Acetic Acid Market Report Scope & Overview:

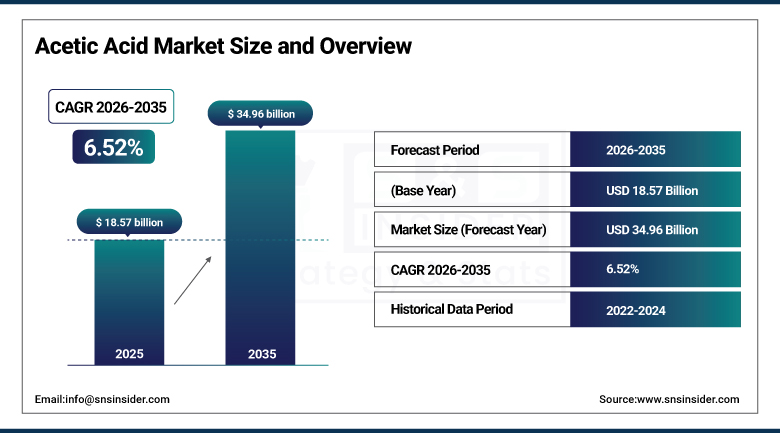

The Acetic Acid Market was valued at USD 18.57 Billion in 2025 and is expected to reach USD 34.96 Billion by 2035, growing at a CAGR of 6.52% from 2026–2035.

The global acetic acid market is growing at a sustained and commercially broad-based pace. Acetic acid (ethanoic acid, CH₃COOH) is one of the most important industrial chemicals, produced predominantly through the methanol carbonylation process using rhodium or iridium catalysts, whose colorless liquid serves as a fundamental building block for manufacturing vinyl acetate monomer, purified terephthalic acid, acetic anhydride, ester solvents, and chloroacetic acid. The market is driven by rising demand for vinyl acetate monomer which drives market growth as the primary catalyst, growing PTA demand for polyester fiber and PET resin production, and expanding pharmaceutical and food-grade applications. The report covers global production capacity and utilization rates, feedstock price fluctuations for methanol and carbon monoxide, regulatory landscape impacts, and sustainability metrics.

In 2023, Eastman Chemical Company launched a new acetic acid production technology aimed at improving production efficiency and reducing environmental impact, incorporating advanced process control and energy integration that reduces per-ton energy consumption and CO₂ emissions relative to conventional methanol carbonylation infrastructure. The technology advancement reflects the commercial recognition that energy cost reduction and sustainability credential create competitive differentiation in the global acetic acid market where commodity pricing creates intense cost competition among major producers.

Market Size and Forecast:

-

Market Size in 2026E: USD 19.78 Billion

-

Market Size by 2035: USD 34.96 Billion

-

CAGR: 6.52% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Acetic Acid Market - Request Free Sample Report

Acetic Acid Market Trends:

-

Rising demand for vinyl acetate monomer (VAM) in adhesives, paints, coatings, and construction materials is driving strong growth in acetic acid consumption

-

Expansion of purified terephthalic acid (PTA) production for polyester fibers and PET packaging is increasing acetic acid demand across textile and packaging industries

-

Development of bio-based acetic acid production technologies is supporting sustainable manufacturing initiatives and green chemistry adoption

-

Growing pharmaceutical production is boosting demand for high-purity glacial acetic acid used in active pharmaceutical ingredient (API) synthesis and drug manufacturing

-

Increasing consumption of acetic anhydride in cellulose acetate, pharmaceuticals, and chemical synthesis is supporting diversified demand growth for acetic acid derivatives

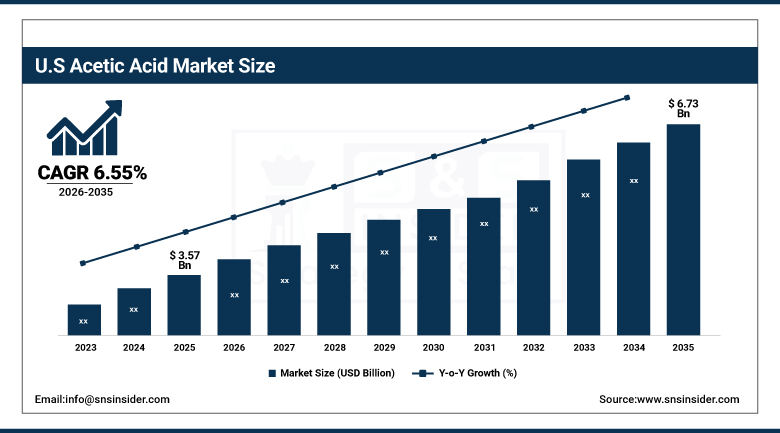

U.S. Acetic Acid Market Outlook:

The U.S. Acetic Acid Market was valued at approximately USD 3.57 Billion in 2025 and is expected to reach approximately USD 6.73 Billion by 2035, growing at a CAGR of approximately 6.55%.

The U.S. is the most commercially significant acetic acid market within the fastest-growing North American region. Celanese Corporation’s Clear Lake, Texas mega-plant, Eastman Chemical’s operations, and INEOS’ Texas City facility following its 2023 acquisition of Eastman’s assets collectively define the domestic acetic acid production landscape. The U.S.’s methanol feedstock accessibility from domestic natural gas creates competitive production economics. Celanese’s U.S. Gulf Coast acetic acid production serves both domestic VAM, acetate ester, and acetic anhydride markets and significant export volumes to global chemical customers.

Celanese Corporation expanded its Clear Lake, Texas acetic acid production capacity in 2024 with process optimization upgrades that increase effective production output without new reactor capital investment, targeting growing global VAM and acetic anhydride demand from the adhesives, coatings, and pharmaceutical sectors. The optimization approach reflects the commercial preference for debottlenecking existing infrastructure over greenfield capacity investment whose capital intensity creates longer payback periods in a commodity chemical market whose cycle creates investment timing sensitivity.

Acetic Acid Market Segment Analysis:

-

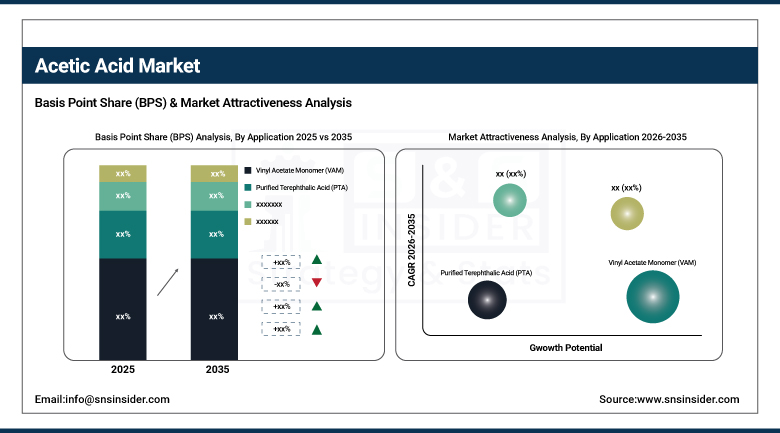

By Application, the Vinyl Acetate Monomer (VAM) segment dominated the Acetic Acid Market with approximately 48% share in 2025, while the Plastics & Polymers segment is the fastest growing.

-

By End-Use Industry, the Adhesives, Paints & Coatings segment dominated the Acetic Acid Market with approximately 35% share in 2025, while the Pharmaceutical & Healthcare segment is the fastest growing.

By Application, VAM dominates, Plastics & Polymers grows fastest

Vinyl acetate monomer retained the dominant application position with approximately 48% of the acetic acid market in 2025. VAM’s commercial primacy reflects its role as the most commercially significant acetic acid derivative whose production from acetic acid and ethylene creates the building block for polyvinyl acetate, polyvinyl alcohol, ethylene vinyl acetate copolymer, and vinyl acetate copolymers. Each construction adhesive formulation that specifies PVAc emulsion creates VAM demand whose aggregate across the global adhesive industry creates commercial scale. Paint and coatings’ vinyl-acrylic binder whose water-based formulation creates low-VOC architectural coating creates VAM procurement that compounds with construction activity. Rising demand for vinyl acetate monomer which drives market growth is SNS Insider’s confirmed primary driver.

Plastics and polymers including PTA for polyester and PET applications is the fastest-growing acetic acid application because Asia Pacific’s extraordinary polyester fiber production expansion, the global PET bottle market’s growth, and the packaging film industry’s PET adoption create above-average PTA demand whose acetic acid component compounds with each new PTA plant’s commissioning. Each ton of PTA produced from p-xylene oxidation requires approximately 35-40 kg of acetic acid as the oxidation solvent whose recovery and recycle creates consistent commercial consumption that compounds with PTA production volume expansion.

By End-Use, adhesives & coatings dominate, pharma grows fastest

Adhesives, paints, and coatings retained the dominant end-use position with approximately 35% of the acetic acid market in 2025. The building and construction industry’s PVAc adhesive, vinyl-acrylic paint binder, and textile finishing VAM application creates the most commercially concentrated and largest end-use procurement category. Each new residential and commercial building project creates VAM-derived adhesive and coating procurement whose volume scales with construction activity. The global construction sector’s progressive recovery and the emerging market’s extraordinary infrastructure investment create geographic market development that sustains the end-use category’s dominant commercial position.

Pharmaceutical and healthcare is the fastest-growing end-use because pharmaceutical API synthesis’ acetic acid solvent and acetylation reagent role, aspirin and acetaminophen production’s acetic anhydride intermediate consumption, and the generic drug market’s extraordinary production volume growth create above-average premium grade acetic acid procurement. Each new pharmaceutical facility that employs acetic acid or acetic anhydride in API synthesis creates procurement whose regulatory grade specification sustains premium commercial relationships with qualified producers.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

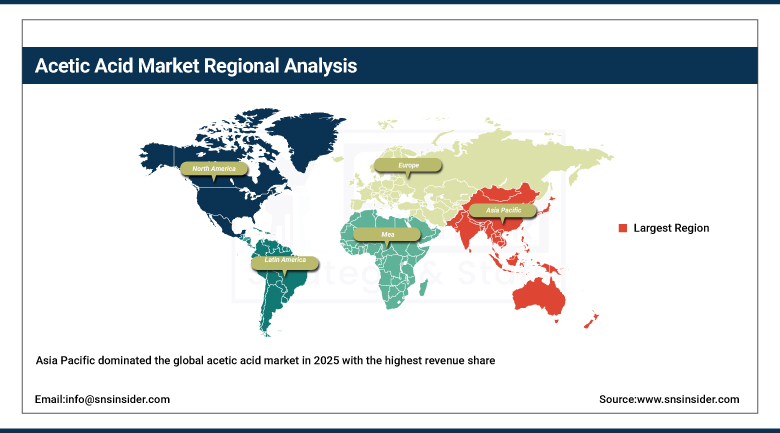

Asia Pacific Acetic Acid Market Insights

Asia Pacific dominated the global acetic acid market in 2025 with the highest revenue share. China accounts for approximately 54.6% of Asia Pacific revenues through its position as the world’s largest acetic acid producer and consumer, whose integrated PTA, VAM, and acetate ester manufacturing creates the most commercially concentrated acetic acid demand globally. The extraordinary pace of China’s polyester, adhesive, and packaging industry expansion creates proportional acetic acid demand growth.

India’s pharmaceutical and textile industries, Japan’s chemical manufacturing, and South Korea’s chemical sector create significant secondary markets whose combined procurement sustains Asia Pacific’s commercial dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Acetic Acid Market Insights

North America is the fastest-growing regional acetic acid market, driven by Celanese’s and INEOS’ U.S. production, growing pharmaceutical procurement, and VAM demand from the construction sector. The United States accounts for approximately 87.4% of North American revenues through Celanese’s Clear Lake mega-plant’s domestic supply and export programme.

Canada and Mexico contribute approximately 12.6% of North American revenues through the chemical processing and pharmaceutical manufacturing sectors’ acetic acid procurement.

Europe Acetic Acid Market Insights

Europe is a technically sophisticated acetic acid market where INEOS Acetyls’ Hull operations, BP Chemicals’ legacy infrastructure, and REACH compliance create structured commercial demand. Germany accounts for approximately 22.3% of European revenues through its chemical industry’s diverse acetic acid intermediate procurement and the pharmaceutical sector’s premium grade demand.

France, the Netherlands, and Belgium are significant secondary markets where chemical processing, pharmaceutical manufacturing, and food-grade applications create consistent acetic acid procurement.

MEA & Latin America Acetic Acid Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through SABIC’s chemical complex, the petrochemical sector’s acetic acid downstream derivatives, and the pharmaceutical industry’s growing procurement. Brazil leads Latin American revenues at approximately 44.2% through its chemical manufacturing sector, the food and beverage industry’s acetic acid application, and the pharmaceutical sector’s procurement.

Market Dynamics:

Growth Drivers: VAM demand in adhesives and coatings and PTA expansion for polyester and PET production

Rising demand for vinyl acetate monomer is SNS Insider’s confirmed primary growth driver for the acetic acid market. The construction sector’s water-based adhesive demand, architectural paint’s vinyl-acrylic binder requirement, and the packaging industry’s EVA copolymer adoption collectively create VAM demand whose commercial scale compounds with global construction activity and consumer packaging growth. Each new emerging market’s construction programme that specifies water-based PVAc adhesive creates VAM demand that sustains above-market acetic acid procurement growth in Asia, Africa, and Latin America.

PTA production expansion for the global polyester fiber and PET resin market creates structured acetic acid solvent demand whose per-ton consumption at every new PTA plant creates long-term commercial procurement. Each new PTA plant commissioned in Asia Pacific, the Middle East, or South Asia creates acetic acid procurement relationships whose duration reflects the plant’s 20–30-year operational lifetime.

Restraints: Methanol feedstock price volatility and stringent environmental regulation on production emissions

Methanol feedstock price volatility, driven by natural gas price cycles and methanol production economics, creates acetic acid production cost uncertainty whose commercial impact moderates pricing predictability. Each natural gas price spike that increases methanol cost creates acetic acid manufacturer margin pressure whose downstream pricing impact creates procurement hesitation in cost-sensitive industrial applications.

Environmental regulation of acetic acid production emissions, including carbonyl compound and volatile organic compound controls, creates compliance investment requirement whose capital and operating cost moderate’s producer economics in tightening regulatory environments. Each new emission standard creates process upgrade investment whose recovery through pricing creates competitive dynamics in commodity acetic acid markets.

Opportunities: Bio-based acetic acid development and pharmaceutical-grade premium market

Bio-based acetic acid from biomass fermentation and CO₂ electrochemical reduction creates sustainable production pathway development whose lifecycle carbon footprint advantages sustain specification preference in sustainability-sensitive procurement contexts. Each commercial demonstration that achieves bio-based acetic acid at competitive economics creates market development opportunity.

Pharmaceutical-grade glacial acetic acid represents a commercially premium opportunity whose above-commodity pricing sustains producer investment in quality management systems and regulatory compliance whose per-ton commercial value creates attractive margin differentiation from commodity applications.

Recent Developments:

-

2023: Eastman Chemical Company launched a new acetic acid production technology in 2023 aimed at improving production efficiency and reducing environmental impact through advanced process control and energy integration that reduces per-ton CO₂ emissions.

-

2023: INEOS completed the acquisition of Eastman Chemical Company’s Texas City site in September 2023, including the 600-kiloton acetic acid plant, significantly expanding INEOS Acetyls’ North American production capacity and commercial positioning.

-

2024: Celanese Corporation expanded its Clear Lake, Texas acetic acid production capacity in 2024 through process optimization upgrades targeting growing global VAM and acetic anhydride demand from the adhesives, coatings, and pharmaceutical sectors.

Acetic Acid Market Key Players:

-

Celanese Corporation

-

INEOS Acetyls (INEOS Group)

-

BP Chemicals Ltd. (BP PLC)

-

Eastman Chemical Company

-

Sinopec Corporation

-

PetroChina Company Limited

-

LyondellBasell Industries Holdings

-

Daicel Corporation

-

Mitsubishi Chemical Corporation

-

Wacker Chemie AG

-

Jiangsu SOPO (Group) Co., Ltd.

-

GNFC Ltd. (Gujarat Narmada Valley Fertilizers)

-

Saudi International Petrochemicals Company (Sipchem)

-

Kingboard Holdings Limited

-

Chongqing Longevity Chemical Co., Ltd.

-

Yankuang Cathay Coal Chemicals

-

Shandong Hualu-Hengsheng Chemical

-

BPX Energy

-

Helm AG

-

Myriant Technologies (PTT MCC Biochem)

Acetic Acid Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.57 Billion |

| Market Size by 2035 | USD 34.96 Billion |

| CAGR | CAGR of 6.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Application (Vinyl Acetate Monomer/VAM, Purified Terephthalic Acid/PTA, Acetic Anhydride, Ester Solvents, Monochloroacetic Acid/MCA, Others) • by End-Use Industry (Adhesives/Paints & Coatings, Plastics & Polymers, Textiles & Apparel, Food & Beverages, Pharmaceutical & Healthcare, Chemical Synthesis, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Celanese Corporation, INEOS Acetyls (INEOS Group), BP Chemicals Ltd. (BP PLC), Eastman Chemical Company, Sinopec Corporation, PetroChina Company Limited, LyondellBasell Industries Holdings, Daicel Corporation, Mitsubishi Chemical Corporation, Wacker Chemie AG, Jiangsu SOPO (Group) Co., Ltd., GNFC Ltd. (Gujarat Narmada Valley Fertilizers), Saudi International Petrochemicals Company (Sipchem), Kingboard Holdings Limited, Chongqing Longevity Chemical Co., Ltd., Yankuang Cathay Coal Chemicals, Shandong Hualu-Hengsheng Chemical, BPX Energy, Helm AG, Myriant Technologies (PTT MCC Biochem) |

Frequently Asked Questions

The Acetic Acid Market is expected to grow at a CAGR of 6.52% from 2026 to 2035.

The Acetic Acid Market was valued at USD 18.57 Billion in 2025.

Rising demand for vinyl acetate monomer (VAM) which drives market growth as the primary catalyst, and expanding PTA production for polyester fiber and PET resin whose acetic acid solvent requirement creates consistent structured procurement that compounds with each new Asian PTA plant commissioned.

Plastics & Polymers will grow rapidly in the Acetic Acid Market from 2026 to 2035 as confirmed by SNS Insider, driven by PTA expansion for polyester and PET production. VAM dominated the market with approximately 48% share in 2025.

Asia Pacific dominated the Acetic Acid Market in 2025 with the highest revenue share, while North America is the fastest-growing region.

Get in Touch