Advanced Air Mobility (AAM) Market Report Scope & Overview:

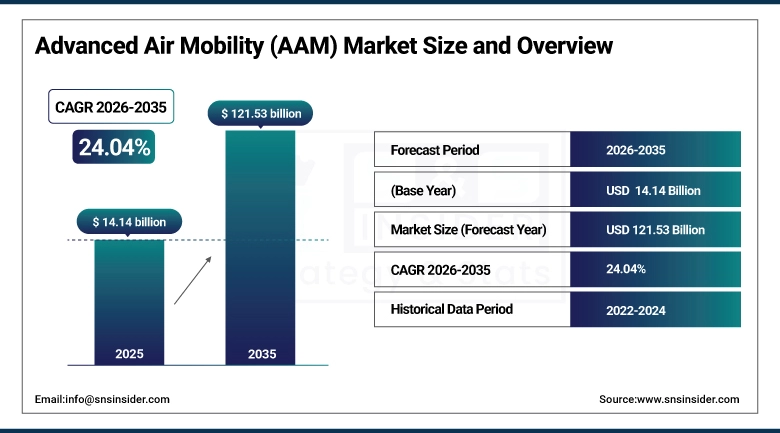

The Advanced Air Mobility (AAM) Market is valued at USD 14.14 billion in 2025 and is expected to reach USD 121.53 billion by 2035, growing at a CAGR of 24.04 % from 2026-2035.

The global Advanced Air Mobility (AAM) Market is projected to grow exponentially as demand for urban air transportation, air taxis, and cargo delivery solutions continues to rise. Especially with electric and hybrid-electric propulsion, autonomous flight systems and vertical takeoff and landing (VTOL) aircraft, technological advancements are quickly expediting the process of integration. Furthermore, increasing investments by aerospace companies, supportive regulatory frameworks, and the efforts to boost sustainable and congestion-free urban mobility are some of the major factors contributing to the growth of the market worldwide. The increasing interest in airspace integration and the development of smart cities is another factor driving the demand for AAM solutions over the forecast period.

89% of global AAM growth was driven by urban air taxi and cargo demand, accelerated by eVTOL innovation, smart city integration, and supportive regulations promoting sustainable, congestion-free mobility.

Advanced Air Mobility (AAM) Market Size and Forecast

-

Market Size in 2025: USD 14.14 Billion

-

Market Size by 2035: USD 121.53 Billion

-

CAGR: 24.04 % from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Advanced Air Mobility (AAM) Market - Request Free Sample Report

Advanced Air Mobility (AAM) Market Trends

-

Increasing investment in electric vertical takeoff and landing aircraft for urban air mobility and logistics applications

-

Steps Towards More Advanced Air Mobility Services The world over which means Faster time to market.

-

Increasing collaborations between aerospace manufacturers technology companies and mobility service providers to grow AAM ecosystems

-

Battery propulsion history and the proximity of autonomous flight systems which improve range safety and operational efficiency

-

Broadening of use cases such as air taxis cargo transport emergency medical services and regional connectivity

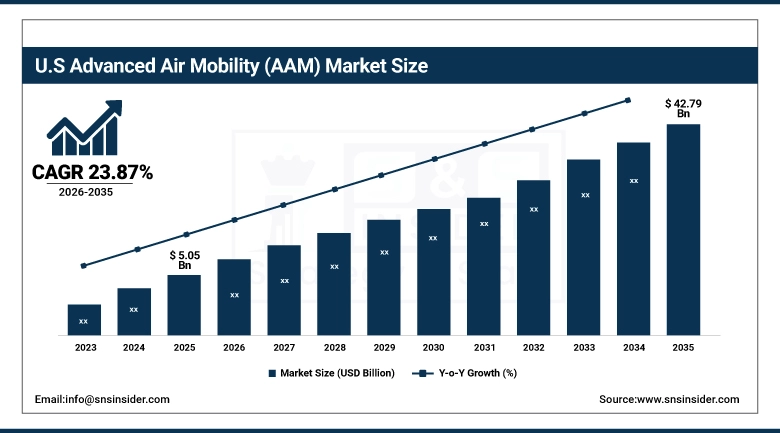

U.S. Advanced Air Mobility (AAM) Market is valued at USD 5.05 billion in 2025 and is expected to reach USD 42.79 billion by 2035, growing at a CAGR of 23.87 % from 2026-2035.

With a demand for urban air transportation, air taxi services and last mile cargo delivery growing rapidly the U.S. Advanced Air Mobility (AAM) Market is expanding. Electric and hybrid-electric propulsion, autonomous flight technology, and small vertical take-off and landing (VTOL) aircraft are accelerating adoption. FAA regulations and growing investments by aerospace companies and initiatives for sustainable and congestion-free urban mobility drive the market expansion.

Advanced Air Mobility (AAM) Market Growth Drivers:

-

Rising urban congestion and demand for faster, sustainable transportation solutions are accelerating investments in electric vertical takeoff and landing aircraft worldwide

Increasing urbanization and traffic congestion across major cities are driving the need for the alternative modes of transportation. AAM(eVTOL) is a form of urban mobility providing fast transit, with significantly lower environmental impact. Organizations and municipalities are pouring investments in advanced air mobility (AAM) solutions to shorten commuting links, lower carbon footprint, and provide greater efficiency and mobility. This has won over both private industry and the public sector alike and urban planners of all stripes who are trying to make our cities better places. These are the factors that are pushing massive investments and global adoption of AAM technologies.

87% of global eVTOL investments surged in response to urban congestion and demand for fast, sustainable urban air mobility solutions.

Advanced Air Mobility (AAM) Market Restraints:

-

High development costs, limited battery energy density, and infrastructure requirements challenge commercialization timelines and increase financial risks for AAM operators

AAM founders are not going to be cheap to read: extensive R&D, manufacturing and certification costs are going to go into building the actual AAM aircraft. Battery technologies today impose constraints on flight range, payload capacity, and turn-around time, limiting commercial applicability. There is also huge capital job for vertiports, charging structure, and maintenance garages. For large scale deployment, it can be infeasible for smaller companies to carry the costs of operation, and for investors, the financial risk is considerable due to uncertainty in both technology performance and market adaptation. Such hurdles can push out commercialization timetables and slow down market growth of AAM. Tackling these hurdles mean developing energy storage solutions, increasing economies of scale, and planning infrastructures so that operations can be done in a cost-effective and sustainable manner.

80% of AAM operators reported delayed commercialization and elevated financial risk due to high development costs, limited battery energy density, and insufficient vertiport infrastructure.

Advanced Air Mobility (AAM) Market Opportunities:

-

Technological advancements in electric propulsion, autonomous flight systems, and battery efficiency create opportunities to improve range, safety, and cost-effectiveness of AAM aircraft

Continuous advancements in electric propulsion systems, energy-dense batteries, and autonomous flight technology are changing the AAM landscape. Higher battery energy density enables larger flight ranges with greater payloads, while automated systems reduce operational risk and pilot reliance. Technological advancements of this sort can reduce costs to operate, extend the rate of acceptance and help to make urban air mobility a commercial success. Companies entering research or sophisticated prototypes can find first-mover opportunities here. In addition, ongoing advancements in technology will ensure compliance with safety regulations around the world, as well as open up new use cases across passenger transportation, cargo delivery, and emergency services, stimulating an enduring growth trajectory for the market.

86% of AAM aircraft leveraged breakthroughs in electric propulsion, autonomous flight, and battery efficiency to enhance range, safety, and operational affordability.

Advanced Air Mobility (AAM) Market Segment Highlights

-

By Vehicle Type: eVTOL aircraft led with 55% share, while STOL aircraft is the fastest-growing segment.

-

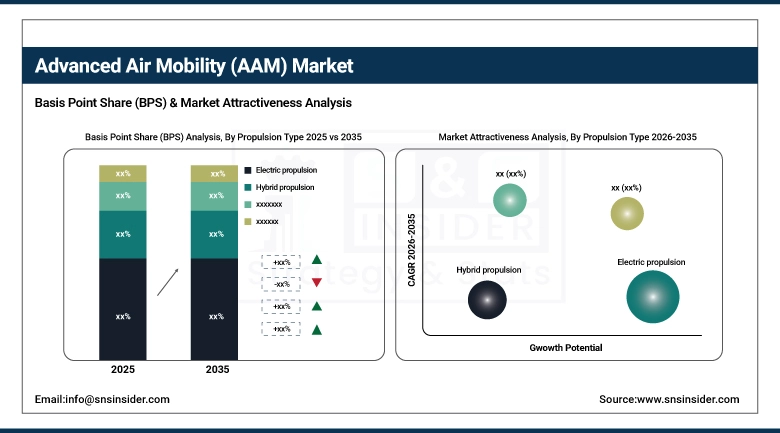

By Propulsion Type: Electric propulsion led with 48% share, while Hybrid propulsion is the fastest-growing segment.

-

By Operating Range: Short Range (Below 100 km) led with 52% share, while Medium Range (100–300 km) is the fastest-growing segment.

-

By Application: Urban Air Mobility (Air Taxis) led with 46% share, while Cargo & Logistics is the fastest-growing segment.

-

By End User: Commercial Operators led with 41% share, while Logistics Service Providers is the fastest-growing segment.

Advanced Air Mobility (AAM) Market Segment Analysis

By Propulsion Type: Electric propulsion led, while Hybrid propulsion is the fastest-growing segment.

Electric propulsion is at the forefront in that sector, thanks to its green credentials, comparative cost efficiencies in actual operations, and natural fit with urban air mobility vehicles. They are equipped with battery-powered motors, which are quiet in operation and emit no local emissions, making them ideal for city operation. Extensive implementation drives for eVTOL airplanes and air taxi services consolidated chief in the market. Additions in battery density, power management, and regenerative systems also lead to more efficient operation. Key market share is being driven by the use of electric propulsion being the most preferred propulsion mode for the commercial Advanced Air Mobility (AAM) fleets.

Hybrid propulsion is the biggest growth area, due to the combination of electric motors and traditional engines for longer range, greater payload, and operational versatility. The growth is driven by the regional travel and cargo missions that will demand longer ranges than currently supported by purely electric solutions. Hybrid systems provide the possibility of reducing the weight of the battery used and making sure that the battery is used efficiently without losing performance. The combination of rising R&D investment and pilot programs for these systems along with government incentives to reduce carbon emissions has led to rapid adoption and a growing place for hybrid propulsion as a high-growth technology within the AAM sectors.

By Vehicle Type: eVTOL aircraft led, while STOL aircraft is the fastest-growing segment.

eVTOL aircraft represent the majority of AAM, as they can vertically take off and land without requiring much space, making them suitable for densley populated urban environments. They also help to lessen infrastructure dependence, allow for air taxi services to operate point-to-point and more and more commercial operators are adopting them. This efficiency and safety gained from using lightweight materials, autonomous flight systems, and advanced battery technology. Strong interest from city transport authorities and private operators means it will be everywhere. eVTOLs accounted for the bulk of the revenue in the market, and the focus of uAM programs in many nations across the globe.

Due to the capability of their operations from shorter runways STOL aircraft are more flexible when it comes to regional transportation and cargo applicability, thus representing the fastest growing segment. They can land at smaller airports and semi-remote area, allowing them to support logistics and emergency services. Market growth is driven, rising demand for inter-city travel, cargo delivery, hybrid-electric propulsion adoption and also due to increase activity in urban air mobility. This drive, combined with technological advances in fuel efficiency, noise reduction, and modular designs make STOL aircraft a natural fit within the fastest-growing segment of the AAM market.

By Operating Range: Short Range led, while Medium Range is the fastest-growing segment

This makes short-range AAM operations the dominant method for air taxi services as they are ideally suited for urban services. Allow fast, short-distance travel in cities without needing massive infrastructure. Domination is driven by high adoption used by commercial operators, integration with eVTOL vehicles and has a business case based on some regulation of existing urban airspace. Short-haul applications are the biggest contributor to the market due to commuter efficiency, shorter travel periods, and functional safety.

Growth of the medium-range AAM has been the most notable and is primarily attributable to regional intercity travel, cargo logistics, and emergency services. The vehicle allows operators to reach beyond the boundaries of cities while still providing enough range for lower-density, suburban and interurban missions. All of which, with the combination of hybrid-electric propulsion and improved energy storage, are paving the way for accelerated adoption, supported by inclusion of regional air mobility into the primary government infrastructure planning strategies. The market will also be driven by increasing commercial routes and the demand for more efficient mid-range travel solutions.

By Application: Urban Air Mobility (Air Taxis) led, while Cargo & Logistics is the fastest-growing segment.

Urban where point-to-point transport is a tedious and long affair within a congested city and the demand for a quick solution will dominate Urban Air Mobility as well as (UAM), Air taxis can be integrated with the urban transit networks which tremendously reduces road congestion. The high stake in adoption from private operators, transport authorities and OEMs are bootstrapping investment in this space. This is why UAM is the top application segment for commercial services, preferably using eVTOLs with self-piloting and safety systems.

The cargo & logistics is the fastest growing application segment, which is driven by the need for rapid deliveries in urban and regional areas. The processing and marketing segment has shown a significant decline since 2019, as the Covid-19 pandemic disrupted food supply and processing chains. AAM lending itself well to pest management for large crop fields. Without significant software advancements, AAM application in agriculture will not be as extensive. It requires advanced intelligence in software and application and efficient spraying to reuse land for commercial use. AAM has facilitated the reincorporation of land into the economic system. Increases in the number of middle-class consumers and a focus on scientific sources of food have contributed to the segment’s growth.

By End User: Commercial Operators led, while Logistics Service Providers is the fastest-growing segment.

Commercial operators are ramped up investments building out air taxi networks, passenger service, and urban mobility programs. Integrating eVTOL fleets with digital and booking platforms as well as, compliance arms. Ample capital availability and strong partnerships with OEMs guarantee rapid adoption. The early adoption of urban air mobility solutions by commercial operators is keeping them as the largest end-user segment within the AAM market.

The logistics service providers represent the fastest-growing end-user segment, due to increasing demand for speedy and flexible transport of cargo. Contribution of integration of eVTOL and STOL aircraft for parcels delivery, medical supplies, and fundamental goods bolsters expansion Hybrid and electric propulsion systems are being adopted by providers to maximize operational range while lowering capital and operational costs. With the expansion of urban and regional logistics networks, logistics service providers will be a fast growing segment in the AAM market and adoption will accelerate.

Advanced Air Mobility (AAM) Market Regional Analysis

North America Advanced Air Mobility (AAM) Market Insights:

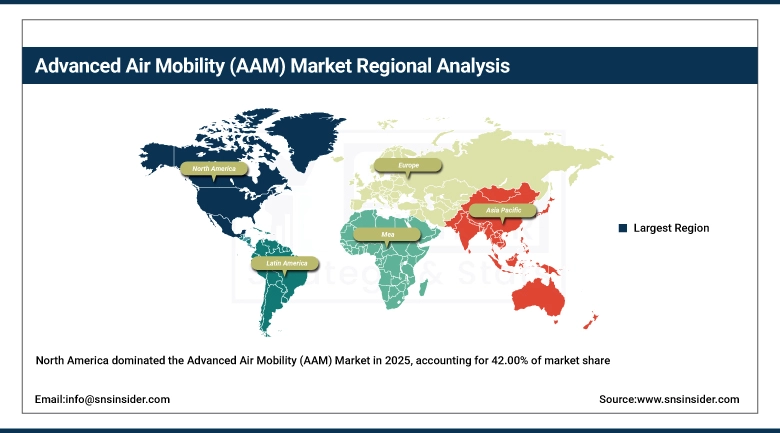

The Advanced Air Mobility (AAM) Market was led by North America with a 42.00% share of the AAM Market, owing to the presence of prominent eVTOL and aerospace manufacturers, developed aviation infrastructure, favorable regulatory environment, and heavy investment in urban air mobility projects in the region. The regional markets secured their leadership due to high technological adoption and government initiatives.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Advanced Air Mobility (AAM) Market Insights

Asia Pacific is anticipated to register the maximum CAGR of approximately 25.67% during the 2026–2035 forecast period, due to rapid urbanization, growing demand for efficient intra-city transport, and increasing investments in electric and hybrid aircraft technologies. Increase in aerospace manufacturing capabilities, supportive government towards smart city initiatives, and growing public acceptance towards air mobility solutions, all contribute to regional market growth.

Europe Advanced Air Mobility (AAM) Market Insights

Europe accounted for a major share of the Advanced Air Mobility (AAM) Market in 2025, due to favorable aerospace manufacturing landscape, robust regulatory process, and availability of investment in urban air mobility infrastructure. Sustainable aviation, regional integration of eVTOL technologies, and a favorable government-led environment ensured a solid market foundation for the region.

Middle East & Africa and Latin America Advanced Air Mobility (AAM) Market Insights

Steady AAM Market growth in 2025 in Middle East & Africa and Latin America together supported by urbanization, Investment in smart transportation solutions and demand for electric and hybrid air mobility technologies Brisk adoption across these regions is being led by expanding infrastructure, favorable regulatory policies and partnerships between local players and global aerospace players.

Advanced Air Mobility (AAM) Market Competitive Landscape:

Airbus S.A.S.

Airbus S.A.S. Airbus is a global leader in aerospace, but is currently developing the AAM market through its CityAirbus and Vahana eVTOL programs. Airbus is working on pioneering the safest and quietest as well as environmentally friendly air mobility solutions which support Urban Air Mobility. Utilising decades of aerospace experience, advanced avionics and autonomous flight technologies, the company is creating a family of eVTOL aircraft including passenger and cargo versions. Airbus also highlights regulatory preparedness, integration with the urban environment, and working with cities in fast tracking the deployment of advanced air mobility worldwide.

-

April 2025, Airbus S.A.S. launched the CityAirbus NextGen Evolution, an updated version of its all-electric vertical takeoff and landing (eVTOL) aircraft featuring extended range (80 km), enhanced battery thermal management, and a modular cabin for passenger or cargo configurations. The aircraft completed its first public demonstration flight in Toulouse, France, and is now undergoing EASA Type Certification with entry into service targeted for 2028 in partnership with ADAC Luftrettung for air medical services.

The Boeing Company (Wisk Aero & Aurora Flight Sciences)

Boeing, a major AAM competitor, holds stakes in Wisk Aero (in conjunction with its rival, the airframer Kitty Hawk) and Aurora Flight Sciences for the creation of these eVTOLs both autonomous and piloted across a spectrum of applications. Boeing Urban Air Mobility focuses on safe, sustainable and efficient solutions for urban air transportation. Its AAM initiatives are based on decades of aerospace engineering, advanced propulsion systems and autonomous flight technology. In working with regulators, municipalities and technology partners, Boeing intends to provide scalable, high-performance solutions that enable the transportation of passengers and cargo in the developing advanced air mobility ecosystem.

-

The Boeing Company, through its subsidiaries Wisk Aero and Aurora Flight Sciences, announced the successful completion of the first piloted test flights of the Wisk Cora Gen6 eVTOL at NASA’s Langley Research Center. The six-seat, self-flying aircraft features distributed electric propulsion, 90-minute endurance, and full autonomy under FAA Part 23 certification pathways. Boeing also confirmed a strategic collaboration with UPS Flight Forward to deploy Cora for urban cargo delivery starting in 2027.

Joby Aviation

Joby Aviation, a eVTOL aircraft manufacturer that will change the future of human air travel in urban areas The firm creates aircraft capable of vertical takeoff and landing, running on electricity for peaceful, secure, and eco-friendly event of passengers. In offering serial production-ready eVTOLs, Joby Aviation is primed for scalable urban air taxi services with an emphasis on performance, autonomy, and energy efficiency. It partners with Regulators, City Planners and Infrastructure Providers to expedite commercial adoption of these solutions and is fast filling the void, as a leader, for what will become the global Advanced Air Mobility market.

-

Joby Aviation received FAA Part 135 Air Carrier Certification, becoming the first eVTOL developer authorized to conduct commercial passenger and cargo operations in the U.S. The company simultaneously began construction of its pilot production facility in Marina, California, capable of building 50 aircraft per year by 2026. Joby also finalized a partnership with Toyota Tsusho to launch commercial air taxi services in Osaka, Japan, ahead of the 2026 World Expo.

Advanced Air Mobility (AAM) Market Key Players

Some of the Advanced Air Mobility (AAM) Market Companies

-

Airbus S.A.S.

-

The Boeing Company

-

Joby Aviation

-

Archer Aviation

-

Lilium GmbH

-

Volocopter GmbH

-

Guangzhou EHang Intelligent Technology Co. Ltd.

-

Vertical Aerospace Group Ltd.

-

Embraer S.A. (Eve Air Mobility)

-

Bell Textron Inc.

-

Hyundai (Supernal)

-

Beta Technologies

-

Pipistrel (Textron)

-

Neva Aerospace

-

Honda Motor Co. (eVTOL initiatives)

-

TCab Tech

-

Horizon Aircraft (New Horizon Aircraft Ltd.)

-

Sarla Aviation

-

Workhorse Group

-

Zipline

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.14 Billion |

| Market Size by 2035 | USD 121.53 Billion |

| CAGR | CAGR of 24.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vehicle Type: eVTOL (electric vertical takeoff and landing) aircraft, STOL (short takeoff and landing) aircraft, Conventional fixed-wing aircraft • By Propulsion Type: Gasoline, Turbine engines (turbo), Reciprocating (piston) engines, Electric propulsion, Hybrid propulsion • By Operating Range: Short Range (Below 100 km), Medium Range (100–300 km), Long Range (Above 300 km) • By Application: Urban Air Mobility (Air Taxis), Cargo & Logistics, Emergency Medical Services, Surveillance & Monitoring, Military & Government Operations • By End User: Commercial Operators, Logistics Service Providers, Government & Defense, Emergency Service Providers, Private Operators |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus S.A.S., The Boeing Company (via Wisk Aero & Aurora Flight Sciences), Joby Aviation, Archer Aviation, Lilium GmbH, Volocopter GmbH, Guangzhou EHang Intelligent Technology Co. Ltd., Vertical Aerospace Group Ltd., Embraer S.A. (Eve Air Mobility), Bell Textron Inc., Hyundai (Supernal), Beta Technologies, Pipistrel (Textron), Neva Aerospace, Honda Motor Co. (eVTOL initiatives), TCab Tech, Horizon Aircraft (New Horizon Aircraft Ltd.), Sarla Aviation, Workhorse Group, Zipline (AAM logistics) |

Frequently Asked Questions

The Advanced Air Mobility (AAM) Market is expected to grow at a CAGR of 24.04% from 2026 to 2035.

North America dominated the Advanced Air Mobility (AAM) Market in 2025.

Growth is driven by rising urban congestion, demand for faster and sustainable transportation solutions, adoption of eVTOL aircraft, and government-backed smart city initiatives.

The Advanced Air Mobility (AAM) Market was valued at USD 14.14 Billion in 2025.

Urban Air Mobility (Air Taxis) dominated the Advanced Air Mobility (AAM) Market.

Get in Touch