Satellite Ground Station Market Report Scope & Overview:

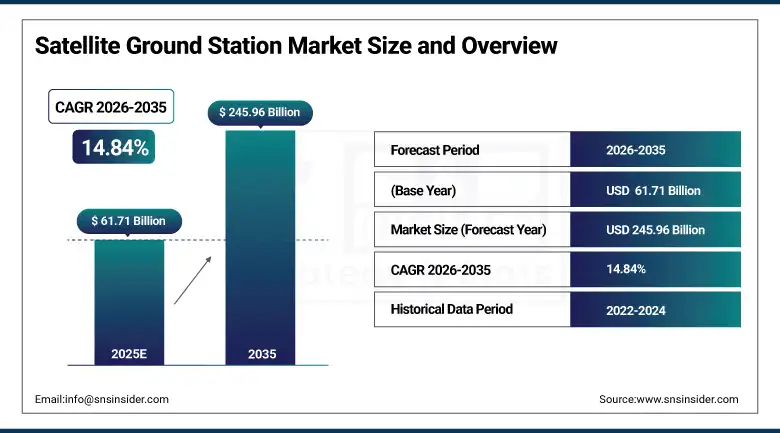

The Satellite Ground Station Market size is valued at USD 61.71 Billion in 2025 and is expected to reach USD 245.96 Billion by 2035 and grow at a CAGR of 14.84% over the forecast period 2026-2035.

The Satellite Ground Station market will grow derivatives of the large number of satellite launches. Increased demand for high-speed broadband, Earth observation data and secure defense communications is driving both governments and commercial operators to invest in sophisticated ground station networks. The rise of software-defined systems, cloud based ground station services and automation are driving operational efficiencies and eliminating infrastructure costs at the ground level. Moreover, rising investments in space exploration missions, increase the participation of private players and proliferation of GSaaS (Ground Station as a Service) are accelerating the growth of the market over period 2026-2035.

According to industry studies, over 50% of Satellite Ground Station demand is driven by last-mile delivery services, fueled by rapid e-commerce growth, rising food delivery demand, and the need for cost-efficient logistics.

Market Size and Forecast:

-

Market Size in 2025: USD 61.71 Billion

-

Market Size by 2035: USD 245.96 Billion

-

CAGR: 14.84% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Satellite Ground Station Market - Request Free Sample Report

Satellite Ground Station Market Trends:

-

LEO & MEO Constellations Growth: Rising low- and medium-earth orbit satellites drive demand for distributed ground station networks.

-

Ground Station as a Service (GSaaS): Cloud-based, on-demand services reduce CapEx and enable scalable satellite operations.

-

Software-Defined & Automated Systems: AI-driven antennas and scheduling improve efficiency and enable remote management.

-

Cloud & Edge Integration: Real-time data handling and analytics for communication, Earth observation, and defense.

-

Commercial & Defense Expansion: Broadband, military, and space research applications boost investment and upgrades.

U.S. Specialty Satellite Ground Station Market Insights:

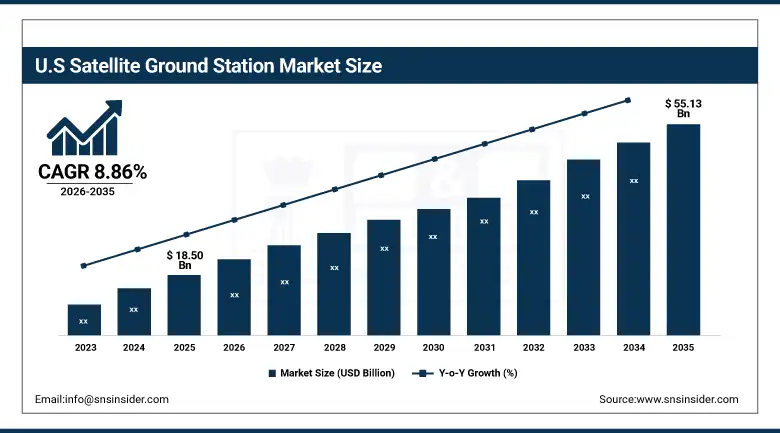

The U.S. Satellite Ground Station Market size is USD 18.50 Billion in 2025 and is expected to reach USD 55.13 Billion by 2035, growing at a CAGR of 8.86% over the forecast period of 2026-2035.

The U.S. demand for Satellite Ground Station is driven by increasing satellite launches, growing LEO and MEO constellation deployment, rising demand of high speed broadband, Earth observation and defense communications. Breakthroughs in SD systems, automation and GSaaS in the cloud deliver operational efficiency and scalability along with supportive government program, space exploration efforts and growing private sector investments drive adoption.

Satellite Ground Station Market Growth Drivers:

-

Rising Demand for High-Speed Data and Satellite Connectivity

The Satellite Ground Station market is being driven by the growing number of satellite launches, particularly in LEO and MEO constellations where dependable ground infrastructure for telemetry, tracking and data downlink is essential. Increasing need for high-speed broadband, earth observing satellite and secured defense communication also drive the market growth. Industry representatives estimated that the proportion of demand derived from commercial broadband and defense is in excess of 45%, so its importance in the market acquisition processes recognized. Moreover, the transition to cloud-based GSaaS and software-driven systems facilitates scalable and cost-effective operations and drives market growth.

Satellite Ground Station Market Growth Restraints:

-

High Infrastructure Costs and Regulatory Challenges

The growth of the market is limited by factor such as high initial investment for ground station infrastructure which would includes acquisition for antennas, tracking system and control software. Adherence to stringent regulatory regimes, spectrum assignment conditions, and security requirements can slow down network roll-out and add extra operational expenditure. Research showed that around 38% of the planned ground stations were delayed due to spectrum licensing, frequency issues and cyber security requirements. Additionally, difficulties in interfacing older technology with cloud-broad host telecommunications or automatic systems are obstructing its swift adoption in some areas.

Satellite Ground Station Market Growth Opportunities:

-

Cloud Integration, Smart Satellites, and Advanced Data Services

There are also tremendous opportunities to combine ground stations with cloud platforms, IoT networks and real-time data processing systems for the burgeoning satellite applications including earth observation, AI-based analytics and broadband extension. Increased investment in GSaaS, optical ground stations and automated antenna networks help manage multiple satellites and high-throughput missions. According to market reports, the growth of cloud enabling ground station deployments is at a rate of 25 percent per year, representing a significant opportunities for adoption. Growing penetration of mission-critical communication, space exploration programs and private sector satellite projects is expected to offer long-term growth prospects in developed and emerging markets.

Satellite Ground Station Market Segment Highlights:

-

By Solutions: In 2025, hardware dominated with 48% share; Ground Station as a Service is the fastest-growing segment during 2026–2035.

-

By Platform: In 2025, fixed ground stations dominated with 52% share; on-the-move stations are the fastest-growing segment during 2026–2035.

-

By Frequency Band: In 2025, C-Band dominated with 45% share; Ka-Band is the fastest-growing segment during 2026–2035.

-

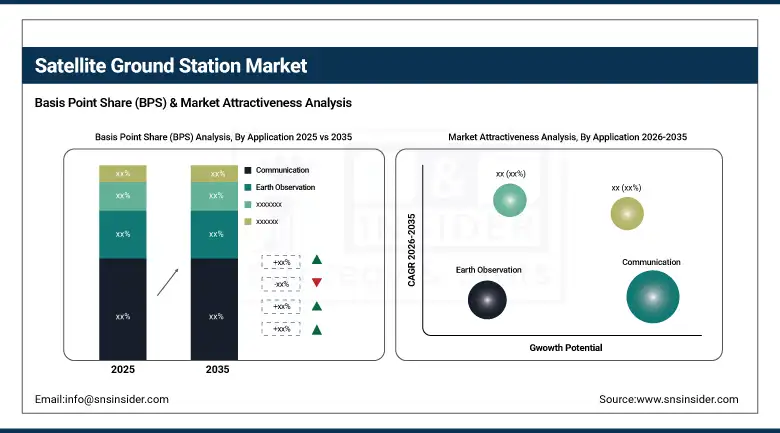

By Application: In 2025, communication dominated with 40% share; Earth observation is the fastest-growing segment during 2026–2035.

Satellite Ground Station Market Segment Analysis:

By Solutions: Hardware Leads as GSaaS & Software Gain Momentum

Hardware segment leads the Satellite Ground Station market owing to rising need for antennas, tracking systems, receivers, and transmitters which are necessary for accurate and strong satellite communication respectively telemetry also data output. The high-costs of physical infrastructure contribute to hardware remaining there largest-earning segment.

Software and GSaaS(ground station as a service) is also actively emerging, much of this has to do with cloud-based command, automation, scheduling and data management. AI-driven operations, remote monitoring and integration with mission control platforms are being increasingly used to work more efficiently, at lower cost and at a scale that can be deployed across many satellites and constellations.

By Platform: Fixed Ground Stations Lead as On-the-Move Stations Expand

Fixed (Land & Naval) ground stations are the most widely used type as these stations ensure reliable communication through continuous connectivity with satellites, consequently supporting various large-scale applications such as commercial, defense and government. They offer a robust underlying network for the data reception and mission critical services.

On-the-move stations are one of the fastest growing segments, thanks to growing demand for mobile communications (tactical military applications and satellite data reception on board ships, aircraft and vehicles). Rapid adoption Significant progress in portable antennas, automatic tracking and deployment flexibility is driving widespread uptake, with defense and emergency communication applications at the forefront.

By Frequency Band: C-Band Leads as Ka-Band Expands.

C-Band dominates the market due to its reliability, wide coverage, and long-established use in satellite communications for both commercial and defense applications. Its resilience to weather interference and extensive adoption across legacy systems make it the preferred choice.

Ka-Band is expanding rapidly, driven by the rising demand for high-throughput satellite (HTS) services, broadband connectivity, and real-time data applications. Technological improvements in antenna design, signal processing, and frequency management are enabling faster adoption of Ka-Band for both commercial broadband and Earth observation services.

By Application: Communication Leads as Earth Observation Expands

Communication has a market predominance on account of large number of satellite-based broadband, telecommunications, and data relay services. Operators use ground stations for 24/7 connectivity and mission-critical satellite command operations.

There is a growing trend in Earth observation, driven by the increased need for real-time imaging, climate control, disaster monitoring and remote sensing needs. High resolution sensors with automated data processing and cloud apps driving large customer adoption in this sector - both commercial (mapping, monitoring) and government-owned.

Satellite Ground Station Market Regional Analysis:

North America Satellite Ground Station Market Insights:

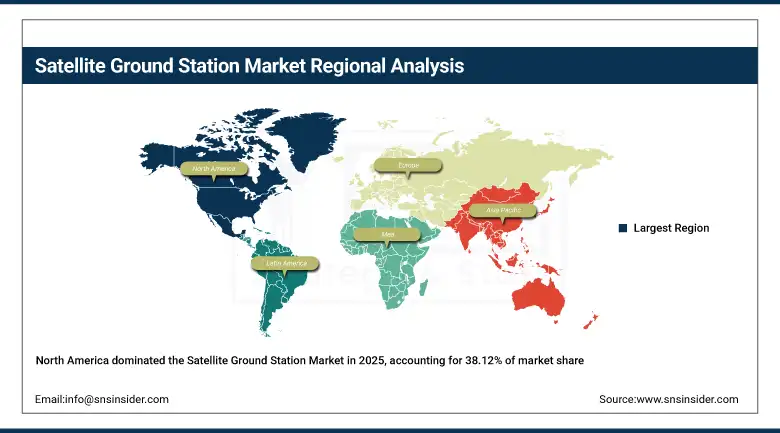

In 2025, North America’s Satellite Ground Station Market accounting for the highest regional revenue share of approximately 38.12% in 2025. North America is leading due to the presence of mature space infrastructure and high number of commercial and government satellite operators, which has resulted in substantial investments in advanced ground station networks. The deployment at a large scale has been facilitated by adopting advanced technologies like the software-defined systems, cloud-based GSaaS and automated antenna management. Furthermore, large investments by the defense sector and military as well as early deployment of LEO and MEO constellations coupled with favorable regulatory policies that have contributed to huge market demand in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. and Canada Satellite Ground Station Market insights:

The U.S. and Canada Satellite Ground Station market growth is influenced by surging number of satellite launches, increasing LEO and MEO constellation deployment and growing demand for broadband services, Earth observation and defense communications. Deployment of cloud-based GSaaS, software-defined systems and automation have improved operation efficiency and scalability.

Asia Pacific Satellite Ground Station Market Insights:

Asia Pacific represents a high-growth region for the Satellite Ground Station market, registering a CAGR of 21.01% during 2026–2035. This rapid growth is powered by a burgeoning national space program and satellite fleet, as well as growing demand for broadband services, Earth observation satellites, and government communications. Strong interest in cloud-based GSaaS and automated ground systems coupled with the region’s increasing technology uptake, as well as growing commercial satellite industry investment have driven demand. Over the same period, a combination of supportive government policies, private sector engagement and developments in software-defined and automated ground station technologies will combine to expedite deployments, underpinning market expansion during 2026–2035.

Europe Satellite Ground Station Market Insights:

Europe satellite ground station market is being propelled by high level government and defense spending, increasing use of LEO and MEO satellite constellations as well as mounting demand for broadband, Earth observation and scientific missions. The adoption of advanced technologies such as software-defined, automated antennas and cloud-based GSaaS (ground systems as a service) lowers operational costs and increases scalability. Favorable regulations, joint space ventures and private investments have facilitated the penetration, resulting in consistent growth of the market demand across the region from 2026–2035.

Latin America Satellite Ground Station Market Insights:

Satellite Ground Station market in Latin America is being increasingly driven by the surging demand for robust broadband connectivity, Earth observation services and telecommunications. Rise in expenditure on national space programs, regional satellite launches and private investments are driving the demand for ground stations. Cloud-enabled GSaaS, software-defined systems and automated ground networks are enabling high efficiency and scalability. Favorable government regulations, collaboration plays, and rising commercial applications are complementing deployment to facilitate industry growth in the region between 2026 and 2035.

Middle East and Africa Satellite Ground Station Market Insights:

The market for the Middle East and Africa Satellite Ground Stations is influenced by growing investments in national space programs, satellite communication infrastructure, as well as military applications. Increase in the demand for broadband, Earth observation, and remote sensing services is driving the requirement of the trustworthy ground stations. Cloud-based GSaaS, software-defined systems, and automation achieve operational efficiency and scalability. Enabling government policies, its regional approach and growing private sector involvement will facilitate deployments in the region, causing market growth to expand across the region from 2026 to 2035.

Satellite Ground Station Market Competitive Landscape:

General Dynamics Mission Systems is a business unit of American defence and aerospace company General Dynamics that focuses on secure communication and information systems, and technology. It is in support of programs such as MUOS and Proliferated Warfighter Space Architecture that relies on ground segment solutions for satellite command, control and data networks.

-

In 2025: The company is advancing integrated ground systems for the Space Development Agency’s Proliferated Warfighter Space Architecture, enhancing connectivity for missile tracking and warfighter support.

L3Harris Technologies is a global aerospace and defense technology company offering mission-critical communication systems, space and airborne systems, ISR capabilities, and satellite communication ground systems. Its products include multi-mission terminals, ground station platforms, and advanced sensors for military and commercial applications. The Space & Mission Systems segment focuses on ground systems, payloads, and secure communications

-

In 2025: L3Harris expanded production at its Florida facility for next‑gen missile tracking satellites and is supporting SDA Tranche 1 & 2 systems, strengthening its space integration and ground support capabilities.

RTX Corporation is a leading American aerospace and defense conglomerate, integrating Collins Aerospace, Pratt & Whitney, and Raytheon Intelligence & Space. It delivers advanced avionics, secure communication systems, radar, and satellite ground station infrastructure for defense, intelligence, and space applications globally. RTX’s technologies support mission-critical satellite command, control, and communication networks with emphasis on AI, cybersecurity, and modular ground solutions.

-

In 2025: In 2025, RTX reported strong defense earnings with revenue growth driven by increased global defense spending and expanded capabilities across its aerospace and satellite systems divisions.

Satellite Ground Station Market Key Players:

-

General Dynamics Mission Systems

-

L3Harris Technologies

-

RTX (Raytheon Technologies)

-

Airbus Defence and Space

-

Lockheed Martin Corporation

-

Viasat Inc.

-

SES S.A.

-

Intelsat S.A.

-

Eutelsat Communications

-

Inmarsat Global Limited

-

Gilat Satellite Networks

-

Kratos Defense & Security Solutions

-

Comtech Telecommunications Corp.

-

Hughes Network Systems

-

Kongsberg Satellite Services (KSAT)

-

Amazon Web Services (AWS) Ground Station

-

Microsoft Azure Orbital

-

Leaf Space S.p.A.

-

Infostellar

-

Atlas Space Operations

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 61.71 Billion |

| Market Size by 2035 | USD 245.96 Billion |

| CAGR | CAGR of 14.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solutions : (Hardware, Software, Ground Station as a Service) • By Platform: (Fixed Ground Stations, Portable Ground Stations, On-the-Move Stations) •By Frequency Band: (C-Band, Ku-Band, Ka-Band) •By Application: (Communication, Earth Observation, Navigation & Positioning, Military & Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | General Dynamics Mission Systems, L3Harris Technologies, RTX (Raytheon Technologies), Airbus Defence and Space, Lockheed Martin Corporation, Viasat Inc., SES S.A., Intelsat S.A., Eutelsat Communications, Inmarsat Global Limited, Gilat Satellite Networks, Kratos Defense & Security Solutions, Comtech Telecommunications Corp., Hughes Network Systems, Kongsberg Satellite Services (KSAT), Amazon Web Services (AWS) Ground Station, Microsoft Azure Orbital, Leaf Space S.p.A., Infostellar, Atlas Space Operations |

Frequently Asked Questions

The Fixed Ground Stations segment dominated the Satellite Ground Station market, driven by high reliability, continuous satellite connectivity, and widespread deployment for commercial, defense, and government space operations.

North-America dominated the Satellite Ground Station market in 2025.

The key drivers of the Satellite Ground Station market are the rising satellite launches, demand for high-speed data services, defense and Earth observation needs, and growth of cloud-based ground station services.

The market was valued at USD 61.71 Billion in 2025 and is projected to reach USD 245.96 Billion by 2035.

The Satellite Ground Station market is expected to grow at a CAGR of 14.84% during 2026-2035.

Get in Touch