Advanced Process Control Market Report Scope & Overview:

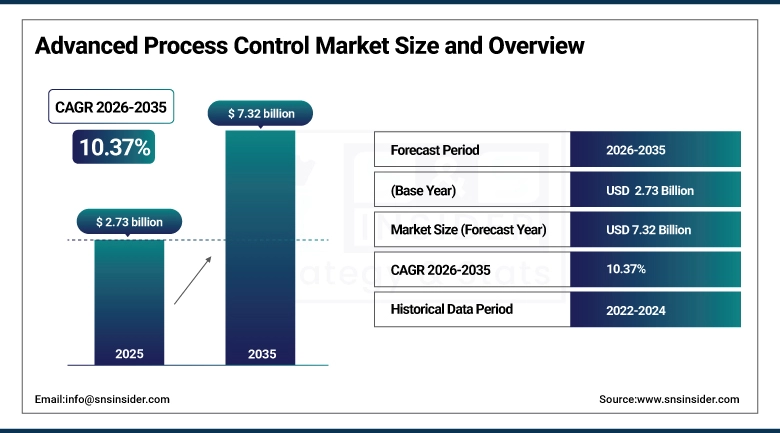

The Advanced Process Control Market Size was valued at USD 2.73 billion in 2025 and is expected to reach USD 7.32 billion by 2035, growing at a CAGR of 10.37% from 2026-2035. Growth in the APC market is being driven by the rising demand for greater operational efficiency, lower costs, and increased quality of products. Moreover, the adoption of Industry 4.0 concepts, use of artificial intelligence (AI), and real-time analytics are adding impetus to the industry’s growth. Environmental legislation and the requirement for energy optimization are also factors that are promoting the implementation of advanced controls.

The U.S. Department of Energy's Industrial Efficiency and Decarbonization Office estimates that advanced process control deployment across U.S. process industries could reduce industrial energy consumption by 5-15% annually. DOE's Better Plants program has documented APC energy savings of 3-8% per plant at over 200 participating industrial facilities.

Advanced Process Control Market Size and Forecast

-

Market Size in 2025: USD 2.73 Billion

-

Market Size by 2035: USD 7.32 Billion

-

CAGR: 10.37% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Advanced Process Control Market - Request Free Sample Report

Advanced Process Control Market Trends

-

Cloud deployment of APC software is eliminating the need for expensive dedicated servers at process facilities and enabling continuous algorithm updates without site disruption.

-

Non-linear Model Predictive Control adoption is growing in pharmaceutical batch processes and specialty chemical production where reaction kinetics exceed linear model approximation capability.

-

Digital twin integration with APC systems is enabling operators to test control strategy changes in simulation before deploying them to live processes.

-

AI-powered fault detection and diagnostic modules are being embedded directly into APC platforms to provide predictive maintenance alerts alongside real-time process optimization.

-

Smaller industrial operators in food and beverage, specialty chemicals, and generic pharmaceuticals are entering the APC market through subscription-based software models that lower upfront investment.

-

OPC UA and ISA-95 standard adoption is simplifying APC integration with existing DCS and MES infrastructure, reducing implementation timelines from months to weeks in some configurations.

-

Sustainability reporting requirements are driving operators to instrument and optimize processes for energy consumption and emissions metrics alongside traditional yield and throughput KPIs.

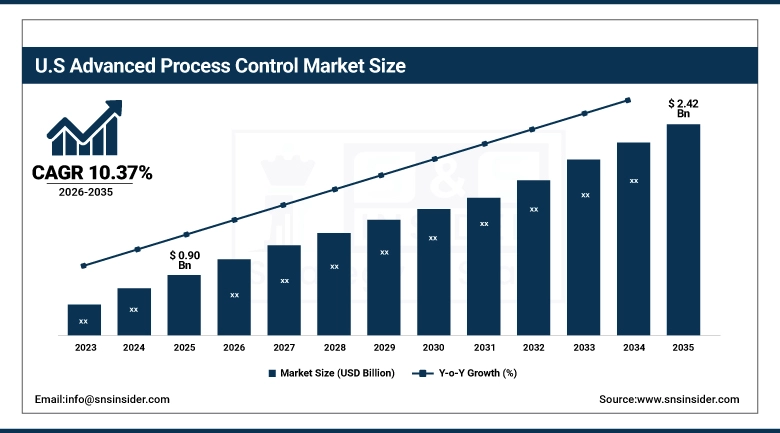

U.S. Advanced Process Control Market Size Outlook:

The U.S. Advanced Process Control Market was valued at USD 0.90 billion in 2025 and is expected to reach USD 2.42 billion by 2035, growing at a CAGR of 10.37% from 2026-2035. The U.S. is the world's most developed Advanced Process Control market, built on the country's enormous oil and gas refining capacity, the world's second-largest chemical industry, and a pharmaceutical manufacturing sector that is increasingly subject to FDA Process Analytical Technology guidance that APC directly enables. Companies including AspenTech, Emerson, Honeywell, and Rockwell Automation are headquartered or have major APC development operations in the U.S., creating a uniquely deep technology ecosystem.

The FDA's Process Analytical Technology (PAT) guidance explicitly endorses real-time process monitoring and multivariate control the functional core of APC as the preferred approach to pharmaceutical quality assurance. FDA's 21st Century Pharmaceutical Quality initiative has made APC adoption a de facto compliance pathway for new drug manufacturing approvals.

Advanced Process Control Market Segment Analysis

-

By Offering, Software segment dominated the Advanced Process Control Market with ~44% share in 2025; Services segment fastest growing (CAGR ~12.38%).

-

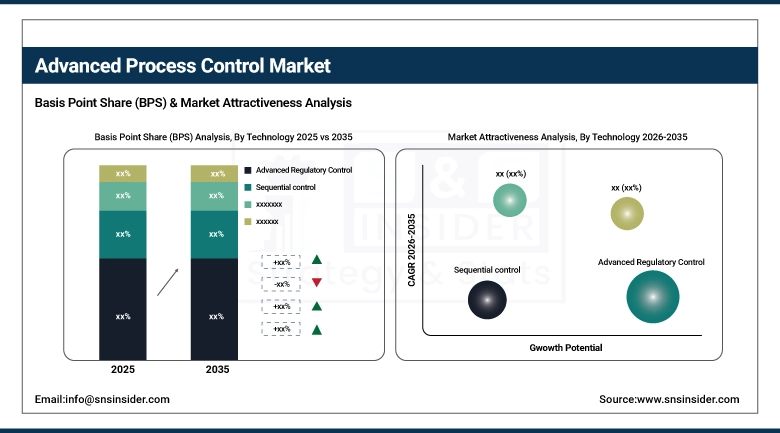

By Technology, Advanced Regulatory Control (ARC) segment dominated with ~33% share in 2025; Multivariable Model Predictive Control (MPC) fastest growing (CAGR ~12.41%).

-

By Organization Size, Large Enterprises dominated with ~69% share in 2025; Small & Medium Enterprises fastest growing (CAGR ~11.95%).

-

By End User, Oil & Gas segment dominated with ~27% share in 2025; Pharmaceuticals fastest growing (CAGR ~14.04%).

By Technology, Advanced Regulatory Control segment dominates the Advanced Process Control Market, Multivariable MPC segment expected to grow fastest

Advanced Regulatory Control maintained the largest technology share of approximately 33% in 2025. ARC sits at the interface between basic PID control and full model predictive control it encompasses cascade control, feed-forward compensation, ratio control, and other structures that improve basic regulatory performance without requiring the full model-building investment of MPC. For process facilities where full MPC deployment is not yet justified either because the scale is too small or the process interactions are manageable with simpler strategies ARC delivers meaningful performance improvement at lower cost and complexity.

Multivariable Model Predictive Control is the fastest-growing technology segment at approximately 12.41% CAGR, reflecting the progressive expansion of MPC from its historic base in large-scale refining and petrochemicals into adjacent industries. MPC's ability to simultaneously optimize across multiple interacting process variables while respecting equipment constraints is uniquely valuable in complex continuous operations and as pharmaceutical batch processes, polymer plants, and renewable fuel refineries increasingly encounter this multi-variable optimization challenge, they are turning to MPC as the validated solution.

By Offering, Software segment dominates the Advanced Process Control Market, Services segment expected to grow fastest

Software held approximately 44% of the Advanced Process Control Market in 2025, reflecting the fundamental nature of modern APC as an intelligence layer rather than a hardware system. APC software platforms including AspenTech's AspenONE, Honeywell's Profit Suite, and Emerson's DeltaV Predict deliver real-time optimization, constraint management, and model-based control logic that sits above the basic regulatory control layer of the distributed control system. The migration from perpetual licenses toward SaaS and subscription models has opened software-based APC to a broader operator population by converting large upfront capital expenditures into predictable operational costs.

Services is projected to grow at the highest CAGR of approximately 12.38% through 2035, and the underlying driver is structural: APC systems require ongoing model maintenance, performance monitoring, and re-identification as process conditions evolve, feedstocks change, and equipment ages activities that most industrial operators cannot perform effectively with internal staff alone. As the APC installed base grows, the demand for specialist services covering model re-tuning, performance auditing, control strategy enhancement, and system upgrades grows proportionally.

By End User, Oil & Gas segment dominates the Advanced Process Control Market, Pharmaceuticals segment expected to grow fastest

Oil and Gas retained the leading end-user position at approximately 27% of market revenue in 2025. Crude distillation, fluid catalytic cracking, hydrotreating, reforming, and alkylation units are each mature APC application domains where the technology has demonstrated return on investment in reduced energy consumption, improved product yield, and higher throughput. A typical large refinery APC implementation across all major process units can improve margins by USD 1-5 per barrel of crude a quantified ROI that makes the business case straightforward for operators.

Pharmaceuticals is projected to grow at the highest end-user CAGR of approximately 14.04% through 2035, driven by the FDA and EMA's explicit embrace of APC-enabled continuous manufacturing and the competitive pressure to reduce batch-to-batch variability that drives product rejections and costly reprocessing. The shift from batch to continuous pharmaceutical manufacturing supported by both regulatory guidance and economic incentives is inherently an APC-enabling transition, as continuous processes require precisely the kind of real-time multi-variable control and disturbance rejection that APC systems provide.

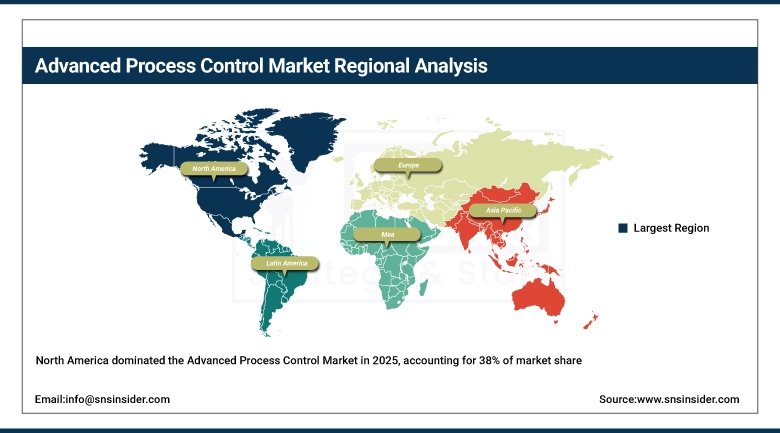

Advanced Process Control Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

Saudi Arabia |

42% |

|

Latin America |

Brazil |

52% |

North America Advanced Process Control Market Insights

North America dominated the global Advanced Process Control Market with approximately 38% revenue share in 2025. The U.S. oil refining complex operating approximately 130 active refineries with combined capacity exceeding 18 million barrels per day represents the world's largest single base of APC deployments, and the ongoing modernization of aging process units is driving steady upgrade spending. The U.S. chemical industry, the world's second largest, is another major demand driver, particularly as sustainability pressures compel chemical manufacturers to optimize energy intensity and reduce waste generation. AspenTech, headquartered in Boston, and Honeywell's Process Solutions division are among the dominant global APC software suppliers, with substantial domestic market share reinforced by deep integration partnerships with major U.S. industrial operators.

The U.S. Department of Energy reports that the chemical manufacturing sector alone consumes approximately 28% of U.S. industrial energy. DOE's Better Plants program documents that APC deployment at member sites reduces energy intensity by an average of 2.5% annually, creating a quantified regulatory alignment incentive for broader APC adoption across the sector.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Advanced Process Control Market Insights

Asia Pacific is the fastest-growing region with a projected CAGR of approximately 12.20% through 2035, driven by the rapid capacity expansion of process industries across China, India, South Korea, and Southeast Asia, combined with progressive adoption of automation and digitalization in manufacturing operations that were previously less instrumented than Western counterparts. China's enormous petrochemical industry which has added more new refining and chemical capacity in the past decade than any other country is a major source of new APC deployment demand, both for grassroots projects where APC is specified from design and for brownfield upgrades of existing capacity. India's pharmaceutical manufacturing sector the world's largest generic drug producer by volume is an increasingly important APC market as FDA inspections and export quality requirements push companies toward tighter process control.

China's Ministry of Industry and Information Technology (MIIT) 14th Five-Year Plan for chemical industry digitalization mandates advanced process control deployment across regulated chemical plants as a condition for continued operating certification. India's CDSCO has aligned pharmaceutical manufacturing standards with FDA PAT guidelines, requiring real-time process monitoring at export-oriented API facilities.

Europe Advanced Process Control Market Insights

Europe held approximately 25% of the global Advanced Process Control Market in 2025, supported by the continent's mature refining, chemical, and pharmaceutical manufacturing industries and increasingly stringent energy efficiency and emissions regulations that make process optimization investment commercially compelling. Germany's large chemical industry anchored by BASF, Covestro, and Lanxess is among the most intensive APC users in the world, with decades of deployment experience in complex continuous chemical processes. The EU's Emissions Trading System carbon pricing is creating direct financial incentives for APC-driven energy efficiency improvements: every ton of CO2 avoided translates into a tradeable permit value that directly improves project economics for APC investment decisions.

The EU Emissions Trading System (ETS) carbon price, which has ranged between EUR 60-100 per tonne CO2 in recent years, creates a direct financial return for energy efficiency improvements achieved through APC deployment. European process manufacturers report APC energy optimization payback periods of 12-18 months under current carbon pricing.

Middle East & Africa and Latin America Advanced Process Control Market Insights

The Middle East represents one of the most APC-intensive regions globally relative to its industrial scale, because the major national oil companies Saudi Aramco, ADNOC, QatarEnergy, and Kuwait Petroleum have been systematic early adopters of APC across their large refining and gas processing complexes. Saudi Aramco in particular has deployed APC at scale across its refinery network and has partnered with AspenTech, Honeywell, and Yokogawa for comprehensive APC implementations that optimize crude distillation, hydrocracking, and gas plant operations simultaneously. In Latin America, Brazil's Petrobras drives the majority of regional APC demand through its extensive refinery network, while Colombia's Ecopetrol and Mexico's PEMEX represent emerging deployment markets as national oil companies modernize aging process infrastructure.

Saudi Aramco's Operational Excellence Management System mandates APC deployment as a standard practice across all refinery process units. Aramco's annual sustainability reports document APC-driven energy efficiency improvements averaging 3-5% per refinery unit, representing hundreds of millions of dollars in annual operational savings.

Advanced Process Control Market Growth Drivers:

-

Accelerating industry automation and demand for real-time process optimization driving global advanced process control investment

The economic case for Advanced Process Control has always been compelling for the right scale of operation, but several converging forces are making it compelling for a wider range of operators than ever before. Energy price volatility has moved to the top of the cost management agenda for energy-intensive process manufacturers, and APC is one of the most quantifiably effective tools for managing energy consumption without sacrificing throughput or product quality. The digitalization of process plant instrumentation more sensors, better data historians, improved network connectivity has reduced the data infrastructure investment required to implement APC, lowering the effective barrier to entry. And the regulatory environment, from FDA pharmaceutical quality to EU carbon pricing to EPA chemical safety, is creating compliance frameworks that APC capabilities directly address, turning optimization investment into regulatory risk reduction investment simultaneously.

The International Energy Agency (IEA) identifies advanced process control as a key energy efficiency lever for the chemicals sector, estimating global implementation could reduce sector energy intensity by 10-15%. The IEA's World Energy Outlook 2024 specifically cites APC alongside electrification and process heat efficiency as priority decarbonization tools for heavy industry.

Advanced Process Control Market Restraints:

-

Cybersecurity vulnerabilities and high integration costs with legacy systems constraining advanced process control market growth

APC adoption faces two structural constraints that reinforce each other. The first is the IT/OT convergence challenge: modern cloud-connected APC platforms require network pathways between process control systems and external servers that were never designed to exist in traditional operational technology security architectures. The more connected an APC system becomes, the more exposed the underlying process control infrastructure is to cybersecurity risks a concern that has been validated by real incidents targeting industrial control systems. Many plant operators and their IT security teams have imposed connectivity restrictions that complicate or limit cloud APC deployment models, pushing projects toward on-premise configurations that cost more and take longer to implement.

Advanced Process Control Market Opportunities:

-

Cloud-native APC platforms and AI-driven predictive analytics creating transformative opportunities in industrial process optimization globally

The architectural shift toward cloud-native APC deployment represents the most transformative opportunity in the market's evolution since model predictive control first reached commercial maturity. Cloud APC eliminates the facility-specific hardware investment that historically made small-scale deployments economically marginal, and the subscription model converts the capital allocation question into an operating cost justification that is far easier to approve in most industrial procurement frameworks. Beyond access economics, cloud platforms enable APC developers to push algorithm improvements and model updates continuously without requiring plant maintenance shutdowns a capability that accelerates the improvement cycle for deployed systems and creates ongoing value delivery that sustains subscription relationships. The integration of generative AI and large-scale process data models into APC platforms is beginning to reduce the model-building phase that historically required expensive specialist consultancy, potentially compressing implementation timelines from months to weeks for standardized process unit configurations.

Recent Developments:

-

2026: AspenTech released Aspen Mtell 2026 with an integrated generative AI model-building capability that autonomously constructs initial MPC process models from existing historian data, reducing the traditional model identification phase from 8-12 weeks of specialist engineering to less than two weeks for standard distillation and reaction unit configurations.

-

2025: Honeywell Process Solutions expanded its Profit Controller MPC platform with new cloud-native deployment architecture and an AI-driven model health monitoring module that automatically detects process model mismatch and initiates model re-identification routines, reducing the need for scheduled manual model maintenance at deployed refinery and chemical plant installations.

-

2025: Emerson Electric launched its DeltaV MPC Pro platform with integrated cybersecurity features compliant with IEC 62443 Level 2 requirements, specifically designed to address the connectivity security concerns that have slowed cloud APC adoption at process facilities operating under stringent OT cybersecurity frameworks and regulatory audit requirements.

Advanced Process Control Companies are:

-

Aspen Technology, Inc (AspenTech)

-

Honeywell International Inc.

-

Emerson Electric Co.

-

Siemens AG

-

ABB Ltd.

-

Yokogawa Electric Corporation

-

Schneider Electric SE

-

General Electric Company (GE Vernova)

-

AVEVA Group plc (Schneider Electric)

-

Pavilion Technologies (Rockwell)

-

KBC Advanced Technologies (Yokogawa)

-

Spartan Controls Ltd.

-

Apex Optimization Inc.

-

DMC3 (Kelley-Mahon)

-

ProcessECC Inc.

-

Tecnimont ICB Pvt. Ltd.

-

Control Station, Inc.

-

Quanta Associates

-

Perceptive Engineering Ltd.

Advanced Process Control Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.73 Billion |

| Market Size by 2035 | USD 7.32 Billion |

| CAGR | CAGR of 10.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Service) • By Technology (Advanced Regulatory Control, Multivariable Model Predictive Control, Sequential Control, Inferential Control, Compressor Control) • By Enterprise Size (Small & Medium Enterprises, Large Enterprises) • By End Use (Oil and Gas, Chemicals, Pharmaceuticals, Energy & Power, Paper & Pulp, Mining, Minerals, and Metals, Food & Beverages, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd., Aspen Technology Inc, AVEVA Group Limited, General Electric Company, Honeywell International Inc., Mitsubishi Electric Corporation, Panasonic Corporation, Rockwell Automation, Rudolph Technology, SAP SE, Siemens, Yokogawa Electric Corporation, Emerson Process Management, Schneider Electric, Invensys, Endress+Hauser, Linde Engineering, Kroger Inc., Veolia North America. |

Frequently Asked Questions

Ans: North America dominated the Advanced Process Control Market in 2025.

Ans: The Pharmaceuticals segment is expected to register the fastest CAGR of approximately 14.04% in the Advanced Process Control Market.

Ans: The Software segment dominated the Advanced Process Control Market with approximately 44% share in 2025.

Ans: The Advanced Process Control Market was valued at USD 2.73 billion in 2025.

Ans: The Advanced Process Control Market is expected to grow at a CAGR of 10.37% from 2026 to 2035.

Get in Touch