Logic Analyzer Market Report Scope & Overview:

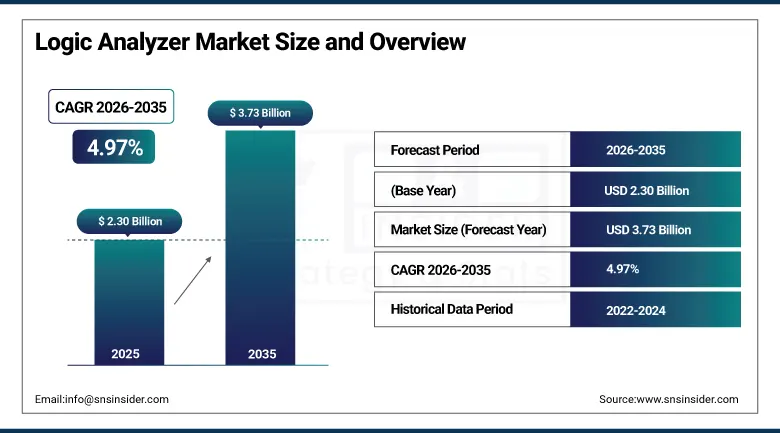

The Logic Analyzer Market size was valued at USD 2.30 Billion in 2025 and is expected to reach USD 3.73 Billion by 2035, growing at a CAGR of 4.97% from 2026–2035.

The global logic analyzer market is growing steadily, supported by rising demand for cloud-based logic analyzers, the influences of Industry 4.0 and IoT adoption, and trends towards energy efficiency and sustainability in electronic system design. Logic analyzers are essential electronic test and measurement instruments that capture, display, and decode multiple digital signal lines simultaneously, enabling hardware engineers and firmware developers to debug, validate, and analyses the timing relationships and protocol compliance of digital circuits, microcontrollers, FPGAs, and communication interfaces. Key factors driving the market growth include intense R&D efforts in semiconductor and electronics development, the proliferation of digital protocols requiring protocol decoding capability, and the growing complexity of embedded systems whose multi-channel signal interactions require comprehensive debug visibility.

In 2024, Keysight Technologies launched its enhanced 34-channel Logic Analyzer Series with integrated protocol decode libraries covering CAN FD, PCIe 4.0, and DDR5 interfaces, addressing automotive and computing electronics engineers’ requirements for high-speed serial protocol analysis alongside traditional parallel bus monitoring. The launch reflects the commercial direction of professional logic analyzer development toward multi-protocol software-defined instruments who’s flexible decode capability serves the diversity of modern embedded system debug challenges without requiring separate protocol-specific test equipment.

Market Size and Forecast

-

Market Size in 2026E: USD 2.41 Billion

-

Market Size by 2035: USD 3.73 Billion

-

CAGR: 4.97% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Logic Analyzer Market - Request Free Sample Report

Logic Analyzer Market Trends

-

Growing adoption of mixed-signal oscilloscopes with integrated logic analyzer functionality is enabling engineers to analyze analog and digital signals using a single platform

-

Cloud-enabled logic analyzer software and remote debugging capabilities are supporting collaboration among geographically distributed hardware development teams

-

Increasing popularity of PC-based USB logic analyzers is expanding access to professional-grade digital debugging tools among startups, educational institutions, and individual developers

-

Rising complexity of FPGA and SoC designs is driving demand for high-channel-count and deep-memory logic analyzers capable of advanced digital signal verification

-

Expanding use of automotive Ethernet, CAN FD, and other advanced communication protocols is increasing demand for logic analyzers with multi-protocol decoding and automotive electronics testing capabilities

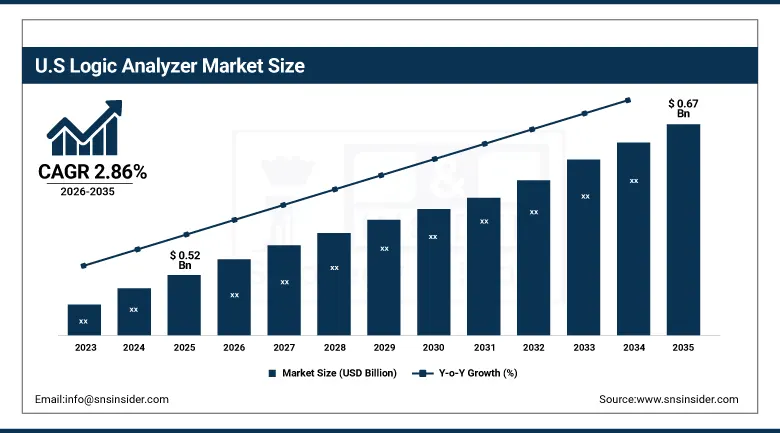

U.S. Logic Analyzer Market Size Outlook:

The U.S. Logic Analyzer Market was valued at approximately USD 0.52 Billion in 2025 and is expected to reach approximately USD 0.67 Billion by 2035, growing at a CAGR of approximately 2.86%.

The U.S. is the most commercially sophisticated logic analyzer market within North America's dominant revenue position. Keysight Technologies, Tektronix (Fortive), and Rohde & Schwarz’s U.S. commercial operations define the professional logic analyzer market standard. The semiconductor industry’s chip validation engineering, the aerospace and defense electronics development sector’s military communications protocol testing, and the automotive electronics engineering community’s embedded system debug collectively create the most commercially diverse logic analyzer application environment of any national market. The CHIPS Act-driven semiconductor manufacturing investment is simultaneously creating engineering talent growth whose test and measurement instrument procurement sustains above-average domestic commercial demand.

In 2023, Saleae released Logic 2.4 software for its USB logic analyzer series, featuring AI-assisted signal characterization that automatically identifies unknown protocol patterns in captured waveforms and suggests appropriate protocol decode configurations. The software release demonstrates the commercial direction of PC-hosted logic analyzer development toward AI-assisted workflow tools whose automated protocol identification reduces the domain expertise requirement for logic analyzer effective use, expanding the addressable market beyond specialist digital hardware engineers toward embedded software developers whose firmware debug requirements create growing logic analyzer adoption.

Logic Analyzer Market Segment Analysis

-

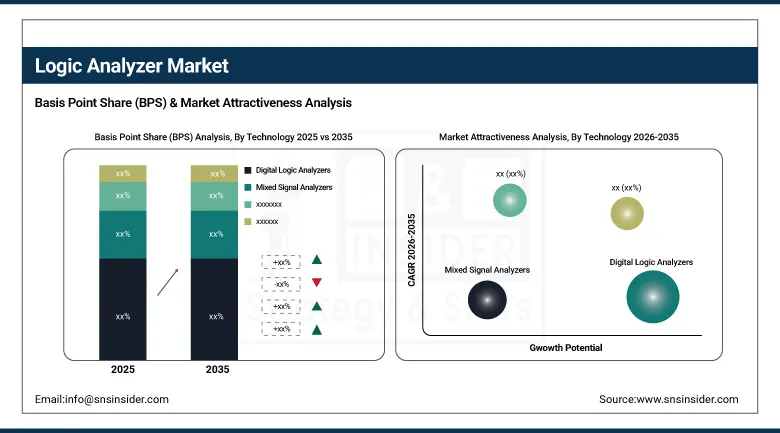

By Technology, the Digital Logic Analyzers segment dominated the Logic Analyzer Market with approximately 52% share in 2025, while the Mixed Signal Analyzers segment is the fastest growing.

-

By Application, the Automotive segment dominated the Logic Analyzer Market with approximately 28% share in 2025, while the Telecommunications segment is the fastest growing.

-

By End Use, the Research and Development segment dominated the Logic Analyzer Market with approximately 44% share in 2025, while the Manufacturing segment is the fastest growing.

-

By Channel, the Offline Sales/Distributors segment dominated the Logic Analyzer Market with approximately 58% share in 2025, while the Online Sales segment is the fastest growing.

By Technology, digital logic analyzers dominate, mixed signal grows fastest

Digital logic analyzers retained the dominant technology position with approximately 52% of the logic analyzer market in 2025. The standalone digital logic analyzer’s specialized capability for high-channel-count parallel bus capture, deep state memory for long protocol sequence capture, and comprehensive timing analysis at sampling rates up to 10 GHz creates an instrument performance envelope that mixed signal oscilloscope-integrated logic capability cannot match in demanding FPGA validation, parallel memory bus analysis, and high-channel-count embedded system debug applications. The professional digital logic analyzer’s established position in semiconductor validation laboratory and aerospace electronics testing environments sustains technology leadership through performance-critical application retention even as general-purpose alternatives gain share in less demanding applications.

Mixed signal analyzers are the fastest-growing technology because the growing prevalence of embedded systems whose design combines analog sensor interfaces with digital processing, power management ICs with digital communication protocols, and RF front-ends with digital baseband processing creates simultaneous analog and digital signal capture requirements that justify the mixed signal oscilloscope with integrated logic analyzer capability. Each automotive ECU design that combines analog sensor conditioning with CAN or Ethernet digital communication, and each IoT device that integrates analog environmental sensing with digital wireless protocol implementation, creates mixed signal capture demand that grows with embedded system design complexity.

By End Use, R&D dominates, manufacturing grows fastest

Research and development retained the dominant end-use position with approximately 44% of the logic analyzer market in 2025. The electronic design engineering community’s fundamental requirement for digital signal debug capability creates R&D as the most commercially concentrated logic analyzer demand category whose semiconductor design center, automotive electronics laboratory, and aerospace embedded system validation facility collectively sustain the highest per-organization instrument procurement intensity. Each new semiconductor product development programme, each FPGA-based system design project, and each automotive ECU firmware development effort creates logic analyzer procurement whose timeline spans the programme’s development and validation phases.

Manufacturing is the fastest-growing end use because automated board-level functional test systems, production line embedded protocol validation, and quality control communication interface verification are creating systematic logic analyzer integration in electronics manufacturing environments. Each new electronics manufacturing facility implementing Industry 4.0 automated test cell creates logic analyzer procurement whose per-facility scale compounds with the global electronics manufacturing investment pace. The shift toward automated flying probe and boundary scan test augmented with protocol-aware functional verification creates structured manufacturing-phase logic analyzer procurement that was historically confined to the R&D phase.

By Application, automotive dominates, telecom grows fastest

Automotive retained the dominant application position with approximately 28% of the logic analyzer market in 2025. The automotive sector’s extraordinary electronic content growth from ADAS, EV powertrain, and V2X communication systems creates an embedded system debug requirement whose multi-protocol complexity, encompassing CAN FD, Ethernet, LIN, FlexRay, and automotive-grade SPI/I2C interfaces simultaneously, creates comprehensive logic analyser specification. Each new automotive ECU development programme creates logic analyser procurement whose channel count, sampling rate, and automotive protocol decode requirements create above-average per-instrument commercial value relative to consumer electronics alternatives. The EV transition’s battery management system ASIL-functional-safety validation requirement creates additional logic analyser demand for verification of safety-critical communication integrity.

Telecommunications is the fastest-growing application because 5G infrastructure chipset development, next-generation mobile modem validation, and high-speed serial interface debug at PCIe 4.0 and DDR5 speeds create logic analyser procurement requirements at performance specifications that push instrument state-of-the-art. Each new 5G millimeter-wave chipset validation programme requiring simultaneous monitoring of multiple high-speed differential pairs creates premium high-speed logic analyser procurement. The AI chip interconnect’s HBM and NVLink interface debug requirements create additional above-average logic analyser procurement from the semiconductor design community’s most commercially intensive validation programmes.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

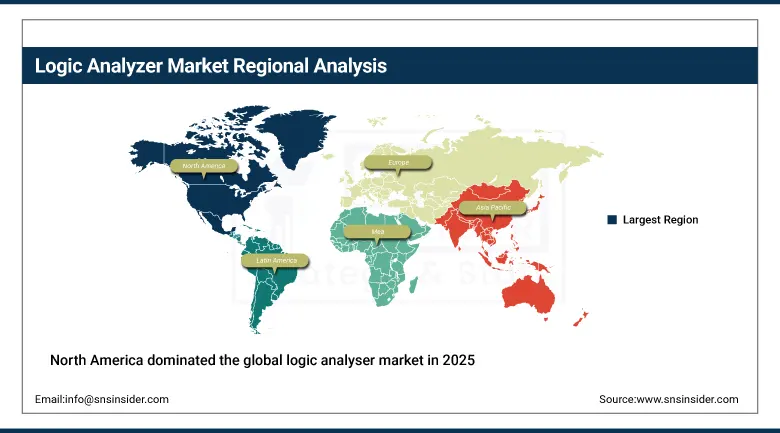

North America Logic Analyzer Market Insights

North America dominated the global logic analyser market in 2025 through Keysight Technologies’ and Tektronix’s commercial leadership, the semiconductor design center concentration in Silicon Valley, Austin, and Boston, and the aerospace and defense electronics validation laboratory infrastructure. The United States accounts for approximately 87.4% of North American revenues through its semiconductor industry’s chip validation engineering, the CHIPS Act investment creating new design capability, and the automotive electronics development community’s complex protocol debug requirements.

Canada contributes approximately 12.6% of North American revenues through its semiconductor design community, the telecommunications equipment industry’s protocol testing investment, and the university electronics engineering programme’s academic procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Logic Analyzer Market Insights

Europe is a technically sophisticated logic analyser market where the automotive electronics industry’s design validation, the aerospace sector’s avionics testing, and Rohde & Schwarz’s and PicoTechnology’s European commercial presence create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive OEM and Tier 1 supplier’s electronics validation investment, the industrial automation sector’s embedded debug requirement, and the industrial electronics manufacturing sector’s production test adoption.

The United Kingdom and Sweden are significant secondary markets where the aerospace electronics testing community, the telecommunications equipment development sector, and the academic research community’s embedded system teaching create consistent logic analyser demand.

Asia Pacific Logic Analyzer Market Insights

Asia Pacific is the fastest-growing regional logic analyser market, driven by China’s extraordinary semiconductor design expansion, Japan’s automotive electronics and robotics investment, South Korea’s Samsung and SK Hynix memory interface validation, and Taiwan’s TSMC customer ecosystem’s SoC validation infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its rapidly expanding semiconductor design center investment, the electronics manufacturing sector’s production test adoption, and the automotive electronics development community’s growing instrument procurement.

India represents an emerging secondary market where the growing semiconductor design center investment, the consumer electronics design community, and the automotive electronics engineering sector create above-average logic analyser market growth that compounds with India’s electronics industry development trajectory.

MEA & Latin America Logic Analyzer Market Insights

UAE leads MEA revenues at approximately 38.4% through its electronics design engineering community, the growing telecommunications infrastructure development sector, and the defense electronics testing investment creating structured logic analyser procurement. Saudi Arabia’s expanding technology sector and Israel’s semiconductor design community add significant secondary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its automotive electronics manufacturing sector, the Embraer aerospace avionics validation programme, and the telecommunications equipment industry’s embedded protocol debug requirements. South Africa’s electronics engineering programmes and Mexico’s automotive electronics manufacturing collectively sustain growing regional market development through 2035.

Market Dynamics

Growth Drivers: Semiconductor design complexity and automotive electronics multi-protocol validation creating structured procurement

Semiconductor design complexity’s exponential growth is the logic analyser market’s most commercially reliable structural demand driver. Each successive SoC generation whose transistor count doubles creates proportionally more complex debug requirements whose signal interaction visibility demands logic analyser channel count, sampling rate, and protocol decode capability above predecessor instrument specifications. The AI processor’s HBM memory interface, PCIe 4.0/5.0 connectivity, and Ethernet fabric create simultaneous high-speed protocol debug requirements whose combined specification creates premium logic analyser procurement from the semiconductor industry’s most commercially intensive validation programme’s.

Automotive electronics multi-protocol validation is creating structured logic analyser demand as EV and ADAS system complexity multiplies the number of communication protocols simultaneously operating in a single vehicle from the handful present in conventional ICE vehicles to dozens in advanced EV platforms. Each automotive electronics debug session requiring simultaneous CAN FD, Automotive Ethernet, and high-speed SPI monitoring creates logic analyser specification motivation whose commercial aggregate grows with vehicle electronic content expansion.

Restraints: Competition from mixed signal oscilloscopes and declining general-purpose instrument ASP

Mixed signal oscilloscopes with integrated logic analyser channels create competitive pressure from Keysight, Tektronix, and Rohde & Schwarz instrument platforms whose single-box combined capability eliminates the need for separate oscilloscope and logic analyser in mixed-signal debug workflows. Each engineering team that specifies a mixed signal oscilloscope as its primary bench instrument creates budget displacement that moderates standalone logic analyser procurement in environments where mixed signal capability satisfies the debug requirement.

PC-hosted USB logic analyzer’s competitive pricing pressure on mid-range bench instrument ASP creates revenue per unit compression as Saleae and similar platforms’ sub-USD-500 hardware combined with powerful software capture grows share in educational and startup segments that professional bench instruments previously served at higher ASPs.

Opportunities: Cloud-based logic analyser and 5G protocol validation instruments

Cloud-based logic analyser capability enabling remote instrument access, shared waveform database, and distributed team collaboration represents the most commercially innovative near-term market development whose subscription service model creates recurring revenue independent of hardware replacement cycles. Each engineering team distributed across multiple geographic locations that adopts cloud logic analyser collaboration creates above-hardware procurement motivation that sustains service revenue growth.

5G and next-generation wireless protocol validation represents the most commercially premium near-term application growth whose millimeter-wave protocol timing analysis and NR physical layer debug create instrument performance requirements that sustain premium professional logic analyser procurement from the telecommunications semiconductor design community.

Recent Developments:

-

2024: Keysight Technologies launched an enhanced 34-channel Logic Analyzer Series in 2024 with integrated protocol decode libraries covering CAN FD, PCIe 4.0, and DDR5 interfaces, addressing automotive and computing electronics engineers’ high-speed serial protocol analysis requirements.

-

2024: Tektronix launched the MSO2 Series mixed signal oscilloscope with expanded 16-channel digital logic analyser integration in 2024, providing automotive and industrial electronics engineers with combined analog and digital signal debug capability in a single bench instrument platform.

-

2024: Rohde & Schwarz introduced enhanced automotive bus protocol decode capabilities for its MXO 4 oscilloscope logic analyser channels in 2024, covering CAN XL, automotive Ethernet 1000BASE-T1, and next-generation automotive serial protocols targeting the automotive electronics verification market.

-

2023: Saleae released Logic 2.4 software in 2023 for its USB logic analyser series featuring AI-assisted signal characterization that automatically identifies unknown protocol patterns in captured waveforms and suggests appropriate protocol decode configurations, expanding effective user accessibility.

-

2023: PicoTechnology launched the PicoScope 2000E Series USB oscilloscope with integrated 16-channel logic analyser capability in 2023, providing embedded system developers with affordable mixed signal debug capability whose PC-hosted software architecture enables field and laboratory deployment flexibility.

Logic Analyzer Companies are:

-

Keysight Technologies Inc.

-

Rohde & Schwarz GmbH & Co. KG

-

Yokogawa Electric Corporation

-

Rigol Technologies Inc.

-

Anritsu Corporation

-

Siglent Technologies Co. Ltd.

-

Saleae Inc.

-

Logic Port

-

Digilent Inc.

-

Analog Devices Inc. (ADI)

-

Texas Instruments Incorporated

-

Synopsys Inc.

-

ZTEC Instruments Inc.

-

Lauterbach GmbH

-

Zeroplus Technology Co. Ltd.

-

Byte Paradigm

-

Novatek Microelectronics Corp.

-

Oscium LLC

Logic Analyzer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.30 Billion |

| Market Size by 2035 | USD 3.73 Billion |

| CAGR | CAGR of 4.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Technology (Digital Logic Analyzers, Mixed Signal Analyzers, Analog Logic Analyzers) • by Channel (Online Sales, Offline Sales, Distributors, Value-Added Resellers) • by Application (Automotive, Consumer Electronics, Telecommunications, Aerospace, Industrial Automation) • by End Use (Research and Development, Manufacturing, Maintenance and Repair, Education and Training) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Keysight Technologies Inc., Tektronix Inc., Rohde & Schwarz GmbH & Co. KG, Yokogawa, Electric Corporation, Rigol Technologies Inc., Anritsu Corporation, Siglent Technologies Co. Ltd., PicoTechnology Ltd., Saleae Inc., Logic Port, Digilent Inc., Analog Devices Inc. (ADI), Texas Instruments Incorporated, Synopsys Inc., ZTEC Instruments Inc., Lauterbach GmbH, Zeroplus Technology Co. Ltd., Byte Paradigm, Novatek Microelectronics Corp., Oscium LLC. |

Frequently Asked Questions

The Logic Analyzer Market is expected to grow at a CAGR of 4.97% from 2026 to 2035.

The Logic Analyzer Market was valued at USD 2.30 Billion in 2025.

Rising semiconductor design complexity creating high-channel-count and high-speed protocol debug requirements, and automotive electronics multi-protocol validation demand from EV and ADAS system complexity creating structured logic analyzer procurement across automotive design engineering organizations.

Digital Logic Analyzers dominated the Logic Analyzer Market with approximately 52% share in 2025, while Mixed Signal Analyzers is the fastest growing segment.

North America dominated the Logic Analyzer Market in 2025, with the United States accounting for approximately 87.4% of North American revenues through semiconductor design center concentration and professional test equipment investment.

Get in Touch