Acrylate Market Report Scope & Overview

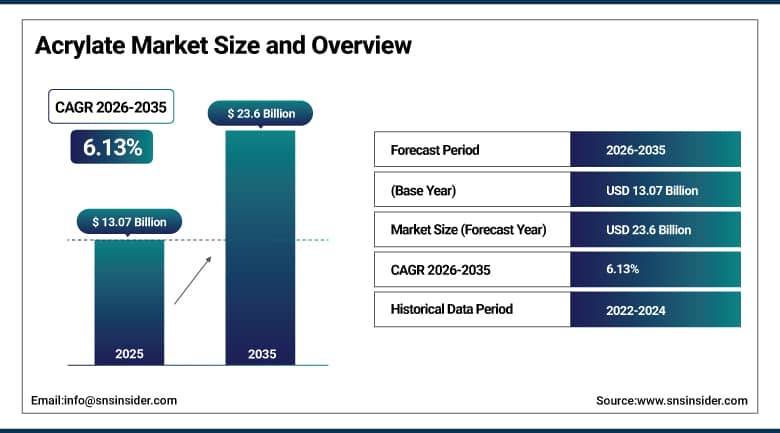

The Acrylate Market was valued at USD 13.07 billion in 2025 and is expected to reach USD 23.6 billion by 2035, growing at a CAGR of 6.13% from 2026–2035.

Acrylates are vital chemicals that serve as starting blocks in the production of plastics and elastomers, paints and lacquers, coatings, adhesives, textiles, and various other materials. Acrylates are predominantly manufactured from propylene and acrylic acid. These chemicals play an important role in the development of materials widely used in construction, automotive, packaging, and consumer goods. Among the current market trends is the transition from solvent-based formulations towards more eco-friendly water-based ones. It is being fueled by the regulation of emissions of volatile organic compounds. Construction growth in Asia and North America, the rising need for low-VOC coatings, as well as new advancements in specialty acrylates are driving the market.

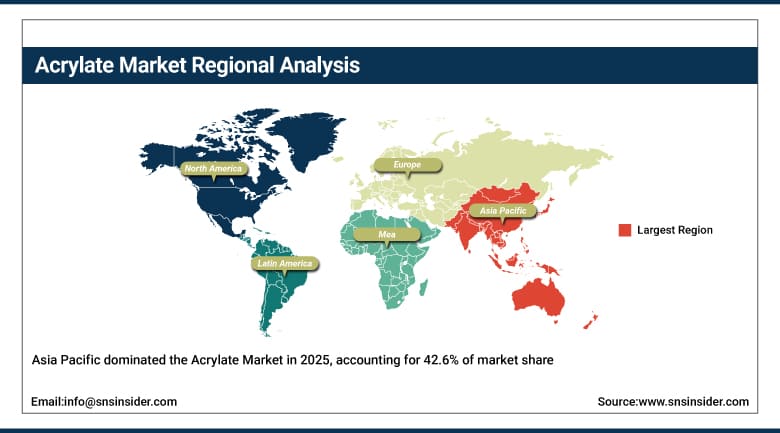

In 2023, Asia Pacific is the major center of both manufacturing and consumption of acrylates and acrylate monomers, capturing more than 42% of the global market share. The reason is a substantial manufacturing capacity in China that uses propylene to produce acrylic acid, providing considerable cost competitiveness against Western suppliers.

One of the promising directions in the future development of the market can be the use of acrylates produced via renewable resources. Indeed, BASF has announced the commercialization of bio-based 2-Octyl Acrylate (73% bio-based material) back in 2023.

Market Size and Forecast

-

Market Size in 2025: USD 13.07 Billion

-

Market Size by 2035: USD 23.6 Billion

-

CAGR: 6.13% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Acrylate Market - Request Free Sample Report

Market Trends

-

Growing adoption of water-based acrylate systems replacing solvent-based formulations in response to VOC emission regulations.

-

Rising demand from the construction industry for acrylate-based weatherproofing coatings and high-performance sealants.

-

The development of UV-curing acrylate polymers that meet fast curing times and high performance in electronics, 3D printing, and specialty coating applications.

-

The manufacture of bio-acrylics using sustainable sources, as the sector trends towards using eco-friendly raw materials.

-

The growing use of acrylic polymer dispersions in the textile industry as finishes and coatings.

-

The expansion of Asia-Pacific facilities by key players in the sector putting pricing pressure on Western firms.

-

The increased use of specialty acrylates in pressure sensitive adhesive applications in label, medical, and electronics assembly applications.

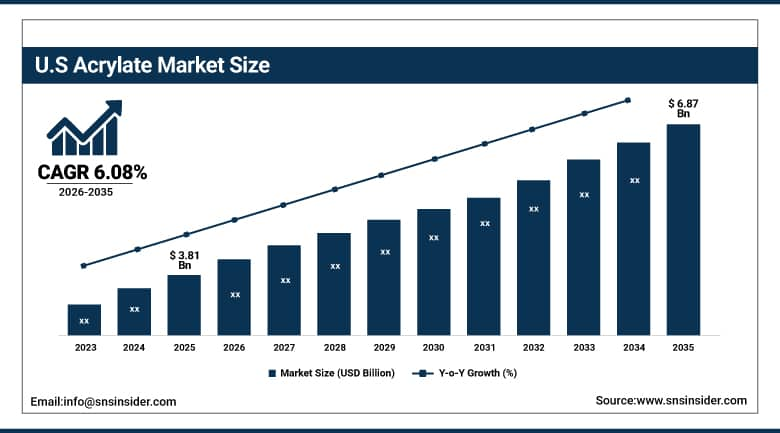

The U.S. Acrylate Market was valued at USD 3.81 billion in 2025 and is expected to reach USD 6.87 billion by 2035, at a CAGR of 6.08% from 2026 to 2035.

The U.S. acrylate market is among the most developed in the world, thanks to high demand from the paints & coatings industry, the adhesive industry, and the construction sector. The U.S. Infrastructure Investment and Jobs Act has boosted spending in construction and renovation activities, thereby boosting the use of acrylate sealants and coatings. U.S. manufacturers such as Dow Inc., BASF Corporation, and Arkema have been developing advanced low-VOC and biobased acrylates. Stringent environmental protection agency emission standards have hastened the move from solvent to water-based acrylate technologies.

According to the American Coatings Association, eco-friendly and low-VOC acrylate compositions constitute more than 30% of the new product introductions in the coatings industry of the United States. This trend is not only regulatory-driven but also represents a strategic advantage, especially for leading brands such as Sherwin-Williams and PPG.

Market Segment Insights

-

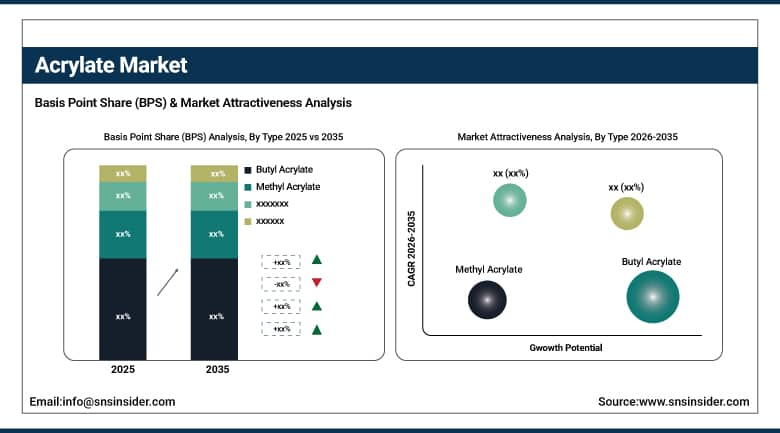

Based on Type, Butyl Acrylate dominated with 42.3% share in 2025 due to extensive use in coatings, adhesives, and textiles.

-

Based on Application, Adhesives & Sealants led with 35.3% share in 2025; Paints & Coatings is the second-largest application.

-

Based on Form, Water-Based acrylate systems dominated with over 55% share in 2025; Solvent-Based forms are declining due to VOC regulations.

-

The Paper & Packaging application segment is growing as flexible packaging adopts acrylate-based coatings for barrier and printability properties.

By Type: Butyl Acrylate & Sealants dominates

Butyl Acrylate occupied the highest revenue share in the Acrylate Market, capturing around 42.3% of the global revenue in 2025. It finds extensive application in water-based coatings, adhesives, sealants, and textiles, thereby fuelling its high demand worldwide. Butyl acrylate exhibits good flexibility, durability, and weathering resistance properties. These properties have made butyl acrylate popular among architectural and automotive coating manufacturers. The quick development of infrastructure in developing nations like China and India, as well as increased use in automotive coatings, further boosts market demand. Methyl acrylate finds application in acrylic fiber production, specialty polymers, and textiles where increased polymer reactivity is desired. High textile manufacturing capacity in regions like Asia Pacific, especially China and India, drives the demand for methyl acrylate. Ethyl Acrylate is extensively applied in water-based emulsion polymers in paints, adhesives, paper coatings, and packaging applications. With its film-forming abilities, flexibility, and glossiness, together with resistance to water, the substance finds application in growing coated paper and packaging uses on a global scale. The 2-Ethylhexyl Acrylate has been applied in pressure-sensitive adhesives in such uses as labels, tapes, protective films, and specialized adhesive items within the medical field. The increasing activities of e-commerce packaging and demand for specialist adhesive products contribute to market growth. Various other acrylates, including acrylic acid, isobutyl acrylate, tert-butyl acrylate, and multifunctional acrylates, are gaining widespread use in various fields.

By Application: Acrylate & Sealants dominates

Acrylate & Sealants dominated the largest share among Application Segments of the Acrylate market due to high usage of acrylate based adhesives in the construction, automotive assembly, packaging, and consumer goods industry. There is a preference for water-based acrylic adhesives due to its eco-friendly nature, adaptability, and high bonding strength, while pressure-sensitive adhesives find wide usage in the labels, tapes, medical bandages, and protective films market. Paints & Coatings is one of the major application segments where Acrylates find a lot of utility owing to their superior performance in terms of durability, UV resistance, weatherability, and color retention. Textiles is yet another field where Acrylates play a key role as they provide properties like softness, wrinkle-resistance, stain resistance, and flame resistance in technical textiles and sports apparels. Acrylates have been used extensively in the manufacture of plastics and polymers, imparting flexibility and impact resistance to automotive and electronic components. Acrylates are also used in paper & packaging products where they offer gloss, printability, water-resistance, and sealability.

By Form: Acrylate-based system dominates

The acrylate-based system accounted for around 55% of the Acrylate Market in 2025 and continues to show the highest growth rate. The intense regulatory push associated with VOC emissions in regions such as Europe, USA, and China is fueling the shift towards eco-friendly water-based acrylate solutions. Water-based systems have started to match up the performance of their solvent-based counterparts in terms of applications including coatings, adhesives, and sealants. They also offer low odor, less toxicity, and better working conditions compared to solvent-based systems. There is still a growing demand for solvent-based acrylate systems in applications that need fast drying, operate in cold temperatures, and require industrial coating properties, but their market share continues to shrink owing to stricter environmental rules and sustainable approaches. Other types of acrylate systems include solid acrylates, UV curable liquid acrylates, and hot melt acrylate systems. Among them, there is a surge in the demand for UV curable acrylates. This is owing to their unique property of quick curing without the need for heat or solvent. UV curable acrylate systems are thus widely used in electronics coatings, optical films, printing inks, and various industrial applications.

Acrylate Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

68% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

51% |

Asia Pacific Acrylate Market Insights

Asia Pacific dominated global acrylate production and consumption with 42.6% market share in 2025 and this leadership will continue through the forecast period. China is both the largest producer of propylene and acrylic acid and the largest consumer of downstream acrylates. The massive construction, textile, and packaging industries in China, India, and Southeast Asia provide the demand base. The region is also seeing growing demand for specialty acrylates as local electronic and automotive manufacturing grows more sophisticated.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Acrylate Market Insights

In North America, the acrylate market had a significant presence in 2025, which was due to the flourishing construction industry in the U.S., the thriving automotive industry, and the prominent position of chemical firms operating there. With the Implementation of the Infrastructure Investment and Jobs Act, the demand for acrylates in the building industry continues to grow. U.S. manufacturers are interested in producing bioacrylate materials that comply with EPA standards. Canada relies on its construction and paper industry.

Europe Acrylate Market Insights

The European market of acrylates is developed well but still very innovative. Tough regulations related to environmental friendliness of chemicals and paints based on them imposed by the EU (REACH and VOC), are driving forces that motivate creation of efficient water-based acrylate coatings. Germany, France, and the UK are the key countries in which demand is growing. Major suppliers from Europe developing such types of acrylates as speciality and bio-acrylates include BASF and Evonik.

Middle East & Africa and Latin America Acrylate Market Insights

The acrylates market in the Middle East is emerging owing to the expansion of the petrochemical complex in countries such as Saudi Arabia, UAE, and Qatar into the specialty chemicals industry. Although the Middle East region remains a relatively small consumer, it enjoys several raw materials benefits due to easy availability of petrochemical intermediates. On the other hand, Africa's market is nascent but witnessing growth due to increasing construction activities in economies like Nigeria and South Africa.

Brazil leads the Latin American market for acrylates owing to its strong automotive and construction industries that require considerable quantities of coatings and adhesives. Argentina, Mexico, and Colombia also have their fair share of demand. Growth in the Latin American acrylates market has been spurred by increased local paint & coating producers who are moving away from imports towards locally produced acrylate formulations.

Market Growth Drivers

-

Construction activity and the shift to water-based coatings are the core growth drivers

Globally, there is a huge investment being made in construction projects, especially in Asia Pacific and North America. Such investments create direct and constant demand for acrylate-based paints, adhesives, sealants, and waterproofing systems. Each new construction project requires acrylate-based products during its many different stages. In addition, environmental laws that prohibit solvent-based coatings are compelling manufacturers to switch from solvent-based acrylic paints to water-based acrylic paints, thereby increasing the addressable market for water-based acrylates.

The Green Deal in Europe and the building efficiency measures under the Inflation Reduction Act in the United States are contributing to a favorable trend for high-performance architectural coatings. New buildings require improved insulation paints and higher-quality exterior surface coating paints, which can only be provided by acrylate-based products.

Market Restraints

-

Raw material price volatility and feedstock concentration create supply risks

The acrylates industry faces substantial risks due to fluctuation in the costs of the raw materials used in production. For instance, both propylene and acrylic acid, which form the core feedstock, are petroleum derivatives, and their prices depend on those of crude oil. Moreover, the production of acrylic acid is done at only a few facilities around the world, and thus any disruption in production owing to environmental conditions, accidents, or maintenance activities poses serious supply issues.

Market Opportunities

-

Bio-based acrylates and specialty applications in electronics and 3D printing

The development of commercially viable bio-based acrylates offers a major growth opportunity as it addresses both sustainability goals and the need to reduce dependence on petroleum feedstocks. Companies that can produce high-purity bio-based acrylic acid at competitive cost will gain significant market advantage as ESG requirements tighten. On the specialty side, UV-curable acrylates for electronics encapsulation, 3D printing resins, and optical coatings are higher-value applications growing much faster than commodity coatings and adhesives.

Recent Developments

-

2025: Dow Inc. expanded its acrylic acid and acrylate production capacity at its Texas Gulf Coast facilities, adding 200,000 metric tonnes annually to serve growing demand from the North American coatings and adhesives markets.

-

2024: Arkema completed the acquisition of specialty acrylate resin producer Covestro's resins business, expanding its portfolio of high-performance acrylate products for industrial coatings, adhesives, and electronics applications.

-

2023 (September): BASF introduced commercial production of 2-Octyl Acrylate with 73% bio-based content confirmed by C-14 analysis, marking a significant step toward sustainable acrylate production at industrial scale.

Key Players

-

BASF SE

-

Dow Inc.

-

Arkema S.A.

-

Celanese Corporation

-

Allnex Group

-

Evonik Industries AG

-

Nippon Shokubai Co. Ltd.

-

Mitsubishi Chemical Corporation

-

LG Chem Ltd.

-

CNOOC and Shell Petrochemicals

-

Formosa Plastics Corporation

-

Toagosei Co. Ltd.

-

Sasol Limited

-

Sumitomo Chemical Co. Ltd.

-

Wanhua Chemical Group Co. Ltd.

-

Solvay S.A.

-

Jiangsu Jurong Chemical Co. Ltd.

-

H.B. Fuller Company

-

Sartomer

-

DSM

Acrylate Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.07 Billion |

| Market Size by 2035 | USD 223.6 Billion |

| CAGR | CAGR of 6.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Butyl Acrylate, Methyl Acrylate, Ethyl Acrylate, 2-Ethylhexyl Acrylate, Others) • By Application (Adhesives & Sealants, Paints & Coatings, Textiles, Plastics, Paper & Packaging, Others) • By Form (Water-Based, Solvent-Based, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Arkema S.A., Celanese Corporation, Allnex Group, Evonik Industries AG, Nippon Shokubai Co. Ltd., Mitsubishi Chemical Corporation, LG Chem Ltd., CNOOC and Shell Petrochemicals, Formosa Plastics Corporation, Toagosei Co. Ltd., Sasol Limited, Sumitomo Chemical Co. Ltd., Wanhua Chemical Group Co. Ltd., Solvay S.A., Jiangsu Jurong Chemical Co. Ltd., H.B. Fuller Company, Sartomer, DSM |

Frequently Asked Questions

The Acrylate Market is expected to grow at a CAGR of 6.13% from 2026 to 2035.

The Acrylate Market was valued at USD 13.07 billion in 2025.

Butyl Acrylate dominated with 42.3% share in 2025, driven by its widespread use in coatings, adhesives, and textiles.

Adhesives & Sealants led with 35.3% share, followed by Paints & Coatings as the second-largest application.

Asia Pacific led with 42.6% of global market share, driven by China's dominant acrylate production and consumption.

Get in Touch