasingly sophisticated automated invoicing and dispute resolution capability.

-

The energy and utilities sector's substantial digital transformation continues creating fresh demand for accounts receivable automation beyond the market's traditional BFSI stronghold.

U.S. Accounts Receivable Automation Market Outlook

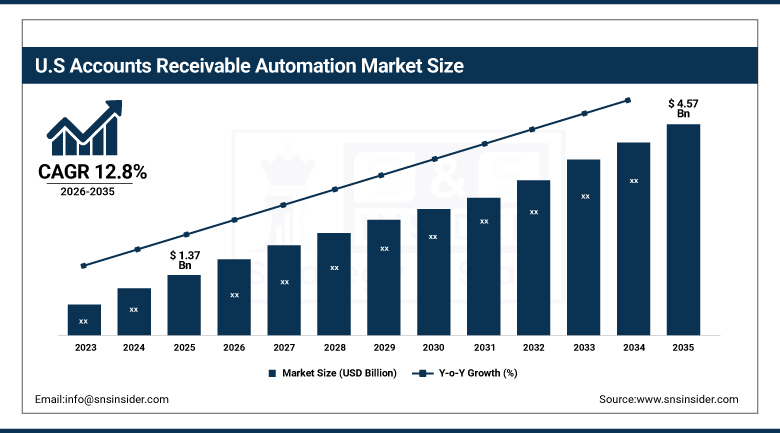

The U.S. Accounts Receivable Automation Market was valued at approximately USD 1.37 Billion in 2025 and is projected to reach approximately USD 4.57 Billion by 2035, registering a CAGR of approximately 12.8% from 2026 to 2035.

Demands in the United States remained influenced throughout the year by technology adaptation, presence of important vendors, and strong digital infrastructure. High technology adaptation, presence of important vendors, and early adaptation to electronic invoicing and payments maintained America’s leading position, with demands from technology, health care, and professional services segments optimizing finances through enhanced financial operations. Increased requirement for enhanced cash flow management and reduction in days sales outstanding maintained the driving force for investments made by enterprises in America for developing advanced automatic collection and credit risk management solutions.

HighRadius continued expanding its AI-driven cash application and credit risk management platform throughout 2025, targeting American BFSI and manufacturing customers seeking automated dispute resolution and predictive credit risk flagging capability across increasingly complex enterprise receivables portfolios.

Accounts Receivable Automation Market Segment Analysis

-

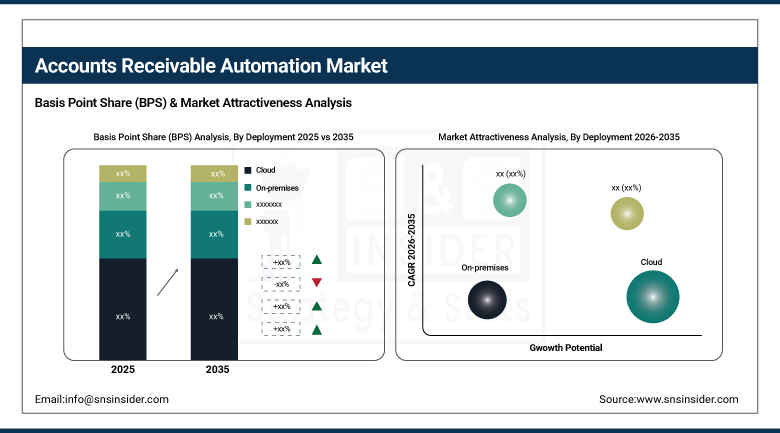

By Deployment, Cloud segment dominated the Accounts Receivable Automation Market in 2025 with 72% share; Cloud segment is also the fastest growing segment.

-

By Vertical, BFSI segment dominated the market in 2025 with 28% share; Healthcare segment is the fastest growing segment.

-

By Component, Solution segment dominated the market in 2025 with 64% share; Services segment is the fastest growing segment.

-

By Organization Size, Large Enterprises segment dominated the market in 2025 with 67% share; Small & Medium Sized Enterprises segment is the fastest growing segment.

By Deployment, Cloud Deployment Dominates the Accounts Receivable Automation Market and Registers the Fastest Growth

The Cloud category accounted for the largest market share in the Accounts Receivable Automation Market in 2025 due to the rise in the demand for scalable, flexible, and cost-effective financial automation services. Cloud-based platforms allow companies to automate invoice processing, payments tracking, and accounts receivables management, along with providing access to financial data in real-time. Adoption of digital transformation strategies, working from home policies, and enterprise-level software integration has further enhanced the use of cloud-based accounts receivable automation solutions. The Cloud category is the fastest-growing in the Accounts Receivable Automation Market due to the adoption of subscription-based software solutions and automated financial processes.

By Vertical, BFSI Dominates the Accounts Receivable Automation Market While Healthcare Emerges as the Fastest-Growing Segment

The BFSI segment dominated the Accounts Receivable Automation Market in 2025 owing to the high volume of financial transactions, invoicing, and payments processing in banking and financial institutions. BFSI businesses need automation solutions to gain visibility on cash flow, minimize errors, and ensure efficiency in operations. The adoption of digital banking systems, regulatory compliance considerations, and advancements in finance technology have facilitated the adoption of accounts receivable automation solutions.

The Healthcare segment is the fastest growing in the Accounts Receivable Automation Market owing to the growing complexity of billing process, claims management, and payments reconciliation. Healthcare institutions are increasingly relying on automation technologies that help them to minimize the amount of manual work, speed up their reimbursement process and increase the efficiency of their revenue cycle management.

By Component, Solutions Dominate the Accounts Receivable Automation Market While Services Witness the Fastest Growth

The Solution segment dominated the Accounts Receivable Automation Market in 2025 because of the rising requirement of software that performs all activities related to invoicing, payment processing, collections, and reconciliation. Companies have been adopting such platforms to increase financial accuracy, decrease costs, and improve cash flow. The use of technology such as AI and analytics has made organizations adopt such accounts receivable automation solutions in large numbers.

The Services segment is the fastest growing in the Accounts Receivable Automation Market because of the rising need for implementation, consulting, integration, and other such services. Such services require specialization on the part of providers as companies need customized automation platforms to be easily integrated into their current financial system. Digital finance operations require software to be continuously optimized which results in a rising need for such services.

By Organization Size, Large Enterprises Dominate the Market While Small & Medium-Sized Enterprises (SMEs) Experience the Fastest Growth

The Large Enterprises segment dominated the Accounts Receivable Automation Market in 2025 because of high transaction volume, sophisticated finance activities, and substantial investment capacity. Larger firms are more likely to utilize automation technology to increase efficiency in receivables collections and optimize working capital, thus improving financial transparency across various departments. The need for automation in larger companies increased because of requirements for optimized workflows, enterprise integration, and analytics.

The Small & Medium Sized Enterprises segment is the fastest growing in the Accounts Receivable Automation Market because of the increased availability of low-cost cloud based automation software. SMEs are opting for these solutions to decrease the burden of manual accounting and increase operational efficiency. The trend of digital transformation, subscription based pricing model, and awareness regarding the benefits of automation is fueling growth in this segment.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.45% |

|

Europe |

Germany |

24.00% |

|

Asia Pacific |

China |

31.90% |

|

Middle East and Africa |

UAE |

26.65% |

|

Latin America |

Brazil |

34.35% |

North America Accounts Receivable Automation Market Insights

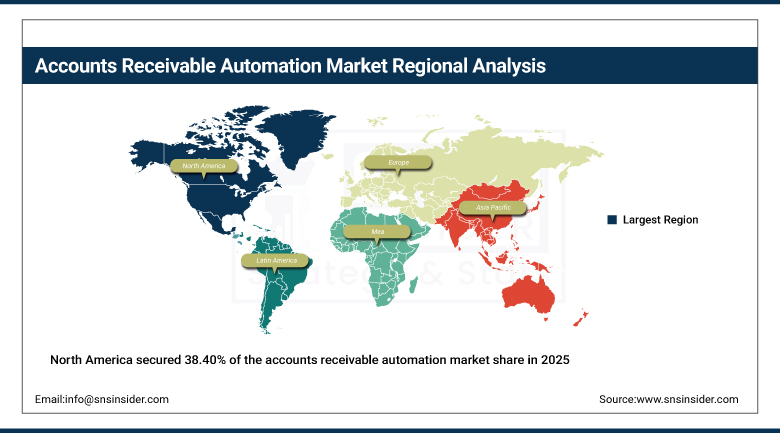

North America secured 38.40% of the accounts receivable automation market share in 2025, supported by early technology adoption, strong presence of key vendors, and robust digital infrastructure. That combination of established finance technology infrastructure and mature vendor ecosystem kept the continent firmly positioned as the market's clear leader by a considerable margin over every other region tracked in this report.

The United States accounted for roughly 80.45% of regional revenue, anchored by high technology adoption, presence of leading vendors, and an early shift to electronic invoicing and payments. Canada added further regional demand through its own growing enterprise finance automation sector, and that combined strength kept North America the largest addressable market for accounts receivable automation vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Accounts Receivable Automation Market Insights

Europe held a meaningful share of global revenue, supported by strong enterprise digital transformation investment and growing regulatory emphasis on financial process compliance across the region's major economies. Continued e-invoicing mandate expansion kept reinforcing steady European demand for accounts receivable automation throughout the year.

Germany led demand at roughly 24.00% of European revenue, supported by its substantial enterprise finance and manufacturing sector base. The UK and France contributed substantial additional demand, and continued European regulatory emphasis on e-invoicing should keep regional demand climbing through the forecast period.

Asia Pacific Accounts Receivable Automation Market Insights

Asia-Pacific is forecast to post the fastest CAGR of approximately 12.67% to 16.8% during the forecast period, fueled by rapid digitalization of SMEs, increasing adoption of cloud accounting, government promotion of e-invoicing, and expansion of cross-border trade requiring efficient receivables management across supply chains. That combination of digitalization momentum and expanding trade complexity kept the region's growth trajectory well ahead of every other region tracked in this report.

China led the pack, supported by its massive enterprise digital transformation and cross-border trade volume. India was expected to register the highest country-level CAGR, with rapid SME digitalization and government-promoted e-invoicing adoption continuing to reinforce Asia Pacific's position as the fastest-growing market tracked in this report.

MEA and Latin America Accounts Receivable Automation Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding enterprise digital transformation investment, growing e-invoicing adoption, and rising government focus on financial process modernization across both areas. As these markets continued developing modern enterprise finance infrastructure, accounts receivable automation adoption grew correspondingly from a considerably smaller base than in more mature markets.

The UAE led Middle East and Africa demand, supported by growing enterprise digital transformation investment and e-invoicing mandate development. Saudi Arabia contributed further demand through its own digital economy diversification programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing enterprise finance automation continuing to anchor regional demand for accounts receivable automation.

Growth Drivers: Cash Flow Optimization Demand and E-Invoicing Adoption

The increasing need for automation of receivable processes and e-invoices results in increasing popularity of the accounts receivable automation market. The accounts receivable automation market increases owing to the increased demand for improved management of the company's cash flows and minimized days sales outstanding since companies begin understanding the real costs and risks associated with manual receivable process.

The need for business improvement in terms of cash flow management, cost reduction, and accounting cycle improvement together with the development of new technologies such as cloud computing becomes a major driver behind the growth of the accounts receivable automation market. The growth of transaction volume within companies, increasing complexity of billing processes, and expanding number of shared service centers become additional drivers behind the increasing demand.

Restraints: Implementation Complexity and Data Privacy Concerns

The complexity involved in the process of invoicing and payment management remains a true restraint on rapid adoption across the market, since not all businesses have the necessary in-house expertise to be able to put such complicated systems in place without proper assistance. This implementation challenge ensures that demand for professional services remains high despite the continuous decrease in software licensing costs.

Privacy and security concerns remain another restraint, since the account receivable automation solutions deal with highly sensitive information of customers and need to be fully secured from any unauthorized access or breach of data. This is especially important for businesses belonging to BFSI and healthcare sectors.

Opportunities: AI-Driven Credit Risk Prediction and SME Market Expansion

Machine-learning engines ingesting live payment signals, dispute frequencies, and email sentiment to flag credit risk weeks before bureau downgrades represent a genuinely significant opportunity, as AI-powered cash application tools already achieving 90% straight-through processing rates demonstrate genuine commercial viability. Vendors offering proven, genuinely predictive credit risk technology stand to capture meaningful share as enterprises increasingly prioritize proactive risk management over reactive collections.

Rising SME recognition of streamlined financial process necessity offers a second substantial opportunity, as this organization-size category's fastest-growing status among all segments tracked in this market reflects genuine demand democratization beyond the market's traditional large-enterprise stronghold. Vendors offering genuinely affordable, easy-to-deploy accounts receivable automation platforms stand to capture meaningful share as smaller organizations increasingly compete effectively in an increasingly digital business landscape.

Recent Developments

-

2025: BlackLine continued expanding its AI-driven accounts receivable and financial close automation platform, targeting enterprise finance teams seeking integrated cash application and dispute resolution capability.

-

2025: Billtrust continued advancing its cloud-based invoicing and payment automation platform, targeting BFSI and manufacturing customers seeking accelerated collections and reduced days sales outstanding.

-

2024: Esker continued expanding its order-to-cash automation suite, integrating machine-learning-driven credit risk scoring capability for enterprise customers seeking proactive receivables management.

Accounts Receivable Automation Market Key Players

-

SAP SE

-

Oracle

-

Microsoft

-

International Business Machines Corporation (IBM)

-

Workday

-

Infor

-

The Sage Group

-

HighRadius

-

Billtrust

-

BlackLine

-

Tesorio

-

Quadient

-

Kofax

-

Esker's

-

Comarch

-

Zoho Corporation

-

Tipalti

-

Stripe

Accounts Receivable Automation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.20 Billion |

| Market Size by 2035 | USD 14.26 Billion |

| CAGR | CAGR of 13.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment (Cloud and On-premises) • By Vertical (Consumer Goods and Retail,BFSI,Manufacturing,Healthcare,IT and Telecom and Others) • By Component (Services and Solution) • By Organization Size (Large Enterprises,Small & Medium Sized Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SAP SE, Oracle, Microsoft, International Business Machines Corporation (IBM), Salesforce, Workday, Infor, The Sage Group, HighRadius, Billtrust, BlackLine, Tesorio, Quadient, Kofax, Esker, Bottomline Technologies, Comarch, Zoho Corporation, Tipalti, Stripe |

Frequently Asked Questions

North America dominates the market with a 41.2% share driven by early fintech adoption and digital payments.

The Accounts Receivable Automation Market was valued at approximately USD 4.20 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is growing demand for business automation in receivable processes and e-invoicing solutions, combined with demand for better cash flow management.

The Cloud segment dominated the Accounts Receivable Automation in 2025.

North America dominated the Accounts Receivable Automation Market in 2025, holding an estimated 38.4% share of total global market revenue.

Get in Touch