Acrylic Acid Market Report Scope & Overview:

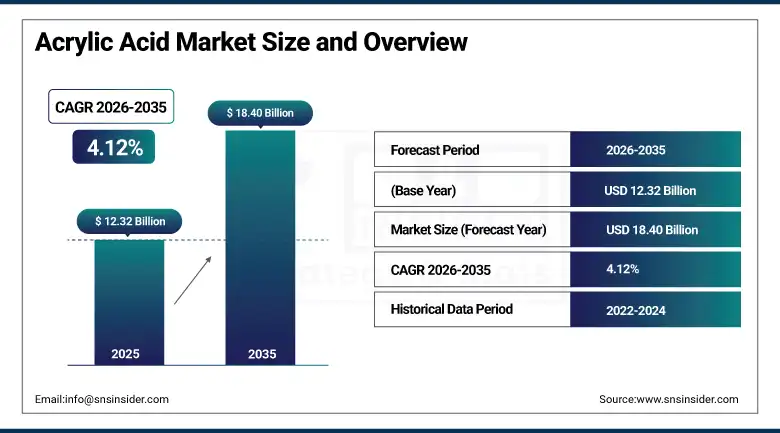

The Acrylic Acid Market was valued at USD 12.32 billion in 2025 and is expected to reach USD 18.40 billion by 2035, growing at a CAGR of 4.12% from 2026–2035.

The acrylic acid market is witnessing steady growth in the global market owing to increasing demand for superabsorbent polymers, coatings, and adhesives. Rising consumption in diapers, adult incontinence products, and hygiene applications is supporting market expansion. Growth in construction activities is increasing usage of surface coatings and cement modifiers across infrastructure projects. Expanding industrial manufacturing and packaging sectors are further driving demand for acrylic acid derivatives. Technological advancements in polymer chemistry and water treatment solutions are supporting product innovation. Increasing focus on sustainable materials and high-performance coatings is fueling market growth across end-use industries.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025 and the European Chemicals Agency regulatory inventory, acrylic acid is a key intermediate primarily used in superabsorbent polymers, with global chemical production capacity heavily concentrated in Asia, accounting for more than 50% of downstream polymer manufacturing inputs. As per OECD chemical safety assessments and national industry statistics, superabsorbent polymer applications represent over 60% of acrylic acid consumption, while personal hygiene products account for more than 70% of end-use demand in developed economies.

Market Size and Forecast

-

Market Size 2026E: USD 12.80 billion

-

Market Size 2035: USD 18.40 billion

-

CAGR: 4.12% from 2026-2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Acrylic Acid Market - Request Free Sample Report

Acrylic Acid Market Trends

-

Bio-based acrylic acid commercialization is accelerating as manufacturers invest in renewable feedstocks to meet sustainability targets and reduce emissions.

-

Demand for sustainable chemicals is rising due to stricter environmental regulations and increasing consumer preference for eco-friendly products.

-

Construction sector expansion is boosting acrylic acid consumption in surface coatings, adhesives, sealants, and cement modification applications.

-

Government infrastructure investments are increasing product adoption across transportation, commercial buildings, and large-scale urban development projects.

-

Research and development activities are improving production efficiency and enhancing the commercial viability of bio-based acrylic acid technologies.

-

Demand for durable and high-performance materials is growing as industries seek products capable of withstanding harsh conditions.

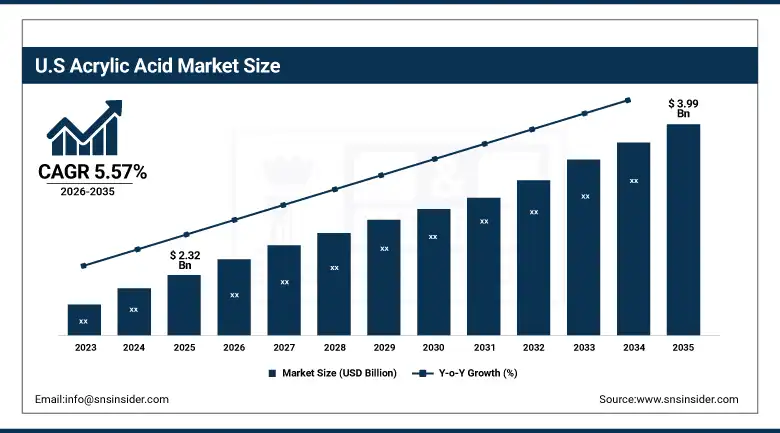

U.S. Acrylic Acid Market Size Outlook.

The U.S. Acrylic Acid Market was valued at USD 2.32 billion in 2025 and is expected to reach around USD 3.99 billion by 2035, growing at a CAGR of 5.57% from 2026–2035.

The U.S. acrylic acid market is growing consistently owing to increased demand for adhesives, coatings, and superabsorbent polymers. The usage of acrylic acid in construction, packaging, and personal care industries has contributed to market growth in a consistent manner. Increased investments in high-performance materials and sustainable chemical manufacturing have generated an increase in demand. Development of advanced polymer technologies, hygiene products, and water treatment applications is further driving the demand for this product.

According to the U.S. Census Bureau and the U.S. Food and Drug Administration, the U.S. acrylic acid market is supported by hygiene, coatings, and food packaging applications. The FDA continues to authorize acrylic-based polymers for specific food-contact uses, while U.S. Census Bureau manufacturing indicators show sustained activity in chemical manufacturing industries supplying downstream sectors. Additionally, the U.S. Department of Agriculture reported record cheese production of 14.66 billion pounds in 2025, supporting demand for acrylic-based packaging and preservation materials used across food processing supply chains.

Acrylic Acid Market Segment Analysis

-

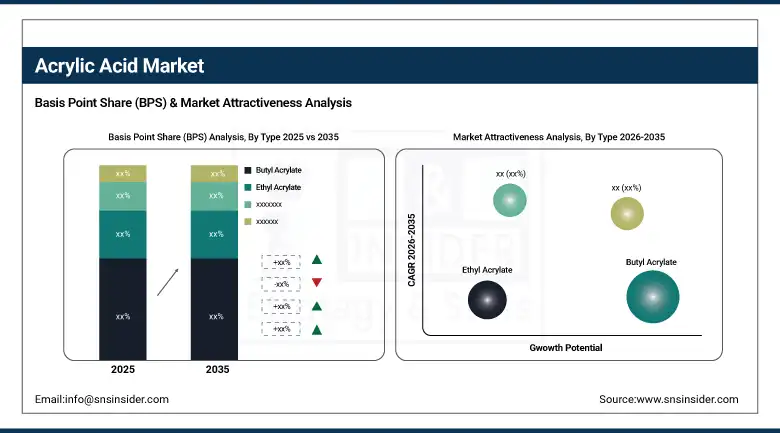

By Type, butyl acrylate dominated the market with 19.40% share in 2025; while 2-ethylhexyl acrylate are the fastest growing segment with CAGR of 5.96% during 2026 to 2035.

-

By Application, surface coating dominated the market with 24.00% share in 2025; while diapers are the fastest growing segment with CAGR of 7.67% during 2026 to 2035.

-

By End-Use Industry, construction dominated the market with 29.10% share in 2025; while healthcare is the fastest growing segment with CAGR of 8.00% during 2026 to 2035.

By Type, butyl acrylate dominated the acrylic acid market, while 2-ethylhexyl acrylate is the fastest growing segment.

The Butyl Acrylate segment held the dominating position in terms of revenue shares in the acrylic acid market in 2025. This has been due to its wide application in paints, coatings, adhesives, and sealants. The increase in construction and automobile manufacturing activities has resulted in the high demand for materials that can provide a protective surface layer. Additionally, its good flexibility, weatherability, and adhesion have made it dominant in industrial applications across the world.

The 2-Ethylhexyl Acrylate segment will exhibit a fastest CAGR in the forecast period of 2026-2035. Increasing demands for pressure sensitive adhesives, and high-performance coatings are driving this growth. Growing application in tapes, labels, and construction industry are helping in the expansion of the market. Superior chemical resistance, low temperature flexibility, and durability are some factors which are compelling manufacturers to use it in modern-day applications.

By Application, surface coating dominated the acrylic acid market, while diapers are the fastest growing segment.

The Surface Coating segment held the dominated share of revenue in the acrylic acid market in 2025. This dominance can be explained by their extensive use in the manufacturing of architectural paints, industrial paints, and automotive finishes. The increasing urbanization and infrastructural activities have led to high consumption of coating products. The growing need for better properties such as anti-corrosion, resistance, and weather proofing will aid segment growth during the forecast period.

The Diaper segment will witness the fastest CAGR during 2026-2035. Growth will be fueled by the rising birth rate and hygiene consciousness. The increasing population, along with disposable incomes, is aiding the growth of the premium baby care products market. Availability of SAP-based products and the high growth witnessed in emerging nations will drive segment growth at a rapid pace.

By End-Use Industry, construction dominated the acrylic acid market, while healthcare is the fastest growing segment.

The Construction segment was the leading segment in the acrylic acid market in terms of revenue shares in 2025, owing to high demand for acrylic acid in the production of paints, coatings, adhesives, and as a cement modifier. There has been an exponential rise in demand owing to rapid urbanization and large-scale infrastructural developments around the world. Increasing residential and commercial construction activities will fuel the growth of the market.

The Healthcare Segment will witness the fastest growth during 2026-2035, driven by the growing demand for hygiene and absorbent healthcare products. Increasing elderly populations will drive the adoption of adult incontinence and patient care products. Increasing development in the healthcare industry will boost the adoption of polymer-based advanced materials. Infection control and high-performance healthcare applications will be driving the market growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

88.20% |

|

Europe |

Germany |

27.40% |

|

Asia Pacific |

China |

42.80% |

|

Middle East & Africa |

UAE |

18.60% |

|

Latin America |

Brazil |

47.30% |

North America Acrylic Acid Market Insights.

North America in acrylic acid market is positioned to register the fastest growth during the forecast period with a market share of about 5.79% in 2025. The region benefits from strong consumption across construction, packaging, and industrial manufacturing sectors. Increasing investments in sustainable chemicals and high-performance materials are accelerating market expansion across the United States and Canada. Rising adoption of water treatment polymers and advanced adhesive technologies is further supporting regional growth. Strong research activities and specialty chemical innovation capabilities are driving long term market development.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025 and the U.S. Census Bureau, North America’s acrylic acid demand is strongly supported by downstream hygiene and construction sectors. In 2025, the United States recorded approximately 1.39 million annualized housing starts, sustaining demand for acrylic-based paints, coatings, adhesives, and sealants.

Additionally, the U.S. Census Bureau reported that adults aged 65 years and above account for about 18% of the population, supporting continued consumption of acrylic acid-derived superabsorbent polymers used in adult incontinence and personal hygiene products.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Acrylic Acid Market Insights.

Europe acrylic acid market holds considerable strength in 2025 due to stringent regulations for sustainability and advanced manufacturing industries. Some important countries include Germany, France, United Kingdom, and Italy which contribute significantly to market demand. The high emphasis placed on the production of green paints, green packaging, and water treatment solutions ensures steady growth of the market. Adoption in applications including adhesives, construction, and hygiene products is helping strengthen market consumption.

As per the Eurostat and the European Commission, the demand from Europe is expected to remain high on account of the growing demand from hygiene, coatings, and plastics sectors. In addition to this, the European Commission has stated that Europe produces approximately 32 million tons of plastic waste per year.

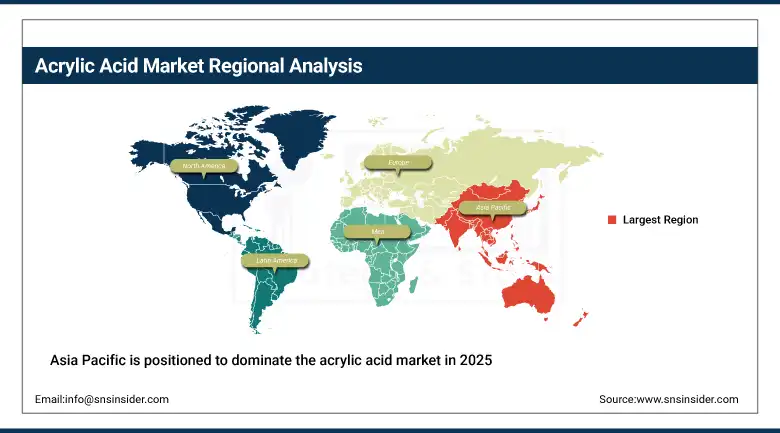

Asia Pacific Acrylic Acid Market Insights.

Asia Pacific is positioned to dominate the acrylic acid market during the forecast period with a market share of about 41.80% in 2025. Rapid industrialization and increasing chemical manufacturing capacities are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Expanding construction projects, growing packaging demand, and rising hygiene awareness are significantly boosting adoption. Increasing demand for cost-effective and high-performance materials is further accelerating market growth. Large scale industrial investments support strong regional demand outlook.

According to the United Nations Department of Economic and Social Affairs and the International Energy Agency, Asia Pacific continues to support acrylic acid demand through rapid urbanization and industrial expansion. The region is home to about 60% of the global population, while urban residents are projected to increase substantially by 2050.

Middle East & Africa and Latin America Acrylic Acid Market Insights.

The Middle East & Africa and Latin America region is witnessing steady growth due to industrial diversification and infrastructure expansion. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in water treatment facilities, construction projects, and packaging industries are supporting market expansion. Growing need for advanced coatings and industrial adhesives is further boosting product adoption. Rising industrialization and government initiatives strengthen long term demand outlook across both regions.

According to the UN Department of Economic and Social Affairs and OPEC Annual Statistical Bulletin 2025, the level of urbanization increased to about 81% in Latin America and the Caribbean and 44% in Africa, which led to increased demand for derivatives of acrylic acid in paints, coatings, adhesives, and construction products. Also, according to OPEC, the Middle East was producing about 23 million barrels per day of crude oil in 2025, ensuring an adequate supply of petrochemical feedstock, while increased industrial activities will further enhance acrylic acid applications in both regions.

Market Dynamics

Growth Drivers: Growing construction and infrastructure activities are increasing demand for coatings adhesives and specialty materials

Urbanization and development of the infrastructure have contributed immensely towards the global demand for acrylic acid. Acrylic acid finds a wide range of application in the manufacture of surface coatings, adhesives, and as a cement modifier. Growth in the residential and commercial building activities will contribute towards the growth of the market. High demand for material that can stand up to extreme conditions is fueling the product demand. Investments by governments in infrastructure and transport projects is another factor helping the product gain more acceptance.

According to the United Nations Department of Economic and Social Affairs and the International Energy Agency, global urbanization is accelerating, with 68% of the world’s population projected to live in urban areas by 2050 and nearly 90% of urban growth concentrated in Asia and Africa. The IEA also reports that global building floor area is expected to expand by around 15% by 2030. These measurable construction trends are increasing demand for acrylic acid-based coatings, adhesives, sealants, and specialty construction materials used in modern infrastructure projects.

Restraints: Stringent environmental regulations are increasing compliance costs for chemical manufacturers globally

The rising concerns about the environment have become a source of difficulty for the acrylic acid producers. The governing bodies have introduced tighter norms for emissions and waste disposal. Cleaner technology needs to be adopted by chemical plants. It involves higher expenses in compliance procedures. Growing attention toward the emissions of volatile organic compounds is causing difficulties for manufacturing procedures. Companies need to constantly improve their manufacturing process in order to satisfy these regulations. This can become a hindrance to growth in many developed countries.

Opportunities: Expanding bio based acrylic acid development is creating new growth avenues for manufacturers

Growing importance of sustainable chemicals is providing immense business opportunities in the marketplace. Companies are making efforts towards developing sustainable technologies for producing acrylic acid from biological sources. Increasing consumer demand for eco-friendly products has been promoting these trends. Regulations regarding reduction in carbon footprint have been providing an impetus towards these trends. R&D efforts have been enhancing commercial feasibility of renewable sources of raw materials. Companies have increased investment in developing production processes which are sustainable. Sustainable technologies will decrease reliance on fossil fuels.

As per the European Union's bioeconomy, 17.1 million jobs were created due to its benefits, where bio-based chemicals helped to increase the industrial output. Furthermore, an analysis conducted in 2025 revealed that 80% of carbon was converted into bio-based acrylic acid production processes, which is quite promising in terms of efficiency and production potential.

Recent Developments

-

2026: BASF SE started the world’s first industrial-scale X3D® 3D-printed catalyst production plant at Ludwigshafen, improving reactor efficiency and reducing energy consumption.

-

2025: Saudi Aramco launched Saudi Arabia’s first direct air capture test unit, removing 12 tons of CO₂ annually.

-

2025: Arkema S.A. advanced its Specialty Materials strategy, integrating Dow’s flexible packaging laminating adhesives business acquisition.

-

2024: Dow Inc. announced a new world-scale U.S. carbonate solvents facility supporting electric vehicle battery supply chains.

Acrylic Acid Market Key Players are:

-

BASF SE

-

Dow Inc.

-

Arkema S.A.

-

Nippon Shokubai Co., Ltd.

-

LG Chem Ltd.

-

Mitsubishi Chemical Group Corporation

-

Sasol Limited

-

Saudi Aramco

-

China Petroleum & Chemical Corporation

-

PetroChina Company Limited

-

Formosa Plastics Corporation

-

Reliance Industries Limited

-

INEOS Group Holdings S.A.

-

Shell plc

-

ExxonMobil Corporation

-

Evonik Industries AG

-

PTT Global Chemical Public Company Limited

-

Idemitsu Kosan Co., Ltd.

-

Sinochem Holdings Corporation Ltd.

-

Lotte Chemical Corporation

Acrylic Acid Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.32 Billion |

| Market Size by 2035 | USD 18.40 Billion |

| CAGR | CAGR of 4.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Methyl Acrylate, Ethyl Acrylate, Butyl Acrylate, 2-Ethylhexyl Acrylate, Elastomers, Superabsorbent Polymers, Water Treatment Polymers, Others) • By Application (Adhesives & Sealants, Diapers, Surface Coating, Cement Modifiers, Paper Industry, Textile, Anti-Scalant, Adult Incontinence Products, Others) • By End-Use Industry (Construction, Automotive, Packaging, Consumer Goods, Personal Care, Industrial Manufacturing, Healthcare, Agriculture) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Arkema S.A., Nippon Shokubai Co., Ltd., LG Chem Ltd., Mitsubishi Chemical Group Corporation, Sasol Limited, Saudi Aramco, China Petroleum & Chemical Corporation, PetroChina Company Limited, Formosa Plastics Corporation, Reliance Industries Limited, INEOS Group Holdings S.A., Shell plc, ExxonMobil Corporation, Evonik Industries AG, PTT Global Chemical Public Company Limited, Idemitsu Kosan Co., Ltd., Sinochem Holdings Corporation Ltd., Lotte Chemical Corporation |

Frequently Asked Questions

The acrylic acid market is expected to grow at a CAGR of 4.12% from 2026 to 2035.

The acrylic acid market was valued at USD 12.32 billion in 2025.

Major growth factors include rising demand for superabsorbent polymers, hygiene products, construction materials, packaging applications, and sustainable high-performance coatings.

The Butyl Acrylate segment dominated the market in 2025 due to extensive demand from paints, coatings, adhesives, and expanding construction and automotive industries globally.

Asia Pacific dominated the acrylic acid market due to rapid industrialization, expanding chemical production, increasing construction activities, growing packaging demand, and rising hygiene product consumption.

Get in Touch