AI in Computer Vision Market Report Scope & Overview:

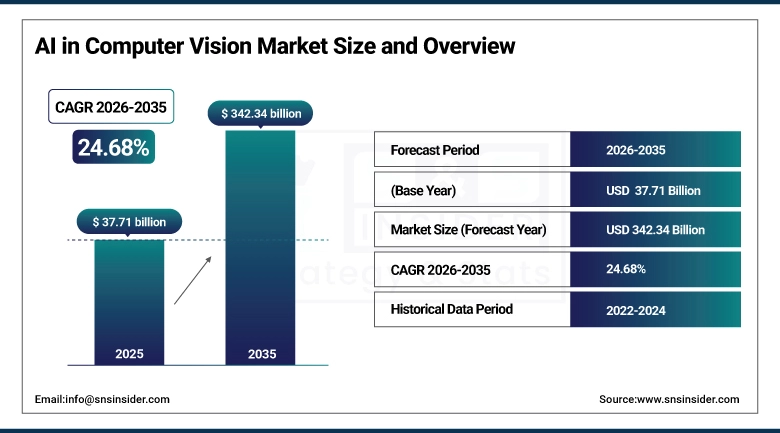

The AI in Computer Vision Market Size was valued at USD 37.71 billion in 2025 and is expected to reach USD 342.34 billion by 2035, growing at a CAGR of 24.68% from 2026-2035.

The growth in the Artificial Intelligence in Computer Vision Market is propelled by the fast adoption of AI-enabled image and video analytics solutions in sectors including health care, automobiles, retail, and security among others. The rising need for automation, facial recognition, autonomous cars, and quality inspection solutions is fueling the expansion of this market. The development of technologies such as deep learning, edge computing, and powerful GPUs is making the AI-based computer vision solutions more efficient in terms of performance.

Market Size and Growth Forecast:

-

AI in Computer Vision Market Size in 2025: USD 37.71 Billion

-

AI in Computer Vision Market Size by 2035: USD 342.34 Billion

-

CAGR: 24.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on AI in Computer Vision Market - Request Free Sample Report

AI in Computer Vision Market Trends

-

Rising demand for intelligent image and video analysis solutions is driving the AI in computer vision market.

-

Growing adoption across healthcare, automotive, retail, manufacturing, and security sectors is boosting market growth.

-

Expansion of autonomous systems, smart surveillance, and industrial automation is fueling deployment.

-

Increasing focus on real-time object detection, facial recognition, and predictive analytics is shaping adoption trends.

-

Advancements in deep learning, neural networks, edge AI, and GPU technologies are enhancing accuracy and processing efficiency.

-

Rising integration with IoT devices, cloud computing, and smart infrastructure is supporting market expansion.

-

Collaborations between AI developers, semiconductor companies, and industry solution providers are accelerating innovation and global adoption.

U.S. AI in Computer Vision Market Size Outlook:

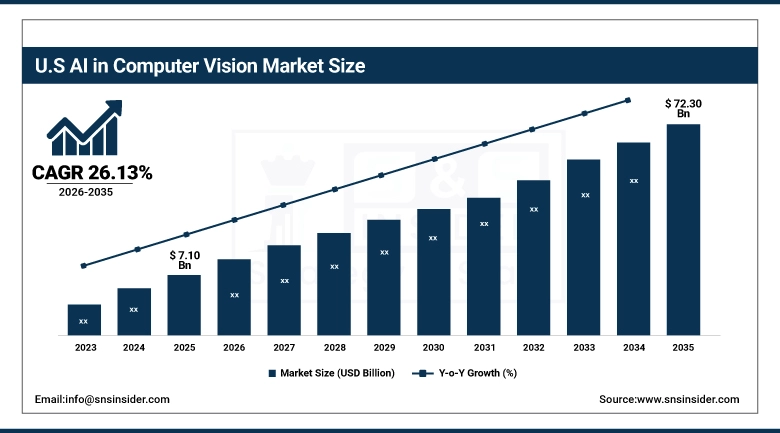

The U.S. AI in Computer Vision Market was valued at USD 7.10 billion in 2025 and is expected to reach USD 72.30 billion by 2035, growing at a CAGR of 26.13% from 2026-2035. U.S. AI in Computer Vision Industry Growth is fueled by growing deployment of AI-driven automation, self-driving cars, and sophisticated surveillance solutions. The increasing requirement for AI-based solutions in healthcare imaging, retail analysis, and manufacturing quality inspections, coupled with robust capital investments in AI frameworks and deep learning platforms, is fostering market growth at an accelerating rate.

AI in Computer Vision Market Segment Highlights

-

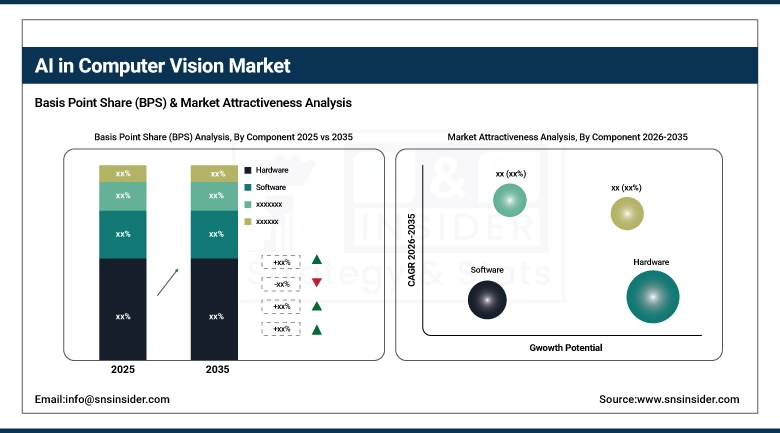

By Component, Hardware segment dominated the AI in Computer Vision Market in 2025 with 56% share; Software segment fastest growing (CAGR).

-

By Function, Training segment dominated the AI in Computer Vision Industry in 2025 with 62% share; Inference segment fastest growing (CAGR).

-

By Application, Industrial segment dominated the AI in Computer Vision Market in 2025 with 54% share; Non-industrial segment fastest growing (CAGR).

-

By End-use, Security and Surveillance segment dominated the AI in Computer Vision Industry in 2025 with 28% share; Healthcare segment fastest growing (CAGR).

By Component, Hardware segment dominates the AI in Computer Vision Market, Software segment expected to grow fastest

Hardware led the AI in Computer Vision Market in 2025 owing to the increasing requirement of GPUs, edge computing devices, cameras, sensors, and processors needed for image and video processing in real-time. These components of hardware play an essential role in developing computer vision technology that supports efficient image and video processing. The growing application of surveillance, industrial automation, and autonomous technologies has added to the dominance of the hardware segment across the globe.

The software segment is projected to be the fastest-growing segment owing to the increasing need for computer vision algorithms, AI frameworks, and cloud-based computer vision platforms. Innovations in deep learning models, image recognition software, and analysis have fueled the adoption rate in various industries. The rising necessity for flexible, scalable, and economical AI solutions coupled with the expanding scope of computer vision in businesses is anticipated to boost growth in the software segment.

By Function, Training segment dominates the AI in Computer Vision Market, Inference segment expected to grow fastest

The Training Segment led the AI in Computer Vision Market in 2025 because of the high computational needs associated with model training, data processing, and algorithm optimization. Training is an important process in ensuring the ability of computer vision systems to identify images, recognize objects, and predict outcomes. Increased investment in model training, datasets, and computational infrastructure will continue to fuel the Training Segment in this industry.

The Inference segment is the most rapidly growing market segment owing to its increased application in deployed computer vision technology across applications like autonomous cars, facial recognition software, and industrial inspection machines. There is a significant demand for inferencing capabilities in edge AI, fast decision making, and real-time analysis, which fuels rapid adoption. Growth in the inferencing process was also fueled by increased application of computer vision in mobiles, cameras, and IoT solutions.

By Application, Industrial segment dominates the AI in Computer Vision Industry, Non-industrial segment expected to grow fastest

The Industrial segment held the largest share of the AI in Computer Vision Market in 2025 owing to extensive use in automation, quality control, predictive maintenance, and robotics in industries. Computer vision helps boost productivity and minimize mistakes while ensuring product quality within industrial settings. The growing use of Industry 4.0 technologies, automation, and deployment of AI on production lines has further reinforced the presence of industrial applications in the market.

The Non-industrial segment represents the fastest-growing segment driven by increasing implementation of computer vision in retail, healthcare, transportation, and smart cities. Growing use of facial recognition, medical image processing, traffic surveillance, and customer behavior tracking is contributing to its rapid expansion. Technological advancements in AI and increasing digitization in the services sector are key drivers behind the global growth of non-industrial applications.

By End-use, Security & Surveillance segment dominates the AI in Computer Vision Industry, Healthcare segment expected to grow fastest

Security & Surveillance segment dominated the AI in Computer Vision Market in 2025 owing to widespread use of facial recognition systems, video analytics, and smart monitoring applications. Governmental organizations, enterprises, and infrastructure organizations are gradually opting for intelligent surveillance systems using AI technology for ensuring safety and preventing security-related threats. Rising awareness on the part of governments to prevent crime and ensure safety is aiding in bolstering the segment's position in the market.

The Healthcare Segment is the Fastest Growing on account of Increased Adoption of Computer Vision for Medical Imaging, Diagnosis, Surgery, and Patient Monitoring Applications. Vision technology driven by AI makes diagnosis more accurate, reduces the chances of human errors, and facilitates early disease detection. The increasing digitization of healthcare sector, along with increasing demand for sophisticated imaging solutions, is accelerating growth in this segment.

AI in Computer Vision Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88.2% |

|

Europe |

United Kingdom |

21.5% |

|

Asia Pacific |

Australia |

8.1% |

|

Middle East & Africa |

UAE |

17.9% |

|

Latin America |

Brazil |

50.6% |

North America AI in Computer Vision Market Insights

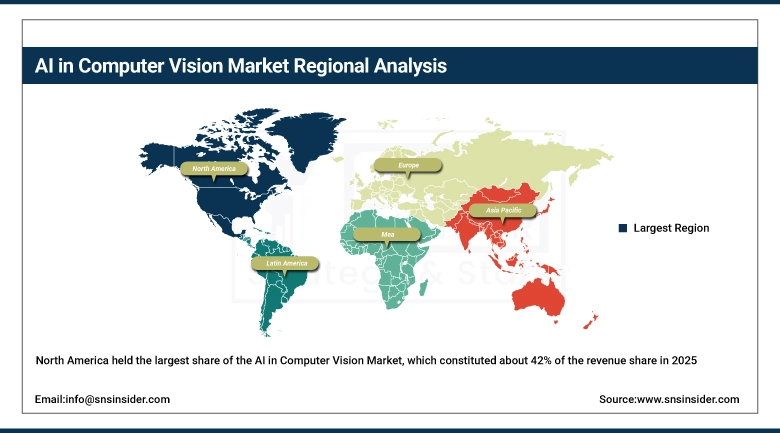

North America held the largest share of the AI in Computer Vision Market, which constituted about 42% of the revenue share in 2025. This market dominance in the region can be attributed to the high adoption rate of AI technologies, well-developed digital infrastructure, and heavy investments made in machine learning and computer vision solutions. Increasing demand in healthcare, automobiles, retail, and security segments will fuel market growth. The presence of top-tier tech firms, academic institutes, and AI start-ups will boost regional market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI in Computer Vision Market Insights

The Asia Pacific region is fast becoming the fastest-growing region in the AI in Computer Vision Market owing to the rapid digital transformation taking place and the increased use of artificial intelligence (AI) technologies in various sectors. Growth in the manufacturing industry, automobile sector, healthcare, and consumer electronics is boosting demand for computer vision systems. Investments in smart cities, surveillance applications, and industrial automation are propelling market growth in the region. Countries like China, Japan, South Korea, and India are making huge investments in AI and other related technology infrastructure.

Europe AI in Computer Vision Market Insights

The Europe AI in Computer Vision Market is experiencing steady growth owing to increased deployment of automation, smart surveillance systems, and industrial robots in many industries. The high level of attention being given to concepts such as Industry 4.0, digitalization, and manufacturing technology innovations are leading to high demands for AI-based computer vision systems. Increasing applications of AI in computer vision for automobile safety systems, diagnostics in healthcare, and analysis in retail are further fueling the growth of the market.

Middle East & Africa and Latin America AI in Computer Vision Market Insights

The AI in Computer Vision Industry in Middle East & Africa and Latin America is growing steadily due to increased use of smart surveillance systems, security systems, and automated industrial systems. This growth can be attributed to various factors including the development of smart cities, development of infrastructure in the region, and increasing applications of AI in the retail and health sectors. Lack of technological infrastructure in addition to high costs is restricting adoption of the technology in some markets.

Market Growth Drivers: Rapid adoption of automation and smart vision systems across industries driving demand for AI-based image and video analytics solutions globally

Extensive use of automation in various industries like automobiles, manufacturing, healthcare, and retail is a key factor driving the growth in demand for AI in computer vision. Vision systems that have been integrated by businesses with intelligence capabilities can help improve efficiency, prevent mistakes, and make data-driven decisions. Increased use of machine vision in inspection, object detection, face recognition, and surveillance applications is also boosting growth in the market. Smart factory and Industry 4.0 initiatives enable deployment of computer vision systems powered by AI for predictive maintenance and optimizing manufacturing operations. The growing need for autonomous vehicles and robots is another aspect that is adding to the demand for computer vision solutions.

Market Restraints: High computational requirements and infrastructure costs limiting widespread deployment of advanced computer vision systems in small enterprises

High computational power requirements for training and deploying AI-based computer vision models significantly increase infrastructure costs. Advanced GPUs, edge devices, and cloud computing resources are essential for processing large volumes of image and video data, making implementation expensive for small and medium enterprises. Additionally, continuous model training and data labeling require substantial financial and technical resources. Integration with existing systems and maintenance of high-performance computing infrastructure further add to operational costs. These financial and technological barriers restrict widespread adoption of computer vision solutions, particularly in cost-sensitive industries and developing regions, despite growing demand for automation and intelligent analytics solutions.

Market Opportunities: Increasing integration of AI with edge computing and IoT devices creating new opportunities for real-time intelligent vision applications

Rapid integration of AI with edge computing and IoT devices is creating significant opportunities for computer vision applications. Edge-based processing enables real-time image and video analysis without relying on centralized cloud systems, reducing latency and improving efficiency. This is particularly valuable in autonomous vehicles, industrial automation, and smart surveillance systems. Growing deployment of IoT-enabled cameras and sensors is expanding data availability for AI-driven insights. Additionally, advancements in lightweight AI models are enabling deployment on edge devices with limited computing power. This convergence of technologies is opening new opportunities for scalable, real-time intelligent vision solutions across multiple industries globally.

Recent Developments:

-

2026: NVIDIA expanded its AI computer vision ecosystem in 2026 by advancing generative AI, edge vision platforms, and robotics-focused visual intelligence systems. The company strengthened real-time perception capabilities for autonomous systems, industrial automation, and next-generation smart manufacturing environments through its physical AI and robotics platforms.

-

2025: Google LLC expanded Gemini multimodal AI capabilities in 2025, improving computer vision performance for image understanding, real-time video analysis, and enterprise automation. The update supports visual search, healthcare imaging, and intelligent robotics applications globally.

-

2024: Microsoft Corporation expanded Azure AI Vision services in 2024 by introducing improved image recognition, facial analysis, object detection, and video intelligence capabilities. These upgrades strengthened enterprise adoption of computer vision for automation, surveillance, retail analytics, and smart infrastructure monitoring.

-

2023: SenseTime Group Limited expanded its AI computer vision deployments in 2023, launching upgraded smart city and surveillance solutions. The enhancements focused on transportation analytics, urban monitoring, and enterprise visual intelligence applications.

AI in Computer Vision Companies are:

-

Intel Corporation

-

Microsoft Corporation

-

Google LLC

-

Amazon Web Services (AWS)

-

IBM Corporation

-

Apple Inc.

-

Huawei Technologies Co. Ltd.

-

Samsung Electronics

-

Sony Corporation

-

Cognex Corporation

-

Basler AG

-

Teledyne Technologies Incorporated

-

Hikvision

-

Zebra Technologies Corporation

-

Omron Corporation

-

Xilinx (AMD)

-

Affectiva (Smart Eye AB)

-

SenseTime Group Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.71 Billion |

| Market Size by 2035 | USD 342.34 Billion |

| CAGR | CAGR of 24.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component-( Hardware , Software) • By Application- ( Industrial , Non-industrial ) • By Function- ( Training, Interference ) • By End-use- ( Automotive, Healthcare, Retail Security And Surveillance, Robotics And Machines, Consumer Electronics ) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA, Intel Corporation, Microsoft Corporation, Google LLC, Amazon Web Services (AWS), IBM Corporation, Apple Inc., Qualcomm Technologies Inc., Huawei Technologies Co. Ltd., Samsung Electronics, Sony Corporation, Cognex Corporation, Basler AG, Teledyne Technologies Incorporated, Hikvision, Zebra Technologies Corporation, Omron Corporation, Xilinx (AMD), Affectiva (Smart Eye AB), SenseTime Group Limited. |

Frequently Asked Questions

North America dominated the AI in Computer Vision Market in 2025.

The Hardware segment dominated the AI in Computer Vision Market in 2025.

The major growth factor of AI in the computer Vision Market is the increasing adoption of AI-powered visual systems in the healthcare, automotive, surveillance, and industrial automation sectors.

The AI in Computer Vision Market was valued at USD 37.71 billion in 2025.

The AI in Computer Vision Market is expected to grow at a CAGR of 24.68% from 2026 to 2035.

Get in Touch